[ad_1]

Coverage Middle for the New South PP-24-21

Introduction

The last decade after the Nice Monetary Disaster (GFC) of 2007–09 noticed important adjustments within the quantity and composition of capital flows within the world financial system. Portfolio investments and different non-bank monetary intermediaries (NBFIs) are behind an growing share of international capital flows, whereas banking flows have shrunk in relative phrases. This coverage paper research the implications of such a metamorphosis of finance for capital flows to rising market economies (EMEs).

Adjustments in capital flows accompanied structural shifts in monetary intermediation in capital-source nations, with NBFIs more and more shaping the demand for and provide of liquidity in monetary markets. The channels of systemic threat propagation have modified with the upper profile acquired by NBFIs, with leverage fluctuations by adjustments in margins rising in weight.

Dangers related to capital flows to EMEs have modified accordingly. Overseas capital probably brings advantages to rising market economies (EMEs). Nonetheless, extensive swings in capital flows carry excessive dangers to macroeconomic and monetary stability, together with the hostile results of sudden stops to capital inflows and challenges confronted by economies with weaker establishments and less-developed monetary markets.

Capital inflows in rising market economies are pushed by each world and country-specific drivers. The abundance of worldwide liquidity for the reason that GFC has pushed traders to seek for yield, with shifts in threat urge for food changing into a supply of fluctuations. However, adjustments within the macroeconomic fundamentals and institutional frameworks of EMEs have made traders extra selective.

The burden of worldwide components got here to the fore within the first half of 2020, when the monetary shock in superior economies brought on by coronavirus outbreaks led to a substantive wave of capital outflows from rising markets, with unprecedented pace and magnitude. The shock was mitigated subsequently by central banks’ counter-shock coverage strikes in supply nations, in addition to by EME coverage instruments in managing the dangers related to excessive shifts in capital flows.

This coverage paper first examines the metamorphosis of finance and of capital flows after the GFC, as much as the shock to capital flows to EMEs in the course of the 2020-21 coronavirus disaster. Then we analyze the extent to which a normalization of financial insurance policies in superior economies might result in shocks in these flows, in addition to why trade price fluctuations between the U.S. greenback and different main currencies can have an effect on capital flows to EMEs. Lastly, we assess the vary of coverage devices that EME policymakers are likely to resort to when managing dangers derived from capital-flow volatility.

1. The Metamorphosis of Finance

1.1 International Capital Flows After the GFC

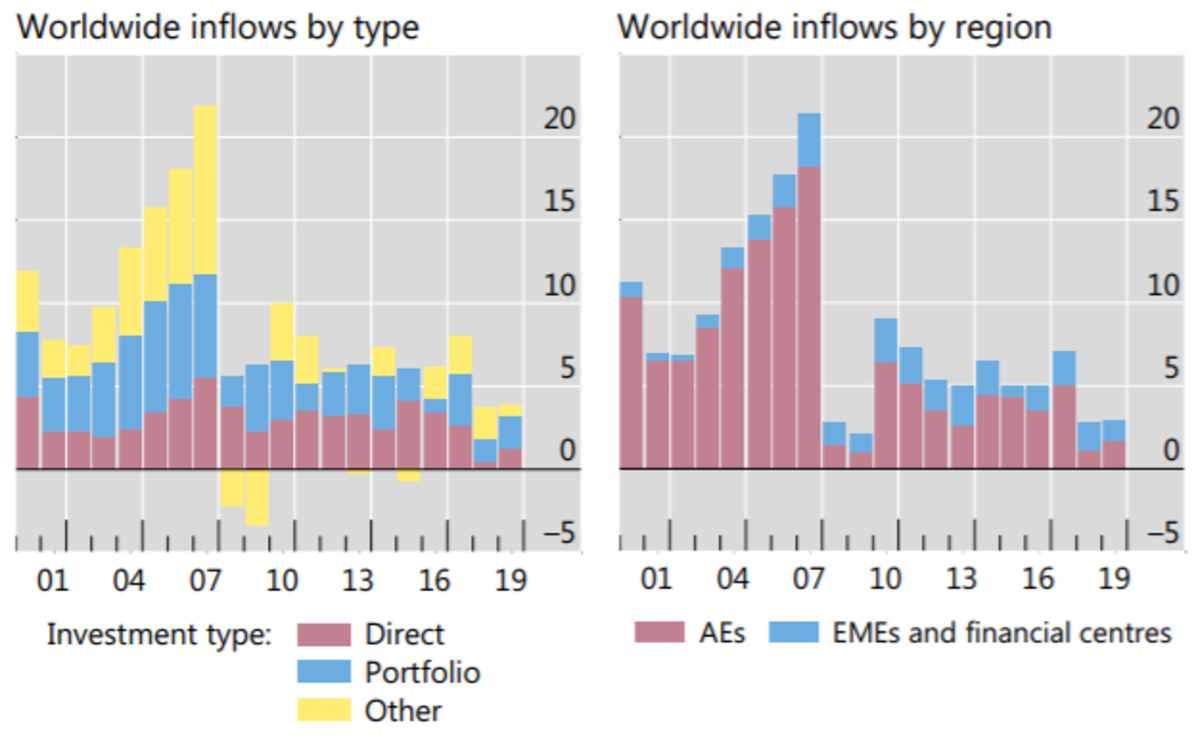

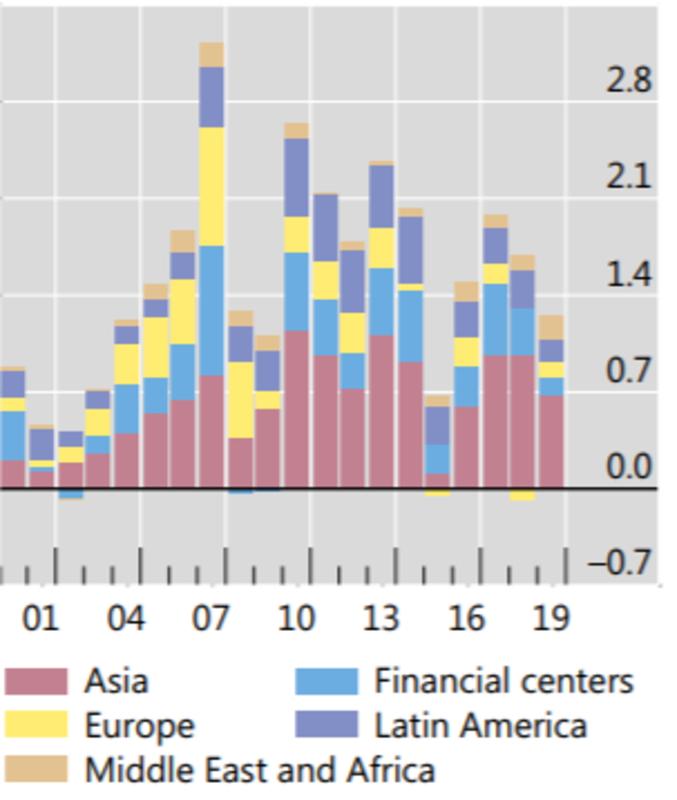

After a robust rising tide beginning within the Nineteen Nineties, gross capital flows reached a peak with the GFC. Determine 1 (left panel) exhibits how inflows rose quickly between 2002 and 2007, reaching US$12 trillion (near 22% of worldwide GDP). After falling steeply in the course of the GFC, flows have trended sideways, by no means recovering their pre-GFC upward momentum.

