[ad_1]

Aura Minerals Inc. (NASDAQ: AUGO) (B3: AURA33) (“Aura” or the “Firm”) broadcasts that it has filed its audited consolidated monetary statements and earnings launch (collectively, “Monetary and Operational Outcomes”) for the interval ended September 30, 2025. The complete model of the Monetary and Operational Outcomes could be considered on the Firm’s web site at www.auraminerals.com, on SEDAR+ at www.sedarplus.ca. or on SEC www.sec.com.

“In Q3 2025, Aura achieved a file manufacturing of 74,227 GEO at fixed costs and an all-time excessive Adjusted EBITDA of US$152 million, contributing to a trailing twelve-month Adjusted EBITDA of US$419 million at a median realized gold value of US$3,068/oz. This efficiency, bolstered by a realized gold value of US$3,385/ozand Recurring Free Money Movement of US$115 million within the quarter —up 91% from Q2 2025—was pushed by robust operational outcomes throughout our mines and the profitable begin of economic manufacturing at Borborema in September 2025, constructed on time and on price range with zero Misplaced Time Incidents. Our price self-discipline – AISC decreased by 4% in comparison with Q2 2025 – and Aura 360 dedication enabled us to take care of sturdy monetary efficiency. We stay targeted on delivering constant shareholder worth by way of our quarterly dividend, advancing the MSG acquisition, and attaining our 2025 manufacturing and value steerage of 266,000-300,000 GEO, ” commented Rodrigo Barbosa President and CEO of Aura.

Operational & Monetary Headlines Q3 2025 and 9M 2025

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Complete Manufacturing (GEO) | 74,227 | 64,033 | 16 | % | 68,246 | 9 | % | 198,346 | 200,759 | -1 | % | |||||

| Complete Gross sales (GEO) | 74,907 | 62,452 | 20 | % | 67,069 | 12 | % | 197,850 | 200,517 | -1 | % | |||||

| Web Income | 247,832 | 190,436 | 30 | % | 156,157 | 59 | % | 600,072 | 422,646 | 42 | % | |||||

| Gross Revenue | 149,609 | 103,939 | 44 | % | 72,181 | 107 | % | 331,976 | 170,171 | 95 | % | |||||

| Gross Margin | 60 | % | 55 | % | 6p.p. | 46 | % | 14p.p. | 55 | % | 40 | % | 15p.p. | |||

| Adjusted EBITDA | 152,105 | 106,224 | 43 | % | 77,974 | 95 | % | 339,808 | 186,813 | 82 | % | |||||

| Adjusted EBITDA Margin | 61 | % | 56 | % | 6p.p. | 50 | % | 11p.p. | 57 | % | 44 | % | 12p.p. | |||

| Web Revenue | 5,626 | 8,147 | -31 | % | (11,923 | ) | -147 | % | (59,476 | ) | (46,915 | ) | -27 | % | ||

| Web Revenue Margin | 2 | % | 4 | % | -2p.p. | -8 | % | 10p.p. | -10 | % | -11 | % | 1p.p. | |||

| Adjusted Web Revenue | 68,672 | 36,834 | 86 | % | 21,650 | 217 | % | 132,409 | 44,630 | 197 | % | |||||

| Money Value (US$/GEO) | 1,110 | 1,146 | -3 | % | 987 | 12 | % | 1,133 | 1,022 | 11 | % | |||||

| All In Sustaining price (US$/GEO) | 1,396 | 1,449 | -4 | % | 1,292 | 8 | % | 1,433 | 1,302 | 10 | % | |||||

| Working Money Movement | 93,096 | 79,865 | 17 | % | 76,770 | 21 | % | 214,189 | 156,233 | 37 | % | |||||

| Web Debt/LTM EBITDA | 0.15x | 0.81x | -0.66x | 0.63x | -0.48x | 0.15x | 0.63x | -0.48x | ||||||||

| Complete CAPEX | 31,605 | 50,325 | -37 | % | 60,483 | -48 | % | 133,655 | 113,761 | 17 | % | |||||

Besides as in any other case famous on this doc, references herein to “US$” or and “$” are to hundreds of United States {dollars}

Headlines

- Complete manufacturing in Q3 2025 reached 74,227 gold equal ounces (“GEO”), 16% larger than Q2 2025 and likewise 9% larger when in comparison with Q3 2024 at present steel costs. At fixed costs, Aura’s quarterly manufacturing was a file excessive, rising by 17% in comparison with Q2 2025 and rising 15% over Q3 2024. This consequence was achieved primarily attributable to:

- The rise manufacturing at Almas from 12,917 GEO in Q2 2025 to fifteen,088 GEO in Q3 2025 (+17%), attributable to larger ore processed volumes, reflecting the outcomes of the plant enlargement at Almas, and improved grades attributable to mine sequencing;

- The primary full quarter of manufacturing at Borborema and its achievement of economic manufacturing, producing 10,219 GEO in Q3 2025 (vs. 2,577 GEO in Q2 2025); and

- The dependable productions at Apoena, Aranzazu and Minosa, which, mixed, remained steady in Q3 2025 in comparison with Q2 2025

In 9M 2025, the whole manufacturing reached 198,346 GEO at present costs in keeping with the identical interval of 2024. At 2025 Manufacturing Steering Costs, the 9M 2025 manufacturing was 203,592 GEO, 3% above 9M 2024, and on observe to realize the 2025 steerage.

- Gross sales volumes have been 74,907 in GEO this quarter, a rise of 10% in comparison with Q3 2024 and a rise of 20% in comparison with the earlier quarter at present costs quarter, primarily as results of improve in manufacturing.

- Web Revenues reached a file excessive of US$247,832 in Q3 2025, representing a rise of 59% in comparison with Q3 2024 and a rise of 30% when in comparison with Q2 2025, primarily attributable to larger gold value and the rise in gross sales volumes. In 9M 2025, revenues reached US$600,072, a rise of 42% in comparison with the identical interval of 2024.

- Common internet realized gold sale costs elevated by 6% in Q3 2025 in comparison with Q2 2025, with a median of US$3,385/ozwithin the quarter. In comparison with Q3 2024, common internet realized gold sale costs elevated 40% (US$2,413). In 9M 2025, common internet realized gold sale costs reached US$3,146, a 43% improve when in comparison with 9M 2024.

- Common copper sale costs elevated 6% in comparison with Q2 2025, with a median of US$4.74/lb within the quarter and was 13% larger in comparison with the identical interval in 2024. In 9M 2025, common copper sale costs reached US$4.49, an 8% improve when in comparison with 9M 2024.

- Adjusted EBITDA reached one other file excessive of US$152,105 in Q3 2025, marking the fifth consecutive quarterly file reported by Aura. The rise was pushed by a mixture of upper steel costs, money prices underneath management (as additional defined under) and improve in manufacturing and gross sales volumes. When in comparison with Q3 2024, Adjusted EBITDA reached a 95% improve. In 9M 2025, Adjusted EBITDA elevated by 82%, for a similar causes.

- AISC for Q3 2025 was US$1,396/GEO, a lower by 4% when in comparison with Q2 2025 (US$1,449/GEO), primarily attributable to higher efficiency at Almas (AISC of US$ 1,128/GEO) attributable to larger ore processed and higher grades and improved waste-to-ore ration attributable to mine sequencing, and as results of the beginning of operations at Borborema, which whereas but in a ramp-up had a lower-than-average AISC profile and recorded an AISC of US$ 1,237/Oz. When in comparison with Q3 2024, the AISC elevated 8% over Q3 2024 at present costs, primarily attributable to Aranzazu, which was negatively impacted by the conversion of copper into GEO because of the sharp improve in gold costs within the interval . At fixed Q3 2024 steel costs, AISC would have been in line in comparison with Q3 2024. In 9M 2025, AISC reached US$1,419, an 8% improve when in comparison with 9M 2024 at present costs and three% improve in fixed costs.

- The Firm’s Web Debt reached US$63,772 by Q3 2025 a 77% lower in comparison with Q2 2025 and likewise a lower of 56% when in comparison with the identical interval of 2024, attributable to (i) larger money place because of the internet proceeds from Nasdaq IPO of US$200.1 million, (ii) robust Recurring Free Money Flows, and (ii) the numerous discount within the CAPEX 18.7 million, from US$50.3 million, in Q2 2025 to US$31.6million, a 37% lower, principally because of the conclusion of the Borborema development. The web debt-to-last 12 months Adjusted EBITDA ratio lowered to 0.15x on the finish of Q3 2025, from 0.81x on the finish of Q2 2025.

OTHER UPDATES:

Train of the Underwriters’ Choice to Buy Extra Shares: In August 2025, Aura closed the sale of 897,134 frequent shares for roughly US$21.8 million on account of the partial train of the underwriters’ choice to buy further shares granted to them in reference to the U.S. Preliminary Public Providing on the public providing value of US$24.25 per frequent share, much less underwriting reductions and commissions.

Delist from Toronto Inventory Trade (TSX): On September eighth, 2025, Aura determined to pursue the Delisting of the Widespread Shares from the TSX following the completion of itemizing its Widespread Shares on Nasdaq on July sixteenth, 2025, together with its intention to consolidate the buying and selling within the U.S. fairness market, which the Firm expects will enhance its inventory liquidity. This modification was accredited by the Brazilian Securities Fee (“Comissão de Valores Mobiliários” or “CVM”), because it doesn’t have an effect on the rights of holders of BDRs listed on the São Paulo Inventory Trade (B3 S.A. – Brasil, Bolsa, Balcão) underneath the image “AURA33”, which continued to be supported by Widespread Shares, listed on Nasdaq. This modification took impact on September 5, 2025 and the shares have been now not traded on the TSX as of September 25, 2025.

Borborema business manufacturing : On September twenty third, 2025, Aura introduced the start of Borborema gold mine business manufacturing. The Borborema mine mill operates above 80% of the design capability, processing 4,500 tonnes per day, with recoveries constantly above 90% and ranging as much as 92%. The mine offered in Q3 2025 a complete of 10,095 GEO. Borborema is poised to grow to be a cornerstone asset for Aura, anticipated to ship the second highest annual gold manufacturing among the many Firm’s 5 working mines. In-built simply 19 months with zero misplaced time incidents, the challenge exemplifies Aura’s dedication to growing easy, scalable, and environment friendly operations. It additionally units a benchmark in ESG efficiency, incorporating renewable power sources and using gray water from the native municipality.

Incentive Program for the Conversion of BDRs into Shares: In October 2025, Aura introduced to the holders of the Firm’s Brazilian Depositary Receipts (“BDRs”) the launch of the Incentive Program for the conversion of BDRs into frequent shares (“Incentive Program”), underneath which holders could request the conversion of their BDRs (“AURA33”) into the underlying frequent shares (“AUGO”) listed on Nasdaq (“frequent shares”), at a ratio of three to at least one, with out being required to pay the relevant charges charged by Banco Bradesco. The Incentive Program is offered for a hard and fast interval of 32 days, from October 6, 2025, to November 6, 2025 (“Subsidy Interval”).

Outcomes Teleconference:

Date : November 5, 2025

Time : 10 a.m. (Brasília) | 8 a.m. (New York and Toronto)

Hyperlink to entry : Click on right here

2. Consolidated Monetary Outcomes

By way of manufacturing and gross sales, for all belongings besides Aranzazu, references herein to “GEO” are equal to precise gold ounces.

