[ad_1]

A latest column mentioned Well being Financial savings Accounts (HSAs). There are a number of necessities for a federal worker or retiree to contribute to an HSA, a very powerful of which is being enrolled in a high-deductible well being plan (HDHP). The Federal Workers Well being Advantages (FEHB) program affords a number of well being plans that meet the IRS definition of an HDHP. However there are some staff and retirees who whereas they’re enrolled in an HDHP, they don’t meet a number of the different necessities to contribute to an HSA. In that case, the FEHB program will present these staff with a Well being Reimbursement Account (HRA). This column discusses what an HRA is and the way federal staff who’ve entry to an HRA can put it to use.

An HRA is an employer-funded tax-sheltered account that’s used to reimburse allowable medical bills incurred by the HDHP enrollee and eligible members of the family. Federal staff and retirees enrolled in an HDHP within the FEHB program who usually are not eligible to contribute to an HSA might be robotically enrolled in an HRA. There isn’t a further paperwork wanted by the worker for enrollment into the HRA. The next instance illustrates:

Steve, a federal worker aged 65, has been enrolled in an FEHB program HDHP since 2018. Through the previous seven years, Steve has contributed to his HSA related together with his HDHP. Steve enrolled in Medicare Half A when he grew to become age 65 in October 2025. An HSA proprietor who enrolls in Medicare is now not eligible to contribute to his or her HSA. If through the present FEHB open season Steve decides to stay in his HDHP, he might be robotically enrolled in an HRA. It’s because Steve has enrolled in Medicare and is due to this fact now not eligible to contribute to his HSA.

Options of an HRA

The next are options of an HRA:

(1) Tax-free withdrawals to pay certified medical bills; (2) Carryover of unused HRA credit with out restrict from yr to yr and into retirement; and (3) Administration of the worker’s HRA is carried out by the worker’s HDHP well being plan.

How An FEHB-Sponsored HDHP Works with an HRA

The next steps clarify how an FEHB program HDHP works with an HRA:

Step 1. A federal worker is enrolled or enrolls in an HDHP within the FEHB program.

Step 2. The worker’s FEHB program HDHP establishes an HRA for the worker. Every HDHP has extra data on how this step works.

Step 3. The worker’s or retiree’s HDHP will credit score a portion of the HDHP premium to the HRA at first of every calendar yr. Observe that the credit score quantity for both a Self Solely enrollment or a Self Plus One/Self and Household enrollment is identical greenback quantity that’s deposited (referred to as the “premium pass-through”) into an HSA (for workers eligible to contribute to HSAs in the identical FEHB program HDHP).

Step 4. When an worker or a member of the family enrolled within the HDHP related to an HRA wants preventive well being care (contains periodic well being evaluations, routine prenatal and well-children visits, and screening companies), the worker’s HDHP will present it with out price to the worker. Preventive care is topic to any limits outlined within the HDHP’s brochure.

Step 5. The worker makes use of funds within the HRA to assist pay the HDHP deductible when non-preventive care is required. For these federal retirees enrolled in Medicare Half B and Medicare Half D, withdrawals from the HRA will also be used to reimburse Medicare Half B and Medicare Half D month-to-month premiums.

Step 6. If an worker or retiree reaches the HDHP’s catastrophic restrict, then the HDHP can pay for one hundred pc of the wanted care with the HDHP participant owing no co-payment or co-insurance. With most HDHP plans, this assumes that the wanted care is supplied by in-network suppliers.

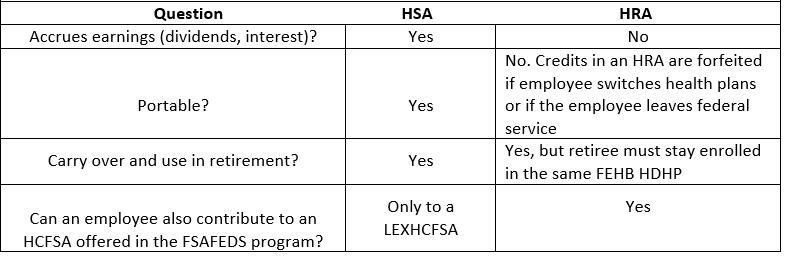

The next desk presents the variations between an HRA and an HSA, each related to enrollment in an HDHP that’s accessible to staff within the FEHB program:

Variations between an HRA and an HSA

Abstract

Abstract

An HRA is an association by which an employer (the sponsor of a gaggle medical health insurance plan, on this case, the federal authorities by the FEHB program) helps pay the medical bills of its staff and retirees. The worker’s FEHB program HDHP plan decides how a lot cash it would put into the HRA on behalf of the worker, and the worker can request reimbursement for precise medical bills incurred as much as that quantity.

An HRA will not be a medical-oriented financial savings account. Which means that staff and retirees can not withdraw funds upfront after which use them to pay qualifying medical bills. As an alternative, they have to incur the expense first after which get reimbursed by the HRA for the quantity they spent.

An worker or a retiree who makes use of up all of the allotted funds within the HRA earlier than year-end should pay any subsequent well being payments out-of-pocket or, if enrolled in an HCFSA, with the funds within the HCFSA. If an worker or a retiree has any remaining funds in an HSA that the worker beforehand was capable of fund however can now not contribute to, then the worker or retiree can withdraw from the HSA to pay these certified medical bills as properly.

Limitations of HRAs

An HRA reimburses solely certified medical bills. In keeping with the IRS, medical bills are bills incurred to alleviate or stop a bodily or psychological ailment, not bills to take care of basic well being reminiscent of nutritional vitamins.

The HRA can’t be used to reimburse for medical bills that aren’t deemed crucial reminiscent of enamel whitening, funeral companies or non-prescription medicines. The HRA is about up by the HDHP who decides how a lot cash goes into the HRA. For non-preventive care, an HRA participant can not withdraw funds first after which pay qualifying medical bills. The HRA participant should pay the bills first after which wait to get reimbursed.

The next desk presents a comparability of an HRA, a well being care versatile spending account (HCFSA) and an HSA:

HRA Versus HCFSA Versus HSA Comparability

[ad_2]