Determine 1: Capital Flows by Kind and Area (as % of world GDP)

Supply: BIS (2021).

As detailed in Canuto (2017) and BIS (2021), the last decade after the GFC (2007–09) introduced substantial adjustments each within the quantity and composition of worldwide capital flows. When one excludes the numerous flows to China, the quantity declined globally.

The general stabilization at decrease move ranges has taken place alongside a deep reshaping of cross-border monetary flows, that includes de-banking and an growing weight of non-banking cross-border monetary transactions. Sources of potential instability and long-term funding challenges have morphed accordingly.

The post-GFC descent in flows was pronounced for financial institution loans, that are categorised amongst ‘different’ funding flows in Determine 1 (left panel). Portfolio debt and fairness flows have been additionally decrease within the post-GFC interval, whereas international direct funding (FDI) maintained its power. Market-based sources of funding changed banks, whereas international participation within the native markets of EMEs grew. On the debtors’ aspect, banks have been additionally substituted by corporates and public-sector entities.

The U.S. greenback has remained the dominant foreign money for cross-border operations and investments, however the foreign money composition of flows has grow to be extra diversified. As we are going to talk about later, that has penalties for EMEs.

One other change in composition accompanied the decline in world flows after the GFC, particularly, a considerable decline in flows between superior economies, whereas EMEs grew to become extra distinguished as locations. Monetary globalization had primarily occurred amongst superior economies (AEs). Rising cross-border actions of economic property from the mid-Nineteen Nineties was exceptional amongst AEs. Ranges of economic openness (the sum of international property and liabilities as a proportion of GDP) relative to commerce openness (the sum of exports and imports as a proportion of GDP) have been comparable for each AEs and EMEs till the mid-Eighties, once they shifted upward within the case of AEs, rising quickly notably after the mid-Nineteen Nineties (Canuto, 2017). Cross-border monetary property and liabilities went from 135% to above 570% of GDP after mid-Nineteen Nineties for AEs, whereas they moved from roughly 100% to 180% of GDP for EMEs.

The post-GFC world development primarily displays adjustments in flows to AEs, which corresponded to 18% of world GDP in 2007, after which moved right down to under 7% after the GFC (Determine 1, proper panel). Flows to monetary facilities comprised a part of the development enhance earlier than 2007 however grew to become extra unstable between 2009 and 2019. Though the share of world GDP of property situated in monetary facilities declined, they’ve remained ascendant over the previous decade.

Such flows to monetary facilities have mirrored the monetary and tax methods of multinational enterprises, aimed toward minimizing prices and the tax burden. BIS (2021) referred to as it the “financialization of international direct funding (FDI).”

Additionally worthy of point out is the deeper regional integration amongst EMEs. That’s the case notably of EMEs as FDI and portfolio traders in different EMEs, despite the fact that AEs stay crucial funding sources in EMEs throughout all varieties of funding.

Some options of “the brand new dynamics of economic globalization” might deliver higher stability (McKinsey, 2017). Larger capital buffers and minimal quantities of liquid property have lowered the burden of financial institution lending and the intrinsic options of mismatch and volatility of banks’ steadiness sheets. The bigger share of fairness and FDI, in flip, might carry longer-term return horizons and nearer alignment of dangers between asset purchasers and originators. The unwinding of big debt-financed current-account imbalances attribute of the worldwide financial system within the run-up to the GFC has additionally contributed to such a view of worldwide finance coming into a extra secure section (Canuto, 2021b, ch.7).

However, as beforehand famous, flows of FDI partially correspond to disguised debt flows and/or transfers motivated by tax arbitrage or regulatory evasion. Cross-border debt flows—together with securities—in flip, are additionally delicate to world components, apart from being extremely delicate and procyclical with respect to monetary-financial circumstances in both supply and/or vacation spot nations.

There are additionally ‘blind spots’ left by de-banking, hitherto not preempted by non-banking monetary transactions. As an example, cross-border de-risking by world banks has entailed closure of correspondent banking relations in lots of nations, during which the paucity of options has led to detrimental penalties for native monetary dynamics (Canuto and Ramcharan, 2015). Moreover, the arms-length distance between asset holders and legal responsibility issuers intrinsic to debt securities and portfolio fairness, within the absence of the project-finance position performed prior to now by worldwide funding banks, usually constrains the cross-border financing of greenfield funding tasks.

Moreover, as we are going to see under, the rise of NBFIs and market-based intermediation has introduced a higher chance of, at instances of stress, liquidity/maturity transformation and leverage procyclicality, main NBFIs to a heightened ‘sprint for money’ and sudden will increase in demand for liquidity.

1.2. European Banks on the Core of Each Surge and Pause of the Wave of Monetary Globalization Because the Nineteen Nineties

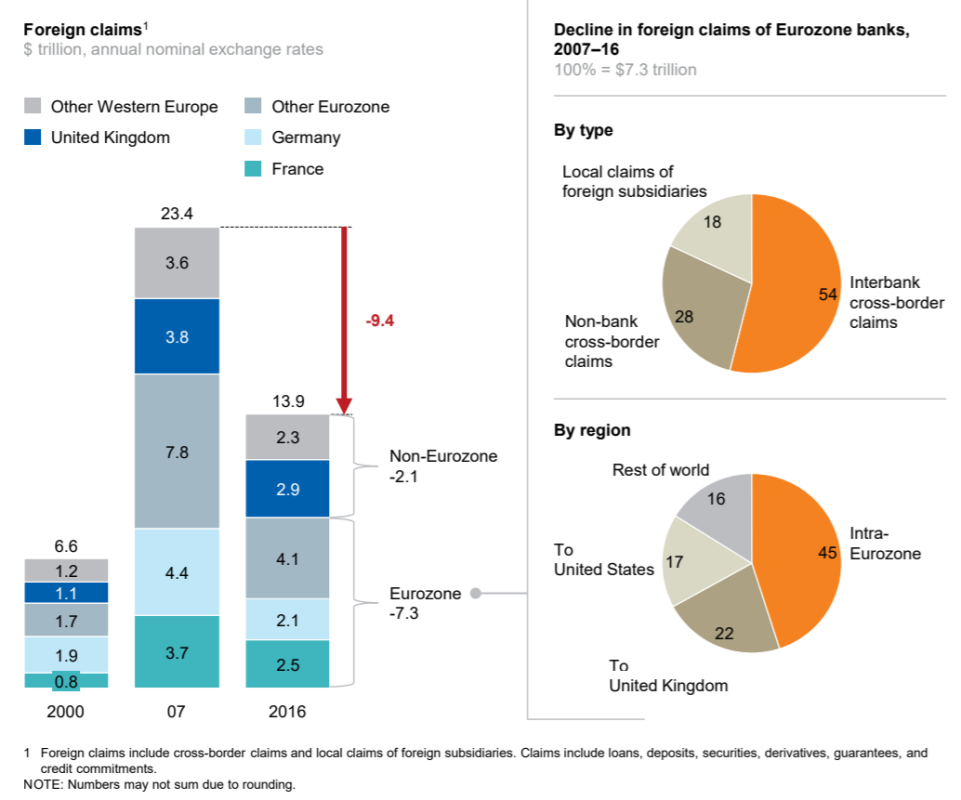

European banks have been on the core of each surge and pause of the wave of economic globalization for the reason that Nineteen Nineties. The substantial piling up of European banks’ international claims within the run as much as the GFC was adopted by an equally substantial retrenchment (McKinsey, 2017).

