[ad_1]

5,150%.

That’s the approximate return I might’ve made if I’d trusted myself.

It was 2022, nonetheless deep within the pandemic’s lengthy fade-out. Many industries had been beneath strain, and the auto market was one of many hardest hit. With little journey and even much less commuting, demand slid and your complete sector slowed.

However in the midst of that slowdown, one thing caught my consideration. It wasn’t loud. It wasn’t apparent. It was a small however regular shift happening the place virtually nobody was wanting.

I used to be satisfied sufficient to message my colleagues about it.

Carvana (NYSE: CVNA) had fallen 97%. “Deep worth” barely captured it.

I’m a dedicated worth investor, however even I hesitated. A collapse that sharp made me assume the market should’ve identified one thing I didn’t.

So I held again because the inventory closed at $8.76 that day.

However inside a yr, it was buying and selling close to $56 – a acquire of properly over 500%. And this week, it pushed previous $460.

Once more, that’s a greater than 50-FOLD acquire.

It’s a second that stays with you – not due to the cash, however as a result of it reminds you ways onerous it may be to behave when the group is working the opposite approach.

That lesson is helpful now as we ask a special query: After such a dramatic rise, the place does the inventory stand immediately?

Carvana has settled into its position as a full-scale on-line market for used vehicles. Consumers can discover a automobile, line up financing, deal with the paperwork, and organize supply with out stepping right into a dealership. And up to date outcomes make it clear that the mannequin is working at scale.

Retail items hit a report 155,941 within the third quarter, up 44% from final yr. Income jumped 55% to $5.6 billion. Web revenue reached $263 million, whereas working margins climbed to 9.8% – each firm information.

Much more hanging, Carvana crossed a $20 billion income run charge. Administration says the agency now has reconditioning and manufacturing capability for greater than 1.5 million retail items a yr, with long-term targets of promoting 3 million.

These good points aren’t coming from hype alone. Carvana continues to bolt ADESA’s community into its system, including extra websites the place vehicles will be processed and delivered quicker and at decrease price. The earnings launch exhibits this technique is lifting each scale and effectivity.

However robust numbers don’t reply the central query: What’s the inventory value proper now?

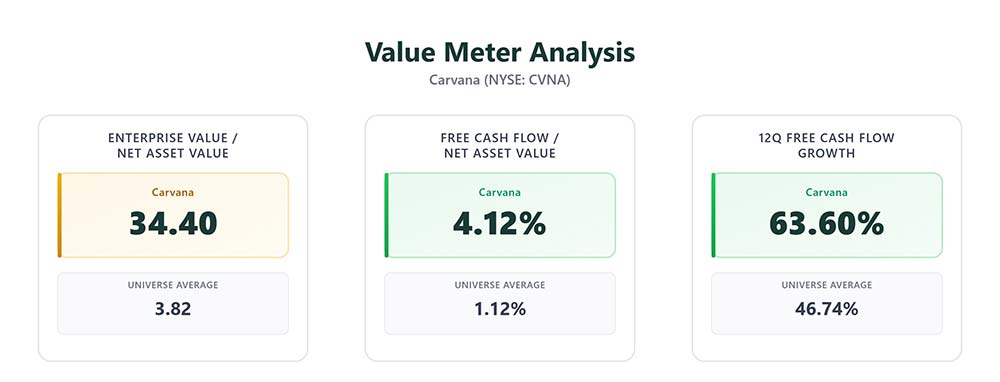

Carvana’s enterprise value-to-net asset worth sits at 34.40, far above the universe common of three.82. Which means buyers are paying a steep premium for every greenback of web belongings. On that measure, the inventory is dear.

Its money era tells a special story. Free money flow-to-NAV is 4.12%, versus a universe common of 1.12%. And over the previous 12 quarters, Carvana has grown its free money movement almost 64% of the time – properly above the 46.74% common.

That form of consistency is unusual, particularly for a enterprise that when regarded fragile.

Whereas the inventory isn’t the deep-value setup it as soon as was, it’s surprisingly not priced past cause both. Right now’s valuation displays a enterprise that’s lastly delivering the dimensions and profitability buyers doubted it may obtain.

In case you already personal shares, nothing within the numbers suggests urgency. In case you’re contemplating coming into now, endurance could reward you with a greater setup.

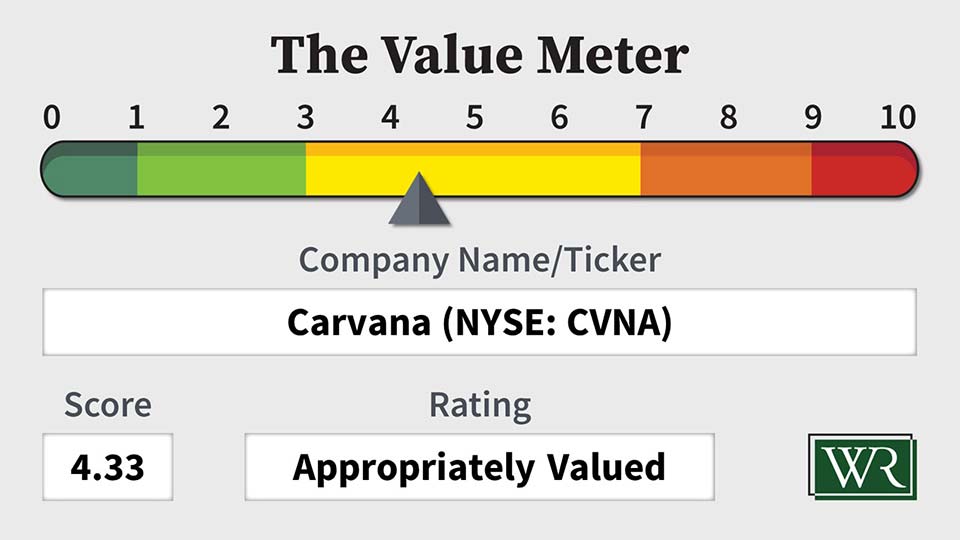

The Worth Meter charges Carvana as “Appropriately Valued.”

What inventory would you want me to run via The Worth Meter subsequent? Publish the ticker image(s) within the feedback part under.

[ad_2]