2.1 Complete Manufacturing and Gross sales (GEO)

| (GEO) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | |||

| Manufacturing | |||||||||||

| Aranzazu | 21,534 | 22,281 | -3 | % | 24,486 | -12 | % | 64,271 | 74,196 | -13 | % |

| Apoena | 9,248 | 8,219 | 13 | % | 8,035 | 15 | % | 26,343 | 30,052 | -12 | % |

| Minosa | 18,138 | 18,039 | 1 | % | 20,750 | -13 | % | 53,831 | 59,078 | -9 | % |

| Almas | 15,088 | 12,917 | 17 | % | 14,975 | 1 | % | 41,107 | 37,459 | 10 | % |

| Borborema | 10,219 | 2,577 | 297 | % | 0 | N.A. | 12,796 | 0 | N.A. | ||

| Complete | 74,227 | 64,033 | 16 | % | 68,246 | 9 | % | 198,346 | 200,785 | -1 | % |

| (GEO) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | |||

| Gross sales | |||||||||||

| Aranzazu | 21,514 | 22,290 | -3 | % | 23,380 | -8 | % | 64,260 | 74,269 | -13 | % |

| Apoena | 9,249 | 8,219 | 13 | % | 7,957 | 16 | % | 26,876 | 29,075 | -8 | % |

| Minosa | 17,827 | 17,836 | 0 | % | 20,757 | -14 | % | 53,189 | 59,723 | -11 | % |

| Almas | 15,089 | 12,917 | 17 | % | 14,975 | 1 | % | 41,107 | 37,450 | 10 | % |

| Borborema | 11,228 | 1,190 | 843 | % | 0 | N.A. | 12,418 | 0 | N.A. | ||

| Complete | 74,907 | 62,452 | 20 | % | 67,069 | 12 | % | 197,850 | 200,517 | -1 | % |

Applies the steel sale costs in Aranzazu realized throughout Q3 2025: Copper value = US$4.45/lb; Gold Value = US$3,477/oz; Silver Value = US$40.03/ozand Molybdenum Value = US$25.02/oz.

Complete manufacturing in Q3 2025 reached 74,227 gold equal ounces (“GEO”), 16% larger than Q2 2025 and 9% larger when in comparison with Q3 2024 at present steel costs, primarily attributable to detrimental affect from the copper-to-GEO conversion at Aranzazu. At fixed costs, Aura’s quarterly manufacturing was file excessive, rising by 17% in comparison with Q2 2025 and 15% above Q3 2024. When in comparison with the final quarter, the consequence was primarily attributable to stronger operational efficiency pushed by larger ore processed volumes and improved grades at Almas and the manufacturing improve of Borborema.

Throughout the quarter, Aura introduced the start of economic operation of Borborema — anticipated to be one of many Firm’s largest and lowest money price operations. Within the quarter, Borborema’s manufacturing totaled 10,219 GEO.

In 9M 2025, manufacturing reached 198,346 GEO, representing a 1% decline in present steel costs. At fixed costs — which neutralize the impact of copper value fluctuations within the GEO conversion at Aranzazu —manufacturing had a rise of 5% over the 185,979 GEO produced in 9M 2024, additionally attributable to Borborema manufacturing and Almas enhancements. At 2025 Manufacturing Steering Costs, the 9M 2025 manufacturing was 203,592 GEO, 3% above 9M 2024, and on observe to realize the 2025 steerage.

At present steel costs, manufacturing in Q3 2025 represents 75% of the decrease finish and 66% of the higher finish of the full-year steerage. At 2025 Manufacturing Steering Costs, the 9M 2025 manufacturing was 203,592 GEO, representing 77% of the decrease finish and 68% of the higher finish of the full-year steerage. This efficiency reinforces the Firm’s confidence in attaining its 2025 steerage.

2.2. Web Income

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change % |

9M 2025 | 9M 2024 | Change % | |||

| Aranzazu | 67,094 | 62,508 | 36 | % | 50,721 | 32 | % | 179,864 | 144,123 | 25 | % |

| Apoena | 31,223 | 26,711 | 67 | % | 19,250 | 64 | % | 84,287 | 64,249 | 31 | % |

| Minosa | 59,204 | 55,776 | 41 | % | 49,184 | 20 | % | 163,042 | 128,793 | 27 | % |

| Almas | 51,329 | 41,751 | 112 | % | 37,002 | 39 | % | 130,207 | 85,481 | 52 | % |

| Borborema | 38,982 | 3,690 | N.A. | – | N.A. | 42,672 | – | N.A. | |||

| Complete | 247,832 | 190,436 | 85 | % | 156,157 | 59 | % | 600,072 | 422,646 | 42 | % |

In Q3 2025, the Firm reported Web Income of US$247.8 million, representing a 59% improve year-over-year and a 30% improve in comparison with Q2 2025. The robust efficiency was primarily pushed by the gross sales improve and better steel costs, with the typical realized gold value rising by 40%, from US$2,413/ozin Q3 2024 to US$3,385/ozin Q3 2025. Copper costs additionally contributed positively, with the typical copper value rising by 13%, from US$4.18/lb in Q3 2024 to US$4.74/lb in Q3 2025. In comparison with the final quarter, molybdenum common realized sale value additionally elevated by 15%, reaching US$25/lb.

With this consequence, Web Revenues reached US$600,072 in 9M 2025, a rise of 42% when in comparison with the identical interval of 2024. The consequence was primarily pushed by larger gold costs, larger gross sales at Almas and of the beginning of operations at Borborema. In 9M 2025, common internet realized costs reached US$3,146, a 43% improve when in comparison with 9M 2024; and common copper costs reached US$4.49/lb, an 8% improve when in comparison with 9M 2024.

2.3. Money Value and All in Sustaining Prices

| (US$/GEO) | Q3 2025 | Q2 2025 | QoQ Change% |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | |||

| Money Value | 1,110 | 1,146 | -3 | % | 987 | 12 | % | 1,133 | 1,022 | 11 | % |

| Aranzazu | 1,133 | 1,110 | 2 | % | 997 | 14 | % | 1,135 | 960 | 18 | % |

| Apoena | 1,082 | 1,168 | -7 | % | 1,095 | -1 | % | 1,159 | 983 | 18 | % |

| Minosa | 1,192 | 1,178 | 1 | % | 998 | 20 | % | 1,173 | 1,090 | 8 | % |

| Almas | 986 | 1,167 | -16 | % | 899 | 10 | % | 1,069 | 1,065 | 0 | % |

| Borborema | 1,127 | 936 | 20 | % | – | N.A. | 1,109 | – | N.A. | ||

| All-in Sustaining Value | 1,396 | 1,449 | -4 | % | 1,292 | 8 | % | 1,433 | 1,302 | 10 | % |

| Aranzazu | 1,511 | 1,514 | 0 | % | 1,338 | 13 | % | 1,523 | 1,269 | 20 | % |

| Apoena | 1,791 | 1,751 | 2 | % | 1,888 | -5 | % | 1,867 | 1,607 | 16 | % |

| Minosa | 1,372 | 2,292 | -40 | % | 1,089 | 26 | % | 1,305 | 1,176 | 11 | % |

| Almas | 1,128 | 1,364 | -17 | % | 1,182 | -5 | % | 1,223 | 1,330 | -8 | % |

| Borborema | 1,237 | 1,441 | -14 | % | – | 0 | % | 1,256 | – | 0 | % |

For Q3 2025, the Firm’s Money Value was US$1,110/GEO, a rise of 12% over Q3 2024 primarily attributed to the rise in prices at Aranzazu, attributable to affect from the copper-to-GEO conversion in manufacturing, and decrease manufacturing at Minosa. When in comparison with Q2 2025, Money Value was 3% decrease, attributable to enhancements at Almas and Apoena pushed by larger grades and better restoration charges, respectively, partially offset by larger prices at Aranzazu and Borborema.

In 9M 2025, Money Value averaged US$1,133/GEO, representing an 11% improve, primarily attributable to decrease grades at Apoena and better waste to ore ratio and the affect of the copper into GEO conversion at Aranzazu. This consequence was additionally impacted by decrease stacking at Minosa attributable to larger rainfall in 2025 than 2024, because of the unusually low rain season in Minosa in 2024. At fixed 2024 steel costs, Money Value of 9M 2025 was US$1,060/GEO, a 4% improve.

In Q3 2025, consolidated All-in Sustaining Value (AISC) was US$1,396/GEO, up 8% from Q3 2024 attributable to larger Money Prices and partially defined by the detrimental affect of steel costs on GEO conversion. At Q3 2024 fixed steel costs, AISC was in keeping with Q3 2024. For 9M 2025, AISC was US$1,419/GEO, a 9% improve from 9M 2024, primarily attributable to copper-to-GEO conversion. In comparison with Q2 2025, AISC lowered 4% because of the constructive efficiency of Almas and decrease than Aura’s common AISC for Borborema.

2.4. Gross Revenue

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change% |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change% | ||||||||

| Web Income | 247,832 | 190,436 | 30 | % | 156,157 | 59 | % | 600,072 | 422,646 | 42 | % | |||||

| Value of products offered | (98,223 | ) | (86,497 | ) | 14 | % | (83,976 | ) | 17 | % | (268,096 | ) | (252,475 | ) | 6 | % |

| Value of manufacturing | (44,745 | ) | (44,470 | ) | 1 | % | (29,838 | ) | 50 | % | (134,134 | ) | (104,899 | ) | 28 | % |

| Value of manufacturing – Contractors | (26,437 | ) | (17,529 | ) | 51 | % | (27,481 | ) | -4 | % | (59,433 | ) | (69,861 | ) | -15 | % |

| Change in stock (money) | (11,983 | ) | (9,550 | ) | 25 | % | (9,971 | ) | 20 | % | (30,659 | ) | (30,138 | ) | 2 | % |

| Depreciation and amortization | (15,058 | ) | (14,948 | ) | 1 | % | (16,686 | ) | -10 | % | (43,870 | ) | (47,577 | ) | -8 | % |

| Gross Revenue | 149,609 | 103,939 | 44 | % | 72,181 | 107 | % | 331,976 | 170,171 | 95 | % | |||||

| Gross Margin | 60 | % | 55 | % | 6 p.p. | 46 | % | 14 p.p. | 55 | % | 40 | % | 15 p.p. | |||

Within the quarter, Value of products offered (COGS) was instantly impacted by the inclusion of Borborema and mirrored a rise of 14% in comparison with Q2 2025 and 17% versus Q3 2024. In Q3 2025, Borborema accounted for US$12.9 million in prices. Excluding this affect, complete COGS for the quarter would have been roughly US$85.6 million, in step with Q2 2025 ranges. For 9M 2025, complete COGS rose 6%, additionally pushed by Borborema’s begin up, which represented US$13.8 million of the whole. Excluding Borborema, price improve versus 2024 would have been round 1%, demonstrating that, underneath comparable circumstances, the Firm maintained steady prices, reflecting Aura’s disciplined price administration and operational effectivity.

In Q3 2025, disciplined price administration, aligned with Q3 2024 on a comparable foundation, and a big rise in Web Income drove Gross Revenue to US$149.6 million, attaining a Gross Margin of 60%. This represents a greater than twofold improve from the US$72.2 million Gross Revenue in Q3 2024. For 9M 2025, Gross Revenue reached US$332.0 million, almost doubling the 9M 2024 determine, propelled by price containment methods and a 42% improve in Web Income for the explanations mentioned.

