[ad_1]

Coverage Heart for the New South

On January 28, each Argentina’s authorities and the Worldwide Financial Fund employees made bulletins about an understanding on new assist program. In the meantime, along with the fee of an amortization due on January 28, one other fee can also be anticipated within the first week of February. Each funds relate to the earlier package deal, accepted in 2018 and considerably disbursed thereafter. Non-payment might bitter relations at a crucial second for a brand new program to be accepted by the IMF’s board of govt administrators in time for disbursements to cowl bigger obligations due in March.

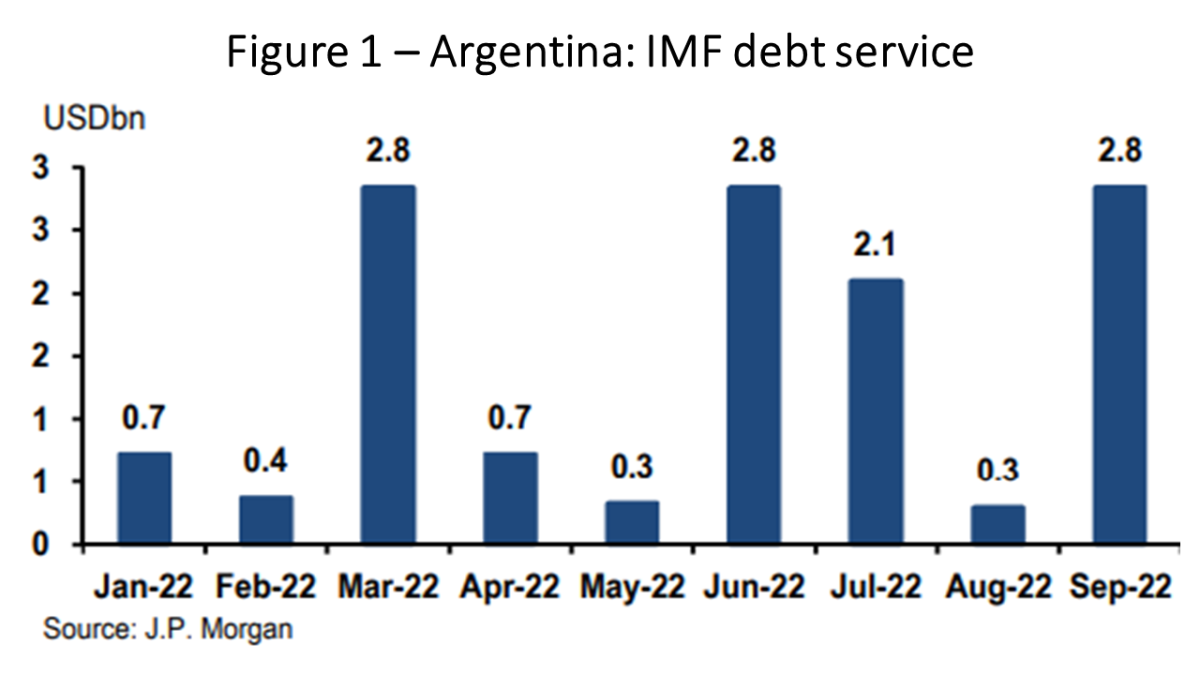

The present squeeze on Argentine international reserves is tight. If a brand new settlement just isn’t accepted, Argentina will hardly be capable to meet forthcoming funds to the IMF, because the quantities owed will improve sharply from March (Determine 1). A default with the IMF would even have penalties within the close to future for Argentina’s different exterior financing wants, since falling into arrears with the IMF would indicate a halt in disbursements from different multilaterals, in addition to interruption of commerce credit score strains.

It could even be unhealthy information for the IMF, provided that the package deal handed in 2018 was the largest in its historical past. As Argentina and the IMF want one another to keep away from catastrophic outcomes, it might not be stunning in the event that they find yourself discovering a compromise.

