[ad_1]

Yves right here. The article under explains how each superior and rising economies can treatment their seemingly intractible drawback of excessive public debt ranges and low development: by correctly focusing spending on productiveness/output rising areas, resembling infrastructure and well being, and rising effectivity of govenment operations. Notice that this evaluation immplicity assumes that the international locations on this repair are, like Eurozone member states, not monetarily sovereign. However even these which are usually need to cope with the objections of funds hawks.

Even Larry Summers, a mainstream economist of solely a mildly Keynesian persuasion, confused that infrastructure spending greater than paid for itself (when you’ve gotten as a lot backlog and deferred upkeep because the US does), producing GDP development of as a lot as 3x the expenditure.

But many superior economies have purchased the neoliberal fairy story that personal growth and possession of pubic providers resembling infrastructre will probably be extra environment friendly. The charges related to complicated authorized strucuting and fundraising for these offers alone makes the concept that they are going to be cheaper (ex delivering a really inferior product) doubtful. A easy proof: within the US, each newly-built public toll street has gone bankrupt. As we wrote in 2021:

One apparent type of grifting is toll roads. A 2014 article on privatizations, describing the economics of recent toll street tasks, explains how they all the time go bust. I’ve seen no proof that the construction or phrases of those offers have modified to favor customers and taxpayers. From Considering Highways:

Starting with the contracting stage, the proof suggests toll working public personal partnerships are transportation shell corporations for worldwide financiers and contractors who blueprint future bankruptcies. As a result of Uncle Sam usually ensures the bonds – by far the most important chunk of “personal” cash – if and when the personal toll street or tunnel companion goes bankrupt, taxpayers are pressured to repay the bonds whereas absorbing all loans the state and federal governments gave the personal shell firm and any gathered depreciation. But the shell firm’s guardian corporations get to maintain years of precise toll earnings, on prime of thousands and thousands in design-build price overruns….

In fact, no government comes ahead and says, “We’re planning to go bankrupt,” however an evaluation of the information is stunning. There don’t look like any American personal toll corporations nonetheless in operation below the identical administration 15 years after development closed. The unique toll corporations appear persistently to have gone bankrupt or “zeroed their property” and walked away, leaving taxpayers a freeway now needing restore and having to repay the bonds and take in the loans and the depreciation.

The checklist of bankrupt corporations is staggering, from Virginia’s Pocahontas Parkway to Presidio Parkway in San Francisco to Canada’s “Sea to Sky Freeway” to Orange County’s Riverside Freeway to Detroit’s Windsor Tunnel to Brisbane, Australia’s Airport Hyperlink to South Carolina’s Connector 2000 to San Diego’s South Bay Expressway to Austin’s Cintra SH 130 to some dozen different toll amenities.

We can’t discover any American personal toll corporations, moreover, assembly their pre-construction visitors projections. Even these shell corporations not in chapter court docket normally produce half the earnings they projected to bondholders and federal and state officers previous to development.

Placing apart apparent public burdens like bankruptices, personal possession of infrastructure is inherently a nasty deal for residents. Financiers “sweat the asset” by jacking up fees, like touchdown charges for airports, and skimping on upkeep.

US healtcare, with its excessive prices and poor outcomes, is the poster youngster of what occurs with revenue incentives in all of the unsuitable locations. And now we now have the EU and US set to bulk up on equally overpriced arms spending.

So even when coverage makers take proposals like these to coronary heart, they’ve to beat plenty of mental seize and corruption to get them carried out. And all of the indicators are that inertia and horrible management will assure that situations will worsen, save for these on the prime.

PS: Earlier than you pooh pooh this text as a result of its authors work for the IMF, understand that there has lengthy been a cut up between the analysis aspect of home, which has lengthy advocated progressive (within the older sense fo the phrase) reforms, and the “program” aspect, which is a hard-nosed neoliberal enforcer.