2.5. Working Bills

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Gross Revenue | 149,609 | 103,939 | 44 | % | 72,181 | 107 | % | 331,976 | 170,171 | 95 | % | |||||

| Operational Bills | (12,704 | ) | (12,998 | ) | -2 | % | (11,216 | ) | 13 | % | (36,714 | ) | (31,920 | ) | 15 | % |

| Basic and administrative bills | (10,371 | ) | (11,284 | ) | -8 | % | (6,923 | ) | 50 | % | (31,291 | ) | (22,734 | ) | 38 | % |

| Exploration bills | (2,333 | ) | (1,714 | ) | 36 | % | (4,293 | ) | -46 | % | (5,423 | ) | (9,186 | ) | -41 | % |

| Working earnings | 136,905 | 90,941 | 51 | % | 60,965 | 125 | % | 295,262 | 138,251 | 114 | % |

Working Bills totaled US$12.7 million within the quarter, 2% decrease than Q2 2025 and 13% larger than Q3 2024.

Basic and Administrative (“G&A”) bills decreased by 8% in comparison with Q2 2025, primarily reflecting the absence of sure non-recurring bills associated to the Nasdaq IPO incurred within the earlier quarter. When in comparison with Q3 2024, G&A bills elevated by US$3.5 million, primarily attributable to: (i) larger stock-based compensation (non-cash) and Deferred Share Unit (“DSU”) bills, pushed by the numerous appreciation within the Firm’s share value throughout the interval; (ii) elevated Administrators and Officers (“D&O”) insurance coverage premiums following the Nasdaq itemizing; and (iii) a rise in different normal and administrative prices.

For the 9 months ended September 30, 2025, the rise in G&A bills was pushed by the identical elements, in addition to larger salaries and advantages {and professional} charges related to the acquisition and incorporation of Period Dorada, the start-up of Borborema, and actions associated to the Nasdaq IPO.

Exploration bills totaled US$2.3 million in Q3 2025, a 36% improve in comparison with Q2 2025 and 46% discount from Q3 2024, as most bills associated to exploration actions within the quarter have been capitalized. Exploration actions within the quarter have been concentrated in Apoena. In Matupá, efforts have been targeted on increasing reserves in areas near X1, Pé Quente and different strategic areas. In Carajás, exploration work efficiently confirmed copper mineralization, increasing the mineral potential of the area.

The Firm thus ended Q3 2025 with Working Revenue of US$137.6 million, in comparison with an Working Revenue of US$90.9 million in Q3 2024, additionally larger in comparison with the Working Revenue of Q2 2025 of US$90.9 million, which displays a constructive results of larger gross revenue.

2.6. Adjusted EBITDA

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Working Revenue | 136,905 | 90,941 | 51 | % | 60,965 | 125 | % | 295,262 | 138,251 | 114 | % | |||||

| Depreciation and Amortization | 15,200 | 15,283 | -1 | % | 17,009 | -11 | % | 44,546 | 48,562 | -8 | % | |||||

| Adjusted EBITDA | 152,105 | 106,224 | 43 | % | 77,974 | 95 | % | 339,808 | 186,813 | 82 | % | |||||

| Adjusted EBITDA Margin | 61 | % | 56 | % | 6 p.p. | 50 | % | 11 p.p. | 57 | % | 44 | % | 12 p.p. | |||

Adjusted EBITDA reached a brand new all-time excessive of US$152.1 million in Q3 2025, marking the fifth consecutive quarterly file for Aura. The Firm’s improve in manufacturing, whereas sustaining disciplined price management, enabled it to totally seize the good thing about rising steel costs. In consequence, Adjusted EBITDA nearly doubled in comparison with Q3 2024 and grew 43% over Q2 2025.

The year-over-year enchancment was primarily pushed by larger manufacturing and gross sales volumes, robust price management and better gold and copper costs, as mentioned beforehand. This consequence was additionally famous on the EBITDA margin acquire of 6 p.p. in comparison with Q2 2025, supported not solely by stronger steel costs but in addition by a 20% improve in gross sales quantity.

In 9M 2025, Adjusted EBITDA reached US$339.8 million, representing an 82% improve in comparison with the identical interval in 2024. This consequence displays additionally the constructive affect of upper steel costs and will increase in manufacturing. In consequence, the Adjusted EBITDA margin expanded to 57%, up from 44% in 9M 2024.

2.7. Monetary End result

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| EBIT | 136,905 | 90,941 | 51 | % | 60,965 | 125 | % | 295,262 | 138,251 | 114 | % | |||||

| Monetary End result | (102,565 | ) | (59,630 | ) | 72 | % | (62,691 | ) | 64 | % | (283,806 | ) | (141,888 | ) | 100 | % |

| Accretion expense | (2,980 | ) | (1,134 | ) | 163 | % | (1,447 | ) | 106 | % | (5,780 | ) | (4,553 | ) | 27 | % |

| Lease curiosity expense | (824 | ) | (161 | ) | 412 | % | (2,758 | ) | -70 | % | (2,580 | ) | (6,779 | ) | -62 | % |

| Curiosity expense on loans and debentures | (5,786 | ) | (6,098 | ) | -5 | % | (7,278 | ) | -21 | % | (17,639 | ) | (15,616 | ) | 13 | % |

| Finance price on post-employment profit | (535 | ) | (747 | ) | -28 | % | (415 | ) | 29 | % | (1,620 | ) | (1,249 | ) | 30 | % |

| Unrealized loss with spinoff gold collars | (75,252 | ) | (24,304 | ) | 210 | % | (56,267 | ) | 34 | % | (199,766 | ) | (89,493 | ) | 123 | % |

| Realized loss with spinoff gold collars | (17,130 | ) | (11,703 | ) | 46 | % | – | N.A. | (34,869 | ) | – | N.A. | ||||

| Loss on different spinoff transactions | (685 | ) | (1,305 | ) | -48 | % | (1,321 | ) | -48 | % | (3,817 | ) | (1,321 | ) | 189 | % |

| Change in legal responsibility measured at honest worth | (1,036 | ) | (4,025 | ) | -74 | % | – | N.A. | (7,420 | ) | (85 | ) | N.A. | |||

| Overseas trade | (36 | ) | (2,462 | ) | -99 | % | – | N.A. | (5,674 | ) | (10,995 | ) | -48 | % | ||

| By-product payment | – | – | N.A. | – | N.A. | – | (13,522 | ) | N.A. | |||||||

| Loss on settlement of legal responsibility with fairness devices | – | (8,768 | ) | N.A. | – | N.A. | (8,768 | ) | – | N.A. | ||||||

| Different finance prices | (585 | ) | (297 | ) | 97 | % | (476 | ) | 23 | % | (1,312 | ) | (1,047 | ) | 25 | % |

| Finance bills | (104,849 | ) | (61,004 | ) | 72 | % | (69,962 | ) | 50 | % | (289,245 | ) | (144,660 | ) | 100 | % |

| Change in legal responsibility measured at honest worth | – | – | N.A. | 3,502 | N.A. | – | – | N.A. | ||||||||

| Overseas trade | – | – | N.A. | 2,279 | N.A. | – | – | N.A. | ||||||||

| Curiosity earnings | 2,284 | 1,374 | 66 | % | 1,490 | 53 | % | 5,439 | 2,772 | 96 | % | |||||

| Finance earnings | 2,284 | 1,374 | 66 | % | 7,271 | -69 | % | 5,439 | 2,772 | 96 | % | |||||

| Different earnings (bills) | (822 | ) | 61 | N.A. | (359 | ) | 129 | % | (1,515 | ) | (952 | ) | 59 | % | ||

| Revenue/ (loss) earlier than earnings taxes | 33,518 | 31,372 | 7 | % | (2,085 | ) | N.A. | 9,941 | (4,589 | ) | N.A. | |||||

The Firm’s Monetary Lead to Q3 2025 was a lack of US$(102.6) million, following on from the US$(59.6) million loss in Q2 2025, impacted by:

- Unrealized loss on gold hedges in Q3 2025, arising from mark-to-market (MTM) changes associated to excellent gold hedge positions, reflecting improve in gold costs between the beginning and the tip of the quarter, coming from US$3,287.45 per Ozand reaching US$ 3,825.30 per Ozon the finish of the interval. In accordance with IFRS requirements, the Firm data MTM changes on the finish of every reporting interval for all excellent spinoff positions.

- Realized losses with gold hedges in Q3 2025 have been associated to money settlement of excellent gold collars throughout the quarter, pushed by the expiration of gold collars inside the quarter.

Most of Aura’s excellent gold collars (213,192 Oz out of about 214,442 Oz) are related to the longer term manufacturing of the Borborema and can expire between October/2025 and Jun/2028. As beforehand disclosed, about 80% of the manufacturing for the primary 3 years of the Borborema Venture is hedged at ceiling costs of US$2,400.

2.8. Web Revenue

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Revenue/ (loss) earlier than earnings taxes | 33,518 | 31,372 | 7 | % | (2,085 | ) | N.A. | 9,941 | (4,589 | ) | N.A. | |||||

| Complete taxes | (27,892 | ) | (23,225 | ) | 20 | % | (9,838 | ) | 293 | % | (69,417 | ) | (42,326 | ) | 64 | % |

| Present earnings tax expense | (38,402 | ) | (29,551 | ) | 30 | % | (11,833 | ) | 225 | % | (88,767 | ) | (36,588 | ) | 143 | % |

| Deferred earnings tax expense | 10,510 | 6,326 | N.A. | 1,995 | N.A. | 19,350 | (5,738 | ) | N.A. | |||||||

| Revenue/(loss) for the interval | 5,626 | 8,147 | -31 | % | (11,923 | ) | -147 | % | (59,476 | ) | (46,915 | ) | 27 | % | ||

| Web Margin | 2 | % | 4 | % | -2 p.p. | -8 | % | 10 p.p. | -10 | % | -11 | % | 1 p.p. | |||

| Unrealized loss with spinoff gold collars | (75,252 | ) | (24,304 | ) | 210 | % | (56,267 | ) | 34%. | (199,766 | ) | (89,493 | ) | 123 | % | |

| Overseas Trade | (36 | ) | (2,462 | ) | -99 | % | 2,279 | N.A. | (5,674 | ) | (10,995 | ) | -48 | % | ||

| Deferred taxes on non-monetary objects | 12,242 | 6,847 | 95 | % | 20,415 | -35 | % | 22,323 | 8,943 | 162 | % | |||||

| Loss on settlement of legal responsibility with fairness devices | – | (8,768 | ) | N.A. | – | N.A. | (8,768 | ) | – | N.A. | ||||||

| Adjusted Web Revenue | 68,672 | 36,834 | 86 | % | 21,650 | 217 | % | 132,409 | 44,630 | 197%. | ||||||

Web earnings in Q3 2025 was US$5.6 million, in comparison with Web Lack of US$(11.9) million in Q3 2024 and a Web earnings of US$8.1 million in Q2 2025. This consequence versus Q3 2024 occurred primarily attributable to larger working earnings, which elevated by 125% on account of income development, partially offset by larger monetary bills associated to gold spinoff losses and better present earnings taxes, as anticipated given the working earnings improve.

In 9M 2025, Web Loss reached US$(59.5) million, additionally primarily attributable to mark-to-market (MTM) changes on open gold hedging positions, pushed by improve in gold value between the beginning and the tip of the interval.

