[ad_1]

Munis have been little modified Monday because the new-issue market slows to a lackluster $1.154 billion this holiday-shortened week, with solely two offers above $100 million on faucet. U.S. Treasuries have been barely firmer and equities ended up.

The 2-year muni-UST ratio Monday was at 70%, the five-year at 67%, the 10-year at 68% and the 30-year at 89%, in accordance with Municipal Market Knowledge’s 3 p.m. EDT learn. ICE Knowledge Companies had the two-year at 70%, the five-year at 66%, the 10-year at 68% and the 30-year at 87% at a 4 p.m. learn.

“We don’t count on any main weak point to take maintain as the brand new challenge calendar is starting to dwindle with solely two non-holiday or non-Federal Reserve weeks left within the 12 months,” stated Birch Creek strategists.

Moreover, December reinvestment money is about to hit, and there appears to be “ample demand at adjusted ranges only a few foundation factors wider than the present provided aspect,” they stated.

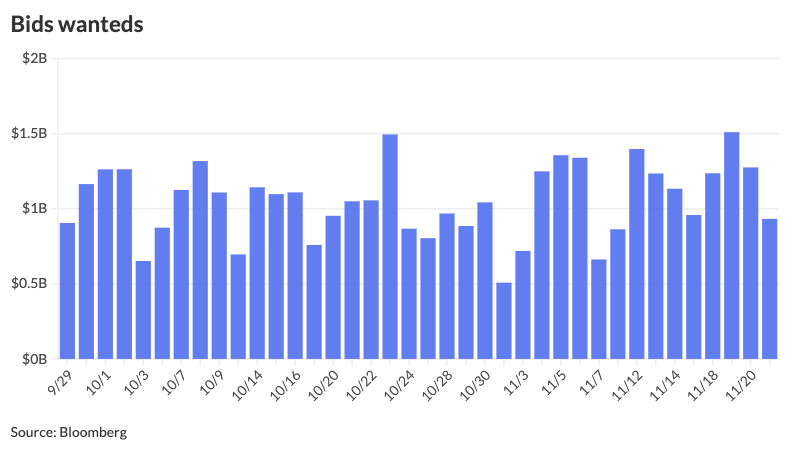

The secondary market is anticipated to “clear up” with this week’s main market pause, stated J.P. Morgan strategists led by Peter DeGroot.

The quiet on Monday continues from final week’s relative steadiness within the muni market, the place long-awaited financial information was launched following the tip of the federal government shutdown, stated Jason Wong, vp of municipal at AmeriVet Securities.

The

Final week, muni yields rose barely throughout the curve, with yields lower by a mean of 1.5 foundation factors, with yields on 10-year notes rising by 2.1 foundation factors, he stated.

“The rise in yields has pushed November returns barely decrease [to] 0.08% for the month and our year-to-date returns of 4%,” Wong stated.

Given final week’s sizable calendar and adverse fund flows, the muni market, following a latest bout of outperformance, felt a bit “caught,” Birch Creek strategists stated.

Buyers pulled $965.8 million from muni mutual funds final week, in accordance with LSEG Lipper. That is the biggest outflow determine because the week ending April 16, when the market was nonetheless coping with the tariff-induced volatility.

Nonetheless, the outflows have been pushed by a fund acquisition that occurred early final month. If this have been excluded, J.P. Morgan strategists estimate inflows would have continued with the addition of $130 million to mutual funds.

“With the outflows, heavy new issuance to give attention to, and conflicting views across the Fed’s subsequent transfer, sellers reported a cautious tone out of the gate,” Birch Creek strategists stated.

Whereas demand appeared to “agency up” on the entrance finish as offers have been launched, “investor hesitation to succeed in for longer length [last] week was evident in each new challenge subscriptions and secondary commerce circulate,” they stated.

Within the investment-grade market, the New York Metropolis Municipal Water Finance Authority’s $1.03 billion of water and sewer system second normal decision refunding income bonds noticed “its serials largely subscribed through the retail order interval, however the time period bonds in 2050 and 2055 have been widened 5 bps as a way to clear,” Birch Creek strategists stated.

Within the high-yield market, a $522 million BB-plus rated United Airways deal, issued by Houston, was downsized to $273 million with

A $94 million nonrated constitution faculty deal was shelved, whereas a $110 million nonrated resort deal acquired downsized and cheapened, Birch Creek strategists stated.

Conversely, some offers within the high-yield cleared with out a drawback, although there weren’t sturdy ranges of oversubscriptions, they stated.

AAA scales

MMD’s scale was unchanged: 2.52% in 2026 and a pair of.46% in 2027. The five-year was 2.41%, the 10-year was 2.75% and the 30-year was 4.16% at 3 p.m.

The ICE AAA yield curve was bumped as much as two foundation factors 15 years and in: 2.48% (-2) in 2026 and a pair of.46% (-1) in 2027. The five-year was at 2.41% (-2), the 10-year was at 2.76% (-2) and the 30-year was at 4.12% (+1) at 4 p.m.

The S&P International Market Intelligence municipal curve was unchanged: The one-year was at 2.51% in 2025 and a pair of.45% in 2026. The five-year was at 2.40%, the 10-year was at 2.75% and the 30-year yield was at 4.13% at 3 p.m.

Bloomberg BVAL was unchanged: 2.51% in 2025 and a pair of.46% in 2026. The five-year at 2.39%, the 10-year at 2.72% and the 30-year at 4.06% at 4 p.m.

Treasuries noticed small beneficial properties.

The 2-year UST was yielding 3.504% (-1), the three-year was at 3.49% (-1), the five-year at 3.606% (-2), the 10-year at 4.039% (-3), the 20-year at 4.642% (-3) and the 30-year at 4.68% (-3) close to the shut.

Main to return

The Pennsylvania Housing Finance Company (Aa1///) is about to cost Tuesday $275.54 million of single-family mortgage income bonds, consisting of $254.2 million of non-AMT social bonds, Collection 2025-151A, and $21.34 million of taxable, Collection 2025-151B. Barclays.

The New York State Mortgage Company (Aa1///) is about to cost Tuesday $107.805 million of social non-AMT home-owner mortgage income bonds, Collection 273. Jefferies LLC.

The Los Angeles Housing Authority (Aa1///) is about to cost Tuesday $78.697 million of multifamily housing income bonds (Victory Blvd), Collection 2025A. RBC Capital Markets.

The Jersey Metropolis Redevelopment Company is about to cost Tuesday $69.87 million of bonds from the Bayfront Redevelopment Mission, consisting of $60.3 million of Collection A and $9.57 million of Collection B. Stifel Nicolaus.

Aggressive

New Rochelle, New York, is about to promote $40.874 million bond anticipation notes at 11 a.m. Jap Tuesday.

[ad_2]