[ad_1]

Your really will not be eager about having to suppose as a lot about inventory market worth ranges as appears warranted of late. It’s fairly apparent AI performs are in a monster bubble, however that doesn’t imply they gained’t go even larger earlier than actuality drags them again to earth. As we’ve mentioned, traditionally a inventory market rout, except fueled by a number of debt as within the Nice Crash, doesn’t generate a disaster however does injury the economic system although buyers pulling manner again on spending and capital expenditures. That lack of demand is recessionary and may produce deflation and zombification. So the hangover can nonetheless do numerous hurt.

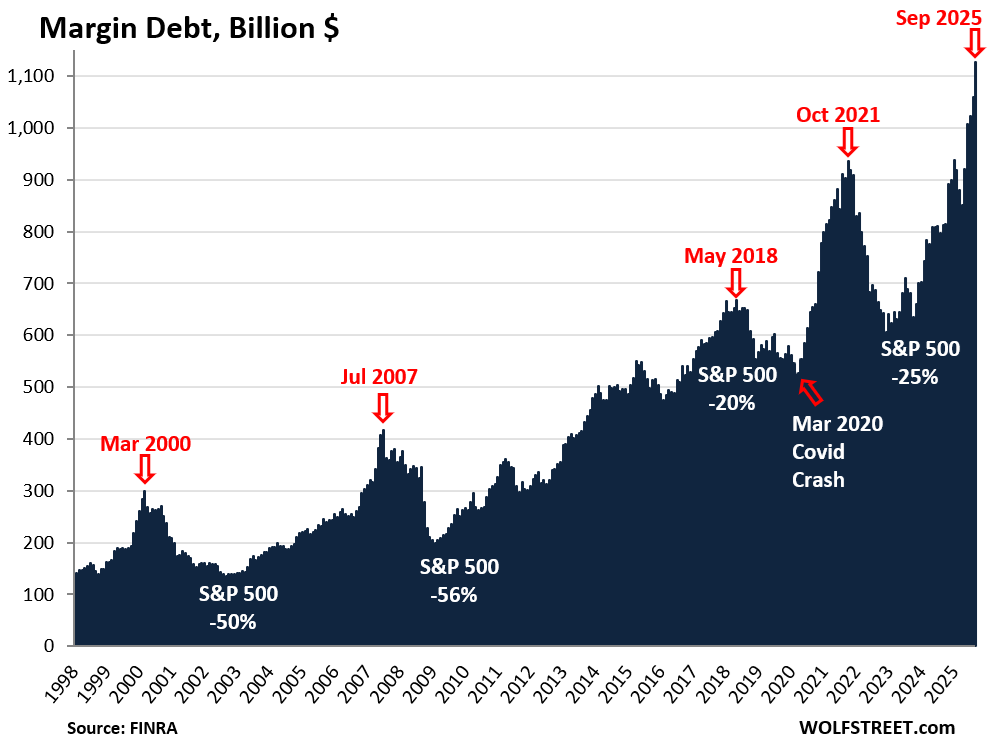

Some market-watching websites, together with Wolf Richter’s, have been sounding alarms about US margin debt hitting an all-time excessive. Right here’s Wolf’s chart and a snippet from his commentary:

Leverage within the inventory market has been spiking since April. In September, margin debt – the quantity buyers borrowed from their brokers – spiked by one other 6.3%, or by $67 billion, from August to a document $1.13 trillion…

The extra leverage – borrowed cash flowing into the inventory market – creates shopping for strain and drives inventory costs larger. Leverage is the nice accelerator on the way in which up, however it’s additionally the nice accelerator on the way in which down. Multi-month surges in margin debt, leaping from new excessive to new excessive, point out extreme hypothesis and risk-taking and have invariably led to sharp selloffs:

The wee drawback is that whereas the image above is correct, it doesn’t add as a lot to what we learn about inventory market frothiness as one would possibly suppose. Borrowing towards shares is strictly regulated. So when market costs go up so much, so to does margin borrowing. The chart above does give one other demonstration of how sharply inventory costs have risen and that when these spells of untamed enthusiasm put on off, the compelled deleveraging accelerates the plunge.

A rejoinder from the admittedly mainstream Morningstar in August:

Margin debt isn’t a pink flag for one investor.

