[ad_1]

Munis have been regular forward of the Thanksgiving vacation as issuance rebounds to $10.9 billion for the primary week of December. U.S. Treasuries have been little modified and equities have been up.

The 2-year muni-UST ratio Wednesday was at 70%, the five-year at 67%, the 10-year at 69% and the 30-year at 90%, in line with Municipal Market Knowledge’s 3 p.m. EDT learn. ICE Knowledge Providers had the two-year at 70%, the five-year at 67%, the 10-year at 69% and the 30-year at 88% at a 3 p.m. learn.

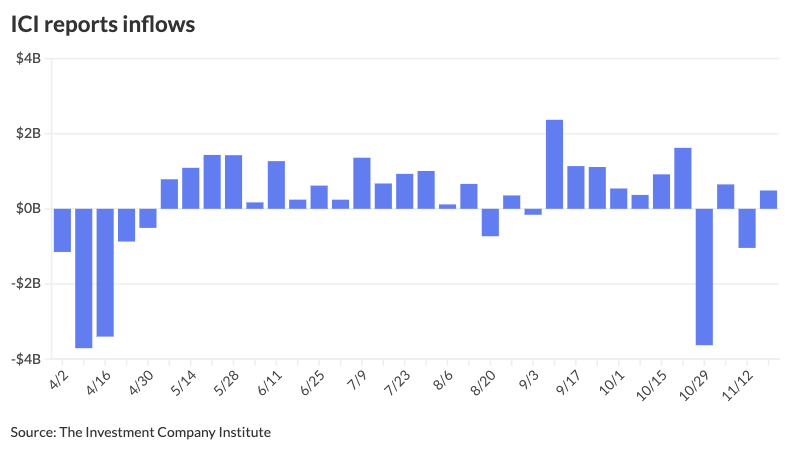

The Funding Firm Institute Wednesday reported inflows of $488 million for the week ending Nov. 19, following $1.042 billion of outflows the earlier week. This differs from the $965.8 million of outflows, as reported by LSEG Lipper, over the identical time interval.

Trade-traded funds noticed inflows of $366 million after $2.735 billion of inflows the week prior, per ICI knowledge.

November’s provide was extra “benign” this month in comparison with earlier months, stated Kim Olsan, senior fastened revenue portfolio supervisor at NewSquare Capital.

Preliminary November issuance figures are at $37.054 billion, up 45.5% year-over-year, in line with LSEG.

“That determine remains to be a wholesome weekly common however is effectively off April by means of August and September, when the month-to-month complete exceeded $50 billion (the biggest month was June at $58.8 billion issued),” Olsan stated.

As a “supply-centric market,” munis, in comparison with different asset lessons, have sure concerns, together with a “smaller purchaser base to leverage the tax-advantaged nature of the product,” she stated.

As December begins, sure parts will play a task in yearend efficiency, Olsan stated.

“An obstacle to quick, fixed-coupon commitments has been excessive money-market charges,” she stated.

Day by day and weekly reset floaters are buying and selling with 2.75% yields, however one-year bonds yield round 25 foundation factors lower than that. For instance, Aaa/AA-plus Denver faculty 5s due 12/1/26 have been bought at 2.52%, Olsan stated.

November’s exchange-traded fund flows, “consumption ranges turned relatively anemic mid-month, with nobody technique dominating flows,” she stated.

ETFs noticed round $2.59 billion in inflows in November, “close to parity” with the typical of the earlier 10 months, Olsan stated.

Extra lively flows have been “discouraged” on account of “flat and inverted circumstances” 10 years and in, she stated.

“A ten-basis-point inversion within the five-year vary has patrons maneuvering round this vary to maximise yields (primarily with quick calls or lower-rated bonds),” Olsan stated.

“An extension into 10 years nets a few 30-basis-point pickup, however with uncooked yields round 2.75%, the taxable-equivalent element falls wanting many patrons’ 5.00% bogey,” she stated.

One caveat is that with the 10-year UST closing at 3.99% Tuesday, cross-market ratios have improved, nearing 70% as soon as extra, Olsan stated.

“Within the longer-intermediate vary, greater than 100 foundation factors of yield may be discovered in comparison with the 10-year vary,” she stated.

“The coupon element distinctive to municipal financing — with 3s and 4s accessible in longer maturities — provides an fascinating choice, significantly with larger efficiency potential if charges decline by means of 2026,” Olsan stated.

Internet provide worth was smaller earlier this yr, with fewer maturities and calls occurring towards provide. Between January and June, the online common worth was detrimental $5 billion, Olsan stated.

“March and April’s upward yield transfer correlated with lowered demand on lighter redemption totals,” she stated.

The “lively” summer season months noticed a complete of $45 billion net-negative provide, Olsan stated, ensuing within the 10-year AAA BVAL yield rallying a median of 10 foundation factors from June to September.

With present estimates of net-negative worth at $18 billion, this might probably set the market up for a year-end rally, she stated.

Final yr was the one yr over the previous decade to see a market loss in December, with the typical return for the month at +0.6%, Olsan stated.

New-issue calendar

The brand new-issue calendar surges to an estimated $10.932 billion, with $8.92 billion negotiated offers on faucet and $2.013 billion of competitives.

Connecticut leads the aggressive calendar with $1.56 million of particular tax obligation bonds, adopted by the Utility Debt Securitization Authority with $1.026 billion of restructuring bonds and Massachusetts with $1.019 billion of GOs.

The aggressive calendar is led by the California Infrastructure and Financial Improvement Financial institution with $554.625 million of Clear Water and Consuming Water State Revolving Fund income bonds.

AAA scales

MMD’s scale was bumped two foundation factors 4 years and in: 2.50% (-2) in 2026 and a pair of.44% (-2) in 2027. The five-year was 2.41% (unch), the 10-year was 2.75% (unch) and the 30-year was 4.16% (unch) at 3 p.m.

The ICE AAA yield curve was bumped a foundation level: 2.47% (-1) in 2026 and a pair of.45% (-1) in 2027. The five-year was at 2.40% (-1), the 10-year was at 2.75% (-1) and the 30-year was at 4.10% (-1) at 3 p.m.

The S&P World Market Intelligence municipal curve was little modified: The one-year was at 2.50% (-1) in 2025 and a pair of.44% (-1) in 2026. The five-year was at 2.40% (unch), the 10-year was at 2.75% (unch) and the 30-year yield was at 4.13% (unch) at 3 p.m.

Bloomberg BVAL was unchanged: 2.50% in 2025 and a pair of.46% in 2026. The five-year at 2.39%, the 10-year at 2.72% and the 30-year at 4.05% at 3 p.m.

Treasuries have been little modified.

The 2-year UST was yielding 3.482% (+2), the three-year was at 3.473% (+2), the five-year at 3.573% (+1), the 10-year at 3.997% (flat), the 20-year at 4.603% (flat) and the 30-year at 4.643% (-1) at 3 p.m.

[ad_2]