Determine 2 (left panel) exhibits this. From 2007 to 2016, Eurozone banks lowered their international claims by US$7.3 trillion, and different Western European banks lowered their international claims by US$2.1 trillion.

Determine 2: Eurozone Banks’ Overseas Claims (2000-2016)

Supply: McKinsey (2017).

Lending by European banks was behind two of the most important contributing components to the rising wave of economic globalization. First, the inauguration of the euro, which was adopted by markets initially converging their assessments of threat premiums throughout the zone downward towards German ranges, boosted cross-border transactions. Based on BIS (2017):

“Between 2001 and 2007, 23 proportion factors of the rise of the ratio of superior economies’ exterior liabilities to GDP was as a consequence of intra-euro space monetary transactions and one other 14 proportion factors to non-euro space nations’ monetary claims on the world (p.102).”

European banks additionally performed an energetic position within the asset bubble-blowing course of within the U.S. monetary system that preceded the GFC. European banks used U.S. wholesale funding markets to maintain exposures to U.S. debtors by the shadow banking system. Regardless of their small presence within the home U.S. industrial banking sector, their weight in total credit score circumstances was magnified by the shadow banking system in america that depends on capital market-based monetary intermediaries, which intermediate funds by securitization of claims (Shin, 2012).

From the standpoint of the balance-of-payments between the U.S. and Europe, these transactions netted out. Nonetheless, in an accounting sense they represented short-term borrowing mixed with long-term lending by European banks, with a corresponding double counting as cross-border monetary transactions.

The retrenchment of European banks’ international claims adopted each the U.S. asset-bubble burst beginning in 2007 and the Eurozone disaster from 2009 onward. Alongside business-driven causes—losses, selections to deleverage steadiness sheets—tighter banking regulation and the orientation towards home property assumed by post-crisis unconventional financial insurance policies additionally weighed. These components have additionally led to deleveraging, balance-sheet shrinking, and home reorientation by banks within the different crisis-affected AEs. Though some banks from exterior the latter have expanded their international lending, ranges of worldwide monetary openness have been maintained, due to rising flows of non-lending devices (debt securities, portfolio fairness, and FDI).

1.3. Morphing Monetary Intermediation in Superior Economies Behind the Metamorphosis of Capital Flows

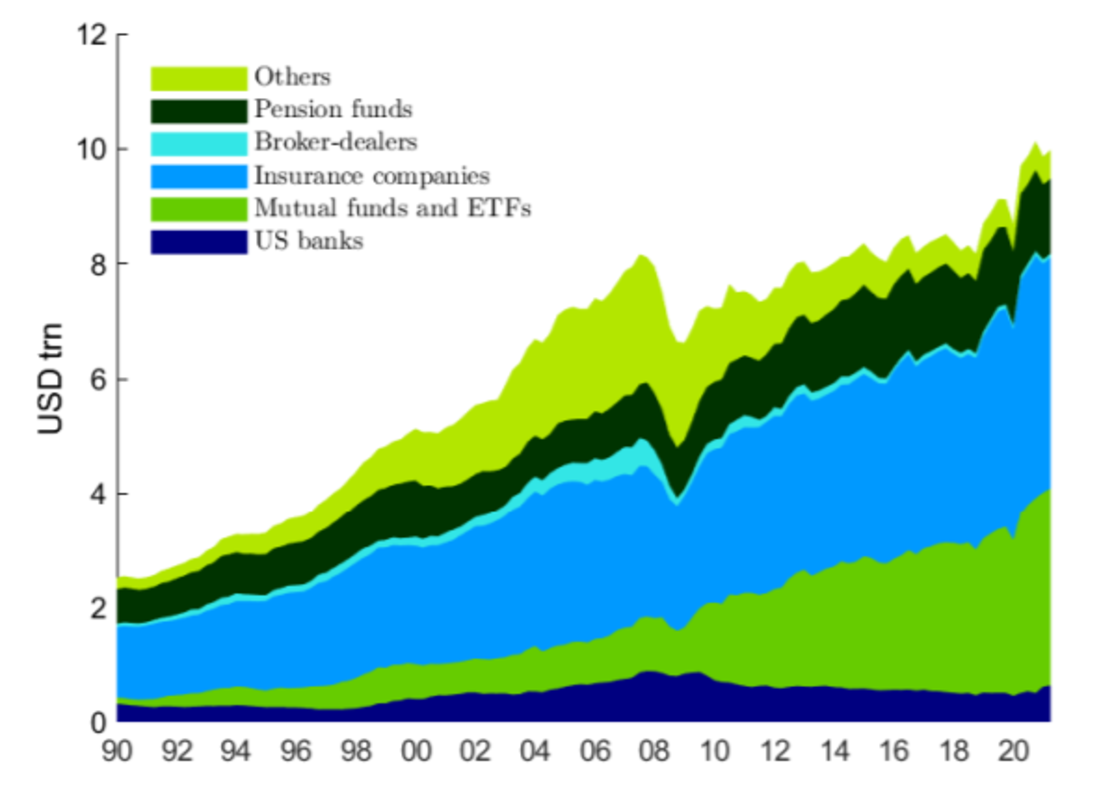

The metamorphosis of worldwide capital flows accompanied the evolution of market-based intermediation in superior economies, after the Nice Monetary Disaster of 2008, when the burden of NBFIs within the monetary system has risen. Banks—and their affiliated broker-dealers—stay an vital part of the mosaic, however they’re now a part of a broader set of establishments that route the move of funds and facilitate buying and selling. NBFIs have grow to be extra vital in debt intermediation, with implications for threat sharing within the monetary system.

Based on the Monetary Stability Board, NBFIs accounted in 2020 for about 50% of worldwide financing actions (FSB, 2020). Determine 3 shows the rise of NBFIs in financing U.S. company debt. Whereas, within the Eighties, banks funded about 30% of non-mortgage debt by loans, their share has fallen to 10%; market-based finance (bonds and industrial paper) now contains 65% of company debt. Mutual funds, insurance coverage corporations, and pension funds held virtually 80% of company and international bonds as of 2020, with a considerable enhance for mutual funds (Determine 3).

Determine 3: Holders of Company and Overseas Bonds Amongst U.S. Monetary Establishments

Supply: Aramonte et al (2021).

