[ad_1]

Yves right here. Despite the fact that anybody who took a primary economics class realized that monopolists and oligopolists set costs greater than sellers do in aggressive market, pols, pundits, and the press are bizarrely loath to level that out in actual world conditions. They appear to have been brainwashed that bigger = extra environment friendly, and that these effectivity financial savings will likely be partly handed on to clients. The put up under is one more demonstration that the businesses in dominant positions can and do set dictate costs, and accomplish that in occasions when inflation begins ticking up. It successfully proves the incorrectly-derided “greedflation” thesis.

But the authors made some extent of not saying something so direct. The unique article headline was The granular origins of inflation. Since when does “granular” evoke “large”? Simply learn the overview paragraph under and see how they bafflegab their essential findings.

By Santiago Alvarez-Blaser; Raphael Auer, Head, BISIH Eurosystem Centre Financial institution For Worldwide Settlements; Sarah Lein, Analysis Community Fellow CESifo; School Member Swiss Finance Institute; Full Professor of Macroeconomics College Of Basel; and Andrei Levchenko, John W. Sweetland Professor of Worldwide Economics College of Michigan, Ann Arbor Initially revealed at VoxEU

Textbook financial economics views inflation as basically pushed by combination shocks, comparable to cash provide or coverage charges. This column presents empirical proof that inflation is extremely granular – it’s considerably influenced by the costs set by a small variety of massive companies. Based mostly on an evaluation of two.9 billion barcode-level transactions spanning 16 economies, it reveals that firm-level idiosyncratic shocks account for a considerable share of inflation variability in superior economies. Granular forces had been additionally a key driver of the 2021–22 inflation shock and are proven to decelerate the transmission of financial coverage.

What’s the position of huge companies in combination inflation, and what are the causes and implications of such ‘inflation granularity’? Textbook financial economics views inflation as basically pushed by combination shocks, comparable to cash provide or coverage charges (Woodford 2003, Galí 2015). Whereas the literature fashions wealthy micro-level value adjustment heterogeneities, idiosyncratic agency behaviour is usually built-in out, leaving no position for particular person companies in combination inflation. On the similar time, following Gabaix’s (2011) seminal contribution, an influential strand of the macro literature has modelled theoretically and documented empirically that shocks to particular person (massive) companies can generate combination fluctuations.

In latest analysis (Alvarez-Blaser et al. 2025), we make clear this challenge. We analyse a multi-country home-scan dataset spanning roughly 2.9 billion barcode-level transactions and 16 superior and rising economies. Every merchandise is linked to a producing agency and a product class, in addition to a retailer.

We begin by displaying that the preconditions for granularity are current within the information, as expenditure is extremely concentrated: within the common superior financial system, the highest ten companies account for about 41% of gross sales and the highest ten classes for round 48%. There may be additionally a excessive diploma of synchronisation of value adjustments inside multi-product companies and inside classes.

We subsequent develop an additive decomposition of combination inflation right into a macro part (i.e. country-level unweighted averages) plus granular residuals on the agency and class ranges. Our decomposition generalises the standard granular residual setup (e.g. Gabaix 2011, di Giovanni et al. 2014, Gabaix and Koijen 2024) in two dimensions. First, we permit for a number of non-nested dimensions of granularity (companies, classes, and, in an extension, retailers). Second, a granular residual can come up both from idiosyncratic shocks to massive companies or from differential responses of huge companies to frequent shocks. 1 Our notion of granular residual explicitly permits for each of those driving forces. We doc which one is extra highly effective in our context.

