[ad_1]

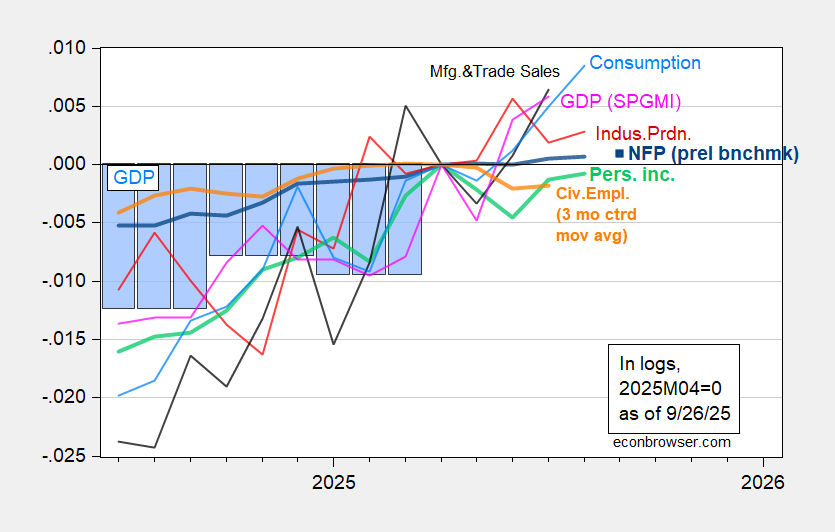

With the non-public earnings for August, we’ve the next image of key indicators adopted by the NBER’s Enterprise Cycle Courting Committee (BCDC). Private earnings ex-current transfers and employment are extra closely weighted than different indicators.

Determine 1: Implied NFP preliminary benchmark revision (daring blue), civilian employment with smoothed inhabitants controls, 3 month centered transferring common (daring orange), industrial manufacturing (pink), Bloomberg consensus employment for implied preliminary benchmark, (blue sq.), private earnings excluding present transfers in Ch.2017$ (daring gentle inexperienced), manufacturing and commerce gross sales in Ch.2017$ (black), consumption in Ch.2017$ (gentle blue), and month-to-month GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M04=0. Supply: BLS through FRED, Federal Reserve, BEA 2025Q2 third launch, S&P International Market Insights (nee Macroeconomic Advisers, IHS Markit) (9/2/2025 launch), and creator’s calculations.

August NFP is just 0.07% above the April worth, whereas the Bloomberg consensus for September (for +39K web acquire) is 0.09% above. The three month centered transferring common of civilian employment is 0.2% beneath April worth. Both in uncooked kind or centered transferring common, civilian employment is beneath latest peak. Basically, employment progress is “useless within the water”. And may one be a believer within the civilian (family) sequence turning factors higher presage recessions, one needs to be fearful.

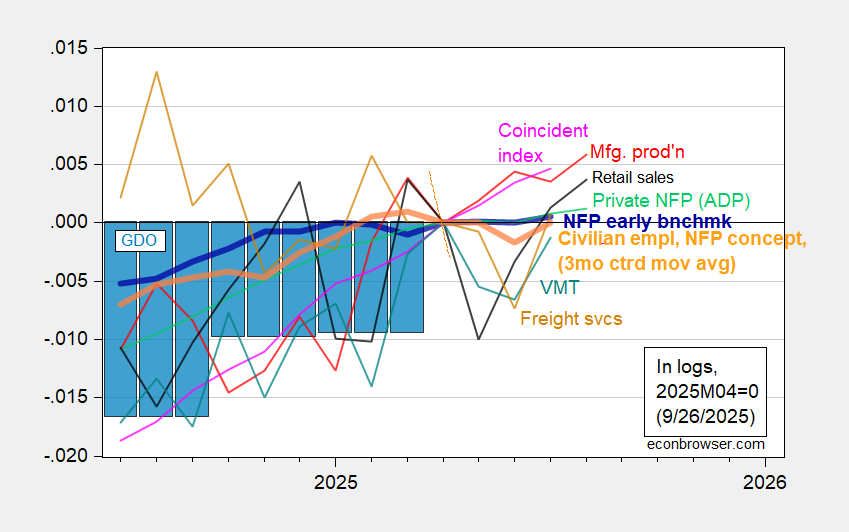

Listed below are different indicators (together with the brand new early benchmark from the Philadelphia Fed), and the newest coincident index

