[ad_1]

Municipals had been combined in Thursday buying and selling whereas U.S. Treasury yields fell and equities rallied, largely ignoring the Federal authorities shutdown and the probably lack of key macroeconomic indicators on account of it.

Triple-A muni yields rose barely on the quick finish on some scales whereas USTs noticed small good points throughout the curve.

The 2-year muni-UST ratio Thursday was at 66%, the five-year at 63%, the 10-year at 71% and the 30-year at 90%, in line with Municipal Market Knowledge’s 3 p.m. EDT learn. ICE Knowledge Providers had the two-year at 64%, the five-year at 63%, the 10-year at 71% and the 30-year at 90% at a 3 p.m. learn.

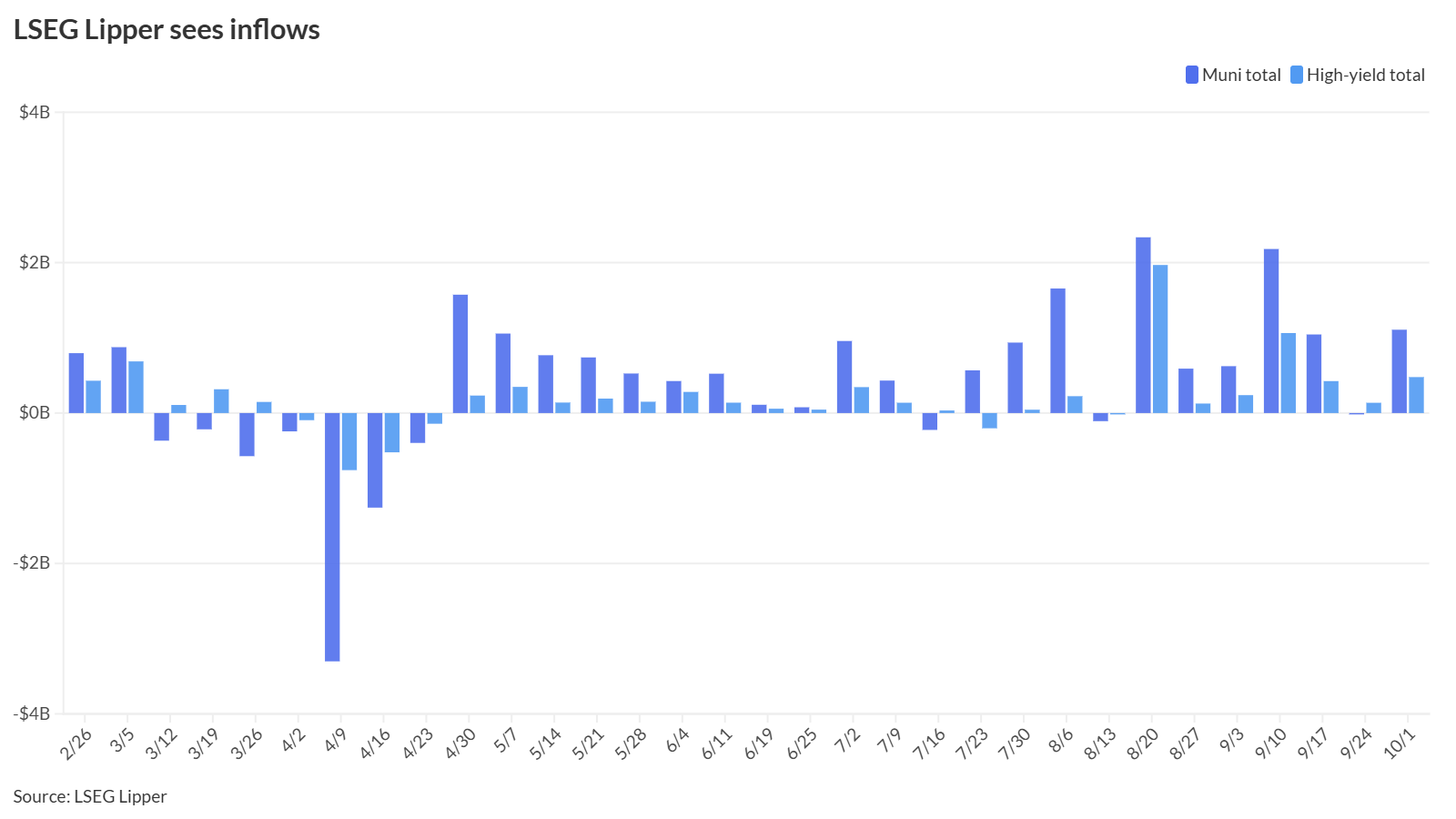

Municipal bond mutual funds returned to inflows as traders put $1.108 billion into the funds within the week ended Wednesday, in comparison with $28.9 million of outflows the week prior, in line with LSEG Lipper knowledge.