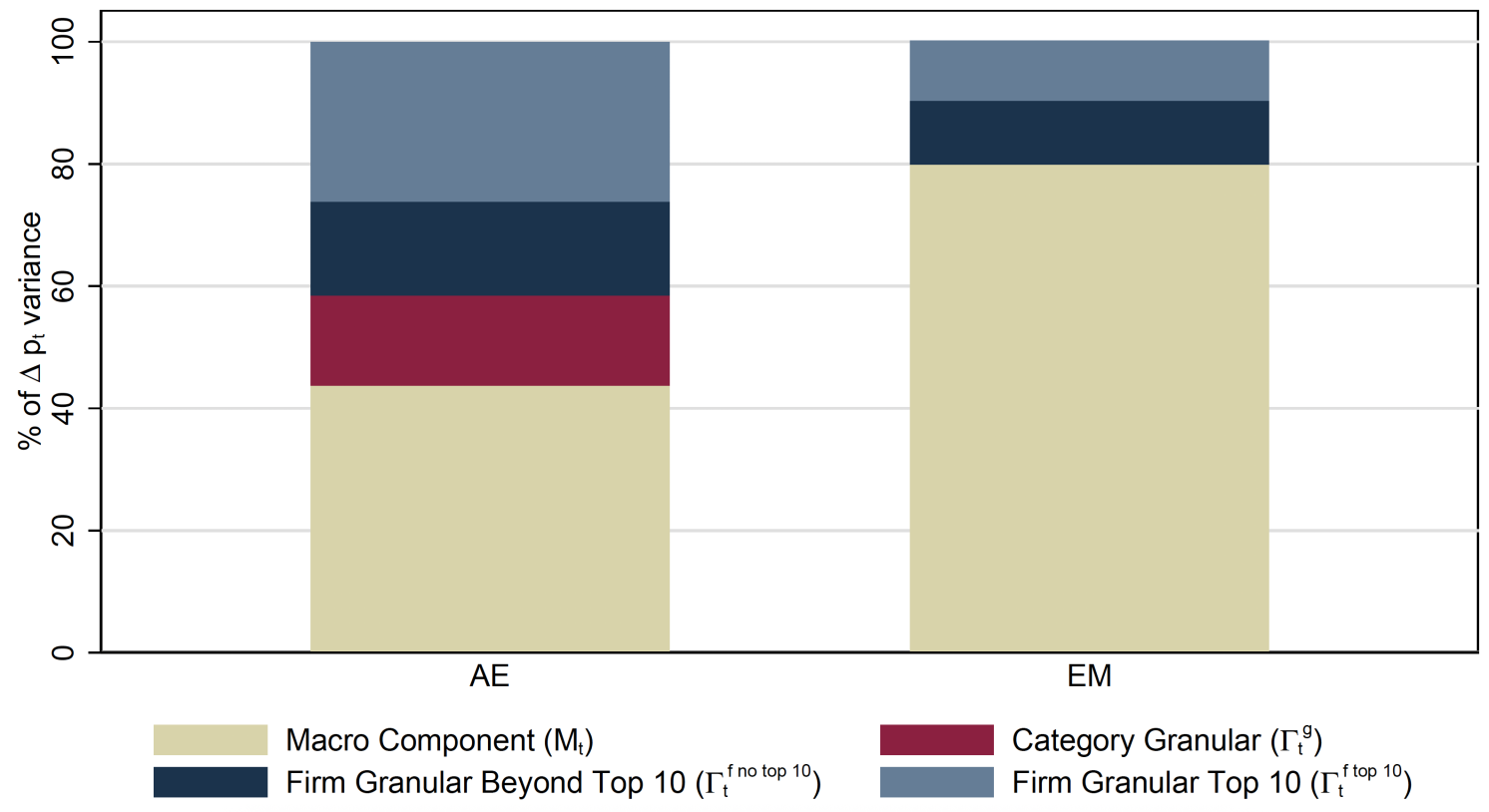

Determine 1 shows the high-level outcomes of our evaluation. On the macro stage, the agency and class granular elements account for 56% of the inflation variance in superior economies over the 2005-2020 interval (see the left-hand column of Determine 1). The agency granular residual is comparatively extra essential, explaining some 41% of inflation variance. Twenty-six share factors (darkish crimson) are accounted for by the ten largest companies alone, and the remaining 15 share factors by massive companies that aren’t within the prime ten (mild crimson). The class granular residual accounts for an extra 15% of inflation variance (yellow space). We subsequent decompose the granular residuals into the elements because of the differential responsiveness to frequent shocks, and the idiosyncratic shocks. The agency granular residual is predominantly pushed by idiosyncratic shocks. In contrast, greater than half of the variability within the class granular residual is because of the classes’ differential responsiveness to frequent shocks.