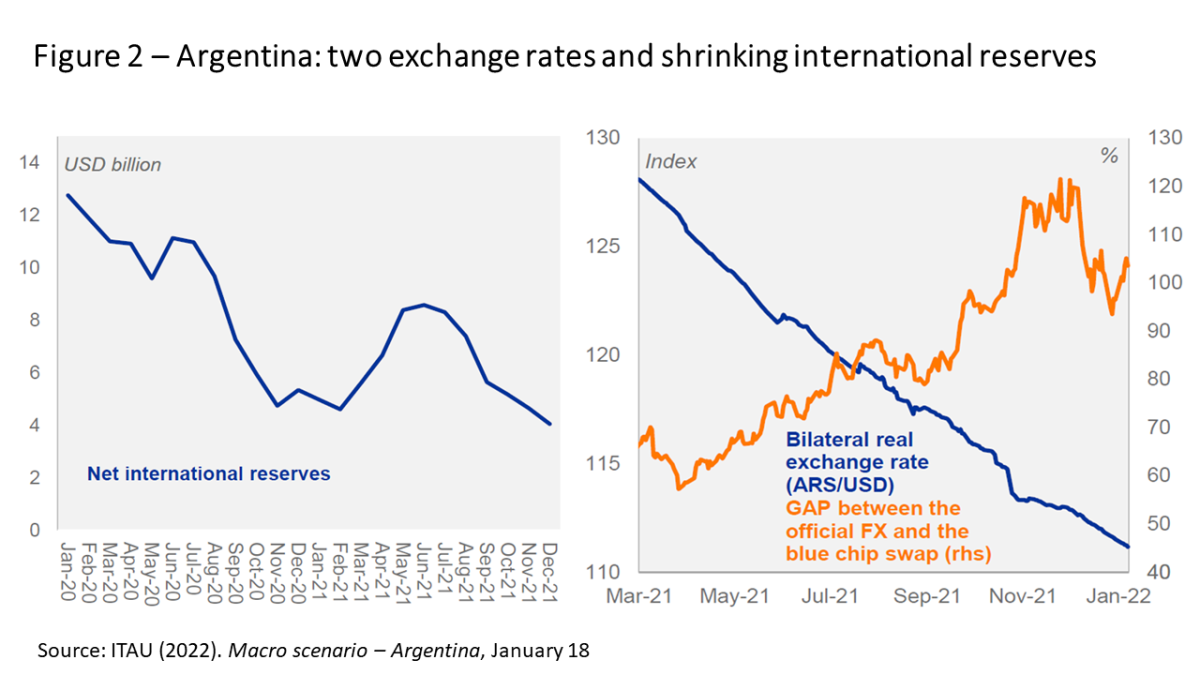

Administration of official and parallel alternate charges in Argentina has been draining the nation’s reserves, regardless of commerce surpluses, and the allocation of Particular Drawing Rights (SDRs) in the course of final yr. Central financial institution interventions within the alternate price market have led to a depletion of reserves (Determine 2, left panel).

An essential concern would be the kind and measurement of a brand new IMF program. Will the package deal underneath negotiation convey new options, or will it merely permit commitments to rollover the IMF debt service, kicking the can down the street?

There’s a distinction in context between now and 2018, when the earlier package deal was accepted. Then, the justification was boosting confidence and the entry of personal buyers. In apply, the assets ended up getting used to pay for capital outflows. Now it’s time to reimburse the IMF.

The kind of program to be accepted issues, by way of content material, measurement, and deadlines. The IMF has the Prolonged Fund Facility (EFF) for use when a rustic faces heavy medium-term balance-of-payments issues due to structural deficiencies that require time to resolve. In comparison with Stand-by Preparations (SBA), the EFF usually includes an extended program—to assist international locations implement medium-term structural reforms—and a correspondingly longer payback interval.

In precept, if this system is to be an EFF or an SBA is determined by the content material of the agreed insurance policies. An EFF requires extra structural adjustment in alternate for longer reimbursement deadlines. The 2018 settlement was an SBA, whereas in a January 28 press convention, Argentine Finance Minister Martin Guzmán referred to an EFF.

The IMF’s subsequent program is predicted to incorporate commitments to deal with the present disconnect between official alternate charges and inflation. The Argentine peso elevated in worth by 12% in actual phrases towards the greenback final yr, whereas the hole between official charges and the blue-chip swap charges has risen (Determine 2, proper panel). A fiscal adjustment to cut back deficit monetization—4.8% of GDP final yr—can even should be contemplated.

