[ad_1]

With NFP at +22K < +75K Bloomberg consensus (hinted at by Trump signaling “pay no heed to the numbers backstage”), we have now the next image of key indicators of the NBER’s BCDC (together with the 48K downward revision in earlier two months):

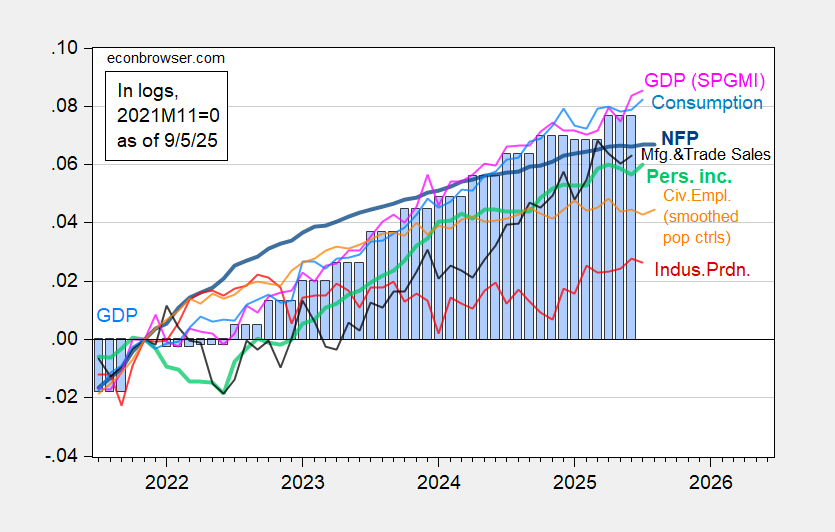

Determine 1: Nonfarm Payroll from CES (daring blue), civilian employment with smoothed inhabitants controls (orange), industrial manufacturing (crimson), Bloomberg consensus industrial manufacturing of 8/14, (crimson sq.), private earnings excluding present transfers in Ch.2017$ (daring gentle inexperienced), manufacturing and commerce gross sales in Ch.2017$ (black), consumption in Ch.2017$ (gentle blue), and month-to-month GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Supply: BLS by way of FRED, Federal Reserve, BEA 2025Q2 second launch, S&P World Market Insights (nee Macroeconomic Advisers, IHS Markit) (9/2/2025 launch), and creator’s calculations.

Discover that the Imply Absolute Revision going from first to 3rd launch in 2022-24 interval is about 40K, so the approximate 95% confidence interval is -62K to +102K.

Whereas smoothed civilian employment rose barely (orange line), given the variability on this sequence, needs to be taken as primarily zero progress. General, civilian employment is beneath latest peak. All in all, these numbers are according to a cooling labor market, as mentioned in yesterday’s publish.

Month-to-month GDP launched on Tuesday by S&P World, rose at a decelerated fee — 2.4% m/m AR in July vs. 11% in June.

[ad_2]