Determine 1 Contributions of granular elements to retail inflation variation

Notice: This determine shows the share of the variance of combination year-on-year inflation accounted for by every part.

Granularities are a much less essential in rising markets (see the right-hand column of Determine 1), the place inflation is greater on common and market shares are much less concentrated: the mixed agency and class residual explains about 20% of inflation variance.

Market Share Focus and Inflation Granularity

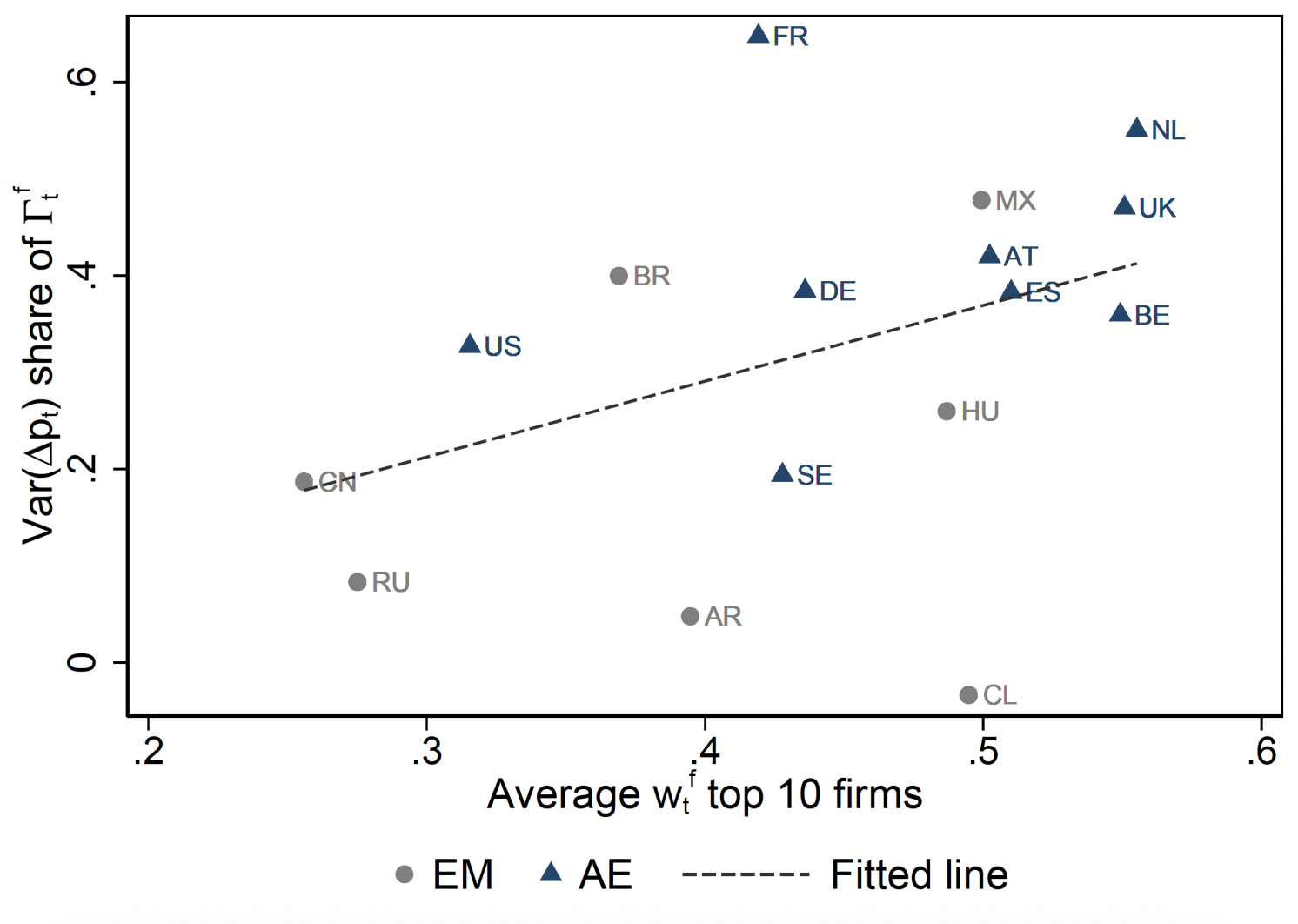

We subsequent examine how the cross-country variations in inflation granularity relate to market focus in these international locations. Specifically, we relate the explanatory energy of granular residuals to the market shares of the highest companies. Determine 2 shows a scatterplot of the variance share in complete inflation accounted for by the highest ten companies towards the typical market share of the highest ten companies in every nation. There’s a optimistic and statistically vital relationship, suggesting that granular results are stronger in international locations with greater market focus.

Determine 2 Granularity and market focus

Notice: The determine shows a scatterplot of the share of the variance of combination year-on-year inflation accounted by the agency granular residual towards the expenditure share of prime 10 companies. The dashed line is a linear match with a slope of 0.78 (strong commonplace error of 0.31) and R-squared of 0.16 (N=16)

This correlation means that developments in market focus, as documented for instance in Autor et al. (2020), could coincide with an growing position of agency granularities in combination inflation dynamics.

