[ad_1]

To cite:

We learn a lot about how housing is now “unaffordable”, however is that true?

We purchased a 2300 sf residence in 1979 with a ten.5% mortgage rate of interest (a step up from our 1200 sf starter residence). It was a little bit of a pressure, however our second baby was on the best way so we bit the bullet. Now it appears that evidently this era whines about housing being unaffordable and needs the federal government to “do one thing” about it.

Mortgage charges: https://fred.stlouisfed.org/collection/MORTGAGE30US

Yeah, up from “free cash”, however nonetheless in step with a lot of the final 50 years and much decrease than the 1980-85 interval that was alleged to be so “reasonably priced” for “boomers”.A bit of AI Help search comes up with this:

Search Help

“Since 1970, the typical measurement of latest single-family properties within the U.S. has elevated considerably, practically doubling in measurement. For instance, the median measurement of a brand new residence was about 1,595 sq. toes in 1980 and grew to roughly 2,386 sq. toes by 2018.”Search Help

“Inflation-adjusted residence costs per sq. foot have remained comparatively steady since 1973, averaging round $116 per sq. foot in 2015 {dollars}.”So the problem of properties being unaffordable is that younger {couples} are not content material with a 1,200 sf “starter residence” that is perhaps 30-years outdated. They “want” one thing twice as massive and model new.

Dwelling unaffordability is a fantasy.

“Whatabout” all the things else. Okay, what about it?

Once more, no “free cash”, however moreover the interval of reckless authorities spending in 2020-22 and ensuing inflation, present value will increase usually are not traditionally out of line.

https://mitsloan.mit.edu/ideas-made-to-matter/federal-spending-was-responsible-2022-spike-inflation-research-showsPrivate earnings will increase have adopted the historic development.

https://fred.stlouisfed.org/collection/PIUnemployment charge not so dangerous.

https://fred.stlouisfed.org/collection/UNRATEPerhaps it’s time to cease whining a lot.

OK, some information:

Home costs from 1979 onward:

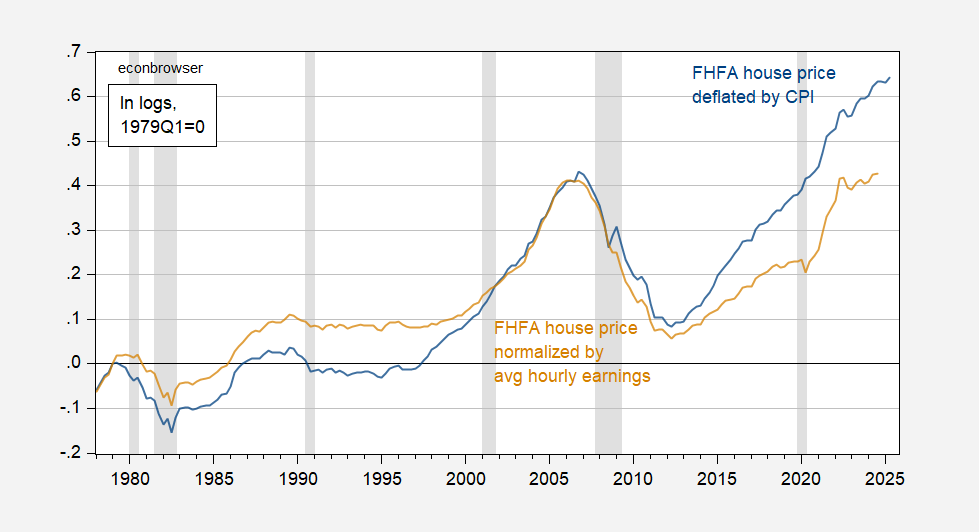

Determine 1: FHFA Home Value Index, deflated by CPI-ex shelter (blue), normalized by common hourly earnings (tan), each in logs, 1979Q1=0. NBER outlined peak to trough recession dates shaded grey. Supply: FHFA, BLS through FRED, NBER, and writer’s calculations.

Expressed both manner, the price of a home has risen relative to the value degree or to common hourly earnings of manufacturing and nonsupervisory employees.

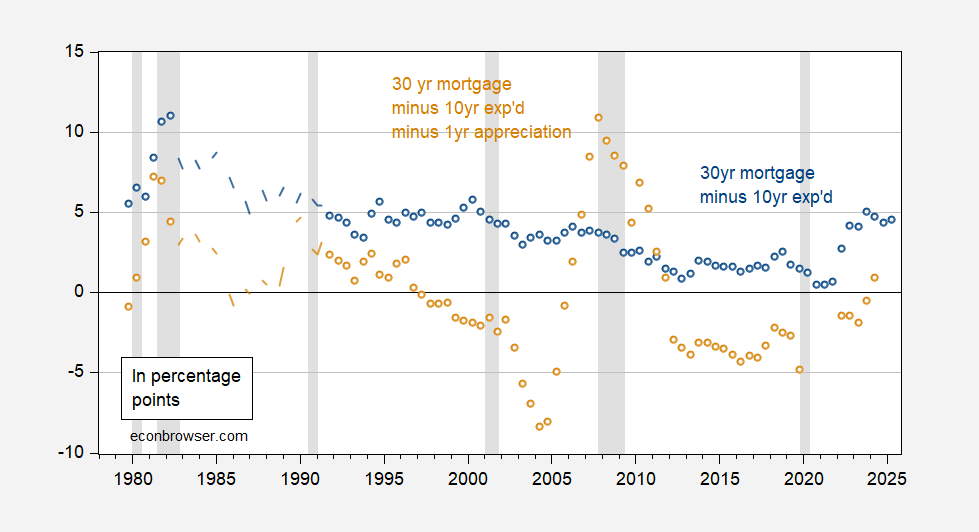

What about actual rates of interest? These are most related for the non-liquidity constrained brokers.

