[ad_1]

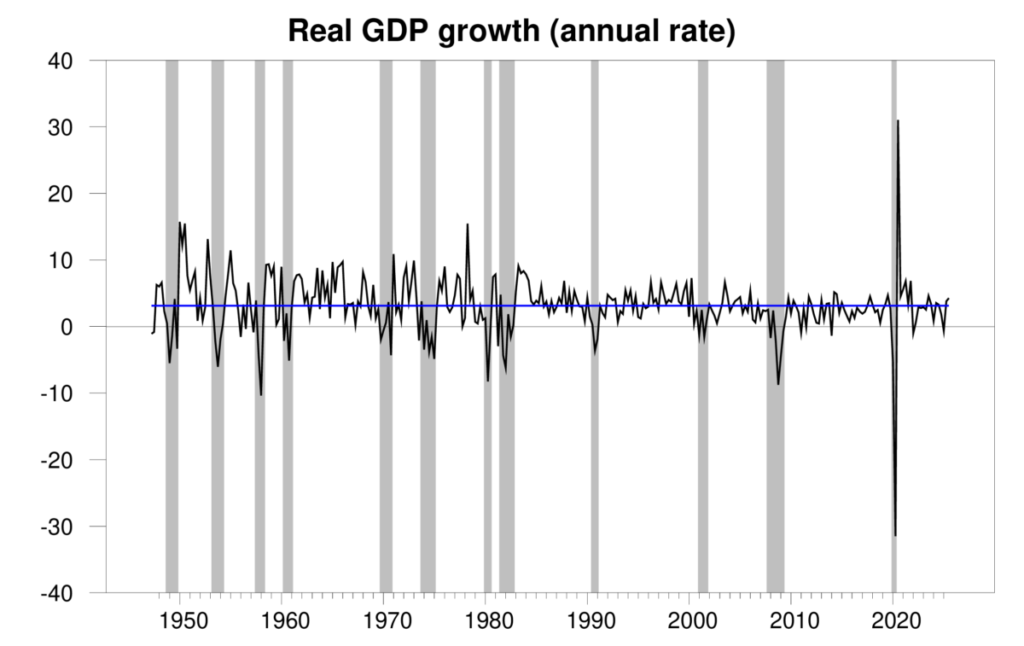

The Bureau of Financial Evaluation introduced right this moment that seasonally adjusted U.S. actual GDP grew at a 4.3% annual fee within the third quarter. That’s considerably larger than each the historic common progress and the worth anticipated by many forecasters.

Quarterly actual GDP progress at an annual fee, 1947:Q2-2025:Q3, with the historic common since 1947 (3.1%) in blue. Calculated as 400 instances the distinction within the pure log of actual GDP from the earlier quarter.

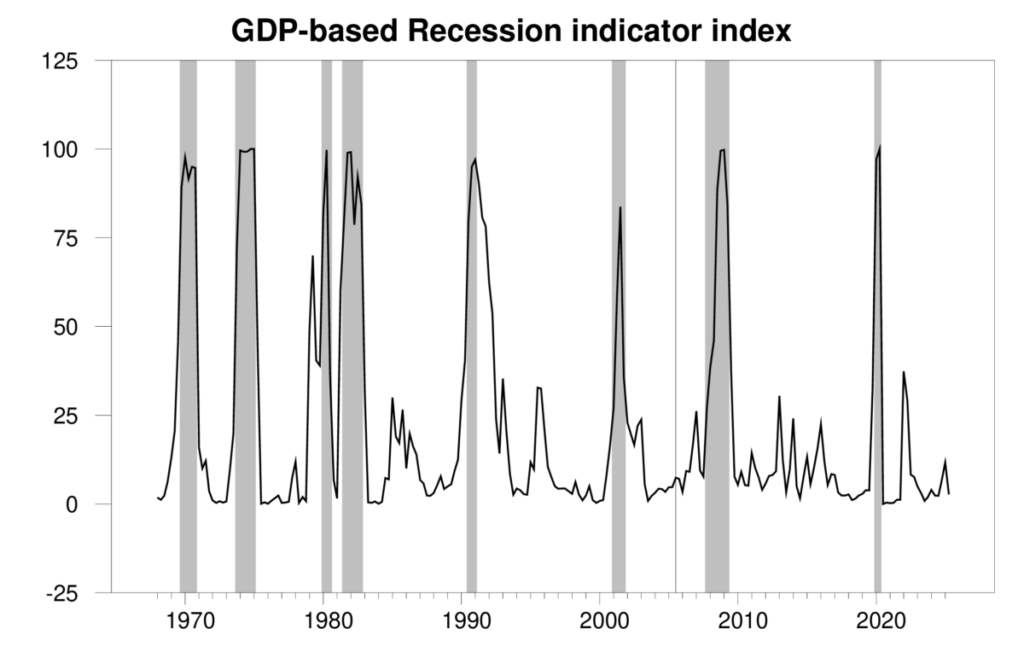

The brand new numbers deliver the Econbrowser recession indicator index all the way down to 2.7%, a traditionally very favorable degree. One of many targets of this index is to offer a purely goal abstract of the info utilizing an algorithm that has been publicly used now for many years. The most recent numbers put to relaxation the priority {that a} recession may need began earlier this yr.

