[ad_1]

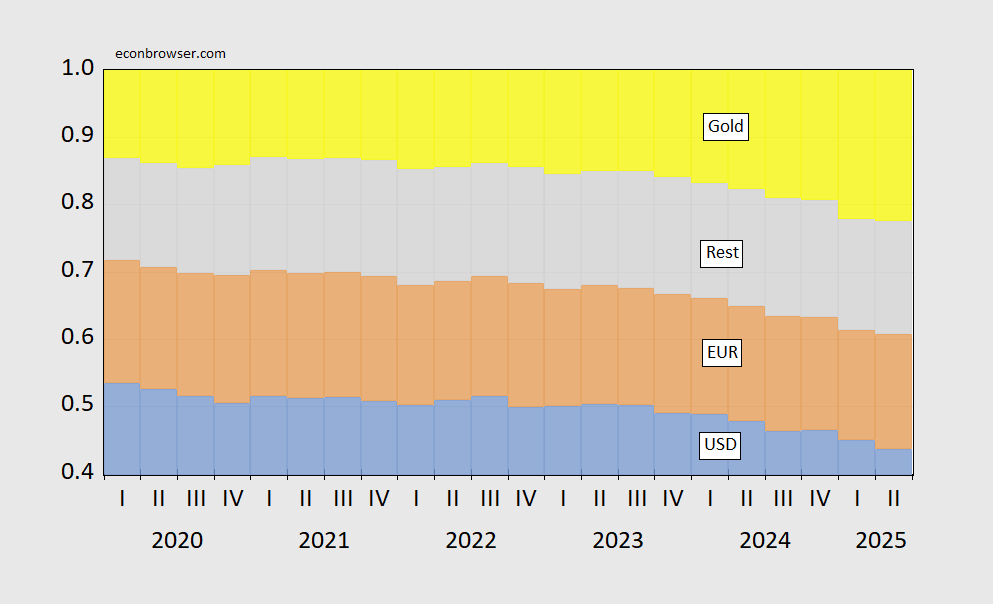

COFER knowledge is out for Q2. With estimated gold held by the central banks, now we have this image of reserve composition.

Determine 1: USD shares of fx (blue bars), EUR (tan), all different (grey). USD(EUR) share assumes 60%(35%) of unallocated reserves are in USD(EUR). Supply: IMF COFER, and creator’s calculations.

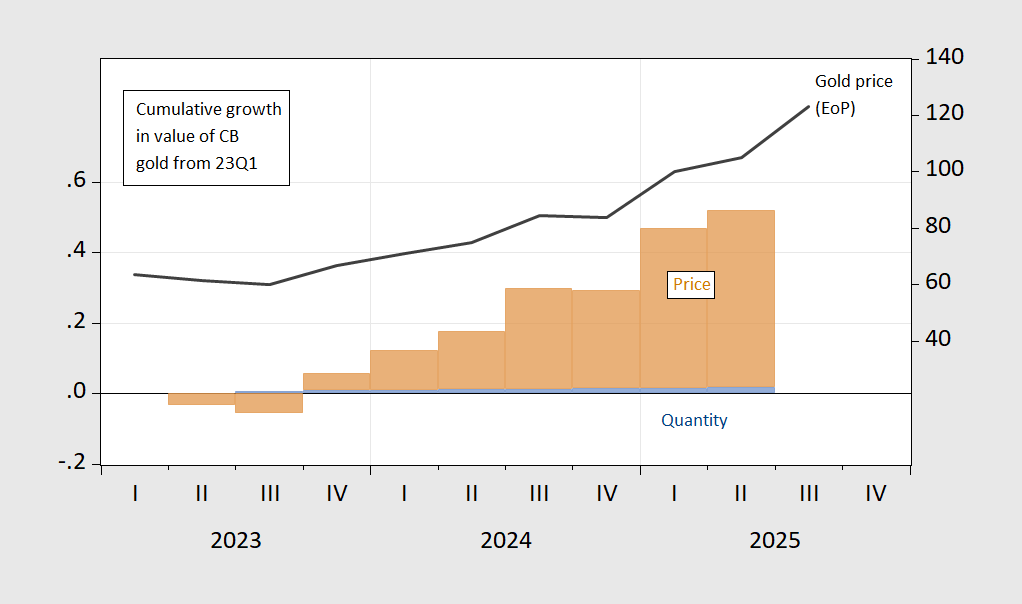

Observe that the rise in gold holding shares of worth is pushed primarily by the rise in gold costs, fairly than quantity of gold. That is proven in Determine 2, the place the change within the worth of gold reserves relative to 2023Q1 is decomposed into worth and amount elements, together with the value of gold index (proper facet).

Determine 2: Cumulative development in worth of gold held by central banks (brown bar), and in amount of gold (blue bar), relative to 2023Q1. 2025Q2 gold is reported acquisitions added to 2025Q1 portions, multiplied by implied gold worth index. Supply: COFER, Gold Council to 2025Q1, 2025Q2-Q3 calculations by creator primarily based on Gold Council knowledge.

The rise in gold holding shares is primarily as a result of valuation adjustments fairly than amount adjustments. With a Q3 improve in gold costs of 17% (not annualized), this distinction is especially necessary.

For an evaluation of particular person central financial institution conduct with respect to gold (as much as 2022), see Chinn, Frankel and Ito (2025).

[ad_2]