Adjusted Web Revenue

As results of improve within the Firm’s Working Revenue, adjusted internet earnings in Q3 2025 was US$68.7 million within the interval, in comparison with US$34.6 million in Q3 2024, excluding:

- Non-cash losses associated to gold hedges: US$(75.2) million

- FX losses: US$(0.36) million

- Deferred taxes over non-monetary objects US$12.2 million

3. Efficiency of the Working Models

3.1 Aranzazu

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Manufacturing at Fixed Costs (GEO)¹ | 21,534 | 21,805 | -1 | % | 20,648 | 4 | % | 62,046 | 59,399 | 4 | % | |||||

| Manufacturing at Present Costs (GEO) | 21,534 | 22,281 | -3 | % | 24,486 | -12 | % | 64,271 | 74,179 | -13 | % | |||||

| Gross sales (GEO) | 21,514 | 22,290 | -3 | % | 23,380 | -8 | % | 64,260 | 74,269 | -13 | % | |||||

| Money Value (US$/GEO) | 1,133 | 1,110 | 2 | % | 997 | 14 | % | 1,135 | 960 | 18 | % | |||||

| AISC (US$/GEO) | 1,511 | 1,514 | 0 | % | 1,338 | 13 | % | 1,523 | 1,269 | 20 | % | |||||

| Web Income | 67,094 | 62,508 | 7 | % | 50,721 | 32 | % | 179,864 | 144,123 | 25 | % | |||||

| Value of products offered | (29,631 | ) | (31,021 | ) | -4 | % | (32,036 | ) | -8 | % | (90,934 | ) | (90,166 | ) | 1 | % |

| Gross Revenue | 37,463 | 31,487 | 19 | % | 18,685 | 100 | % | 88,930 | 53,957 | 65 | % | |||||

| Bills | (2,459 | ) | (2,310 | ) | 6 | % | (1,952 | ) | 26 | % | (7,252 | ) | (6,962 | ) | 4 | % |

| Basic and administrative bills | (1,784 | ) | (1,516 | ) | 18 | % | (759 | ) | 135 | % | (5,074 | ) | (3,003 | ) | 69 | % |

| Exploration bills | (675 | ) | (794 | ) | -15 | % | (1,193 | ) | -43 | % | (2,178 | ) | (3,959 | ) | -45 | % |

| EBIT | 35,004 | 29,177 | 20 | % | 16,733 | 109 | % | 81,678 | 46,995 | 74 | % | |||||

| Adjusted EBITDA | 39,646 | 35,684 | 11 | % | 24,361 | 63 | % | 99,900 | 65,863 | 52 | % | |||||

| Monetary End result | (2,441 | ) | (4,292 | ) | -43 | % | (982 | ) | 149 | % | (7,339 | ) | (2,657 | ) | 176 | % |

| Monetary bills | (2,173 | ) | (3,762 | ) | -42 | % | (432 | ) | 403 | % | (5,969 | ) | (1,180 | ) | 406 | % |

| Different earnings (bills) | (268 | ) | (530 | ) | -49 | % | (550 | ) | -51 | % | (1,370 | ) | (1,477 | ) | -7 | % |

| EBT | 32,563 | 24,885 | 31 | % | 15,751 | 107 | % | 74,339 | 44,338 | 68 | % | |||||

| Complete taxes | (8,088 | ) | (12,532 | ) | -35 | % | (7,170 | ) | 13 | % | (28,003 | ) | (18,400 | ) | 52 | % |

| Present earnings tax expense | (10,248 | ) | (13,035 | ) | -21 | % | (7,057 | ) | 45 | % | (29,714 | ) | (19,348 | ) | 54 | % |

| Deferred earnings tax expense | 2,160 | 503 | 329 | % | (113 | ) | N.A. | 1,711 | 948 | 80 | % | |||||

| Revenue for the interval | 24,475 | 12,353 | 98 | % | 8,581 | 185 | % | 46,336 | 25,938 | 79 | % | |||||

Word: Applies the steel sale costs in Aranzazu realized throughout Q3 2025: Copper value = US$4.45/lb; Gold Value = US$3,477/oz; Silver Value = US$40.03/ozand Molybdenum Value = US$25.02/oz.

At Aranzazu, manufacturing reached 21,534 GEO, representing a 3% lower in comparison with the earlier quarter, ensuing primarily from steel costs since larger gold costs negatively affect the conversion to GEO. When in comparison with Q3 2024, manufacturing decreased by 12% additionally because of the sharp improve in gold costs between the durations which additionally impacted GEO conversion. At fixed costs, Aranzazu manufacturing was in line when in comparison with Q2 2025 (21,805 GEO) and 4% larger when in comparison with Q3 2024, additionally attributable to larger copper and silver grades, closing the quarter with copper grade of 1.55% and silver grade of twenty-two.26 g/tonne. Within the 9M 2025, complete manufacturing at present costs decreased by 13% in comparison with the earlier quarter, reaching 64,271, in keeping with the detrimental affect of the metals value conversion. At 9M 2024 fixed costs, Aranzazu produced 62,046 GEO, 4% larger than the identical interval of the earlier 12 months, primarily attributable to larger grades – round 4% of gold and silver, closing the interval with a median of 0.86 g/tonne and 22.24 g/tonne, respectively – and molybdenum manufacturing.

Aranzazu’s Web Income in Q3 2025 was US$67.1 million, up 7% from Q2 2025 and 32% from Q3 2024, primarily pushed by larger steel costs. Common gross sales costs rose quarter-over-quarter, with copper rising 3%, gold 6%, silver 19%, and molybdenum 15%. For 9M 2025, Aranzazu’s Web Income reached US$179.9 million, a 25% improve over 9M 2024, additionally attributed to elevated steel costs.

The Money Value was US$1,133/GEO for the quarter, 2% larger than Q2 2025 and 14% larger than Q3 2024, with barely decrease grades and restoration. In 9M 2025, Money Value elevated by 18%, with a complete of US$1,135/GEO, primarily impacted by the impact of steel costs within the conversion to GEO.

Aranzazu’s AISC was US$1,511 within the quarter, in step with Q2 2025 however up 13% from Q3 2024, primarily attributable to variations in steel costs and elevated G&A bills. At fixed Q3 2024 steel costs, AISC was US$1,273/GEO. For 9M 2025, AISC at fixed steel costs lowered 5% from 9M 2024.

Aranzazu’s Adjusted EBITDA was US$39.6 million in Q3 2025, reflecting an 11% improve from Q2 2025 and a 63% surge in comparison with Q3 2024, pushed by sturdy Web Income development from larger steel costs. For 9M 2025, Adjusted EBITDA totaled US$99.9 million, up 52% from 9M 2024, propelled by a 25% improve in Web Income, primarily from elevated steel costs and steady Value of Items Bought.

3.2 Apoena

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Manufacturing (GEO) | 9,248 | 8,219 | 13 | % | 8,035 | 15 | % | 26,343 | 30,052 | -12 | % | |||||

| Gross sales (GEO) | 9,249 | 8,219 | 13 | % | 7,957 | 16 | % | 26,876 | 29,075 | -8 | % | |||||

| Money Value (US$/GEO) | 1,082 | 1,168 | -7 | % | 1,095 | -1 | % | 1,159 | 983 | 18 | % | |||||

| AISC (US$/GEO) | 1,791 | 1,751 | 2 | % | 1,888 | -5 | % | 1,867 | 1,607 | 16 | % | |||||

| Web Income | 31,223 | 26,711 | 17 | % | 19,250 | 62 | % | 84,287 | 64,249 | 31 | % | |||||

| Value of products offered | (15,307 | ) | (14,270 | ) | 7 | % | (14,561 | ) | 5 | % | (44,681 | ) | (46,310 | ) | -4 | % |

| Gross Revenue | 15,916 | 12,441 | 28 | % | 4,689 | 239 | % | 39,606 | 17,939 | 121 | % | |||||

| Bills | (374 | ) | (998 | ) | -63 | % | (931 | ) | -60 | % | (2,797 | ) | (3,106 | ) | -10 | % |

| Basic and administrative bills | (292 | ) | (936 | ) | -69 | % | (802 | ) | -64 | % | (2,529 | ) | (2,807 | ) | -10 | % |

| Exploration bills | (82 | ) | (62 | ) | 32 | % | (129 | ) | -36 | % | (268 | ) | (299 | ) | -10 | % |

| EBIT | 15,542 | 11,443 | 36 | % | 3,758 | 314 | % | 36,809 | 14,833 | 148 | % | |||||

| Adjusted EBITDA | 20,735 | 16,151 | 28 | % | 9,645 | 115 | % | 50,432 | 32,691 | 54 | % | |||||

| Monetary End result | (5,402 | ) | (1,453 | ) | 272 | % | (5,220 | ) | 3 | % | (13,422 | ) | (11,570 | ) | 16 | % |

| Monetary bills | (5,386 | ) | (1,497 | ) | 260 | % | (5,441 | ) | -1 | % | (13,519 | ) | (11,881 | ) | 14 | % |

| Different earnings (bills) | (16 | ) | 44 | N.A. | 221 | N.A. | 97 | 311 | -69 | % | ||||||

| EBT | 10,140 | 9,990 | 2 | % | -1,462 | N.A. | 23,387 | 3,263 | 616.7 | % | ||||||

| Complete taxes | (717 | ) | (1,211 | ) | -41 | % | 1,486 | N.A. | (586 | ) | (2,021 | ) | -71 | % | ||

| Present earnings tax expense | (893 | ) | (862 | ) | 4 | % | (83 | ) | 976 | % | (2,418 | ) | (1,965 | ) | 23 | % |

| Deferred earnings tax expense | 176 | (349 | ) | N.A. | 1,569 | -89 | % | 1,832 | (56 | ) | N.A. | |||||

| Revenue for the interval | 9,423 | 8,779 | 7 | % | 24 | N.A. | 22,801 | 1,242 | N.A. | |||||||

In Q3 2025, Apoena manufacturing was 9,248 GEO, up 13% from Q2 2025, pushed by improved restoration charges of 95%. In comparison with Q3 2024, manufacturing rose 15%, fueled by larger restoration charges and elevated processed tonnage. For 9M 2025, manufacturing fell 12% versus 9M 2024, primarily attributable to elevated grades in 9M 2024, significantly in Q1 2024, from the high-grade Ernesto pit. Total, 2025 efficiency exceeded Firm expectations.

Apoena’s Web Income totaled US$31.2 million for Q3 2025, 17% larger than Q2 2025 and 62% above the Q3 2024, pushed primarily by elevated gross sales quantity and better gold costs. In 9M 2025, Apoena reached a Web Income of US$84.3 million, a rise of 31% in comparison with 9M 2024, supported by larger gold costs that partially offset decrease gross sales quantity throughout the interval.

The Money Value was US$1,082/GEO for the quarter, down 1% from Q3 2024 and seven% from Q2 2025. The quarter-over-quarter lower was primarily pushed by improved restoration charges, partially offset by a better strip ratio throughout the growth section. 12 months over 12 months, Apoena’s Money Value rose 18% to US$1,082/GEO in Q3 2025, pushed by an elevated waste-to-ore ratio from 6.56 tonnes in Q3 2024 to 19.04 tonnes in Q3 2025, mixed with decrease grades. For 9M 2025, All-in Sustaining Value elevated 16% to US$1,867/GEO, primarily attributable to decrease grades, in step with anticipated mine sequencing. In Q3 2025, Apoena’s AISC was US$1,791/GEO,principally steady in comparison with Q2 2025, because of the elevated lease bills.

