[ad_1]

Just a few years again, Hole (NYSE: GAP) was the retail equal of an overstuffed closet – too many manufacturers, not sufficient course, and piles of unsold stock hanging round like dangerous vogue decisions.

Quick-forward to 2025, and one thing shocking is occurring: The corporate is quietly turning into a money stream machine once more.

Once I see an old-school retailer producing actual income in a brutally aggressive market, my ears perk up. That form of turnaround – if it sticks – could make affected person traders some huge cash.

Hole is the biggest specialty attire firm within the U.S., proudly owning Previous Navy, Hole, Banana Republic, and Athleta. After years of uneven execution for the corporate, new management has spent two years tightening prices, refreshing model identities, and modernizing provide chains.

The second quarter of fiscal 2025 confirmed that the plan is beginning to click on. Internet gross sales held regular at $3.7 billion, with comparable gross sales up 1% 12 months over 12 months – the corporate’s sixth straight quarter of constructive comps. Earnings per share rose 6% to $0.57, and working margin got here in at 7.8%.

Money and equivalents hit $2.4 billion – the very best stage in 15 years – and the corporate returned $144 million to shareholders by way of dividends and buybacks.

The Previous Navy and Hole manufacturers each posted positive aspects, whereas Banana Republic confirmed early traction in its premium repositioning. Athleta stays a sore spot however has a brand new CEO from Nike to steer its reset.

Gross margin was 41.2%, down from 42.6% final 12 months because of the lapping of final 12 months’s credit-card profit and tariff prices. On-line gross sales rose 3% and now make up 34% of complete income. Stock climbed 9%, largely from accelerated receipts forward of latest tariffs.

Administration reaffirmed full-year steerage of 1% to 2% gross sales progress and an working margin of 6.7% to 7%.

For a mature retailer combating tariffs and fickle shoppers, these are respectable numbers.

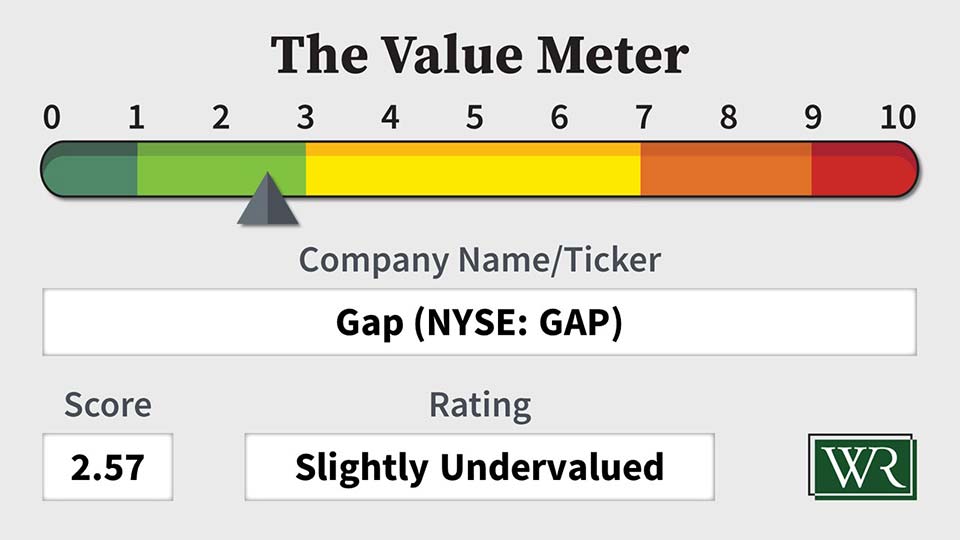

Let’s run Hole by way of The Worth Meter and see what’s actually taking place beneath the floor.

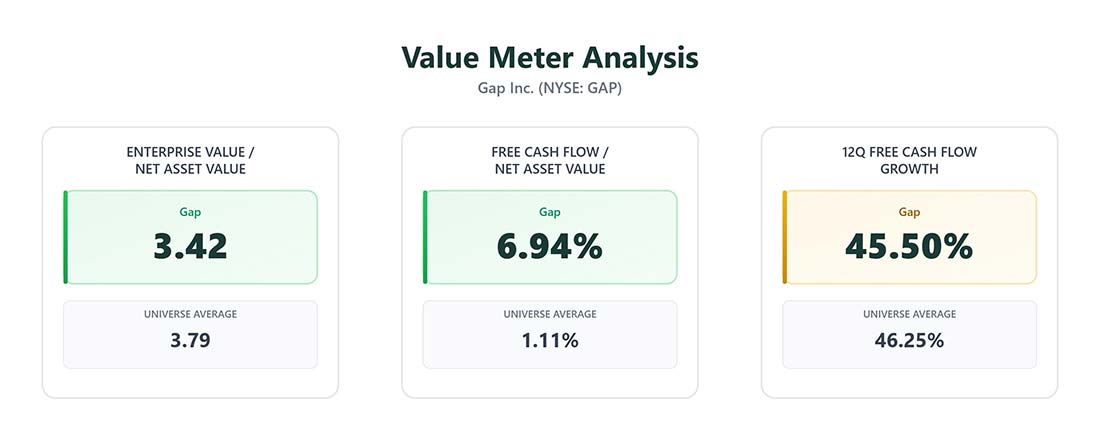

Hole’s enterprise worth in contrast with its web asset worth sits at about 3.4, a contact cheaper than the market’s 3.8 common. Meaning traders are paying much less for every greenback of belongings than they might for a typical peer.

On the identical time, the corporate is changing these belongings into money with uncommon effectivity. Quarterly free money stream now equals almost 7% of Hole’s web asset worth – six occasions increased than the broader market common.

What makes this extra convincing is the consistency. Practically half of the previous dozen quarters confirmed progress in free money stream, roughly matching the typical firm in our universe. Which will sound strange, however in retail, strange stability generally is a uncommon benefit.

Since surging 70% in a month on the finish of 2023, the inventory has seen some huge swings, bouncing forwards and backwards between $17 and $29. It presently sits proper across the midpoint of that vary.

Hole isn’t all of the sudden a progress rocket, and tariffs or shifting vogue developments might simply knock it off steadiness for some time. However proper now, the corporate is quietly producing actual money, paying its payments, rewarding shareholders, and buying and selling for lower than it most likely ought to.

That’s a setup long-term traders don’t see typically on this sector.

The Worth Meter charges Hole as “Barely Undervalued.”

What inventory would you want me to run by way of The Worth Meter subsequent? Put up the ticker image(s) within the feedback part beneath.

[ad_2]