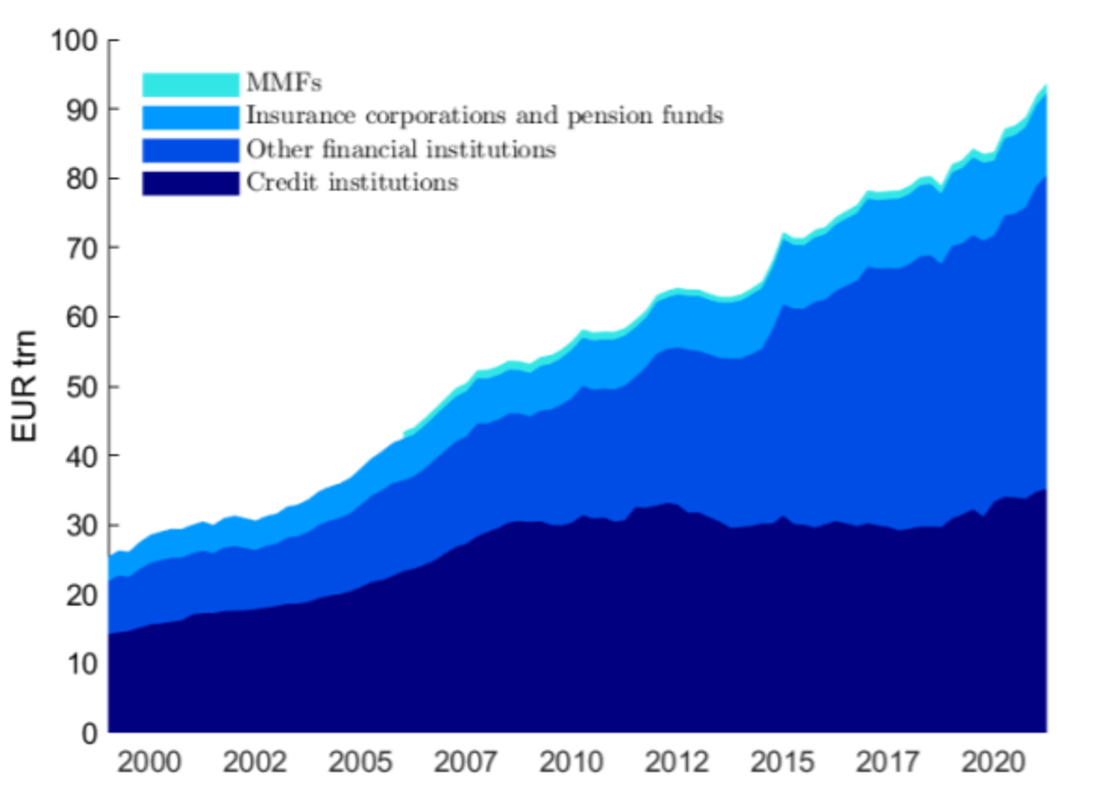

Related traits have additionally appeared internationally. Determine 4 exhibits the rising position performed by NBFIs in Europe, notably by asset managers.

Determine 4: Progress in Financial institution vs Non-Financial institution Belongings within the Eurozone

Supply: Aramonte et al (2021).

The bond holdings of broker-dealers—which are sometimes a part of banking teams—diminished after the GFC, whilst the general market expanded (Determine 3). That is fairly totally different from the dynamics pre-GFC, when broker-dealers performed a serious position in driving the shift from a bank-centric monetary system in direction of a market-based one, and their steadiness sheets noticed a ten-fold enlargement between 1990 and 2008, with a corresponding enhance in leverage. The position performed by European banks that we beforehand highlighted illustrates that. Because the GFC, regulatory tightening over the actions of banks and their affiliated broker-dealers, demographic adjustments, and a higher weight of capital markets in offering for retirement, in addition to technological change and the pursuit of operational efficiencies, have led to a rising position of market intermediation and NBFIs (Aramonte et al, 2021).

How do stability properties have a tendency to vary with such a metamorphosis? NBFIs deliver a spread of attributes to the monetary system and the financial system, resembling higher range within the ecosystem, and the benefit of less-correlated buying and selling motives amongst intermediaries. NBFIs might fill the hole when banks retreat from sure intermediation actions.

However, like banks, NBFIs may also feed systemic threat, i.e. disruptions to the exercise of a monetary middleman producing substantial prices—notably as externalities—for different monetary establishments or non-financial companies.

The roles of market costs and of steadiness sheet administration by NBFIs increase new points. The debt capability of an investor is more and more depending on the debt capability of different traders within the system, in order that leverage permits higher leverage, and spikes in margins can result in system-wide deleveraging. Deleveraging and ‘sprint for money’ situations grow to be two sides of the identical coin, moderately than being two distinct channels of stress propagation (Aramonte et al, 2021).

The higher weight of NBFIs signifies that threat exposures are more and more intermediated and held exterior the banking system. As an alternative of banks warehousing liquidity and credit score dangers on their steadiness sheets, such dangers are more and more outsourced to NBFIs. Such structural adjustments have mitigated counterparty credit score threat however have led to a monetary system extra delicate to giant swings in liquidity imbalances. In any case, the enterprise fashions of NBFIs are sometimes constructed round exploiting liquidity mismatches, and have a tendency to, on internet phrases, present liquidity in good instances. During times of economic turmoil, nonetheless, NBFIs usually retrench, and their liquidity provide can all of a sudden flip into substantial liquidity demand.

We noticed such an intense ‘sprint for money’ turmoil in March 2020, on the apex of the pandemic monetary shock, when traders shifted away abruptly and massively from dangerous property to cash-like property, thereby making specific such structural NBFI vulnerabilities with spillovers that impacted different contributors within the monetary system. Finally, it was the central banks’ versatile use of their steadiness sheets, together with the crossing into areas beforehand thought of exterior their territory, that stopped the hostile suggestions loops and helped to revive market functioning.

Such options of NBFI-based, market-based monetary intermediation have been carried over to world capital flows, because the latter have accompanied the previous.

2. Capital Flows to EMEs

2.1 Capital Flows to EMEs From the GFC to the Pandemic Shock

Capital inflows to EMEs held up properly after the GFC, even when sometimes passing by excessive turbulence (Determine 5). They slowed sharply in some years (Canuto, 2013a; 2016; 2018; 2021a):

Determine 5: Capital Inflows to EME areas

Supply: BIS (2021).

In June 2013, then-Fed Chair Ben Bernanke urged that the Federal Open Market Committee (FOMC) may quickly begin to decelerate its bond purchases. With that one assertion, made in passing, Bernanke unwittingly triggered a wave of interest-rate hikes and capital flight from rising markets.

On the time, the ‘fragile 5’—South Africa, Brazil, India, Indonesia, and Turkey—had excessive current-account deficits and have been strongly depending on inflows of international capital. For years, they skilled the spillover results of ultra-loose U.S. financial insurance policies, which despatched traders in search of larger yields in direction of rising markets. When Bernanke raised the potential for gradual monetary-policy tightening, traders briefly panicked.

Market jitters additionally occurred in 2015 when commodity costs fell and the financial outlook for China deteriorated.

One other bout of capital outflows from rising markets occurred in Could 2018, when the Fed actually did begin to cut back its asset holdings. However this tapering—adopted by a sell-off in U.S. bond markets and greenback appreciation—was halted in 2019. This time, the ‘fragile 5’ had been lowered to the delicate two of Turkey and Argentina, each with excessive current-account deficits and acute vulnerability to exchange-rate fluctuations, owing to their giant volumes of foreign-currency debt. Determine 5 exhibits these years when shocks occurred.

Rising Asia stands out because the one area that noticed a sustained enhance in capital flows after the GFC. Boosted by China, inflows to rising Asia doubled between the 2000–07 interval and the 2009-19 interval, from round 0.4% of worldwide GDP to a median of 0.8%.