Determine 2: 30 12 months mortgage charges minus anticipated 10 12 months CPI inflation charges (blue), and 30 12 months mortgage charges minus anticipated 10 12 months CPI inflation charges minus ex publish future 12 months home value appreciation (tan), each in %. NBER outlined peak to trough recession dates shaded grey.Supply: Freddie Mac, FHFA through FRED, Blue Chip and Livingstone through Phildelphia Fed, NBER, and writer’s calculations.

The standard actual charge is proven because the blue circles/traces. Nevertheless, for belongings, the appreciation of the asset over time must be included. The tan line incorporating just one 12 months of future ex publish value appreciation is proven. This actual charge is roughly 2 proportion factors what held in 1979.

One implication of Determine 2 is that bringing down the nominal charge in and of itself is not going to have a big affect on the “actual charge of curiosity” for housing, outlined as an funding.

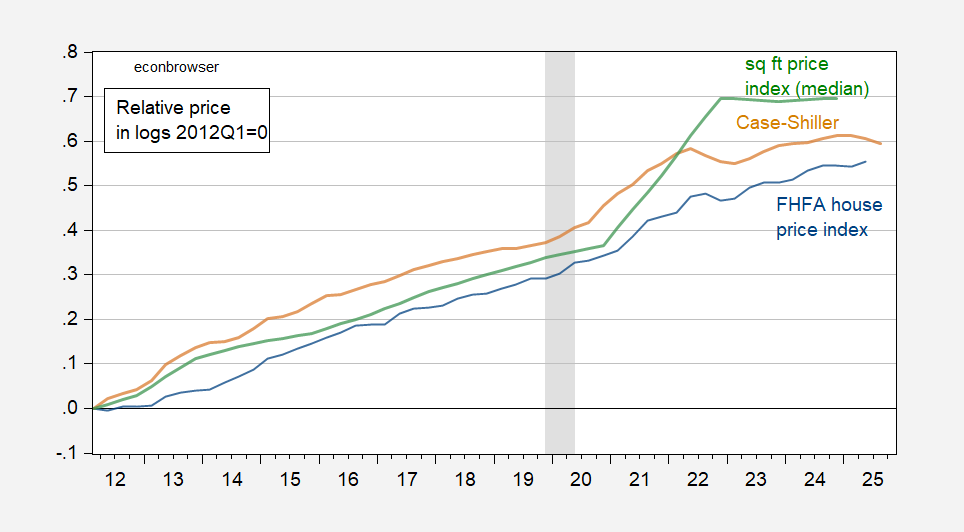

We have now extra information over the current interval, notably with respect to repeat-sales costs (the Case-Shiller index). Therefore, in utilizing this index, we’re controlling for measurement of home. As well as, we now have common and median costs per sq. foot of housing.

Determine 3: FHFA home value index (blue), Case-Shiller home value index – nationwide (tan), and median value per sq. foot of housing (inexperienced), deflated by CPI ex-shelter. NBER outlined peak-to-trough recession dates shaded grey. Annual sq. foot value measures linearly interpolated to quarterly frequency. Supply: FHFA, S&P, BLS through FRED, Census Bureau, NBER, and writer’s calculations.

Not one of the calculations embrace measures of credit score rationing, which might be essential given altering restrictiveness of lending necessities.

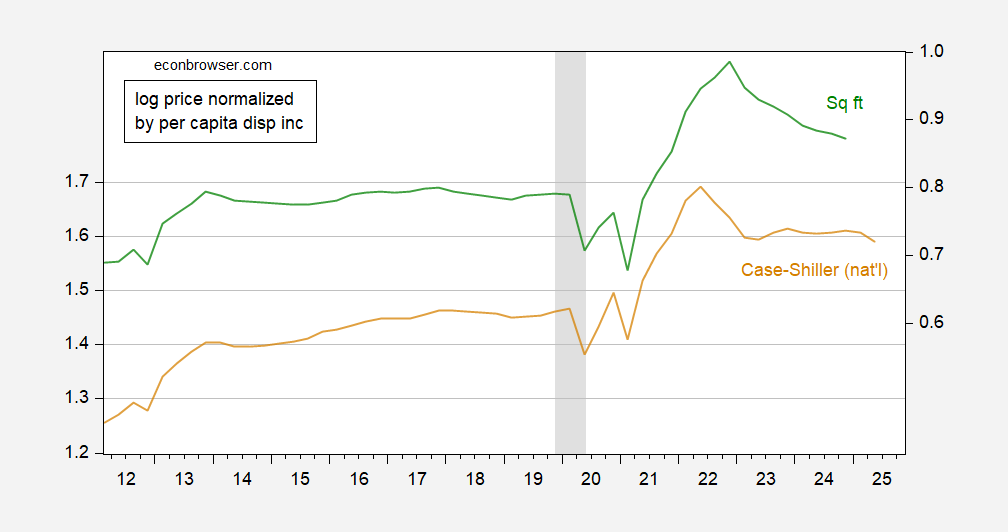

What about affordability when it comes to earnings? I may repeat the calculations utilizing common hourly earnings, however because the family distribution of out of doors work has modified, maybe it’s extra helpful to point out collection normalized by per capita disposable earnings.

Determine 4: Case-Shiller home value index – nationwide normalized by per capita disposable earnings (tan, left scale), and value of sq. foot of housing – median normalized by per capita disposable earnings (inexperienced, proper scale), each in logs. NBER outlined peak-to-trough recession dates shaded grey. Annual sq. foot value measures linearly interpolated to quarterly frequency. Supply; S&P, BEA through FRED, Census Bureau, NBER, and writer’s calculations.

In brief, I don’t suppose persons are “whining” with out some cause.

[ad_2]