Determine 2: Nonfarm Payroll early benchmark (NFP) (daring blue), Bloomberg consensus (blue sq.), civilian employment adjusted to NFP idea, 3 month centered transferring common (daring orange), manufacturing manufacturing (pink), personal NFP from ADP/Stanford (gentle inexperienced), actual retail gross sales (black), automobile miles traveled (teal), BTS Freight Providers Index (tan), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2025M04=0. Retail gross sales deflated by chained CPI, adjusted by creator utilizing geometric X-13. Supply: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve through FRED, BEA 2025Q2 third launch, and creator’s calculations.

Discover that the Philadelphia Fed’s early benchmark worth for July is just 0.05% above April’s worth.

For many who argue for the substitution of personal sequence for presidency (BLS) employment sequence, it’s of curiosity that the ADP-Stanford Digital Lab personal employment sequence is just 0.2% above April ranges.

Whereas the labor market statistics should not very optimistic, it’s fascinating that consumption progress continues (regardless of actual private earnings trending sideways). This signifies both the inventory of financial savings stays excessive, optimism about future disposable earnings (which appears counter to family survey outcomes), or accelerated spending to keep away from future tariffs.

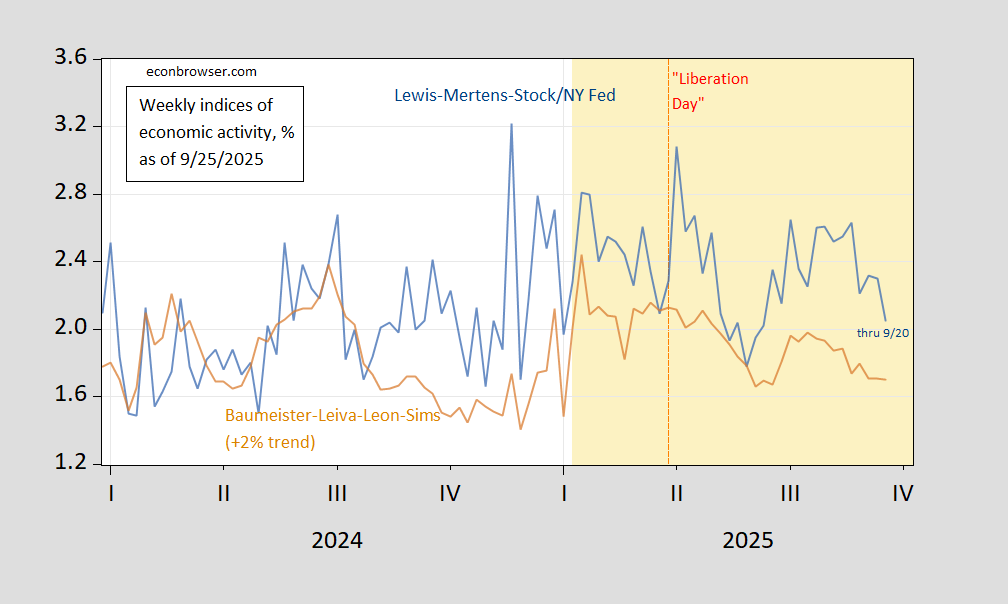

All in all, knowledge by means of August recommend the economic system has not but hit detrimental progress alongside all key dimensions of financial exercise. Nevertheless, larger frequency knowledge going by means of mid-September suggests a slowdown is coming.

Determine 3: Lewis-Mertens-Inventory WEI (blue), and Baumeister-Levia-Leon-Sims WECI plus pattern progress of two% (tan), each in %. Supply: Dallas Fed through FRED, Weekly State Indexes.

[ad_2]