Apoena’s Adjusted EBITDA in Q3 2025 reached US$20.7 million, a 115% improve from Q3 2024 and 28% larger than Q2 2025, pushed by a 62% rise in Web Income from larger gross sales quantity and gold costs. For 9M 2025, Adjusted EBITDA was US$50.4 million, up 54% from 9M 2024, supported by a 31% improve in Web Income from larger gold costs, regardless of an AISC attributable to decrease grades and mine sequencing.

3.3 Minosa

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Manufacturing (GEO) | 18,138 | 18,039 | 1 | % | 20,750 | -13 | % | 53,831 | 59,078 | -9 | % | |||||

| Gross sales (GEO) | 17,827 | 17,836 | 0 | % | 20,757 | -14 | % | 53,189 | 59,723 | -11 | % | |||||

| Money Value (US$/GEO) | 1,192 | 1,178 | 1 | % | 998 | 19 | % | 1,173 | 1,090 | 8 | % | |||||

| AISC (US$/GEO) | 1,378 | 1,292 | 7 | % | 1,089 | 27 | % | 1,307 | 1,176 | 11 | % | |||||

| Web Income | 59,204 | 55,776 | 6 | % | 49,184 | 20 | % | 163,042 | 128,793 | 27 | % | |||||

| Value of products offered | (22,486 | ) | (22,056 | ) | 2 | % | (21,809 | ) | 3 | % | (66,018 | ) | (69,022 | ) | -4 | % |

| Gross Revenue | 36,718 | 33,720 | 9 | % | 27,375 | 34 | % | 97,024 | 59,771 | 62 | % | |||||

| Bills | (2,031 | ) | (1,430 | ) | 42 | % | (1,648 | ) | 23 | % | (4,832 | ) | (4,040 | ) | 20 | % |

| Basic and administrative bills | (1,271 | ) | (1,166 | ) | 9 | % | (1,059 | ) | 20 | % | (3,572 | ) | (3,450 | ) | 4 | % |

| Exploration bills | (760 | ) | (264 | ) | 188 | % | (589 | ) | 29 | % | (1,260 | ) | (590 | ) | 114 | % |

| EBIT | 34,687 | 32,290 | 7 | % | 25,727 | 35 | % | 92,192 | 55,731 | 65 | % | |||||

| Adjusted EBITDA | 35,478 | 33,533 | 6 | % | 26,831 | 32 | % | 96,124 | 59,627 | 61 | % | |||||

| Monetary End result | (1,428 | ) | (1,189 | ) | 20 | % | (1,556 | ) | -8 | % | (4,173 | ) | (5,982 | ) | -30 | % |

| Monetary bills | (1,147 | ) | (1,442 | ) | -20 | % | (1,417 | ) | -19 | % | (3,901 | ) | (5,253 | ) | -26 | % |

| Different earnings (bills) | (281 | ) | 253 | N.A. | (139 | ) | 102 | % | (272 | ) | (729 | ) | -63 | % | ||

| EBT | 33,259 | 31,101 | 7 | % | 24,171 | 38 | % | 88,019 | 49,749 | 77 | % | |||||

| Complete taxes | (8,350 | ) | (7,425 | ) | 12 | % | (6,136 | ) | 36 | % | (21,993 | ) | (14,879 | ) | 48 | % |

| Present earnings tax expense | (8,725 | ) | (7,774 | ) | 12 | % | (6,352 | ) | 37 | % | (23,110 | ) | (14,860 | ) | 56 | % |

| Deferred earnings tax expense | 375 | 349 | 7 | % | 216 | 74 | % | 1,117 | (19 | ) | N.A. | |||||

| Revenue for the interval | 24,909 | 23,676 | 5 | % | 18,035 | 38 | % | 66,026 | 34,870 | 89 | % | |||||

In Q3 2025, Minosa produced 18,138 GEO, one other steady quarter and in line when in comparison with the earlier quarter, ensuing from larger grades processed throughout the quarter and better restoration fee, which achieved 68%. When in comparison with the identical quarter final 12 months, manufacturing decreased by 13%, attributable to decrease stacking in Q3 2025 in comparison with Q3 2024 attributable to larger rainfall in Q3 2025. Within the 9M 2025, manufacturing decreased 9% primarily attributable to decrease ore feed to the plant, reflecting mine sequencing and weather-related constraints, and was in step with Aura’s expectations.

Web Income totaled US$59.2 million in Q3 2025, up 6% from Q2 2025, whereas compared to Q3 2024 it grew 20%, primarily because of the improve within the value of gold over the interval. In 9M 2025, Web Income reached US$163.0 million, 27% larger than 9M 2024.

The Money Value was US$1,192/GEO in Q3 2025, 1% larger than Q2 2025 and 9% larger than Q3 2024, pushed by decrease manufacturing attributable to lowered stacking volumes. For 9M 2025, Money Value was US$1,173/GEO, an 8% improve from 9M 2024, attributed to decrease grades and barely elevated mine prices. The All-in Sustaining Value (AISC) for Q3 2025 was US$1,372/GEO, up 6% from Q2 2025 and 26% from Q3 2024, primarily attributable to larger Capital Expenditures (CAPEX). For 9M 2025, AISC was US$1,305/GEO, an 11% improve over 9M 2024, reflecting the mixed affect of decrease grades and elevated CAPEX.

In Q3 2025, Minosa’s Adjusted EBITDA reached US$35.5 million, up 32% from Q3 2024 and 5% from Q2 2025, pushed by larger gold costs, regardless of lowered manufacturing from decrease stacking volumes attributable to elevated rainfall and better CAPEX. For 9M 2025, Adjusted EBITDA was US$96.1 million, a 61% improve from 9M 2024, supported by elevated gold costs, although impacted by decrease grades, larger mine prices, and elevated CAPEX attributable to mine sequencing and climate constraints.

3.4 Almas

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Manufacturing (GEO) | 15,089 | 12,917 | 17 | % | 14,975 | 1 | % | 41,107 | 37,450 | 10 | % | |||||

| Gross sales (GEO) | 15,089 | 12,917 | 17 | % | 14,975 | 1 | % | 41,107 | 37,450 | 10 | % | |||||

| Money Value (US$/GEO) | 986 | 1,167 | -16 | % | 899 | 10 | % | 1,069 | 1,065 | 0 | % | |||||

| AISC (US$/GEO) | 1,132 | 1,364 | -17 | % | 1,182 | -4 | % | 1,225 | 1,330 | -8 | % | |||||

| Web Income | 51,329 | 41,751 | 23 | % | 37,002 | 39 | % | 130,207 | 85,481 | 52 | % | |||||

| Value of products offered | (18,147 | ) | (18,036 | ) | 1 | % | (15,569 | ) | 17 | % | (52,697 | ) | (46,977 | ) | 12 | % |

| Gross Revenue | 33,182 | 23,715 | 40 | % | 21,432 | 55 | % | 77,510 | 38,504 | 101 | % | |||||

| Bills | (1,595 | ) | (1,898 | ) | -16 | % | (941 | ) | 70 | % | (4,533 | ) | (2,938 | ) | 54 | % |

| Basic and administrative bills | (1,107 | ) | (1,475 | ) | -25 | % | (941 | ) | 18 | % | (3,385 | ) | (2,938 | ) | 15 | % |

| Exploration bills | (488 | ) | (423 | ) | 15 | % | – | N.A. | (1,148 | ) | – | N.A. | ||||

| EBIT | 31,587 | 21,817 | 45 | % | 20,491 | 54 | % | 72,977 | 35,566 | 105 | % | |||||

| Adjusted EBITDA | 34,525 | 24,709 | 40 | % | 22,931 | 51 | % | 81,661 | 43,993 | 86 | % | |||||

| Monetary End result | (2,426 | ) | (4,468 | ) | -46 | % | (1,371 | ) | 77 | % | (10,640 | ) | (5,877 | ) | 81 | % |

| Monetary bills | (2,421 | ) | (4,448 | ) | -46 | % | (1,345 | ) | 80 | % | (10,609 | ) | (5,832 | ) | 82 | % |

| Different earnings (bills) | (5 | ) | (20 | ) | -75 | % | (26 | ) | -81 | % | (31 | ) | (45 | ) | -31 | % |

| EBT | 29,161 | 17,349 | 68 | % | 19,120 | 52.5 | % | 62,337 | 29,689 | 110.0 | % | |||||

| Complete taxes | (8,478 | ) | (1,226 | ) | 892 | % | 4,194 | N.A. | (14.461 | ) | (4,123 | ) | 87 | % | ||

| Present earnings tax expense | (9,614 | ) | (7,101 | ) | 35 | % | 3,937 | N.A. | (22,713 | ) | 1,863 | N.A. | ||||

| Deferred earnings tax expense | 1,136 | 5,875 | -80 | % | 257 | 911 | % | 8,252 | (5,986 | ) | N.A. | |||||

| Revenue for the interval | 20,683 | 16,123 | 28 | % | 23,314 | -11 | % | 47,876 | 25,566 | 251 | % | |||||

Throughout Q3 2025, Almas produced 15,088 GEO, 17% larger than Q2 2025 (12,917 GEO), pushed by improved grades (1.01 g/ton vs. 0.94g/ton) and better ore processed volumes, reflecting the outcomes of the plant enlargement. Manufacturing was in line when in comparison with Q3 2024, because of the larger ore processed, because the grades decreased attributable to mine sequencing (1.21 g/ton in Q3 2024). Within the 9M 2025, manufacturing elevated 10%, pushed by a better quantity of ore processed, because of the plant capability enlargement.

Web Income was US$51.3 million in Q3 2025, up 39% from Q3 2024, pushed by elevated gross sales volumes, supported by larger ore processing from the plant enlargement, and elevated steel costs. In comparison with Q2 2025, Web Income rose 23%, primarily attributable to a big rise in gold costs and a 17% improve in manufacturing volumes. For 9M 2025, Web Income was US$130.2 million, a 52% improve from 9M 2024, fueled by larger gross sales volumes from enhanced operational capability and bigger tools, alongside larger steel costs.

The Money Value was US$986/GEO in Q3 2025, 10% larger than Q3 2024, pushed by decrease grades attributable to mine sequencing. In comparison with Q2 2025, Money Value fell 16%, attributed to a manufacturing plan with a decrease waste-to-ore (from 6.08 to 4.44) ratio and better grades (up 7% from 0.94 to 1.01). For 9M 2025, Money Value remained in keeping with 9M 2024. Almas’ All-in Sustaining Value was US$1,128/GEO in Q3 2025, down 5% from Q3 2024, supported by improved operational efficiency and lowered CAPEX. In comparison with Q2 2025, AISC decreased 17%, attributable to decrease CAPEX and G&A bills. In 9M 2025, the AISC was US$1,223, a lower of 8% in comparison with the identical interval in 2024.

Adjusted EBITDA totaled US$34.5 million in Q3 2025, 51% larger than Q3 2024 consequence, pushed by elevated ore processing from the plant enlargement, improved operational efficiency, larger gross sales volumes, and elevated gold costs. In comparison with Q2 2025, Adjusted EBITDA rose 38%, primarily attributable to larger gold costs and a 17% improve in manufacturing volumes. For 9M 2025, Adjusted EBITDA was US$81.7 million, an 86% improve from 9M 2024, supported by larger gross sales volumes from expanded operational capability, regardless of steady Money Prices and an 8% discount in AISC to US$1,223/GEO.

