[ad_1]

Treasury Secretary Bessent says housing is in recession due to excessive rates of interest. May not excessive coverage uncertainty have some impact?

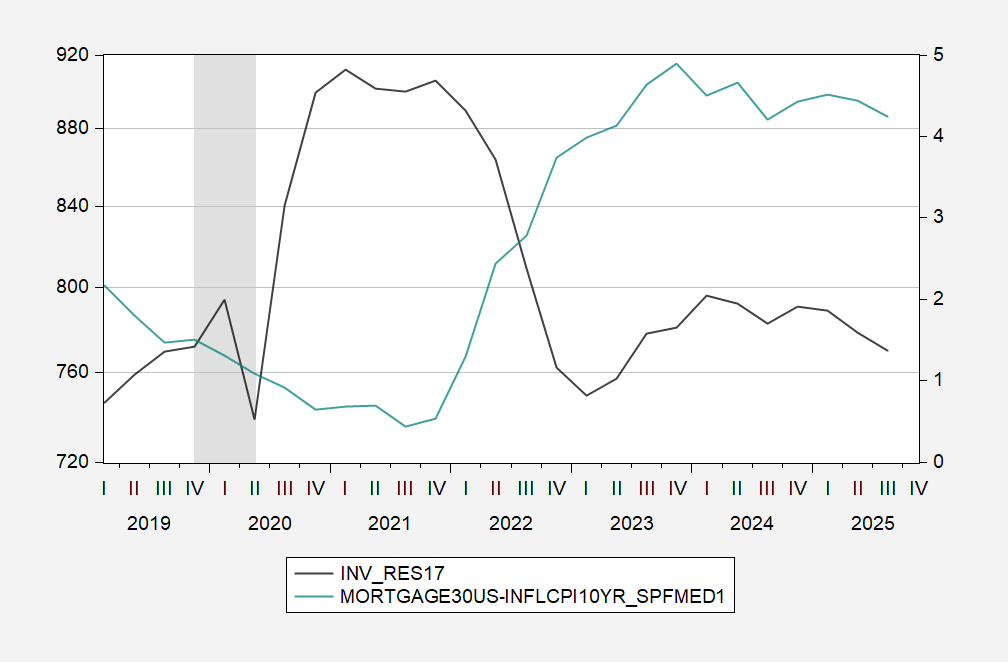

First, the 30yr mortgage adjusted by anticipated 10yr inflation:

Determine 1: Actual residential funding, in bn.Ch.2017$ SAAR (black, left scale), 30 12 months mortgage charge adjusted by 10 yr SPF median inflation, in % (blue, proper scale). 2005-2012 information is in Ch.2012$, rescaled into Ch.2017$. Q3 actual residential funding is nowcast from GDPNow. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Fannie Mae by way of FRED, Philadelphia Fed, NBER, and writer’s calculations.

