[ad_1]

That’s immediately on Meet the Press. I agree that it doesn’t seem like we’re in a recession now, given the restricted quantity of present financial knowledge now we have; nonetheless what little employment knowledge now we have isn’t that encouraging.

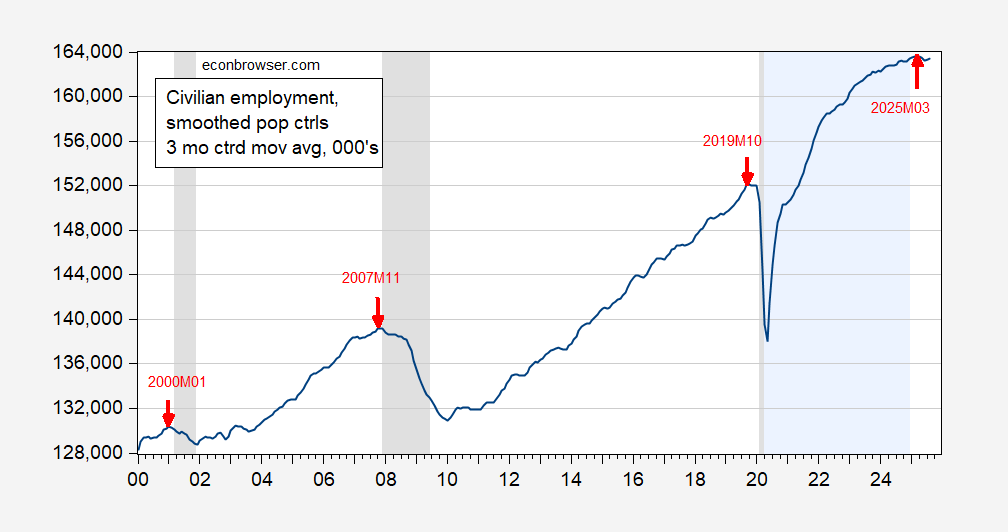

Determine 1: Three month centered shifting common of civilian employment (blue), in 000’s on log scale. April 2020-December 2024 knowledge is with smoothed inhabitants controls (interval denoted by mild shaded blue space). NBER outlined peak-to-trough recession dates shaded grey. Supply: BLS through FRED, BLS, NBER and creator’s calculations.

Be aware the native maxima are usually earlier than a NBER outlined peak (2000M01 precedes 2001M03, 2007M11 precedes 2007M12, 2019M10 precedes 2020M02).

Whereas I warn individuals about counting on the civilian sequence for prime frequency monitoring, it’s extra helpful trying on the implied tendencies – which is what I’m doing in Determine 1.

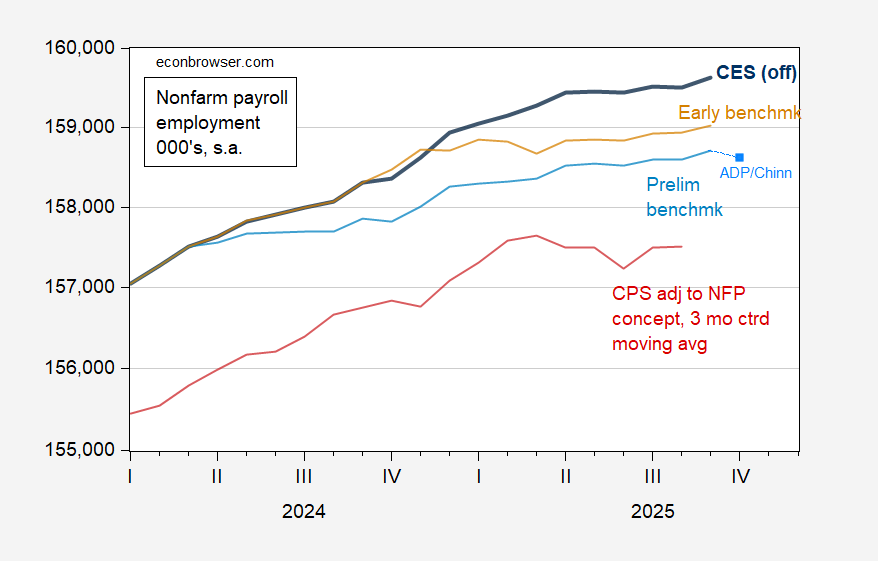

It’s additionally of curiosity to contemplate what the varied variations of the CES numbers point out:

Determine 2: Nonfarm payroll employment (official) (daring blue), implied preliminary benchmark revision, with April-September progress equal to official (mild blue), Chinn estimate based mostly on ADP knowledge (sky blue sq.), Early benchmark revision, with prolonged benchmark progress equal to official (tan), and Present Inhabitants Survey civilian employment adjusted to NFP idea, utilizing smoothed inhabitants controls, 3 month centered shifting common (crimson), all in 000’s, on log scale. Supply: BLS through FRED, BLS, Philadelphia Fed, and creator’s calculations.

The methodology to estimate October NFP (implied preliminary benchmark) is described right here, besides I now use a regression over 2022-2025M09 knowledge to foretell 2025M10 personal employment, add in 22K and subtract 150K (to account for deferred furlough program results).

Bessent’s assertion is much more daring than Lazear’s 2001 declare. We’ll see.

[ad_2]