3.5 Borborema

| (US$ mil) | Q3 2025 | Q2 2025 | ||

| Manufacturing (GEO) | 10,219 | 2,577 | ||

| Gross sales (GEO) | 11,228 | 1,190 | ||

| Money Value (US$/GEO) | 1,127 | 936 | ||

| AISC (US$/GEO) | 1,237 | 1,441 | ||

| Web Income | 38,982 | 3,690 | ||

| Value of products offered | (12,652 | ) | (1,114 | ) |

| Gross Revenue | 26,330 | 2,576 | ||

| Bills | (1,186 | ) | (378 | ) |

| Basic and administrative bills | (869 | ) | (378 | ) |

| Exploration bills | (317 | ) | – | |

| EBIT | 25,144 | 2,198 | ||

| Adjusted EBITDA | 25,144 | 2,084 | ||

| Monetary End result | (252 | ) | (4,971 | ) |

| Finance expense | (232 | ) | (4,982 | ) |

| Different earnings (bills) | (20 | ) | 11 | |

| EBT | 24,892 | (2,773 | ) | |

| Complete taxes | (522 | ) | (309 | ) |

| Present earnings tax expense | (6,585 | ) | – | |

| Deferred earnings tax expense | 6,063 | (309 | ) | |

| Revenue/(loss) for the interval | 24,370 | (3,082 | ) | |

Word: Borborema’s Q2 2025 outcomes didn’t offered important gross sales because of the starting of gold manufacturing on its ramp-up section, whereas Q3 2025 counts with a full quarter of related gross sales. Attributable to this, the outcomes of Q3 2025 and Q2 2025 usually are not comparable.

Borborema manufacturing in Q3 2025 totaled 10,219 GEO advancing alongside the ramp-up curve and attaining business manufacturing in September 2025 as scheduled.

In Q3 2025, Borborema’s Web Income reached US$38.9 million, contributing to a 9M 2025 Web Income of US$42.7 million. The Money Value was US$1,127 per Gold Equal Ounce (GEO) in Q3 2025, in keeping with Firm expectations for the mine’s ramp-up section, which started with the primary gold manufacturing shipped in June 2025. Borborema’s All-in Sustaining Value (AISC) was US$1,237/GEO in Q3 2025, additionally in keeping with the Firm’s expectations for this stage of Borborema.

Adjusted EBITDA was US$25.1 million in Q3 2025, pushed by robust Web Income from 10,219 GEO produced and favorable gold costs.

4. Money Movement

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Adjusted EBITDA | 152,105 | 106,224 | 43 | % | 77,974 | 95 | % | 339,808 | 186,813 | 82 | % | |||||

| (+) Exploration Bills | 2,333 | 1,714 | 36 | % | 4,293 | -46 | % | 5,423 | 9,186 | -41 | % | |||||

| (-) Sustaining Capex | (14,335 | ) | (15,151 | ) | -5 | % | (10,570 | ) | -36 | % | (40,377 | ) | (27,770 | ) | 45 | % |

| (+/-) ∆ Working Capital, Modifications in Different Belongings and Liabilities and Others | (26,033 | ) | 7,024 | N.A | 3,065 | N.A | (37,092 | ) | (26,670 | ) | 39 | % | ||||

| (-) Revenue Taxes Paid | (17,755 | ) | (22,570 | ) | -21 | % | (3,728 | ) | 376 | % | (57,199 | ) | (15,162 | ) | 277 | % |

| (-) Lease Funds | (4,551 | ) | (5,122 | ) | -11 | % | (4,810 | ) | -5 | % | (13,912 | ) | (13,490 | ) | 3 | % |

| (-) Realized Losses on Gold Hedges | (17,130 | ) | (11,699 | ) | 46 | % | – | 0 | % | (34,869 | ) | – | 0 | % | ||

| Recurring Free Money Movement | 74,633 | 60,420 | 24 | % | 66,224 | 13 | % | 161,781 | 112,907 | 43 | % | |||||

In Q3 2025, Recurring Free Money Movement reached US$74.6 million, up 24% from Q2 2025 and 13% from Q3 2024. In comparison with Q2 2025, the rise was primarily pushed by:

- 43% rise in Adjusted EBITDA to US$152.1 million, attributable to larger gross sales volumes and better steel costs;

- 21% discount in earnings taxes paid (from US$22.6 million to US$17.8 million), as in Q2 2025 there have been annual adjustment tax funds in Minosa;

- These have been partially offset by:

- “Working Capital, Modifications in Different Belongings and Liabilities and Others outflow of US$26.0 million, primarily attributable to improve in low-grades stockpiles in Almas and Borborema; and

- improve in realized losses on gold hedges (to US$17.1 million), resulted from the gold value improve.

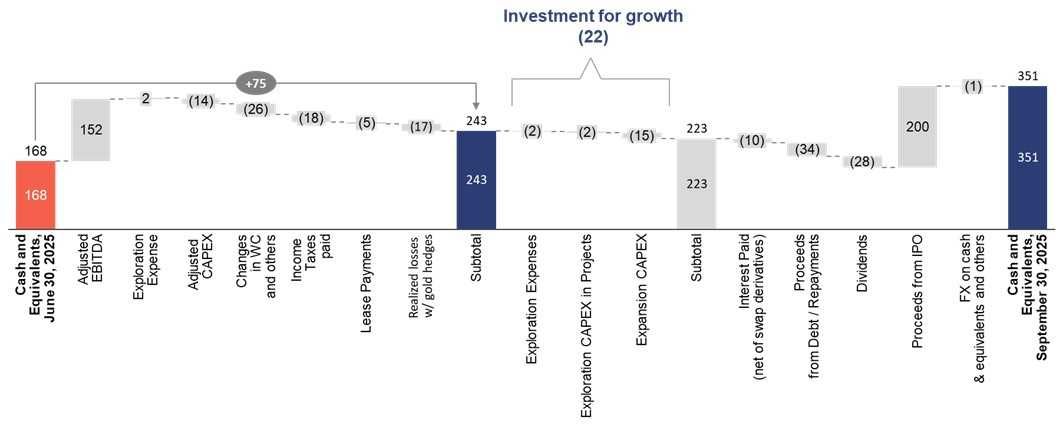

The chart under exhibits the change in money place for the three months ending September 30, 2025, from a administration perspective:

Modifications to the Money Place Q2 2025 vs. Q3 2025 – Managerial View (US$ Million)

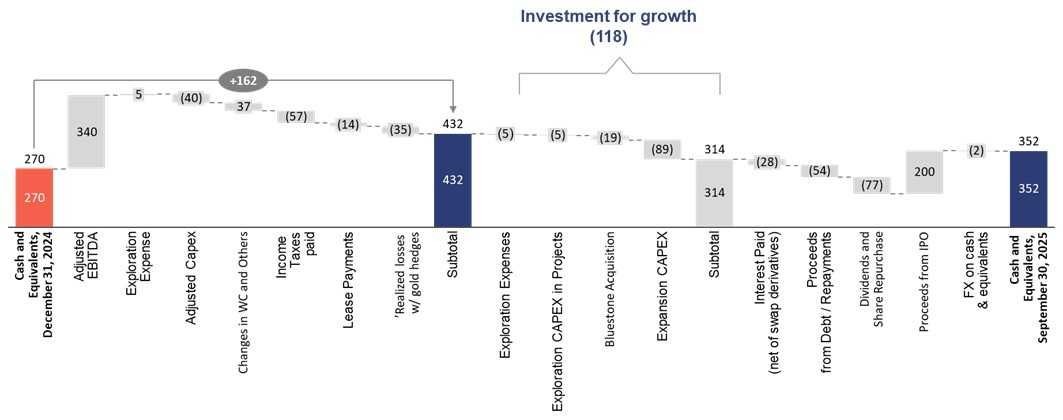

Modifications to the Money Place This fall 2024 vs. Q3 2025 – Managerial View (US$ Million)

Word: Adjusted Capex consists of Exploration and Enlargement Capex.

5. Funding

The Firm’s consolidated Capex for Q3 2025 totaled US$31.6 million. The principle funding headlines for the quarter embody:

- Enlargement of Capex : US$15.6 million, concentrated primarily on Apoena and Almas, the place US$5.1 million was invested at Apoena, US$3.4 million at Almas, US$1.1 at Period Dorada and the remaining US$0.4 million was at Borborema and Minosa. Different enlargement tasks totaled US$4.7 million.

- Upkeep Capex : US$11.7 million, of which US$5.7 million was allotted to Aranzazu, US$1.8 million to Apoena, and US$1.2 million to Almas, US$2.0 million to Minosa and US$0.9 million to Borborema.

- Exploration Capex : US$4.5 million, allotted to exploration actions. Apoena led funding with US$1.4 million, adopted by Aranzazu with US$0.9 million. Different exploration tasks totaled US$2.2 million.

6. Gross and Web Debt

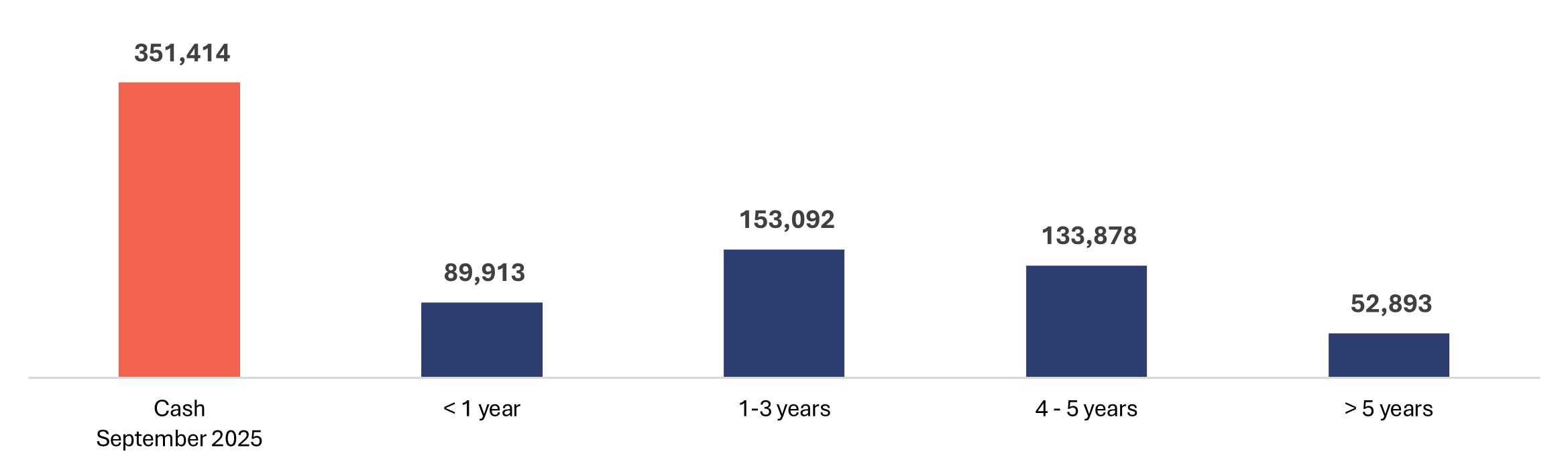

Complete gross debt (brief and long-term portion) was US$429,776 on the finish of Q3 2025, a lower when in comparison with U$453,893 on the finish of Q2 2025. This lower was primarily pushed by curiosity and principal funds within the quarter.