The 2021–22 Inflation Surge

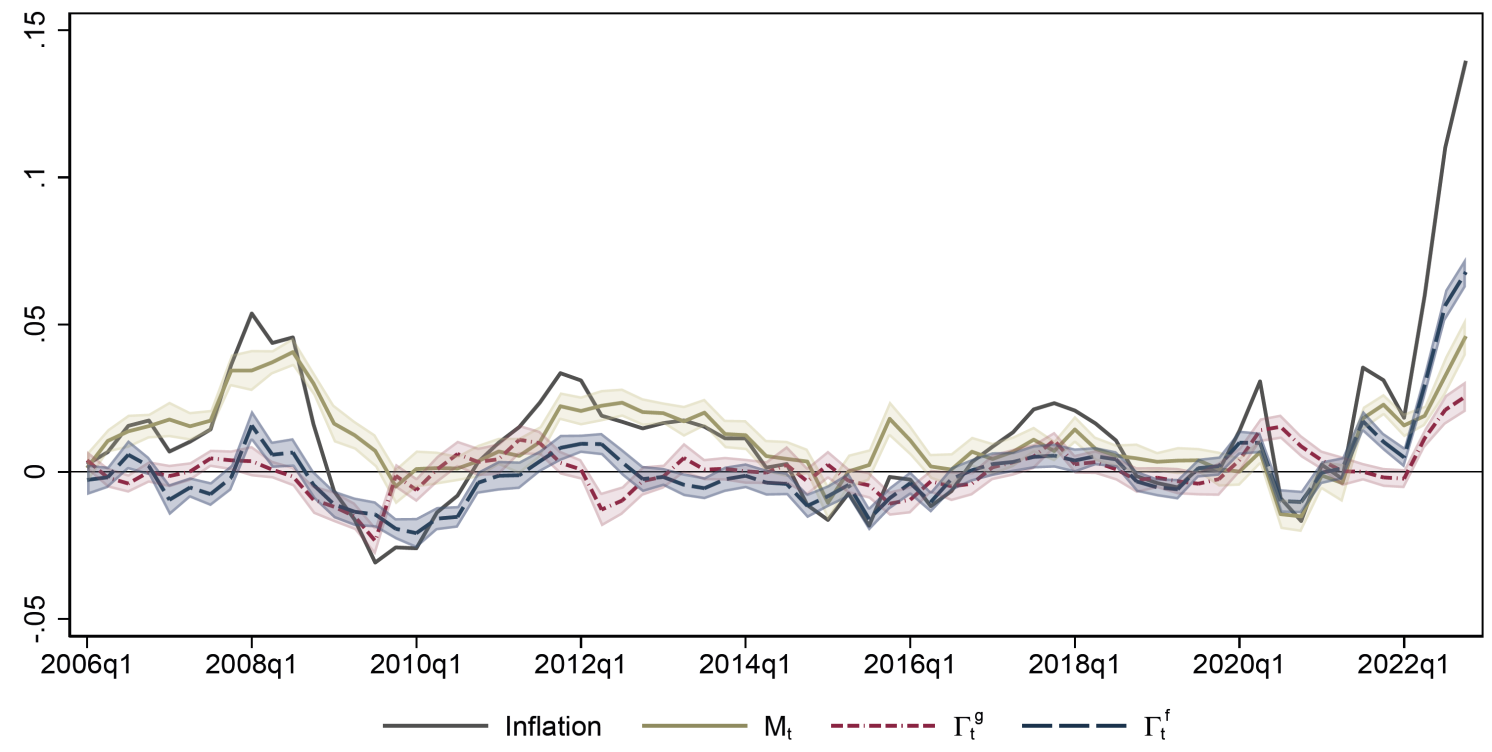

In the course of the post-pandemic interval, granular forces elevated in relative significance in superior economies. On common, the agency granular part accounts for a large fraction of the 2021–22 inflation fee, reflecting each idiosyncratic shocks and heightened sensitivity of huge companies to frequent disturbances (e.g. provide bottlenecks, vitality). This once more highlights the position of huge companies and multi-product value synchronization in amplifying macro shocks.

Determine 3 exemplifies these findings for Germany. Its reveals general inflation (stable line) cut up into the unweighted common (the macro part, dashed line) and the granular elements (the sum of the agency and sectoral one). The determine reveals that through the inflation surge, granular forces performed a bigger position.

Determine 3 Germany: Combination retail inflation and granular elements – retailer dimension

Notice: This determine shows the mixture year-on-year inflation and every part. The remainder of the international locations and figures displaying all accessible years may be present in the principle paper.