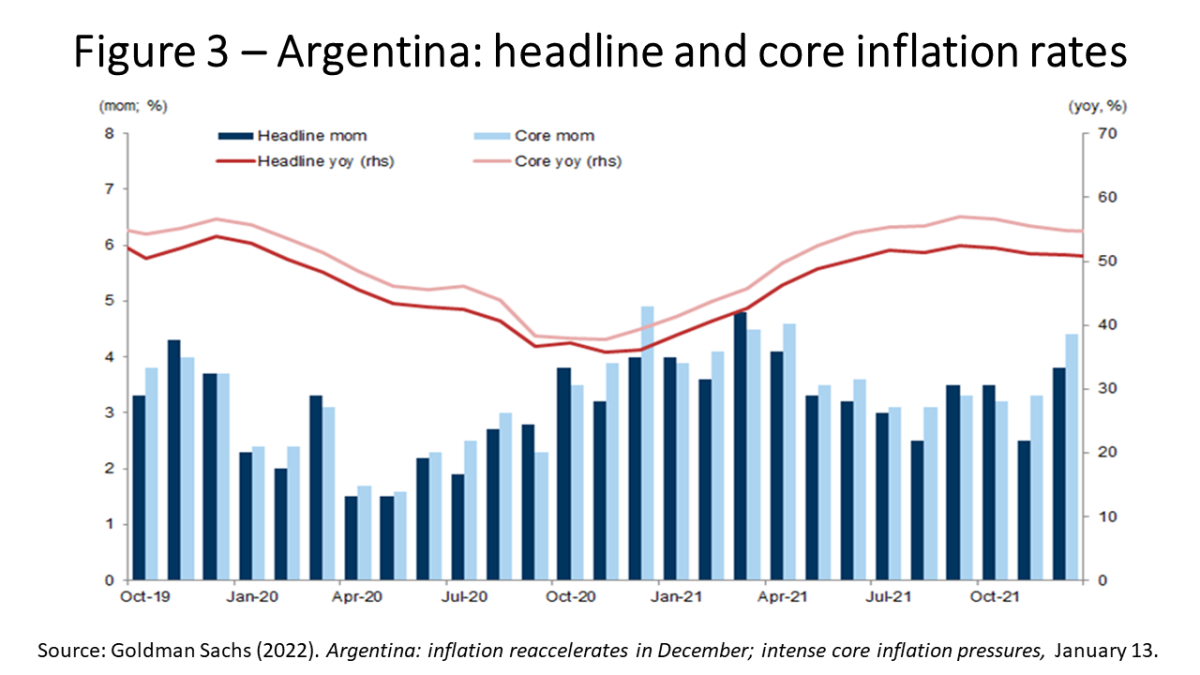

Progress won’t be simple on both entrance, as tackling excessive inflation (Determine 3) will imply resisting the monetization of public deficits, along with now not resorting to the shortcut of letting the official actual alternate price recognize as a means of attempting to include inflation.

In January 28 press convention, the Argentine minister offered some particulars of what, in his phrases, has already been agreed. Beneath the brand new program, the first fiscal deficit could be step by step decreased from 2.5% of GDP in 2022 to 1.9% of GDP in 2023 and 0.9% of GDP in 2024. Beneath this system, Argentina would decide to step by step cut back the central financial institution’s monetization of fiscal deficits: from 1% of GDP in 2022 to 0.6% in 2023, reaching one thing near zero in 2024. However “worth management agreements” with sellers/retailers would proceed as a part of the inflation management technique.

Minister Guzmán said that the brand new EFF program could be value $44.5 billion and would final two and a half years, whereas authorities would intend to extend reserves by $5 billion in 2022. Thus, the package deal would cowl each the amount of future amortizations with the IMF, in addition to what has been paid since September.

Authorities would anticipate to shut the deal by March, earlier than the massive principal fee is due. It ought to be famous, nevertheless, that the IMF employees communiqué says that “IMF employees and Argentine authorities reached an understanding on key insurance policies as a part of their ongoing discussions on an IMF-supported program.” Anybody who is aware of the language is aware of that which means there are nonetheless particulars to be finalized…

From the standpoint of evaluating the package deal, the main points can be essential: within the coverage conditionality matrix that can underpin this system and the trail of fiscal consolidation. Simply as difficult as offering a reputable dedication to affordable fiscal consolidation, can be addressing massive monetary-financial imbalances (e.g., a really misaligned alternate price, excessive inflation above 50% a yr, and monetary repression mechanisms that aren’t solely widespread, however more and more extra distorted). All the pieces signifies that the financial/monetary technique won’t be notably powerful.

It will likely be crucial to have a look at the trajectory of disbursements underneath the brand new program in relation to Argentina’s scheduled debt service funds to the IMF. A disbursement path forward of the debt service schedule would give Argentina new internet financing within the brief time period, however the IMF would threat seeing its already very excessive publicity to Argentina improve additional if this system goes off the rails.

Argentina’s gross exterior financing wants over the following three years are anticipated to be larger than the amortizations of the earlier IMF package deal, whereas different sources will stay scarce. The present account is at present in surplus, relieving funding strain. Nevertheless, sustaining strict restrictions on imports indefinitely doesn’t appear possible. It’s probably that even average present account deficits of 1.5%-2% of GDP in 2023 will create financing gaps if, as is probably going, assets underneath the brand new program are used particularly for the rollover of the present debt with the IMF itself, with out massive extra new liquid quantities.

For now, no less than Argentina’s default with the IMF has been prevented. The course forward will rely on IMF disbursements if targets are reached..

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]