The Firm’s money place stays snug, closing out the 12 months at US$351,414, because of the Nasdaq IPO and robust Recurring Money Flows.

The Firm’s Web Debt reached US$63,772 by Q3 2025 a 77% lower in comparison with Q2 2025 and likewise a lower of 56% when in comparison with the identical interval of 2024, attributable to (i) larger money place because of the internet proceeds from Nasdaq IPO of US$200.1 million, (ii) robust Recurring Free Money Flows, (iii) the numerous discount within the CAPEX of US$31.6 million, 37% decrease than Q2 2025 CAPEX (US$50.3 million), principally associated to decrease CAPEX at Borborema because of the conclusion of the development, regardless of cost of dividends of US$27.6 million. The web debt-to-last 12 months EBITDA ratio lowered to 0.15x on the finish of Q3 2025, from 0.81x on the finish of Q2 2025.

Web Debt Breakdown

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % | Q3 2024 | YoY Change % | ||

| Loans and debentures (present) | 89,810 | 78,786 | 14 | % | 163,115 | -45 | % |

| Loans and debentures (non-current) | 339,966 | 375,107 | -9 | % | 177,444 | 92 | % |

| Gross debt | 429,776 | 453,893 | -5 | % | 340,559 | 26 | % |

| Money and money equivalents | 351,414 | 167,938 | 109 | % | 195,979 | 79 | % |

| By-product monetary instrument (Almas Swap) | 14,590 | 5,395 | 170 | % | 214 | 6718 | % |

| Web Debt | 63,772 | 280,560 | -77 | % | 144,366 | -56 | % |

| Web Debt/LTM EBITDA | 0.15x | 0.81x | -0.7 | x |

0.63x | -0.5 | x |

The desk under exhibits the debt amortization timeline:

Debt Amortization Timeline (US$ thousand)

7. Steering vs. Precise 1

The Firm is on observe to realize the 2025 Steering, together with Manufacturing, Money Value, All-in Sustaining Value (AISC) and CAPEX, as proven within the outcomes under:

| Gold equal ounces manufacturing (‘000 GEO) – 2025 | ||||||

| Decrease Certain | Higher Certain | 9M 2025 A | 9M 2025 at Steering steel costs |

% | ||

| Aranzazu | 88 | 97 | 64 | 70 | 79% – 72% | |

| Apoena | 29 | 32 | 26 | 26 | 91% – 82% | |

| Minosa | 64 | 73 | 54 | 54 | 84% – 74% | |

| Almas | 51 | 58 | 41 | 41 | 80% – 70% | |

| Complete ex-Borborema | 233 | 260 | 186 | 191 | 82% – 73% | |

| Borborema | 33 | 40 | 13 | 13 | 39% – 32% | |

| Complete | 266 | 300 | 198 | 204 | 77% – 68% | |

| Money Value per equal ounce of gold produced – 2025 | |||||||

| Decrease Certain | Higher Certain | 9M 2025 A | 9M 2025 at Steering steel costs | % | |||

| Aranzazu | 1,029 | 1,132 | 1,135 | 1,002 | 97% – 88% | ||

| Apoena | 1,258 | 1,384 | 1,159 | 1,159 | 92% – 84% | ||

| Minosa | 1,108 | 1,219 | 1,173 | 1,173 | 106% – 96% | ||

| Almas | 1,013 | 1,114 | 1,167 | 1,167 | 115% – 105% | ||

| Borborema | 1,084 | 1,232 | 1,109 | 1,109 | 102% – 90% | ||

| Complete | 1,078 | 1,191 | 1,133 | 1,086 | 101% – 91% | ||

| AISC per equal ounce of gold produced – 2025 | ||||||

| Decrease Certain | Higher Certain | 9M 2025 A | 9M 2025 at Steering steel costs | % | ||

| Aranzazu | 1,348 | 1,455 | 1,523 | 1,344 | 100% – 92% | |

| Apoena | 2,425 | 2,619 | 1,771 | 1,867 | 73% – 68% | |

| Minosa | 1,263 | 1,364 | 1,305 | 1,305 | 103% – 96% | |

| Almas | 1,113 | 1,202 | 1,223 | 1,223 | 110% – 102% | |

| Borborema | 1,113 | 1,304 | 1,256 | 1,256 | 113% – 96% | |

| Complete | 1,374 | 1,492 | 1,419 | 1,373 | 99% – 91% | |

| Capex (US$ million) – 2025 | |||||

| Low – 2025 | Excessive – 2025 | 9M 2025 A | % | ||

| Sustaining | 40 | 47 | 34 | 84% – 72% | |

| Exploration | 10 | 13 | 11 | 113% – 84% | |

| New tasks + Enlargement | 99 | 106 | 96 | 97% – 91% | |

| Complete | 149 | 167 | 141 | 85% – 95% | |

______________________________

1 Key Components:

The Firm’s future profitability, working money circulate and monetary place will likely be instantly associated to prevailing gold and copper costs. Key elements that affect the worth of gold and copper embody, amongst others, the availability and demand for gold and copper, the relative energy of currencies (particularly the US greenback) and macroeconomic elements, equivalent to present and future expectations for inflation and rates of interest. Administration believes that the financial atmosphere within the brief and medium time period ought to stay comparatively favorable with respect to commodity costs, albeit with continued volatility.

To cut back the dangers related to commodity costs and forex volatility, the Firm will proceed to evaluate and deploy hedging packages. For extra data on this topic, please seek advice from the Reference Kind.

Different key elements influencing profitability and working money flows are: manufacturing ranges (affected by grades, ore portions, course of recoveries, labor, nation stability and availability of services and tools); manufacturing and processing prices (impacted by manufacturing ranges, costs and the usage of key consumables, labor, inflation and trade charges), and different elements.

8. Shareholder Info

As of September 30, 2025, the Firm had the next excellent: 83,534,506 Widespread Shares, 1,493,492 inventory choices, and 189,795 deferred share models.

9. Attachments

9.1 Monetary Statements

| (US$ thousand) | Q3 2025 | Q2 2025 | QoQ Change % |

Q3 2024 | YoY Change% |

9M 2025 | 9M 2024 | Change % | ||||||||

| Web income | 247,832 | 190,436 | 30 | % | 156,157 | 59 | % | 600,072 | 422,646 | 42 | % | |||||

| Value of products offered | (98,223 | ) | (86,497 | ) | 14 | % | (83,976 | ) | 17 | % | (268,096 | ) | (252,475 | ) | 6 | % |

| Gross revenue | 149,609 | 103,939 | 44 | % | 72,181 | 107 | % | 331,976 | 170,171 | 95 | % | |||||

| Basic and administrative bills | (10,371 | ) | (11,284 | ) | -8 | % | (6,923 | ) | 50 | % | (31,291 | ) | (22,734 | ) | 38 | % |

| Exploration bills | (2,333 | ) | (1,714 | ) | 36 | % | (4,293 | ) | -46 | % | (5,423 | ) | (9,186 | ) | -41 | % |

| Working earnings | 136,905 | 90,941 | 51 | % | 60,965 | 125 | % | 295,262 | 138,251 | 114 | % | |||||

| Monetary bills | (102,565 | ) | (59,630 | ) | 72 | % | (62,691 | ) | 64 | % | (283,806 | ) | (141,888 | ) | 100 | % |

| Different earnings (bills) | (822 | ) | 61 | N.A. | (359 | ) | 129 | % | (1,515 | ) | (952 | ) | 59 | % | ||

| Revenue earlier than earnings taxes | 33,518 | 31,372 | 7 | % | (2,085 | ) | N.A. | 9,941 | (4,589 | ) | N.A. | |||||

| Present earnings tax expense | (38,402 | ) | (29,551 | ) | 30 | % | (11,833 | ) | 225 | % | (88,767 | ) | (36,588 | ) | 143 | % |

| Deferred earnings tax expense | 10,510 | 6,326 | 66 | % | 1,995 | 427 | % | 19,350 | (5,738 | ) | N.A. | |||||

| Revenue/(loss) for the interval | 5,626 | 8,147 | -31 | % | (11,923 | ) | N.A. | (59,476 | ) | (46,915 | ) | 27 | % | |||

9.2 Steadiness Sheet

| (US$ million) | Q3 2025 | Q2 2025 | Q3 2024 | |||

| ASSETS | ||||||

| Present | ||||||

| Money and money equivalents | 351,414 | 167,938 | 195,979 | |||

| Accounts receivables | 13,142 | 4,826 | 15,355 | |||

| Worth added taxes and different recoverable taxes | 23,586 | 21,292 | 41,329 | |||

| Inventories | 76,671 | 80,034 | 63,151 | |||

| By-product monetary instrument | 14,590 | 5,395 | 214 | |||

| Different receivables and belongings | 28,949 | 21,560 | 19,901 | |||

| Complete present belongings | 508,352 | 301,045 | 335,929 | |||

| Non-current belongings | ||||||

| Worth added taxes and different recoverable taxes | 49,843 | 46,329 | 17,148 | |||

| Stock | 44,406 | 23,025 | 16,472 | |||

| Different receivables and belongings | 7,012 | 4,319 | 3,490 | |||

| Property, plant and tools | 783,346 | 762,566 | 560,993 | |||

| Deferred earnings tax belongings | 35,903 | 28,639 | 20,970 | |||

| Complete non-current belongings | 920,510 | 864,878 | 619,073 | |||

| Complete belongings | 1,428,862 | 1,165,923 | 955,002 | |||

| LIABILITIES | ||||||

| Present | ||||||

| Commerce and different payables | 125,447 | 111,156 | 100,061 | |||

| By-product monetary devices | 26,521 | 26,654 | – | |||

| Loans and Debentures | 89,810 | 78,786 | 163,115 | |||

| Legal responsibility measured at honest worth | 5,322 | 4,850 | 2,350 | |||

| Present earnings tax liabilities | 46,228 | 28,507 | 18,737 | |||

| Present portion of different liabilities | 15,988 | 14,939 | 14,225 | |||

| Provision for mine closure and restoration | 2,551 | – | – | |||

| Liabilities instantly related to belongings categorised as held on the market | 2,757 | 2,757 | 4,087 | |||

| Complete present liabilities | 314,624 | 267,649 | 302,575 | |||

| Non-current liabilities | ||||||

| Loans and debentures | 339,966 | 375,107 | 177,444 | |||

| Legal responsibility measured at honest worth | 17,311 | 17,689 | 17,406 | |||

| By-product Monetary Devices | 297,801 | 222,901 | 133,622 | |||

| Deferred earnings tax liabilities | 31,888 | 35,925 | 11,360 | |||

| Provision for mine closure and restoration | 64,830 | 64,470 | 52,852 | |||

| Different provisions | 29,215 | 28,467 | 13,986 | |||

| Different liabilities | 10,794 | 13,951 | 15,340 | |||

| Complete non-current liabilities | 791,805 | 758,510 | 422,010 | |||

| SHAREHOLDERS’ EQUITY | ||||||

| Share capital | 833,382 | 633,271 | 602,909 | |||

| Contributed surplus | 56,937 | 55,669 | 55,560 | |||

| Collected different complete earnings | (1,584 | ) | (4,812 | ) | 2,357 | |

| Collected losses | (566,302 | ) | (544,364 | ) | (430,408 | ) |

| Complete fairness | 322,433 | 139,764 | 230,418 | |||

| Complete liabilities and fairness | 1,428,862 | 1,165,923 | 955,002 | |||

9.3 Money Movement Assertion

| (US$ thousand) | Q3 2025 | Q2 2025 | Q3 2024 | 9M 2025 | 9M 2024 | |||||

| Money flows from working actions | ||||||||||

| Revenue /(Loss) for the interval | 5,626 | 8,147 | (11,923 | ) | (59,476 | ) | (46,915 | ) | ||