By Period Dabla-Norris, Deputy Director, Fiscal Affairs Division Worldwide Financial Fund, Davide Furceri, Division Chief, Fiscal Affairs Division Worldwide Financial Fund. Zsuzsa Munkacsi, Economist Worldwide Financial Fund, and Galen Sher, Economist, Worldwide Financial Fund. Initially printed at VoxEU

With excessive public debt and weak medium-term development, finance ministries search to do extra with much less. This column argues that effectivity gaps in public spending stand at about 30-40% globally and are pronounced in infrastructure funding and R&D spending. Utilizing empirical and model-based evaluation, it exhibits that reallocating spending to infrastructure, schooling, well being, and R&D and shutting effectivity gaps can increase GDP by 11% in rising market and growing economies and 4% in superior economies, over the long run, and crucially with out will increase in whole spending.

Public debt is ready to surpass 100% of GDP within the subsequent 4 years globally, in response to the most recent IMF projections. Increased rates of interest, and strain to spend extra on defence, ageing societies, and growth create a constrained surroundings the place each greenback of public cash has to work more durable in delivering higher outcomes. Compounding this problem, medium-term development prospects have remained persistently subdued because the COVID-19 pandemic.

The IMF’s October 2025 Fiscal Monitor finds that international locations have substantial scope to reallocate public spending to help financial development, and so they may acquire round one third extra worth for cash by adopting the practices of greatest performers (IMF 2025). Furthermore, the report finds that spending smarter – by improved composition and elevated effectivity – can increase GDP by 11% in rising market and growing economies and 4% in superior economies, over the long run.

Scope for Reforms

Public spending as a share of GDP has doubled in superior and rising market economies because the Nineteen Sixties; nonetheless, the allocation has not been pro-growth. Globally, public funding as a share of whole expenditure has declined by two proportion factors, whereas spending on public schooling has stagnated at about 11% of whole expenditure – lower than half of public wage payments.

Critically, our new estimates for 174 international locations recommend that just about all have substantial room to enhance the effectivity of public spending. Constructing on a wealthy literature (e.g. Apeti et al. 2023, Herrera et al. 2025), we measure the gap of nations from a manufacturing potentialities frontier, which represents the absolute best outcomes in infrastructure, well being, schooling, and analysis and growth spending. Importantly, our estimates are the primary to fluctuate over time whereas additionally permitting for structural variations throughout international locations, statistical noise, and uncertainty over the selection of final result variables.