Excessive-yield funds noticed one other week of inflows with $478.1 million over final week’s $133.7 million.

This week marks a ninth week of inflows over the past 11, and the twentieth week of inflows within the final 23, per J.P. Morgan, which famous that on a mixed foundation — open-end funds and ETFs — flows had been uniformly constructive throughout all classes, save for brief/intermediate funds, which had been destructive $13 million.

September was “a turnaround month for municipals,” aided by each a Federal Reserve fee reduce and “rising recognition of the comparative worth within the asset class,” mentioned Kim Olsan, senior mounted earnings portfolio supervisor for NewSquare Capital.

Olsan highlighted high-grade municipals earned 2.3% in September, which brings year-to-date returns to 2.6%. GOs and income bonds “maintain comparable annual returns, as consumers have change into much less keen about particular income sectors on slim credit score spreads,” she mentioned.

One other noteworthy thread was “the power within the lengthy finish after lagging shorter maturities in current months,” Olsan mentioned, including {that a} “long-dated index gained 4.0%, properly surpassing a near-0% achieve for 1-2 yr index.”

“Commerce allocations rotated post-rate reduce as additional Fed actions raised expectations that the curve might flatten (which it has) and actual yields will fall in coming months,” she mentioned.

On the prime of the month, long-term AAA yields had been above 4.50% however up to now have fallen to roughly 4.25%, Olsan famous.

Moreover, numerous income sectors turned out “significant efficiency” final month, with Healthcare main the pack up 2.8% however nonetheless behind the broader marketplace for the yr, Olsan mentioned.

“Though the brand new tax regulation might have an effect on income fashions with decreased funding to Medicaid/Medicare, the offset has been a drop in provide,” she mentioned. “Final month’s issuance within the class barely surpassed $1 billion amongst $100 million or bigger points, and with a shorter maturity focus.”

Taxable munis noticed a “mid-month rally” however “wound up reversing course by the shut of September,” closing out with a “1.2% achieve (100 foundation factors under the principle tax-exempt index) however have gained greater than 6.0% this yr,” Olsan mentioned.

For the month forward, “the upcoming problem for munis is a heavy bias towards destructive returns with mismatched redemptions towards projected provide,” she mentioned.

Elsewhere, the federal government shutdown has taken maintain and is poised to “elevate market uncertainty” as “credit score implications for the muni market can change into extra acute the longer the shutdown lasts,” mentioned Jeff Lipton, municipal market intelligence analyst for The Bond Purchaser.

“Because it stands, futures contracts are pricing in a 90%+ certainty of a 25 foundation level fee reduce, and any threats to financial progress would solely add additional justification to the coverage motion and encourage [Federal Reserve] Chair Powell’s post-meeting presser,” Lipton mentioned.

He famous that whereas the “shorter finish of the muni curve might see downward yield motion in sync with the Central Financial institution’s expectations,” the long-end “tethered to the disruptive forces of D.C. actions” might react oppositely with “heavier upward yield strain.”

“Nonetheless, whereas the shutdown will finally be resolved, current circumstances might catalyze tactical funding alternatives as a solution to seize much more compelling yield and earnings alternatives,” Lipton added.

AAA Scales

MMD’s scale was unchanged: 2.38% (unch) in 2026 and a couple of.30% (unch) in 2027. The five-year was 2.32% (unch), the 10-year was 2.91% (unch) and the 30-year was 4.21% (unch) at 3 p.m.

The ICE AAA yield curve noticed small cuts: 2.36% (+1) in 2026 and a couple of.29% (+2) in 2027. The five-year was at 2.31% (+1), the 10-year was at 2.91% (unch) and the 30-year was at 4.23% (unch) at 3 p.m.

The S&P World Market Intelligence municipal curve was reduce on the quick finish: The one-year was at 2.39% (+3) in 2025 and a couple of.29% (+3) in 2026. The five-year was at 2.30% (unch), the 10-year was at 2.91% (-1) and the 30-year yield was at 4.21% (unch) at 3 p.m.

Bloomberg BVAL was reduce on the quick finish: 2.29% (+2) in 2025 and a couple of.25% (+1) in 2026. The five-year at 2.28% (unch), the 10-year at 2.88% (-1) and the 30-year at 4.21% (-1) at 3 p.m.

Within the major market Thursday, Jefferies priced for Hays County, Texas, (/AA+/AA+/) $187.06 million of mixture tax and income certificates of obligation, with 5s of two/2026 at 2.58%, 5s of 2030 at 2.50%, 5s of 2035 at 3.05%, 5s of 2040 at 3.78%, 5s of 2045 at 4.26% and 5s of 2050 at 4.48%, callable 2/2035.

Loop Capital Markets priced for Riverside County, California, (Mig 1//F1+/) $148.165 million of Teeter Plan-issue obligation notes, Collection 2025A, priced at par with 2.55s of 10/2026.

[ad_2]