2.2. The Pandemic Shock to Capital Flows to EMEs

During times of heightened uncertainty, the standard response of markets is a flight to security due to threat aversion. Capital flows to EMEs confronted such a deep shock at the start of the COVID-19 disaster. Though short-lived, capital outflows have been bigger than at any level in the course of the GFC (Canuto, 2021b, ch.23). Whereas banks’ broker-dealers have been within the epicenter of the GFC shock, this time the brand new options of worldwide capital flows led to a dramatic shock to capital flows to EMEs.

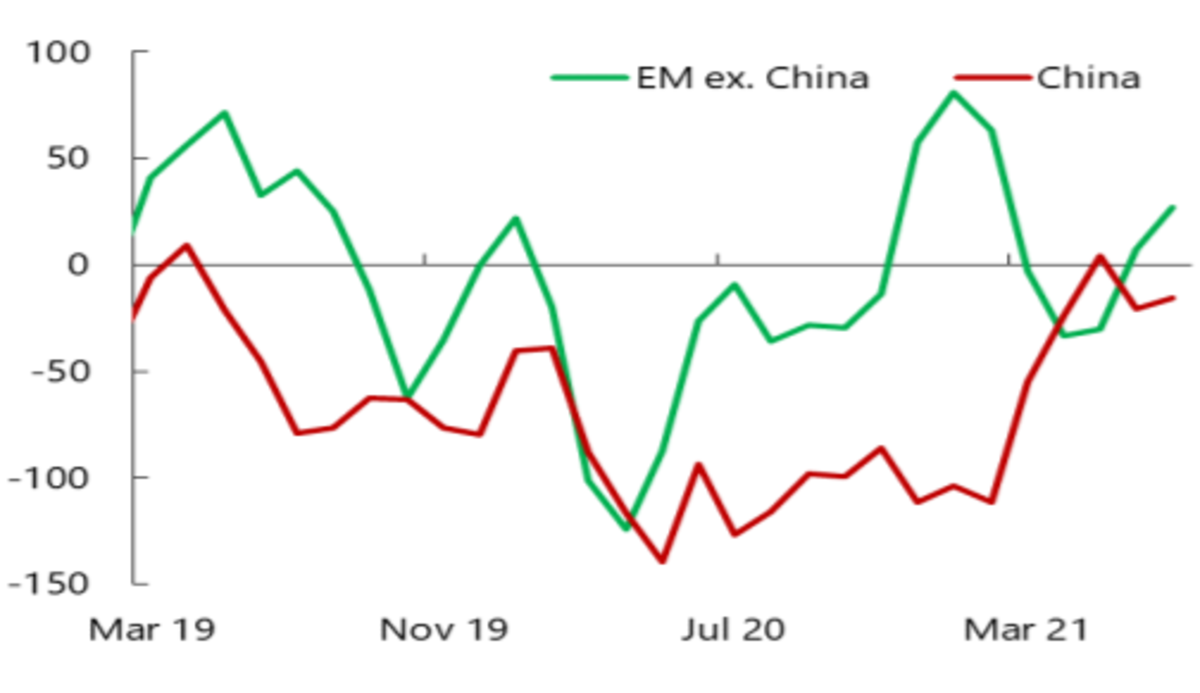

The extraordinary financial and monetary assist in main economies stabilized flows to EMEs within the months after Could 2021. General, the web capital flows have diverged considerably between China and EMEs excluding China (Determine 6). That displays the simultaneous presence of each common-to-EMEs and country-specific capital-flow drivers, together with some substitution impact of capital flows between China and different EMEs.

Determine 6: Web Capital Flows (USD Billions; Month-to-month)

Supply: IMF (2021).