Implications for Financial Coverage Effectiveness

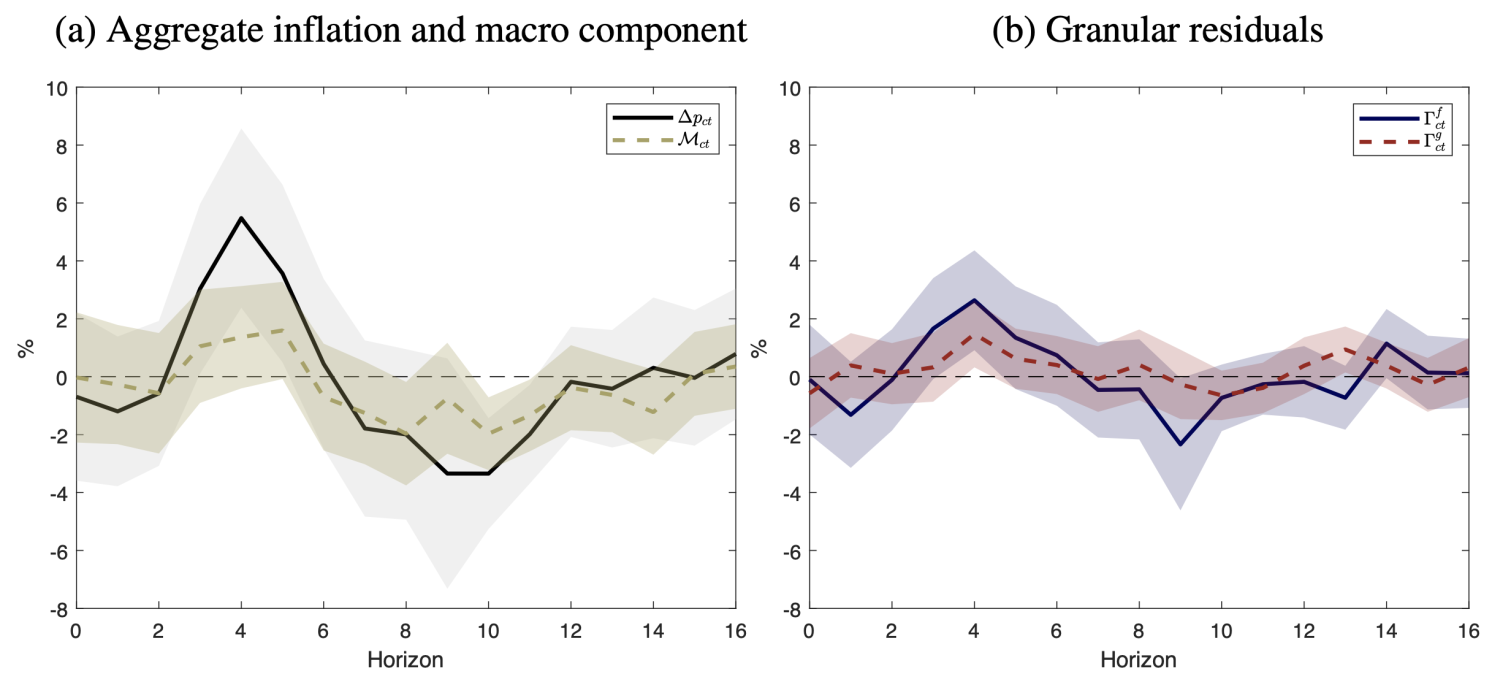

A key coverage result’s that granularity alters the impulse response of inflation to contractionary financial coverage. In native projection estimates for the US and the euro space, combination inflation shows a short-run ‘value puzzle’, in line with earlier proof comparable to Christiano et al. (1999). This preliminary enhance is nearly completely pushed by the granular elements, which collectively account for roughly three-quarters of the short-run rise. In contrast, the macro part doesn’t elevate inflation within the 12 months following the financial coverage shock – it reveals no vital response for about 5 quarters after which declines, according to commonplace theoretical predictions. This means that market focus and the pricing behaviour of huge companies can delay disinflation, weakening near-term transmission. Put otherwise, in additional concentrated environments, financial non-neutrality is formed by the behaviour of a small set of huge price-setters whose pass-through of financing and input-cost shocks could also be stronger.

Determine 4 Impulse response capabilities for combination inflation and elements

Notes: Panel (a) reveals the quarterly native projection outcomes for all elements aggregated into general year-on-year inflation, in addition to for the macro part alone. Panel (b) presents the corresponding outcomes for the firm-level and category-level granular residuals. Shaded areas point out 90% confidence intervals based mostly on HAC commonplace errors.

Conclusion