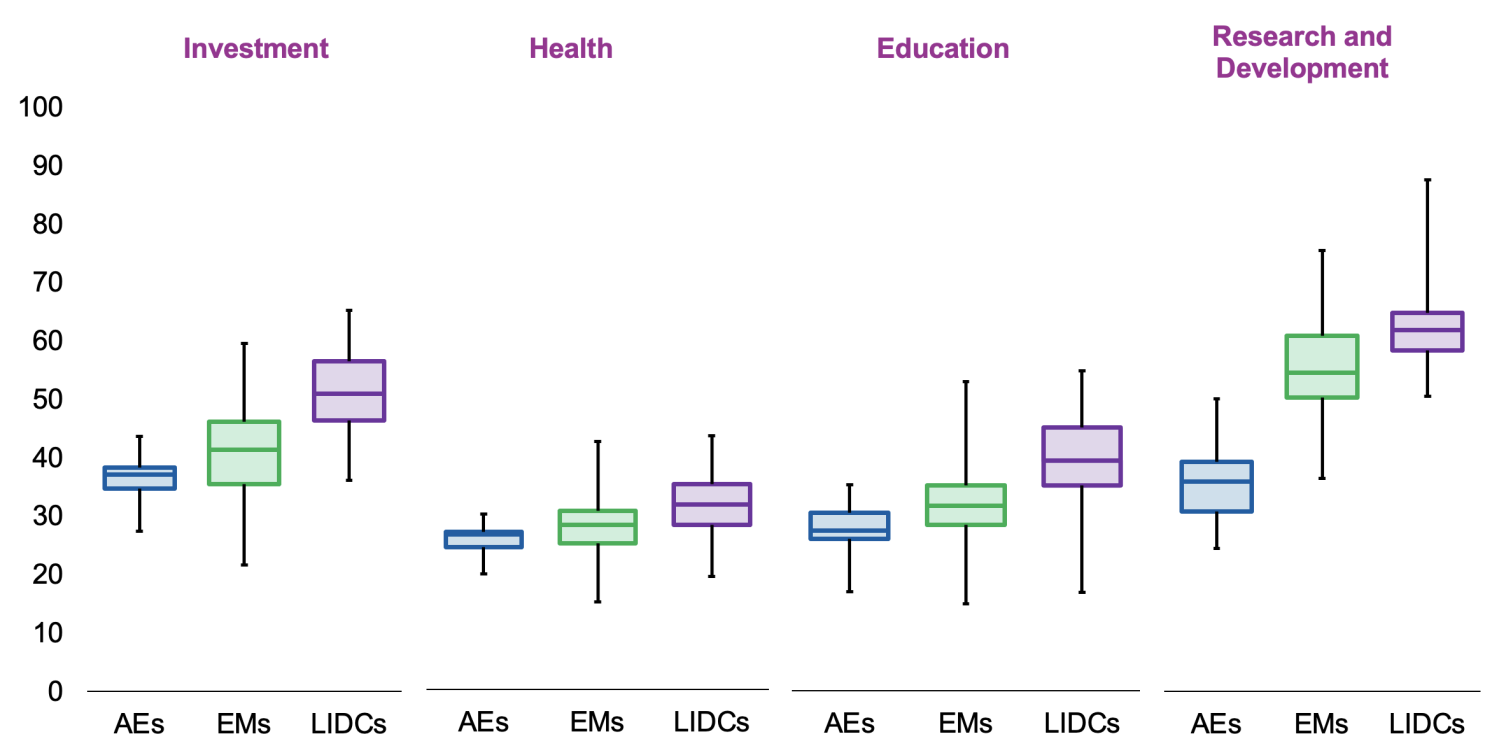

The dataset reveals that effectivity gaps stand at about 30-40% globally in the present day and are pronounced in infrastructure funding and analysis and growth spending (Determine 1). These gaps have narrowed significantly over the previous 4 many years, reflecting worldwide will increase in life expectancy, technological developments, and expanded entry to primary infrastructure in low-income growing international locations.

Determine 1 Public spending effectivity gaps (%)

Notes: The determine exhibits effectivity gaps, that are distances to the spending effectivity frontier. Effectivity gaps vary from 0 (totally environment friendly) to 100 (totally inefficient). The determine exhibits averages from 1980 to 2023. The containers point out medians and interquartile ranges (twenty fifth –seventy fifth percentiles), and the whiskers delineate the minimal and most values. AEs = superior economies, EMs = rising market economies, LIDCs = low-income growing international locations.

Output Beneficial properties from Reforms

An enormous literature examines how the allocation and effectivity of public spending contribute to development. In customary development fashions, public funding in bodily and human capital will increase the economic system’s productive capability, and public R&D spending provides to the data base that corporations use to innovate (Barro and Sala-i-Martin 2004). Extra environment friendly public funding provides extra to the capital inventory (Gupta et al. 2014, Presbitero et al. 2016).

We contribute to this literature in two key dimensions. First, we analyse – by each empirical and model-based evaluation – how the composition of public spending impacts financial exercise, assuming whole spending stays fixed. Second, we assess how the financial results fluctuate throughout international locations and over time, based mostly on the brand new estimates of effectivity.

Empirical proof – utilizing native projection and artificial management strategies – from about 700 episodes of huge reallocations in public spending in 155 international locations means that output will increase considerably within the brief to medium time period. A serious reallocation to public funding is adopted by a rise in output of about 4% ten years later. Reallocations to public well being and R&D spending are adopted by 3% will increase in output over ten years. These good points begin to emerge even within the first 5 years and enhance over time.

Certainly, simulations of an endogenous development mannequin clearly illustrate the potential long-term good points and the financial mechanism. Public infrastructure provides to output alongside personal capital and labour (as in Traum and Yang 2015), whereas public funding in human capital enhances the productiveness of time spent in schooling, accelerating ability accumulation. Public R&D spending expands the inventory of improvements accessible for corporations to undertake, with expertise diffusion occurring step by step as corporations put money into adoption (as in Anzoategui et al. 2019). The mannequin explicitly incorporates inefficiencies in public funding, human capital, and R&D, by permitting some public spending to be wasted as an alternative of contributing to the shares of capital and data (as in Berg et al. 2019).