One of many explanations put ahead not too long ago for the record-breaking rally within the U.S. inventory market was the equally record-breaking quantity of margin debt that had been incurred within the course of. Cash borrowed to spend money on shares topped $1 trillion in August.

For Brian Jacobs of Aptus Capital, nevertheless, this isn’t the five-alarm fireplace it sounds and is much less ominous than buyers would possibly suspect. Economist David Rosenberg posted on X a couple of weeks again that the quantity was “fairly scary” however Jacobs contends it’s merely a coincident indicator, a symptom of the market’s meteoric rise, moderately than a sign of its imminent demise.

Jacobs writes in a latest funding weblog: “It (margin debt) strikes with the market. When equities rise, account values enhance, and buyers naturally tackle extra leverage. Margin debt rising 25% over the past yr? The S&P 500 SPX is up about the identical. Margin debt has nearly doubled over the past 5 years? The S&P 500 is up about the identical.”

However having mentioned that, whereas a crude take a look at margin debt ranges could not do greater than show that shares have gone up so much, and rapidly of late, different methods of parsing margin borrowing do paint a worrisome image. On the finish of September, Cory McPherson at Professional-Lively Capital printed Margin Debt Exhibiting Buyers Going All In. Key sections:

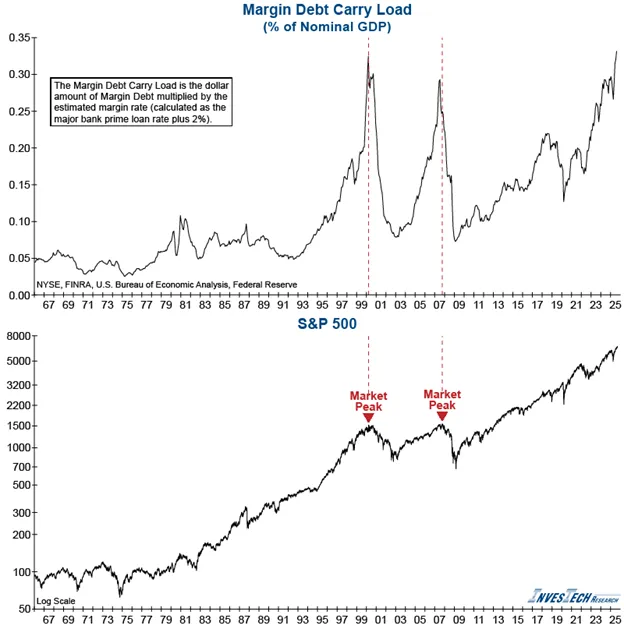

From the August [2025] numbers, margin debt relative to nominal GDP sits at 3.48%. The document excessive studying was 3.97% in October 2021. For historic context although, the height in that ratio was 2.6% within the dot-com bubble days in 2000, and a couple of.5% in 2007 earlier than the nice recession.

One other manner to have a look at is Margin Debt Carry Load. This components within the curiosity being paid on the margin debt. The chart beneath reveals the greenback quantity of margin debt multiplied by the estimated margin price, which is calculated as the most important financial institution prime price plus 2%. That is then put in % of nominal GDP. You’ll be able to see we have now now reached ranges seen over the last levels of the dot-com bubble days in 2000. Margin debt, although, is certainly not a timing indicator. This could proceed to get larger and better, simply because the inventory market can. What it may well do, although, is create violent downturns available in the market. When an investor owns inventory on margin and that inventory goes down a specific amount, the brokerage forces the investor to promote, which might create an elevator down have an effect on, much like what we noticed in April of this yr.

