[ad_1]

Coverage Middle for the New South

In 2010, once I was one of many vice presidents on the World Financial institution, colleagues I and revealed a really upbeat ebook about the potential of rising and growing economies changing superior international locations as engines of worldwide financial development. Whereas the latter can be grappling with the aftermath of the worldwide monetary disaster, the previous, already rising at a sooner tempo within the earlier decade and accounting for greater than half of the annual will increase in international GDP, had largely proven an urge for food for finishing up structural reforms wanted to converge with the richest.

Within the years that adopted, I used to be pressured to mood that optimism. The exuberant Chinese language development had been basic for the dynamism of different non-developed international locations, and the Chinese language route had change into one in every of decrease pace. Moreover, the financial rise of most of the huge rising markets had given rise to a sure conceitedness and complacency about persevering with to reform – this is applicable nicely to Brazil, Russia, South Africa, Turkey, and lots of others.

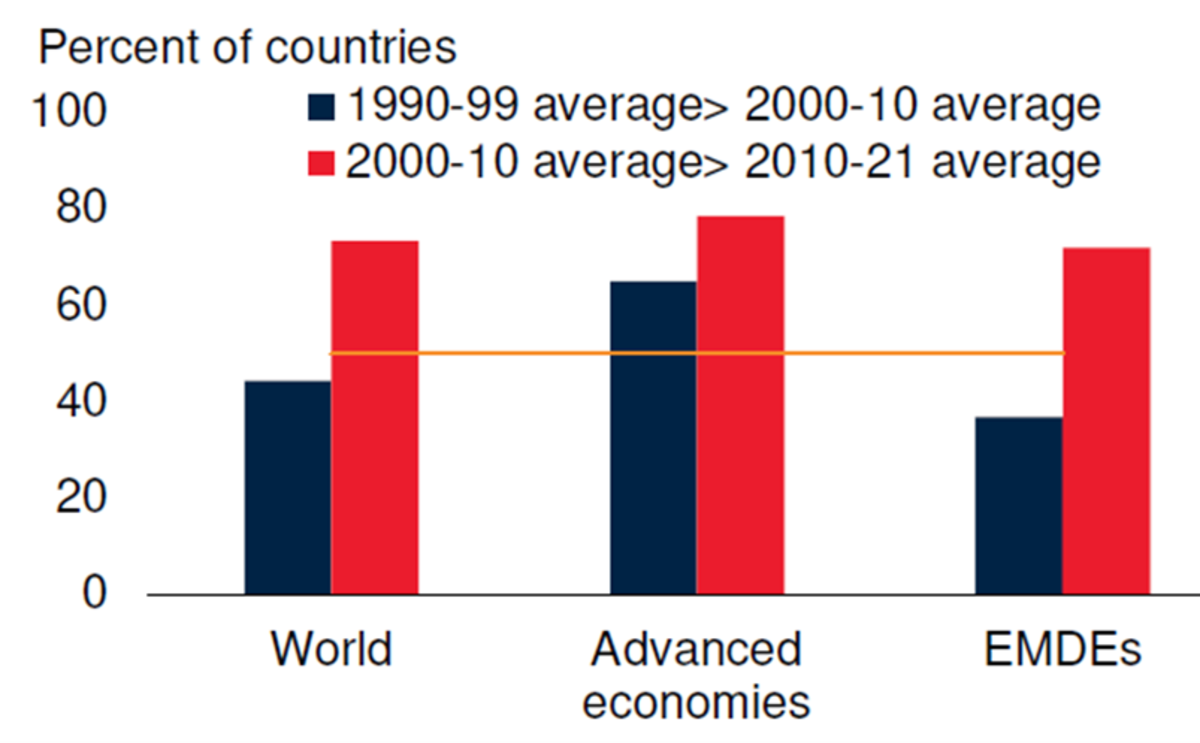

The low development of the richer economies ended up dragging down the efficiency of the others. The slowdown was widespread: in 80% of superior economies and 75% of rising and growing economies, common annual development was decrease in 2011-21 than in 2000-10 (Determine 1)

Determine 1 – Share of nations with slower development than within the earlier decade

Final week the World Financial institution launched a examine – Falling Lengthy-Time period Development Prospects – projecting a discount within the pace restrict at which the worldwide economic system can develop over the rest of this decade. The financial components which have propelled prosperity over the previous three a long time are reportedly shedding their grip.