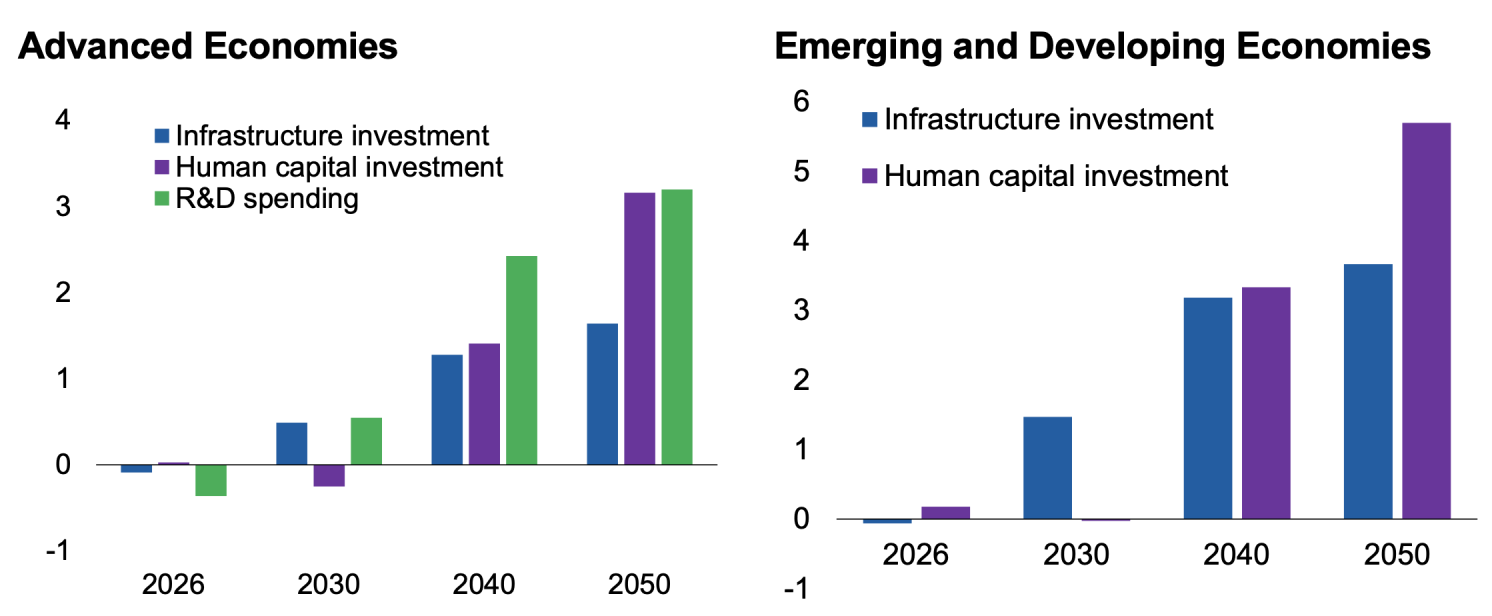

Determine 2 Lengthy-term output good points from reallocating spending (%)

Notes: The bars present long-term output good points as a result of a everlasting enhance, within the expenditure classes listed within the legend, of 1% of GDP in 2025, funded by a reduce in public consumption.

The outcomes present that reallocating 1% of GDP from authorities consumption (resembling administrative overhead) to public funding in human capital – resembling updating nationwide curricula and equipping faculties – can enhance output by 3% in superior economies and 6% in rising market and growing economies over the long run (Determine 2). The bigger good points for rising market and growing economies replicate their decrease preliminary ranges of human capital, which means the next marginal return on funding. These findings are echoed by de La Maisonneuve et al. (2024), who spotlight that boosting participation in early childhood schooling and rising schooling spending among the many lowest-spending international locations may generate giant good points in long-run productiveness. The output good points emerge solely after about 15 years, when the following era enters the labour power.