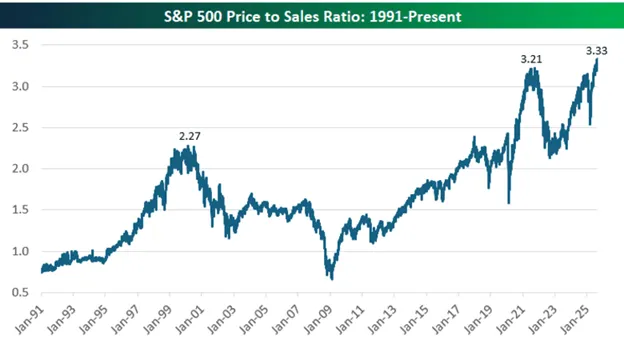

A basic metric on the inventory market has additionally reached excessive heights not too long ago. The value to gross sales ratio is a valuation metric that compares an organization’s inventory worth to its income. Mainly, a measure of what buyers are keen to pay for every greenback of gross sales from an organization. In wanting on the worth to gross sales ratio of the S&P 500 (taking the market cap of the S&P 500 and dividing by the overall gross sales of all corporations within the S&P 500 over the previous 12 months), you’ll be able to see we’ve surpassed final yr’s and 2021’s peak within the ratio. It’s also well beyond the height that was seen within the dot-com bubble days, which is regarded as one in all if not the largest inventory market bubbles in historical past. A lot of that is being pushed after all by know-how shares and the AI increase we’ve seen over the previous few years. Inventory costs have gotten manner forward of precise gross sales. Whereas overvaluation doesn’t trigger market drops or bear markets, they do typically precede them.

McPherson then considers some actual economic system information anomalies, that the massive downward jobs revision occurred with no recession, and that the Convention Boards main indicators have been falling for 3 years whereas its coincident indicator continues to rise. Evidently working very massive fiscal deficits for some time can produce complicated outcomes.

The rationale for concern about inventory market froth is moderately so much is using on it. We identified that US households’ inventory holding relative to different monetary belongings was at an all time excessive:

⚠️That is really INSANE:

US households now personal a RECORD 52% of their monetary belongings in equities.

This share has greater than DOUBLED because the Nice Monetary Disaster and surpassed the 2000 Dot-Com Bubble by ~5 factors.

The maintain simply 15% in money and 14% in debt belongings. pic.twitter.com/6DRmtxYSze

— International Markets Investor (@GlobalMktObserv) October 13, 2025

Overseas buyers have additionally wagered so much within the US on line casino. The Economist has simply posted, Gita Gopinath on the crash that would torch $35trn of wealth. From Gopinath, the previous chief economist of the IMF:

Over the previous decade and a half, American households have considerably elevated their holdings within the stockmarket, inspired by sturdy returns and the dominance of American tech corporations. Overseas buyers, notably from Europe, have for a similar causes poured capital into American shares, whereas concurrently benefiting from the greenback’s power. This rising interconnectedness signifies that any sharp downturn in American markets will reverberate world wide.

To place the potential influence in perspective, I calculate {that a} market correction of the identical magnitude because the dotcom crash might wipe out over $20trn in wealth for American households, equal to roughly 70% of American GDP in 2024. That is a number of instances bigger than the losses incurred through the crash of the early 2000s. The implications for consumption could be grave. Consumption progress is already weaker than it was previous the dotcom crash. A shock of this magnitude might lower it by 3.5 proportion factors, translating right into a two-percentage-point hit to total GDP progress, even earlier than accounting for declines in funding.

The worldwide fallout could be equally extreme. Overseas buyers might face wealth losses exceeding $15trn, or about 20% of the remainder of the world’s GDP. For comparability, the dotcom crash resulted in overseas losses of round $2trn, roughly $4trn in in the present day’s cash and fewer than 10% of rest-of-world GDP on the time. This stark enhance in spillovers underscores how weak world demand is to shocks originating in America.

Traditionally, the remainder of the world has discovered some cushion within the greenback’s tendency to rise throughout crises. This “flight to security” has helped mitigate the influence of misplaced dollar-denominated wealth on overseas consumption. The buck’s power has lengthy offered world insurance coverage, typically appreciating even when the disaster originates in America, as buyers search refuge in greenback belongings.

There are, although, causes to imagine that this dynamic could not maintain within the subsequent disaster. Regardless of well-founded expectations that American tariffs and expansionary fiscal coverage would bolster the greenback, it has as an alternative fallen towards most main currencies…

Compounding the state of affairs, and including to the general danger, is the escalation of the tariff wars. Additional tit-for-tat tariffs between America and China would injury not simply their bilateral commerce however world commerce too, as nearly all international locations are uncovered to the world’s two largest economies through advanced provide chains. Extra usually, avoiding chaotic or unpredictable coverage selections, together with those who threaten central-bank independence, is important to stop a market collapse…

In sum, a market crash in the present day is unlikely to end result within the transient and comparatively benign financial downturn that adopted the dotcom bust. There may be much more wealth on the road now—and far much less coverage area to melt the blow of a correction. The structural vulnerabilities and macroeconomic cont

Ouch. However you’ll be able to see why we’re watching with bated breath.

[ad_2]