We present that inflation in superior economies is extremely granular, i.e. it’s considerably influenced by the costs set by a small variety of massive companies. Within the cross-section of nations, granular residuals are much less essential in economies with much less concentrated market shares and better inflation, comparable to rising markets. Granular residuals contributed to the post-COVID inflation surge, with the firm-level part accounting for roughly one-third of the 2021-2022 inflation in superior economies.

General, these findings spotlight that granular components past conventional macroeconomic determinants matter enormously in shaping inflation, which additionally impacts the effectiveness of financial coverage and therefore the conduct of financial coverage. An operational takeaway is that granular value microdata of huge companies and merchandise are a precious enter for inflation nowcasting. The ECB’s Each day Worth dataset and the BIS Innovation Hub’s Venture Spectrum are examples of efforts to develop instruments for real-time analytics and nowcasting based mostly on detailed costs, enhancing sign extraction from inflation (BIS Innovation Hub 2025).

______

- Since we observe costs however not marginal prices, we can not separate the noticed value adjustments into markup changes versus price adjustments. Thus, our findings don’t instantly converse to a latest debate on whether or not massive companies had disproportionately raised their markups through the 2021-22 inflation surge (i.e. the so-called ‘greedflation’ or ‘vendor’s inflation’ debate). Out there empirical proof means that markup adjustment was not a significant driver within the inflation surge (e.g. Alvarez-Blaser et al. 2024).

See authentic put up for references

[ad_2]