Related reallocations to infrastructure funding yield long-term output good points of 1.5% in superior economies and three.5% in rising market and growing economies. In superior economies, reallocating public spending towards R&D by 1% of GDP may enhance output by 3% over the long run.

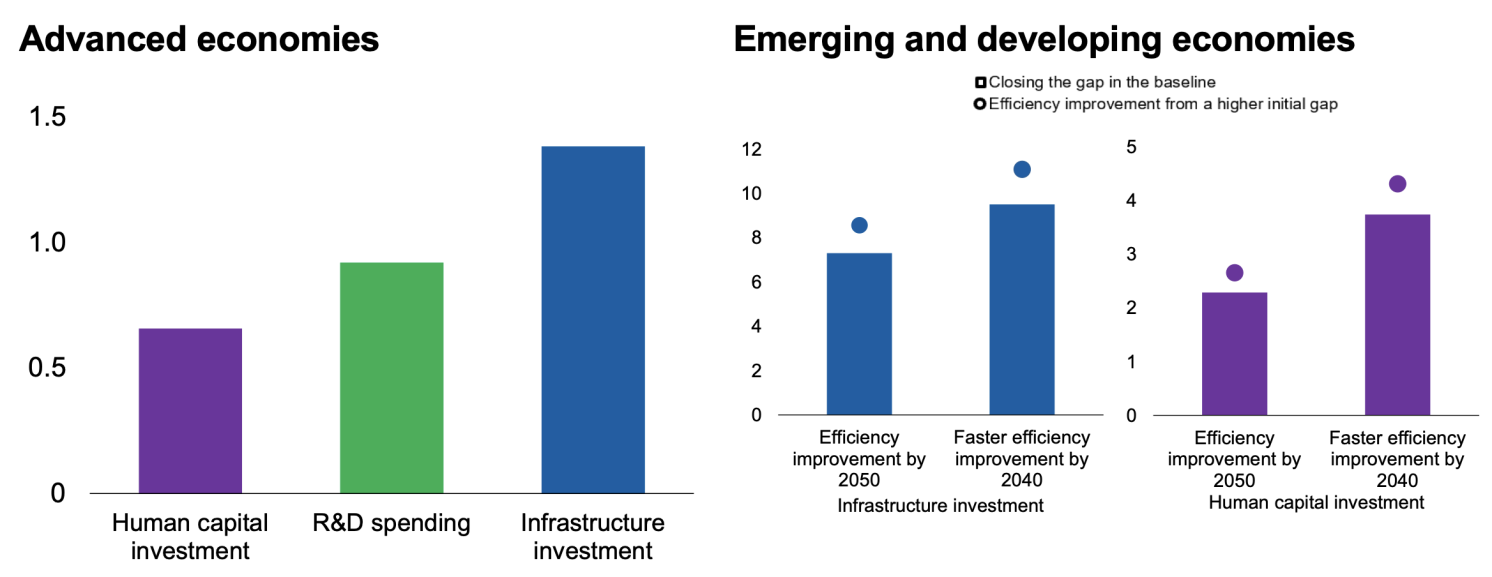

Crucially, closing gaps in spending effectivity can additional enhance the output impression by 1.5% in superior economies and a pair of.5-7.5% in rising market and growing economies, as extra of the accessible public spending interprets into productive types of capital and scientific data (Determine 3). The output good points will be as much as 2% bigger if spending effectivity is improved quicker.

Complementary insurance policies can additional increase these good points. In superior economies, combining investments in human capital and R&D yields larger advantages than focusing completely on one space, as innovation and abilities complement one another. For rising market and growing economies, pairing infrastructure and human capital investments capitalises on each short-term and long-term good points.

Determine 3 Lengthy-term output good points from enhancing spending effectivity (%)

Notes: The bars present the long-term output good points when gaps in spending effectivity are step by step closed, by 2050 within the left panel, and in the suitable panel, by 2040 or 2050 as indicated on the horizontal axis. In the suitable panel, the circles present the bigger acquire that’s achievable for international locations ranging from the next preliminary effectivity hole.

See authentic put up for references

[ad_2]