GDP-based recession indicator index. The plotted worth for every date relies solely on the GDP numbers that had been publicly obtainable as of 1 quarter after the indicated date, with 2025:Q2 the final date proven on the graph. Shaded areas characterize the NBER’s dates for recessions, which dates weren’t utilized in any method in setting up the index.

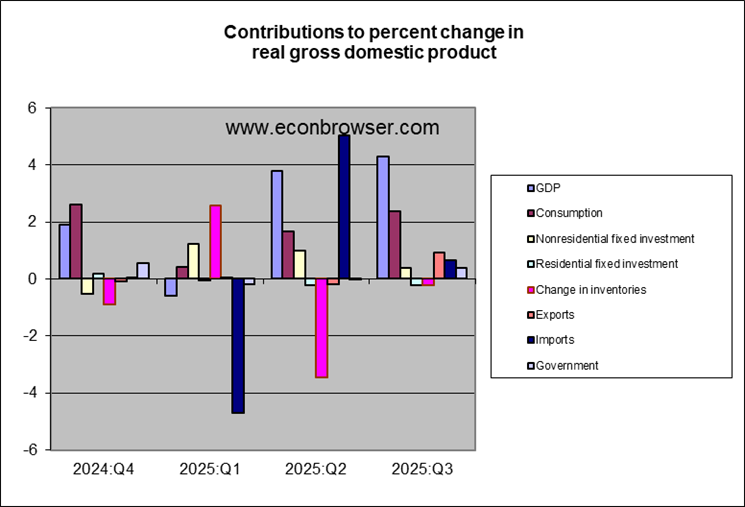

The small print behind the GDP numbers are additionally encouraging. Web exports and nonresidential mounted funding supplied a small increase to offset the persevering with weak housing market.

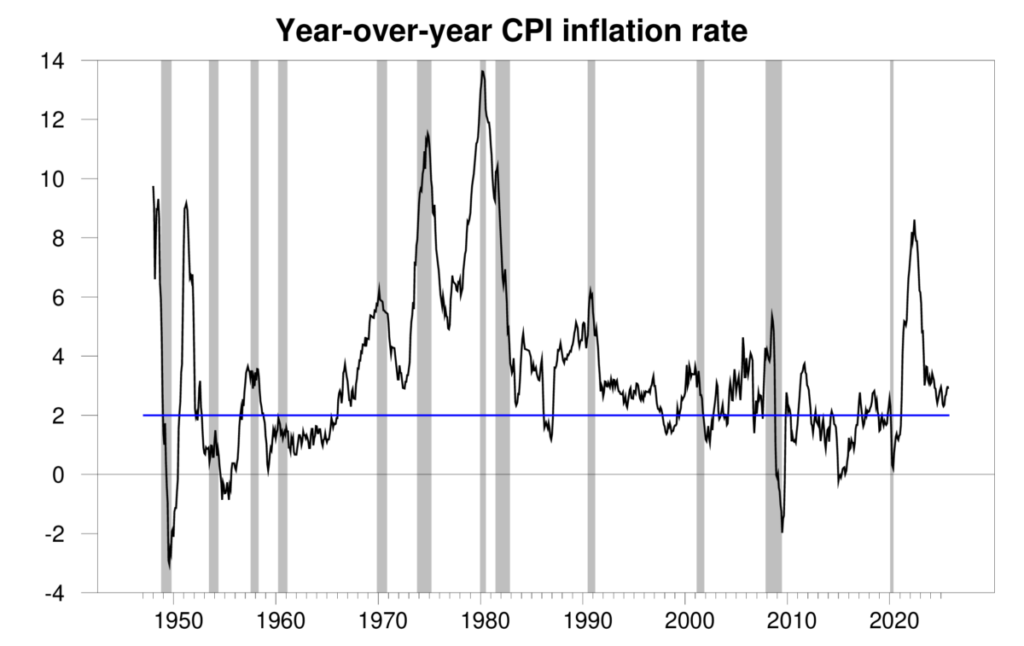

In line with the CPI, inflation hasn’t been trying that unhealthy both.

100 instances the year-over-year change within the pure logarithm of the month-to-month CPI.