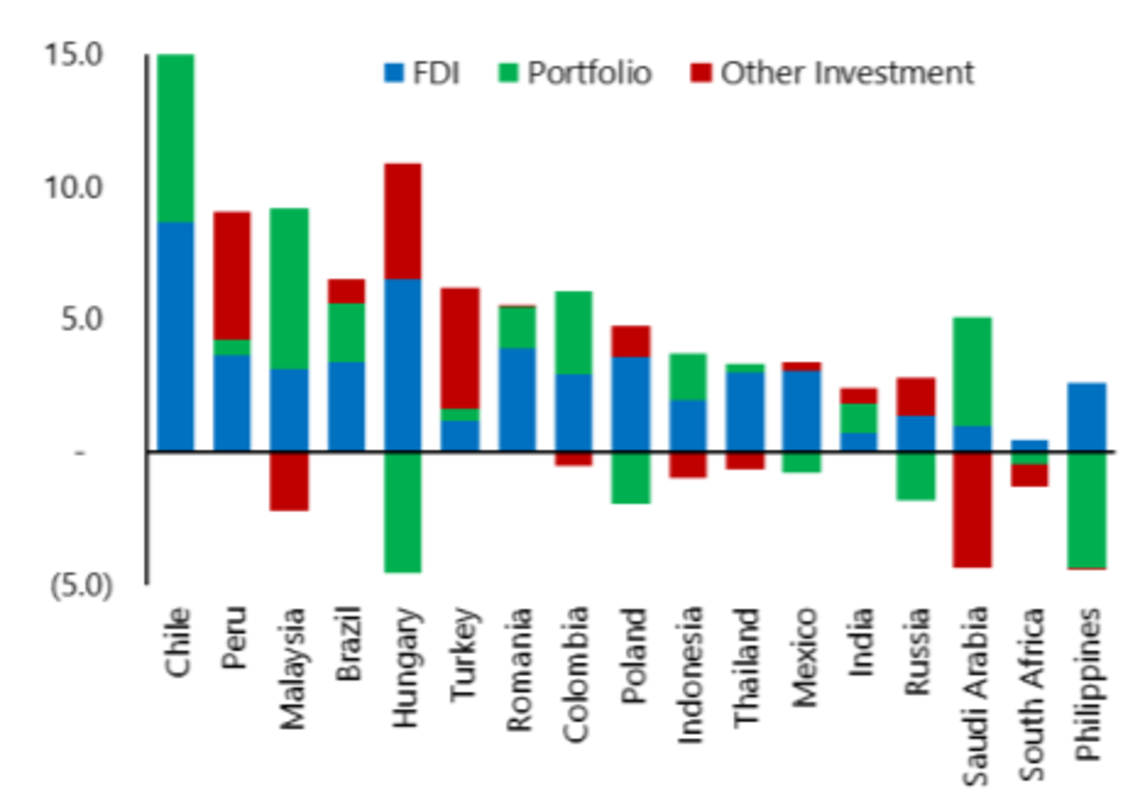

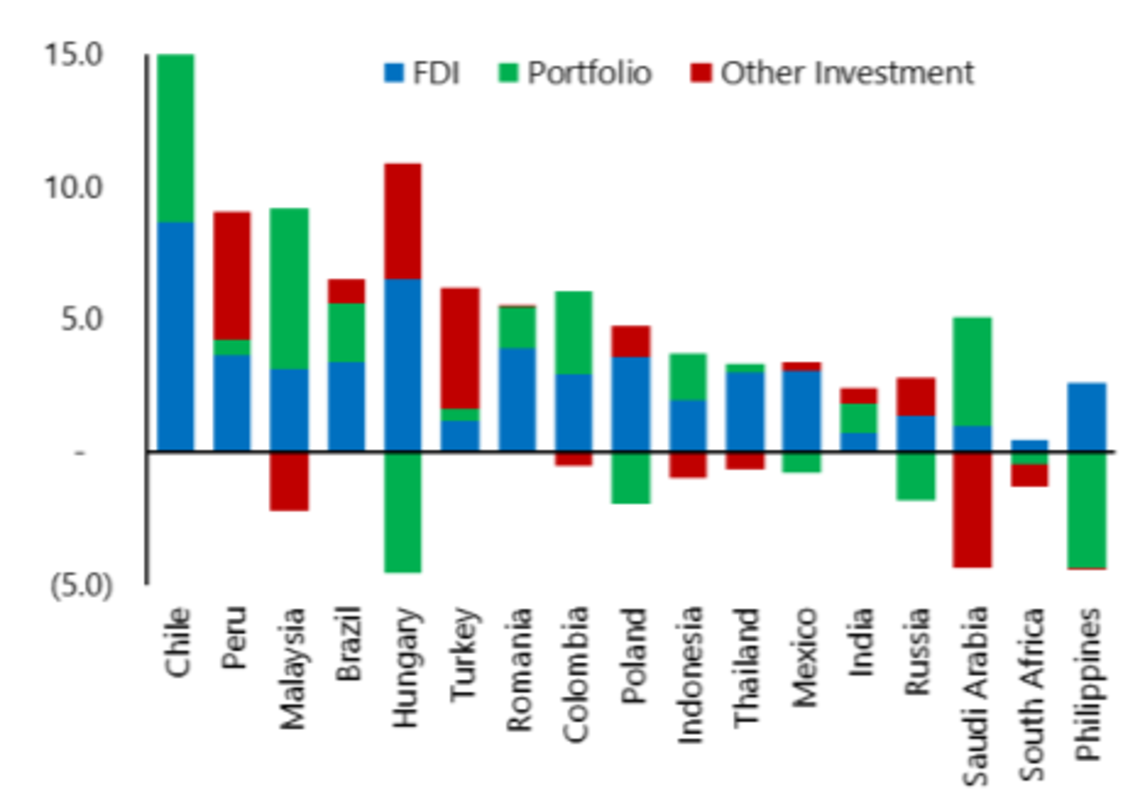

Worldwide bond issuance has partially compensated for the outflows from native equities and bonds. In reality, the variety within the composition of the non-resident flows to EMEs excluding China in 2021 illustrates the variety of country-specific determinants of capital flows (Determine 7).

Determine 7: EMEs excluding China: Composition of the Non-Resident Flows

(% of GDP; 2021 flows)

Supply: IMF (2021).

General flows to EMEs have carried out higher than initially anticipated, notably contemplating the severity of the shock, even when the restoration was uneven and incomplete in some market segments. The loss by the governments of a number of nations of international funding in native foreign money didn’t reverse. Capital flows to EMEs in 2021 haven’t maintained the robust tempo of the second half of 2020 (IIF, 2021). As consideration has shifted to attainable implications of reorientation of financial insurance policies of main AEs to capital flows to EMEs, we think about subsequent what the chances are of recent capital outflows as soon as it occurs.

2.3 Will One other Taper Tantrum Hit Rising Markets?

Market actions in mid-2021 led to renewed fears that adjustments in U.S. monetary and financial circumstances would set off a painful wave of capital flight from rising markets, as occurred in 2013. However instances have modified, and the best dangers to rising markets are actually elsewhere (Canuto, 2021a).

In early July 2021, the yield on U.S. ten-year Treasury bonds fell to its lowest stage in 4 months, and inventory markets dipped due to fears that the yr’s rosy projections for financial progress wouldn’t be borne out. Nonetheless, as we write, the prevailing view is that the 2021 spike in inflation might be short-term, permitting the U.S. Federal Reserve to pursue a clean unwinding of its steadiness sheet sooner or later sooner or later.

The July 2021 market episode may very well be partly traced again to February and March 2021, when U.S. long-term charges rose in anticipation that the Fed may quickly begin tightening its financial coverage. With U.S. President Joe Biden’s giant fiscal packages got here new fears about inflation and financial overheating. Ten-year Treasury yields duly elevated from under 1.2% to shut to 1.8%, earlier than stabilizing and falling again to earlier ranges. And ten-year Treasury yields began to rise considerably in September and October because it grew to become clear that the U.S. Fed would begin tapering its QE earlier than the tip of the yr and fundamental rate of interest hikes would in all probability are available 2022.

Although there have been some jitters following the June assembly of the policy-setting Federal Open Market Committee, when some FOMC members assumed a extra hawkish angle, the Fed nonetheless managed to maintain markets cool by promising to offer loads of advance discover earlier than starting to taper its month-to-month bond purchases. Since then, rates of interest have declined at a notable tempo.

However uncertainties stay for rising markets, most of which suffered capital flight because of the February-March tantrum and the attendant hike in U.S. market rates of interest. Though these outflows have since reversed, there may be at all times a chance that the Fed will really feel obliged to vary tack, leaving open the query of whether or not we’re heading for an additional ‘taper tantrum’ of the sort that shook world markets in 2013 (see part 2.1).

The February-March market tantrum was sufficient to generate a big discount in non-resident portfolio flows to rising markets. Though these losses have been partly recovered over the next three months, worries of a ‘taper tantrum 2.0’ will stay over the following two years, particularly if it begins to seem like the Fed will tighten sooner than it’s at the moment projecting.

However it is very important keep in mind that we’re not in 2013. Again then, the delicate 5’s (South Africa, Brazil, India, Indonesia, and Turkey; part 2.1) current-account deficits averaged round 4.4% of GDP, in comparison with simply 0.4% in 2021(Canuto, 2021a). Furthermore, the move of exterior sources into rising markets in recent times has been nowhere near as giant as within the years earlier than the 2013 tantrum. Nor are actual trade charges as overvalued as they have been then. Aside from Turkey, the delicate 5’s gross exterior financing wants as a proportion of international reserves have fallen considerably.

Two further mitigating components are additionally value contemplating. First, if stronger financial progress drives up U.S. rates of interest, constructive commerce linkages for some rising markets may assist to offset any detrimental monetary spillover. Second, it’s affordable to imagine that the Fed will provide extra acceptable ‘signaling’ this time round, thereby minimizing the danger of one other panic episode.

What about the issue of “twin deficits” in lots of rising economies? One can’t dismiss the truth that rising markets suffered giant capital outflows final yr simply as their fiscal deficits have been rising in response to the pandemic. However regardless of the COVID-19 disaster, rising markets usually have been in a position to finance their bigger fiscal deficits by counting on home traders and, in some circumstances, their central banks (Canuto, 2020). And beginning within the second half of 2020, purchases of presidency securities by non-residents in some rising markets began to select up once more.

True, as a result of some issuance of foreign-currency-denominated securities should still be essential, the dangers related to altering foreign-exchange flows haven’t been eradicated completely. International locations resembling Colombia and Chile nonetheless have comparatively excessive ranges of dollar-denominated debt, and in some rising markets, portfolio inflows will stay essential to financing fiscal deficits.

However, in the end, the larger dangers dealing with rising markets lie elsewhere. Moderately than worrying about one other taper tantrum, we needs to be extra involved with the gradual tempo of COVID-19 immunizations resulting in an anemic post-pandemic restoration; commodity worth hikes producing inflation; and financial methods that merely restore the low progress charges of the pre-pandemic period.