| Objects adjusting revenue (loss) of the interval | 133,542 | 82,263 | 105,657 | 371,374 | 237,672 | |||||

| Modifications in working capital | 2,174 | 3,372 | (6,674 | ) | (8,589 | ) | (23,807 | ) | ||

| Revenue tax paid | (17,755 | ) | (22,570 | ) | (3,728 | ) | (57,199 | ) | (15,162 | ) |

| Different present and non-current belongings and liabilities | (30,491 | ) | 8,653 | (6,562 | ) | (31,921 | ) | 4,445 | ||

| Web money generated by working actions | 93,096 | 79,865 | 76,770 | 214,189 | 156,233 | |||||

| Money flows from investing actions | ||||||||||

| Buy of property, plant and tools | (31,605 | ) | (50,325 | ) | (60,483 | ) | (133,655 | ) | (113,761 | ) |

| Acquisition of funding – Bluestone Sources | – | – | – | (18,538 | ) | – | ||||

| Acquisition of funding – Altamira | – | (439 | ) | – | (439 | ) | – | |||

| Web money utilized in investing actions | (31,605 | ) | (50,764 | ) | (60,483 | ) | (152,632 | ) | (113,761 | ) |

| Money flows from financing actions | ||||||||||

| Web Proceeds from the Nasdaq IPO | 200,116 | – | – | 200,116 | ||||||

| Proceeds acquired from loans and debentures | – | – | 39,640 | – | 73,640 | |||||

| Reimbursement of loans and debentures | (33,728 | ) | (9,147 | ) | (32,017 | ) | (54,330 | ) | (55,329 | ) |

| By-product settlement- debt swap agreements | (1,418 | ) | 2,582 | 1,186 | 1,164 | 4,054 | ||||

| By-product payment | – | – | – | – | (13,522 | ) | ||||

| Curiosity paid on loans and debentures | (8,308 | ) | (13,397 | ) | (11,758 | ) | (29,480 | ) | (29,456 | ) |

| Cost of legal responsibility (NSR settlement) | (942 | ) | (852 | ) | (489 | ) | (2,536 | ) | (1,699 | ) |

| Principal and curiosity funds of lease liabilities | (4,551 | ) | (5,122 | ) | (4,810 | ) | (13,912 | ) | (13,490 | ) |

| Reimbursement of different liabilities | (1,044 | ) | (1 | ) | (1,749 | ) | (2,025 | ) | (2,573 | ) |

| Cost of dividends | (27,564 | ) | (29,811 | ) | – | (75,708 | ) | (25,339 | ) | |

| Acquisition of treasury shares | – | – | (6,068 | ) | (1,200 | ) | (9,526 | ) | ||

| Proceeds and (funds) from train of inventory choices | – | – | 65 | – | 165 | |||||

| Web money generated by (utilized in) financing actions | 122,561 | (55,748 | ) | (16,000 | ) | 22,089 | (73,075 | ) | ||

| Enhance (lower) in money and money equivalents | 184,052 | (26,647 | ) | 287 | 83,646 | (30,603 | ) | |||

| Impact of overseas trade acquire (loss) on money equivalents | (576 | ) | (3,481 | ) | 3,729 | (2,421 | ) | (10,713 | ) | |

| Money and money equivalents, starting of the interval | 167,938 | 198,066 | 191,963 | 270,189 | 237,295 | |||||

| Per stability sheet on the finish of comparative interval | 351,414 | 167,938 | 195,979 | 351,414 | 195,979 | |||||

9.4 Non-GAAP Efficiency Measures

Set out under are reconciliations for sure non-GAAP monetary measures (together with non-GAAP ratios) utilized by the Firm on this Earnings Launch: Adjusted EBITDA; Adjusted internet Revenue, money working prices per gold equal ounce offered; AISCs; Web Debt; and Adjusted EBITDA Margin, that are non-GAAP monetary measures. These non-GAAP measures would not have any standardized that means inside IFRS and due to this fact will not be corresponding to comparable measures offered by different firms. The Firm believes that these measures present traders with further data which is beneficial in evaluating the Firm’s efficiency and shouldn’t be thought-about in isolation or as an alternative choice to measures of efficiency ready in accordance with IFRS.

A. Reconciliation from earnings for the quarter to Adjusted EBITDA:

(US$ thousand)

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Revenue / (Loss) for the interval | 5,626 | (11,923 | ) | (59,476 | ) | (46,915 | ) | |

| Present earnings tax expense | 38,402 | 11,833 | 88,767 | 36,588 | ||||

| Deferred earnings tax expense | (10,510 | ) | (1,995 | ) | (19,350 | ) | 5,738 | |

| Finance expense | 102,565 | 62,691 | 283,806 | 141,888 | ||||

| Different earnings (expense) | 822 | 359 | 1,515 | 952 | ||||

| Depletion and amortization | 15,200 | 17,108 | 44,546 | 49,198 | ||||

| Adjusted EBITDA | 152,105 | 78,073 | 339,808 | 187,449 |

B. Reconciliation from the consolidated monetary statements to money working prices per gold equal ounce offered:

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Value of products offered | (98,223 | ) | (83,976 | ) | (268,096 | ) | (252,475 | ) |

| Depletion and amortization | 15,058 | 16,686 | 43,870 | 47,577 | ||||

| Subtotal | (83,165 | ) | 67,069 | (224,226 | ) | (204,898 | ) | |

| Gold Equal Ounces offered | 74,907 | 67,069 | 197,850 | 200,517 | ||||

| Money prices per gold equal ounce offered | 1,110 | 987 | 1,133 | 1,022 |

C. Reconciliation from the consolidated monetary statements to all in sustaining prices per gold equal ounce offered:

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Value of products offered | (98,223 | ) | (83,976 | ) | (268,096 | ) | (252,475 | ) |

| Depletion and amortization | 15,058 | 16,686 | 43,870 | 47,577 | ||||

| Subtotal | (83,165 | ) | (67,290 | ) | (224,226 | ) | (204,898 | ) |

| Adjusted capex | 14,196 | 13,535 | 40,240 | 34,725 | ||||

| Basic and Administrative Bills | 4,177 | 2,444 | 11,494 | 7,900 | ||||

| Lease Funds | 3,041 | 4,810 | 7,490 | 13,490 | ||||

| Subtotal | (61,751 | ) | (46,500 | ) | (165,002 | ) | (148,783 | ) |

| Gold Equal Ounces offered (in hundreds) | 74,907 | 67,069 | 197,850 | 200,517 | ||||

| All In Sustaining prices per ounce offered equal ounce offered | 1,396 | 1,292 | 1,433 | 1,302 |

D. Reconciliation from the consolidated monetary statements to realized common gold value per ounce offered, internet 2 :

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 |

| Gold Income, internet of Gross sales Taxes | 180,738 | 105,436 | 420,208 | 278,523 |

| Ounces of gold offered | 53,393 | 43,689 | 133,590 | 126,259 |

| Realized common gold value per ounce offered, internet | 3,385 | 2,413 | 3,146 | 2,206 |

E. Web Debt:

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Loans and debentures (present) | 89,810 | 163,115 | 89,810 | 163,115 | ||||

| Loans and debentures (non-current) | 339,966 | 177,444 | 339,966 | 177,444 | ||||

| By-product Monetary Instrument (Swap – Aura Almas (Itaú Financial institution) | (14,590 | ) | (214 | ) | (14,590 | ) | (214 | ) |

| Money and Money Equivalents | (351,414 | ) | (195,979 | ) | (351,414 | ) | (195,979 | ) |

| Web Debt | 63,772 | 144,366 | 63,772 | 144,366 |

(1) By-product Monetary Instrument: solely consists of the swap associated to the Aura Almas Debenture.

F. Adjusted EBITDA Margin 3 (Adjusted EBITDA/Revenues):

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Web Income | 247,832 | 156,157 | 600,072 | 422,646 | ||||

| Adjusted EBITDA | 152,105 | 78,073 | 339,808 | 187,449 | ||||

| Adjusted EBITDA Margin (Adjusted EBITDA/Revenues) | 61 | % | 50 | % | 57 | % | 44 | % |

G. Adjusted Web Revenue

| (US$ thousand) | Q3 2025 | Q3 2024 | 9M 2025 | 9M 2024 | ||||

| Revenue/(Loss) for the interval | 5,626 | (11,923 | ) | (59,476 | ) | (46,915 | ) | |

| Overseas trade acquire (loss) | (36 | ) | 2,279 | (5,674 | ) | (10,995 | ) | |

| Loss on spinoff transactions | (75,252 | ) | (56,267 | ) | (199,766 | ) | (89,493 | ) |

| Loss on settlement of legal responsibility with fairness devices | – | – | (8,768 | ) | – | |||

| Deferred taxes over non-monetary objects | 12,242 | 20,415 | 22,323 | 8,943 | ||||

| Adjusted Web Revenue | 68,672 | 21,650 | 132,409 | 44,630 |

_______________________

2 Realized common gold value per ounce offered, internet is a non-GAAP monetary measure with no standardized that means underneath IFRS, and due to this fact will not be corresponding to comparable measures offered by different issuers.

3 Adjusted EBITDA Margin is a non-GAAP monetary measure with no standardized that means underneath IFRS, and due to this fact will not be corresponding to comparable measures offered by different issuers.

Certified Particular person

Farshid Ghazanfari, P.Geo., Mineral Sources and Geology Director for Aura Minerals Inc., has reviewed and accredited the scientific and technical data contained inside this Earnings Launch and serves because the Certified Particular person as outlined in NI 43-101 and S-Okay 1300. All NI 43-101 technical studies associated to properties materials to Aura can be found on SEDAR+ at sedarplus.ca and all S-Okay 1300 technical report summaries associated to properties materials to Aura can be found .from the SEC web site at www.sec.gov..

About Aura 360° Mining

Aura is concentrated on mining in full phrases – pondering holistically about how its enterprise impacts and advantages each one in all our stakeholders: our firm, our shareholders, our staff, and the nations and communities we serve. We name this 360° Mining.

Aura is an organization targeted on the event and operation of gold and base steel tasks within the Americas. The Firm’s 5 working belongings embody the Minosa gold mine in Honduras; the Almas, Apoena, and Borborema gold mines in Brazil; and the Aranzazu copper, gold, and silver mine in Mexico. Moreover, the Firm owns Period Dorada, a gold challenge in Guatemala; Tolda Fria, a gold challenge in Colombia; and three tasks in Brazil: Matupá, which is underneath growth; São Francisco, which is in care and upkeep; and the Carajás copper challenge within the Carajás area, within the exploration section.

CAUTIONARY NOTES AND ADDITIONAL INFORMATION