[ad_1]

I’ve realized the exhausting method that nice tales don’t at all times make nice investments.

When a inventory dominates headlines and dinner conversations, the simple cash is normally gone. That doesn’t make it a foul enterprise. It simply means the market has already achieved the rewarding.

I believe that could be the place Superior Micro Gadgets (Nasdaq: AMD) sits at this time. The corporate is now not the challenger it as soon as was. It’s a fixture of the fashionable tech panorama.

Its chips energy servers, PCs, gaming consoles, and now among the most demanding AI workloads on the planet. And traders know this. That’s why the inventory worth displays it.

As you possibly can see, after spending a lot of final yr constructing a base, AMD didn’t grind increased. It surged. Shares leapt from beneath $80 in April to nicely above $250 in a brief window earlier than volatility set in.

Now, it’s simple to take a look at AMD and see a “chipmaker.” However that may be reductive.

The corporate designs high-performance semiconductors throughout information facilities, shopper gadgets, gaming, and different computation-heavy ecosystems. These days, which means the corporate sits on the intersection of cloud computing and synthetic intelligence.

That’s a strong place to be – because the market acknowledges. Nevertheless it’s additionally a crowded one.

The most recent quarter reveals that the enterprise is firing on all cylinders. Income rose 36% yr over yr to $9.2 billion, pushed by power in information facilities, AI accelerators, and consumer CPUs. Working revenue expanded. Free money movement hit a document $1.5 billion.

The stability sheet is stable: over $7 billion in money and about $3.2 billion in debt. AMD has room to take a position with out stretching itself.

It is a stable enterprise producing nice money movement.

However the query isn’t whether or not AMD is a good firm. (It’s.) The actual query is whether or not you’re being provided worth at at this time’s worth.

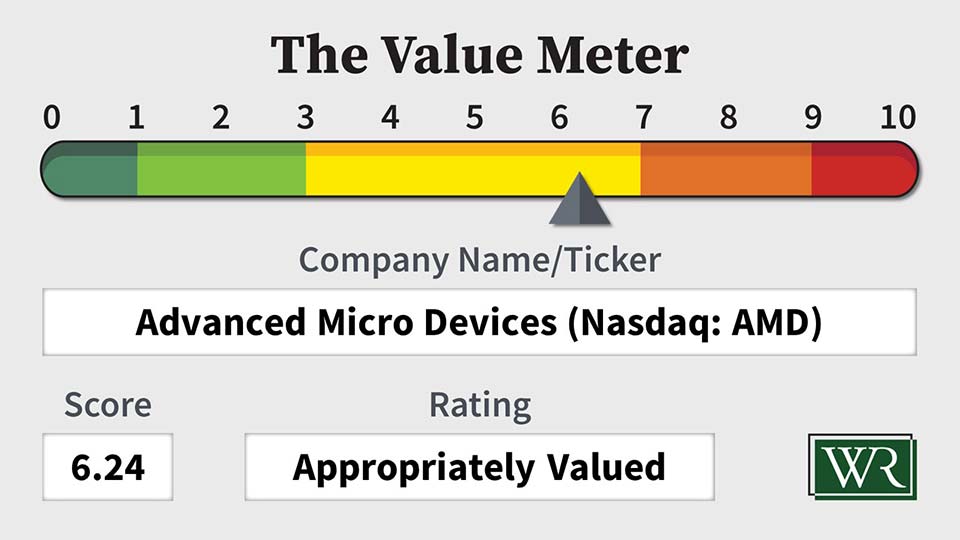

That, in fact, is the place our handy-dandy Worth Meter is available in.

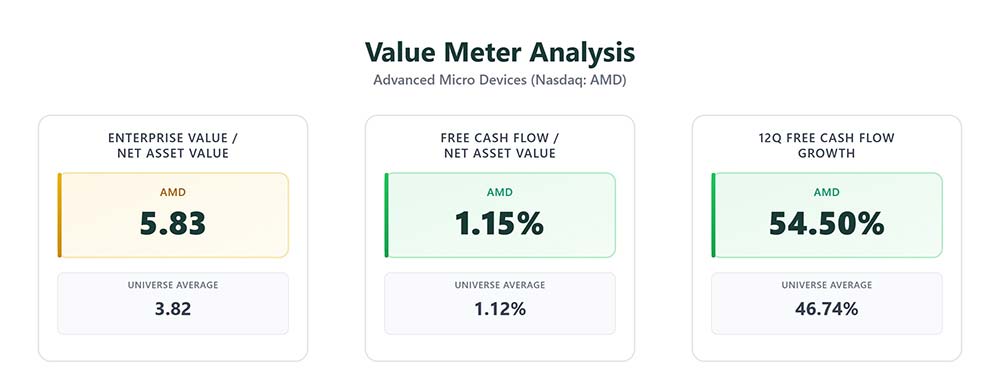

AMD’s enterprise value-to-net asset worth ratio sits at 5.83. The broader universe averages 3.82. This tells us traders are paying a premium for AMD’s property and its future. That premium could show justified – nevertheless it leaves little room for error.

On effectivity, AMD’s free money flow-to-net asset worth ratio is 1.15%, solely barely above the 1.12% common. That’s fantastic. It’s not distinctive.

The place AMD does stand out is consistency. Over the previous three years, it’s grown its quarterly free money movement 54.5% of the time, nicely forward of friends. Execution has been regular. The momentum is actual.

Briefly, AMD has robust progress and stable money era… however a valuation that already assumes each will proceed.

The inventory’s latest run reinforces the purpose. A lot of the upside got here shortly, pushed by shifting expectations, not uncared for worth. Early consumers have been paid. New consumers are paying consideration – and paying up.

For long-term holders, endurance nonetheless is sensible. The enterprise is powerful, and the technique is undamaged.

For brand new capital, self-discipline issues. The margin of security is skinny, and skinny margins have a tendency to indicate up after sharp rallies, not earlier than them.

The Worth Meter charges AMD as “Appropriately Valued.”

What inventory would you want me to run via The Worth Meter subsequent? Submit the ticker image(s) within the feedback part beneath.

[ad_2]