2.4. Why a Weakening Greenback Tends to be Good for EMEs

After peaking towards different currencies in March 2020, the greenback fell by virtually 15% by the tip of that yr. Asset portfolio managers have been taking ‘quick’ positions towards the greenback, that’s, betting on its future fall. The greenback is predicted to finish 2021 way more devalued towards the euro, the yen, and the Chinese language RMB.

The height in the course of the coronavirus monetary shock mirrored the seek for a protected haven in short-term U.S. bonds or money that occurs in instances of heightened world aversion to threat. The greenback rose virtually 10% within the first quarter of the yr. The temper enchancment within the subsequent months lowered the seek for security. There’s at the moment a convergence of views that, regularly or not, U.S. present account deficits and inadequate home financial savings have a tendency to slip down the relative worth of the greenback (see, for instance, Roach, 2020, and Rogoff, 2020).

That is excellent news for rising economies in 2021, judging from an essay by Hofmann and Park (2020), included within the Financial institution for Worldwide Settlements (BIS) Quarterly Report of December 2020. Free monetary circumstances and sustained enlargement of worldwide credit score favor progress on the true aspect of rising economies, with the presence of the greenback as an influential issue on this transmission. Based on the authors’ estimates, a shock of 1% appreciation of the greenback towards a large basket of different currencies reduces by 0.3 proportion factors the financial progress of a bunch of 21 rising nations that they think about. One might count on an impression in the wrong way within the occasion of a devaluation of the greenback.

The authors spotlight 4 “channels of greenback transmission” to elucidate the detrimental correlation between the greenback’s power and the expansion of the worldwide financial system. First, the demand for the foreign money displays, as a barometer, the worldwide urge for food for threat by traders. When the latter collapses, the seek for refuge raises the worth of the greenback, similtaneously capital outflows and worsening monetary circumstances on the origins are witnessed, along with retraction with respect to higher-risk property and shoppers. The greenback rises, whereas the extent of financial exercise tends to fall.

Second, there’s a mismatch between currencies on the perimeters of liabilities and property in world credit score in {dollars} exterior america, the magnitude of which is appreciable. When the greenback falls, steadiness sheets during which liabilities decline relative to property in different currencies get stronger. The provision of credit score, in flip, will increase as a result of enchancment in threat evaluation. This tends to occur even with short-term commerce finance.

Third, one thing in the identical course happens within the markets for presidency bonds in native currencies, not least as a result of world traders who carry securities from numerous nations regulate their portfolios in accordance with the danger circumstances of the group as a complete. It’s attention-grabbing to notice that Hofmann and Park (2020) point out a examine displaying that adjustments within the greenback towards a broad set of currencies weigh extra, for securities markets in native foreign money individually, than adjustments within the worth of the nation’s personal foreign money towards the greenback.

The fourth channel of greenback transmission is international commerce. A devaluation of the greenback tends, in fact, to negatively have an effect on competitiveness in relation to dollarized economies on the a part of these whose currencies recognize. Nonetheless, notably in circumstances during which invoices are in {dollars}, there may be worth rigidity within the quick time period.

Now, these 4 channels are notably related within the case of rising economies. Regardless of the ‘deepening’ and improvement of the monetary methods of those nations in current a long time, together with the enlargement of local-currency securities markets, their monetary methods nonetheless shouldn’t have the density of these in superior economies and are depending on exterior financing. It isn’t by probability that they’ve comparatively excessive dollar-denominated debt (Determine 8, left panel) and a big presence of international traders as holders of native foreign money sovereign bonds (Determine 8, middle panel). When the provision of sources of international trade hedge will not be satisfactory, native debtors of greenback funds and exterior consumers of native foreign money securities are typically uncovered in relation to trade price variations. Lastly, greenback commerce invoicing is extra widespread in rising market economies than in superior economies (Determine 8, proper panel).

Determine 8: Greenback Debt, Overseas Buyers, and Greenback Commerce Invoicing in EMEs

(median values)

Notes: 1. Non-banks’ complete cross-border USD-denominated liabilities (financial institution loans and debt securities). 2 Excluding Singapore, Hong Kong and Czech Republic as a consequence of lack of information availability. For Korea, information are primarily based on all listed bonds. 3 Newest obtainable information.

Supply: Hofmann & Park (2020).

So long as a future downward shift within the greenback will not be abrupt, whereas low rates of interest in superior economies and abundance of worldwide liquidity proceed, its transmission through monetary channels to rising economies on the whole tends to be favorable within the close to future.

The weights of the 4 channels differ by nation. As an example, whereas the commerce relationship with america and the fourth channel issues loads to Mexico, the monetary transmission channels are extra highly effective within the case of Brazil. General, the estimates of Hofmann and Park (2020) level to a acquire.

That is according to a earlier paper by Samer Shousha, from the Federal Reserve Board, displaying that the transmission of greenback actions to rising economies takes place primarily by monetary circumstances moderately than internet exports, and that (Shousha, 2019):

“… the central position of the U.S. greenback in world commerce invoicing and financing – the dominant foreign money paradigm – and the elevated integration of EMEs into worldwide provide chains weaken the standard commerce channel. Lastly, as anticipated if monetary vulnerabilities are distinguished, EMEs with larger publicity to credit score denominated in {dollars} and decrease financial coverage credibility expertise higher contractions throughout greenback appreciations.”

It’s value retaining in sight the burden of home, country-specific components. Within the expertise of the detrimental monetary impact of the appreciation of the greenback in Could 2018, it was not by probability that Argentina and Turkey have been captured by the storm, due to their explicit vulnerability to greenback fluctuations. In Brazil, the probably favorable tide from overseas will solely be taken benefit of if the home fiscal mooring is agency. In any case, most EMEs are likely to welcome greenback depreciation towards a large basket of currencies.

3. A Coverage Toolkit to Deal With Capital Circulation Volatility in EMEs

Main dangers accompany the advantages of economic improvement and worldwide monetary integration for EMEs (Canuto and Ghosh, 2013). There’s the inherent pro-cyclicality of the monetary system, amplifying enterprise cycles. Constructive shocks have a tendency to guide monetary establishments and markets to maneuver in the identical course, feeding asset worth and credit score booms, and boosting a generalized enlargement of financial exercise. When the cyclical tide adjustments, asset costs decline, credit score shrinks, and the financial slowdown tends to be deeper due to the passion in the course of the upside section. On the excessive, monetary crises with main actual sector dislocations and enormous fiscal prices can occur.

Such pro-cyclicality and the accompanying dangers of economic crises are additionally current in worldwide monetary integration, and capital flows usually have unstable options. However the evolution of economic intermediation in the previous few a long time, as we’ve got mentioned, has accentuated such options as a ‘draw back’ accompanying its ‘upside’ penalties.

In AEs, the buildup of banking methods’ vulnerabilities previous to the GFC occurred by complicated chains of credit score intermediation and associated to giant gross capital flows, as we’ve got famous. After the GFC, nations undertook measures to strengthen the resilience of their monetary methods, together with towards dangers originating overseas. A key part has been to aim to curb the propensity of economic methods to behave pro-cyclically. Cross-border spillovers have additionally been tentatively handled within the monetary structure.

Nonetheless, EMEs face higher challenges in coping with worldwide monetary integration and cross-border flows (Claessens and Ghosh, 2013). First, capital flows to EMEs, even in internet phrases, are sometimes giant relative to their home economies and total absorptive capability—particularly relative to the scale and depth of their monetary methods. Monetary flows correspond to a lot bigger shares of the home capital markets of EMEs than of AEs.