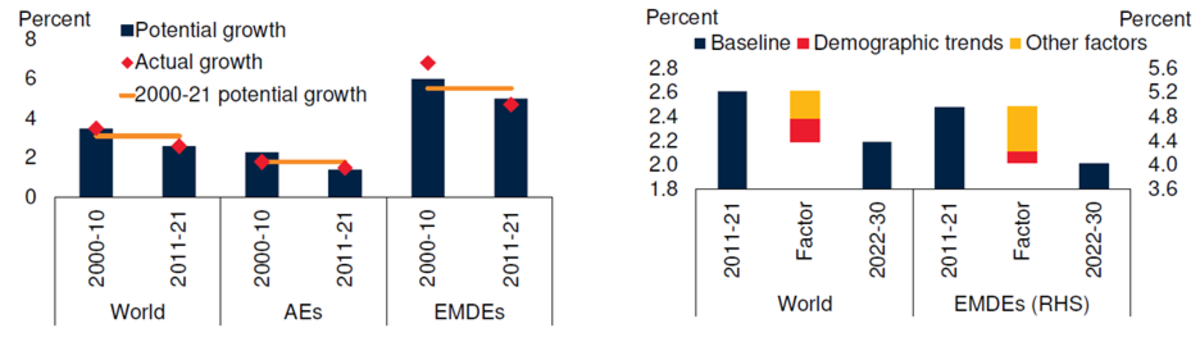

Between 2022 and 2030, the report initiatives a lower to 2.2% per 12 months in common potential international GDP development – that’s, with out triggering inflation – which corresponds to a couple of charge a 3rd decrease than that prevailing. within the first decade of this century. The autumn on the facet of growing economies, together with China, can be equally sharp: from 6% per 12 months between 2000 and 2010 to 4% per 12 months for the rest of this decade (Determine 2).

Determine 2 – Potential Development

It isn’t only a query of the results of the sequence of shocks to the worldwide economic system over the past three years, such because the pandemic, the invasion of Ukraine, the better frequency and depth of adversarial climate phenomena, and the acceleration of inflation. The sharp rise in inflation over the previous two years has led to the tightest international financial coverage tightening in 4 a long time.

Fiscal coverage additionally turned much less supportive following the numerous deterioration in public funds balances in the course of the 2020 international recession, when debt ranges reached historic highs. Amidst these a number of adversarial shocks, within the final three years, the worldwide economic system has skilled the most important development slowdown following a world recession. The image might worsen if the continuing financial tightening unfolds into monetary crises, which are typically digested with decrease subsequent financial development.

Nonetheless, all the basic components of GDP development have already been slowing down within the final decade. China has been transferring in direction of a slower tempo of financial growth. However essentially, enhancements in human capital, labor drive development, funding (together with due to political uncertainty) and complete issue productiveness (together with by way of the reallocation of manufacturing components throughout sectors) have slowed their tempo, as proven by the World Financial institution report. These development engines are anticipated to proceed shedding steam for the rest of the last decade.

The getting older and gradual development of the worldwide workforce are highlighted as downward components, explaining half of the anticipated slowdown in potential GDP development by way of 2030 (Determine 2). Decrease ranges of participation within the labor drive, as societies age, may have fiscal penalties through social safety, as well as, in fact, to decrease common productiveness per inhabitant.

Moreover, worldwide commerce development is way weaker now than within the early 2000s. The prospect of “deglobalization”, even when partial and relative, tends to convey increased prices than the positive aspects realized in globalization.

What ought to international locations do within the face of this prospect of a “misplaced decade”? Above all, adhere to macroeconomic and monetary insurance policies that mitigate the ups and downs of financial cycles: controlling inflation, guaranteeing the soundness of the monetary sector, lowering very excessive debt ranges, and restoring fiscal prudence. Such insurance policies may help international locations appeal to funding by bolstering investor confidence in nationwide establishments and home policymaking.

This should be completed constantly with elevated funding in areas akin to transport and power, climate-smart agriculture, and manufacturing, in addition to land and water programs. The report estimates that sound investments aligned with key local weather targets can enhance potential development by as much as 0.3 share factors per 12 months and strengthen the longer term resilience to pure disasters.

Lowering nonetheless excessive and pointless commerce prices stays an necessary merchandise on the agenda. Nations with the very best transport and logistics prices might minimize their buying and selling prices in half by adopting commerce facilitation and different practices from international locations the place such prices are low. Commerce prices, furthermore, could be lowered in a climate-friendly approach by eradicating the biases that exist in favor of carbon-intensive items in tariff partitions of many international locations and by eradicating restrictions on entry to inexperienced items and companies.

Exploring the service sector as a brand new engine of financial development additionally applies. To offer you an thought, in response to the report, digitally delivered skilled companies exports have risen to over 50% of complete service exports in 2021, up from 40% in 2019. Higher service supply can also be a supply of considerable productiveness positive aspects.

Lastly, there’s what could be completed to boost labor drive participation charges. The report highlights how, in some areas, akin to South Asia, he Center East, and North Africa, a rise in feminine workforce participation charges for the common of all rising markets and growing economies might speed up their potential GDP development of as much as 1.2 share factors per 12 months between 2022 and 2030. The case of Morocco has been lately approached right here.

One final name is the toughest to acquire: restoring the worldwide financial integration that has been instrumental in leveraging international prosperity for over 20 years for the reason that Nineteen Nineties!

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Middle for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Growth. He’s a former vice chairman and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund, and a former vice chairman on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil.

[ad_2]