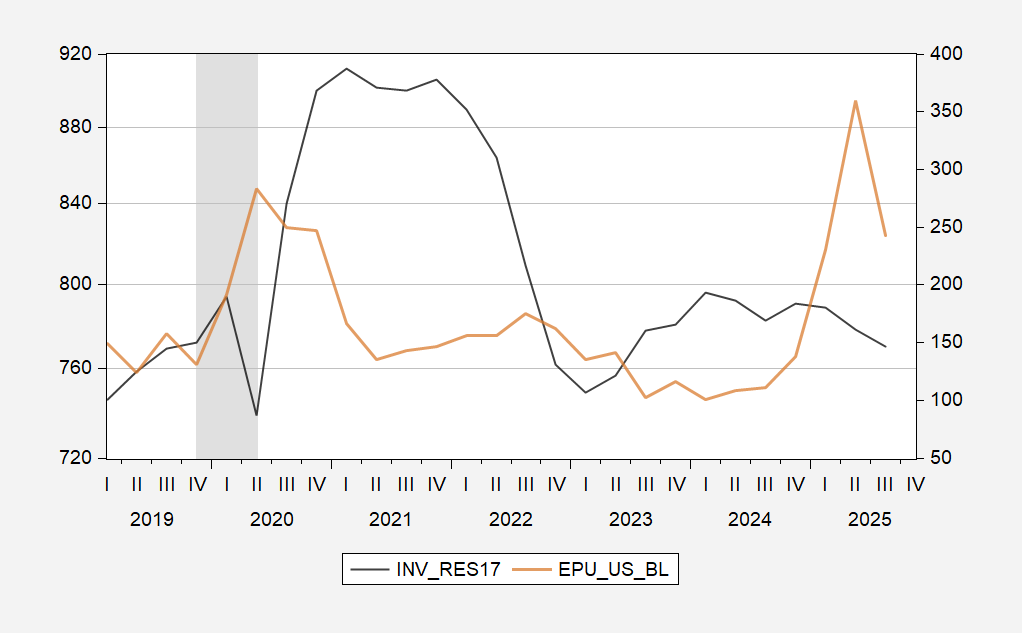

Now evaluate in opposition to Financial Coverage Uncertainty (baseline):

Determine 2: Actual residential funding, in bn.Ch.2017$ SAAR (black, left scale), Financial Coverage Uncertainty, legacy collection (tan, proper scale). 2002-2012 information is in Ch.2012$, rescaled into Ch.2017$. Q3 actual residential funding is nowcast from GDPNow. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Fannie Mae by way of FRED, Philadelphia Fed, NBER, policyuncertainty.com, and writer’s calculations.

Appears to me that coverage uncertainty is no less than as believable as an evidence for the lower in residential funding as excessive rates of interest.

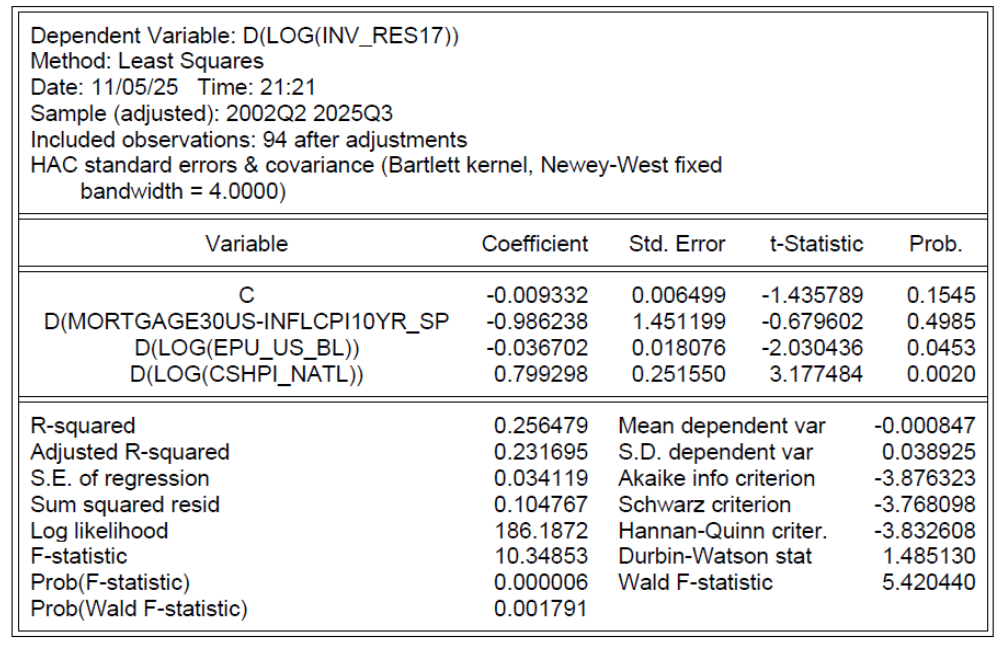

To confirm this, I estimate a regression over the 2005-2025 interval, in first variations, relating progress in actual residential funding to modifications in the true rate of interest and EPU, and appreciation in home costs (from Case-Shiller nationwide home value index).

I estimate the connection in first variations as a result of residential funding and home costs are unit root processes.

Find out how to assess the relative significance of actual rates of interest vs. coverage uncertainty? I confer with standardized coefficients, aka “beta” coefficients. The coefficent for coverage uncertainty is twice the magnitude of that for the true rate of interest (though the biggest coefficient is for value appreciation): -0.08 vs -0.17 vs. 0.46. To the extent that home value appreciation is dependent upon rates of interest, the true rate of interest impact could possibly be bigger.

[ad_2]