A second problem comes from the truth that EMEs usually tend to endure bigger shocks. Their economies are smaller and fewer diversified, and detrimental shocks—home or from overseas—are typically exacerbated and propagated extra simply in EMEs due to structural and institutional options (resembling weaker enforcement of property rights and poor info infrastructures). Giant capital inflows are likely to work together with and amplify the home monetary and actual enterprise cycles in EMEs to a higher extent than in AEs.

The challenges to financial and monetary sector stability in EMEs introduced by worldwide monetary integration are important. Enterprise cycles and monetary cycles are extra unstable in EMEs than in AEs (Canuto and Ghosh, 2013). Opposed monetary cycles mixed with recessions, though not essentially extra frequent or longer, are likely to result in worse and deeper losses in EMEs than in AEs. Conversely, recoveries mixed with favorable monetary cycles are typically stronger (and sooner) in EMEs than in AEs. Capital move surges and sudden capital outflows are related to the best amplification in enterprise cycles in EMEs.

To handle these dangers, as argued by Canuto and Cavallari (2013), EMEs should use a unique and broad set of insurance policies, together with macroprudential instruments, along with financial, fiscal, and micro prudential insurance policies. EMEs are additionally topic to tighter constraints than AEs on fiscal and financial insurance policies, and relatedly, extra restricted headroom. EMEs are prone to have to make use of a extra heterodox mixture of coverage instruments, notably together with macroprudential insurance policies, but additionally capital-flow administration (CFM) instruments.

International monetary integration has challenged the assumption that floating trade charges would suffice as a response to the ‘Mundell trilemma’, i.e. that free capital mobility, pegged trade charges, and impartial financial insurance policies are incompatible (Obstfeld and Taylor, 2004). As argued by Rey (2013):

“Essentially the most acceptable insurance policies are these aiming instantly on the foremost supply of concern (extreme leverage and credit score progress). This requires a convex mixture of macroprudential insurance policies guided by aggressive stress-testing and harder leverage ratios. Relying on the supply of economic instability and institutional settings, the usage of capital controls as a partial substitute for macroprudential measures shouldn’t be discarded.”

The IMF’s built-in coverage framework designed to assist policymakers to face frequent troublesome tradeoffs in pursuing home and exterior stabilization goals, acknowledges that, below some circumstances, impartial financial insurance policies are attainable if and provided that the capital account is managed, instantly or not directly.

A powerful macroprudential construction was erected after the GFC however coping with the pandemic emergency led to the comfort of laws in 2020-2021. As mentioned by Edwards (2021), in each nation regulatory forbearance was given a key position within the response to COVID-19. Rebuilding the macroprudential cloth—together with capital-flows administration (CFM) controls as macroprudential devices—might be key to lowering the prices of future systemic shocks.

4. Backside Line

The transformation of worldwide finance has not suppressed the necessity for insurance policies to watch and deal with dangers. The higher weight of NBFIs and market-based intermediation has introduced adjustments to the danger panorama.

On the aspect of recipients of internet capital inflows, home methods of institutional strengthening to bolster alignment of dangers between traders and nations, along with regulatory vigilance towards extra monetary euphoria or despair, stay essential. The bar by way of home institutional high quality—company governance requirements, enterprise surroundings—has been raised within the new section of worldwide finance.

To finalize, it’s also value referring to the potential transformative impression—and corresponding want for regulatory adaptation—of digital applied sciences on cross-border finance. We could be getting ready to an extra metamorphosis of worldwide finance, and the instability that might deliver.

References

Aramonte, S.; Schrimpf, A.; and Shin, H.Y. (2021). Non-bank monetary intermediaries and monetary stability, BIS Working Papers No 972, October.

BIS – Financial institution for Worldwide Settlements (2017). Annual report, July.

BIS – Financial institution for Worldwide Settlements (2021). CGFS Papers No 66 – Altering patterns of capital flows.

Canuto, O. (2013a). “QE tapering as a wake-up name for rising markets”, Capital Finance Worldwide, Fall subject.

Canuto, O. (2013b). Forex Struggle and Peace. Challenge Syndicate, March 12.

Canuto, O. (2016). “China’s spill-overs on Latin America and the Caribbean”, Capital Finance Worldwide, Summer time subject.

Canuto, O. (2017). The metamorphosis of economic globalization, Coverage Middle for the New South, September 15.

Canuto, O. (2018). Argentina, Turkey and the Could Storm in Rising Markets,

Canuto, O. (2020). Quantitative Easing in Rising Market Economies, Coverage Middle for the New South, November 19.

Canuto, O. (2021a). Will one other taper tantrum hit rising markets? Challenge Syndicate, July 14.

Canuto, O. (2021b). Climbing a excessive ladder: improvement within the world financial system. Coverage Middle for the New South, June 6.

Canuto, O. and Ghosh, S.R. (eds.) (2013). Coping with the Challenges of Macro Monetary Linkages in Rising Markets, World Financial institution: Washington, DC.

Canuto, O. and Cavallari, M. (2013). “Financial Coverage and Macro Prudential Regulation: Whither Rising Markets”, In Canuto and Ghosh (2013), p. 119-154.

Canuto, O. and Ramcharan, V. (2015). De-Risking Is De-linking Small States from International Finance, Nasdaq.com, October 23.

Claessens, S. and Ghosh, S.R. (2013). “Capital move volatility and systemic threat in rising markets: the coverage toolkit”, Canuto and Ghosh (2013), p. 91-118.

Edwards, S. (2021). Macroprudential insurance policies and the Covid-19 pandemic: dangers and challenges for rising markets, NBER Working Paper No. 2944, October.

FSB – Monetary Stability Board (2020), International Monitoring Report on Non-Financial institution Monetary Intermediation, Monetary Stability Board Report, December 16.

Hofmann, B. and Park, T. (2020). “The broad greenback trade price as an EME threat issue”, BIS Quarterly Evaluate, December.

IMF – Worldwide Financial Fund (2020). Towards an Built-in Coverage Framework, October 8.

IMF – Worldwide Financial Fund (2021). EM capital flows monitor, September 13.

IIF – Institute of Worldwide Finance (2021). Capital Flows Tracker – September 2021 Bond Issuance Saves the Day, October.

McKinsey International Institute (2017). The brand new dynamics of economic globalization. August.

Obstfeld, M and Taylor, A.M. (2004). International capital markets: integration, disaster and progress, Cambridge College Press.

Rey, H. (2013). Dilemma not Trilemma: The worldwide monetary cycle and financial coverage independence, VoxEU, August 13.

Roach, S. (2020). “The top of the greenback’s exorbitant privilege”, Monetary Occasions, October 5.

Rogoff, Okay. (2020). The calm earlier than the exchange-rate storm? Challenge Syndicate, November 10.

Shin, H. S. (2012). “International Banking Glut and Mortgage Threat Premium. 2011 Mundell-Fleming Lecture”, IMF Financial Evaluate, 60 (July), p. 155–92.

Shousha, S. (2019). The greenback and rising market economies: monetary vulnerabilities meet the worldwide commerce system. Federal reserve System, October.

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Middle for the New South, a nonresident senior fellow at Brookings Establishment, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]