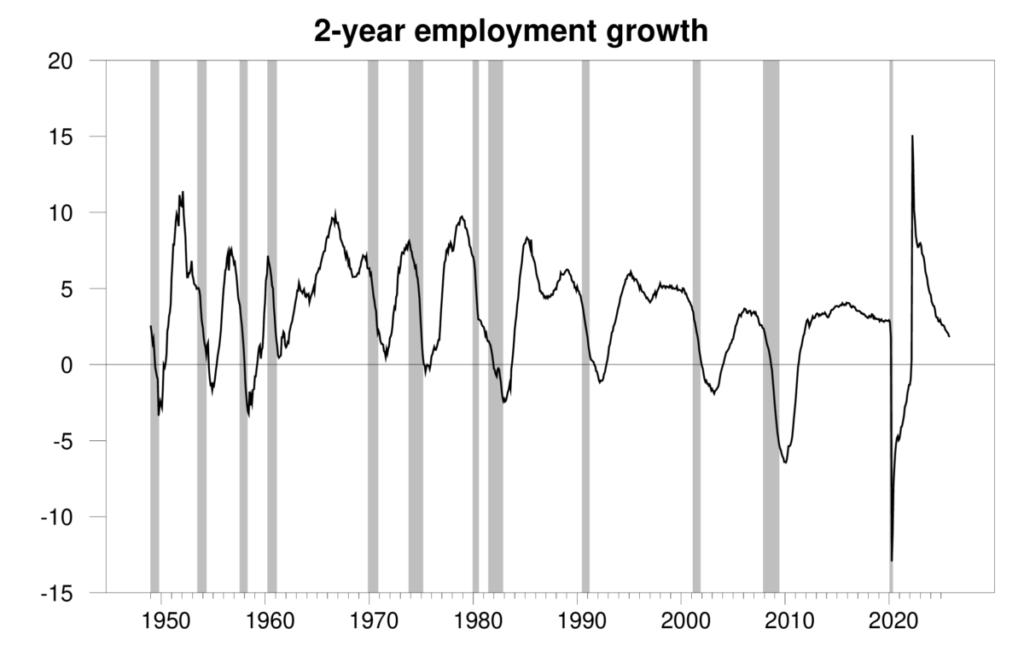

Then again, a number of indicators level to a weaker labor market. The 2-year progress fee of the variety of individuals working has positively slowed down. I have instructed {that a} slowdown like this will likely typically be an early indication {that a} recession is about to start. However the present crackdown on overseas employees makes this measure tougher to interpret than traditional.

100 instances the two-year change within the pure logarithm of month-to-month seasonally adjusted nonfarm payrolls, Jan 1949 to Dec 2025.

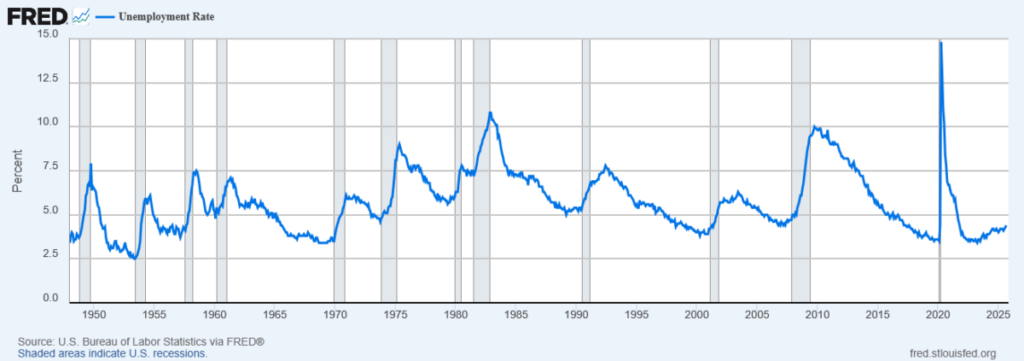

The unemployment fee ticked as much as 4.6% in November. That’s nonetheless nicely beneath the historic common degree of unemployment. However, Corridor and Kudlyak argued that it’s uncommon for the unemployment fee to be drifting up when the financial system continues to be rising, because it seems just lately to have been doing.

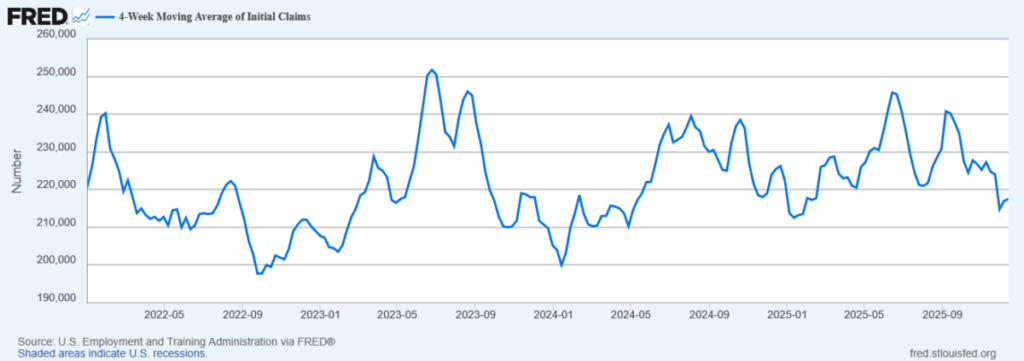

I regard preliminary claims for unemployment compensation as the only most dependable indicator of whether or not the labor state of affairs has taken a pointy flip for the more severe. Not everybody who’s unemployed is eligible to obtain compensation, and never everybody who’s eligible applies for it. So when individuals apply, it offers a ground-level indication that they anticipate private challenges forward. In line with this indicator, the labor market continues to be strong.

4-week common of preliminary claims, Jan 1, 2022 to Dec 13, 2025.

[ad_2]