[ad_1]

A triple structural change within the macroeconomic coverage regime in superior economies has taken place within the final two years, as in comparison with the post-global monetary disaster interval.

First, a persistent insufficiency of combination demand, recognized as a development deterrent prevailing after the 2008 international monetary disaster, has been outmoded by extra frequent and important supply-side shocks and better inflation. Some imagine that the period of ultra-low rates of interest and low inflation is certainly gone, whereas others declare that such change is non permanent and reversable.

Consequently, the period of ample and low cost liquidity supplied by central banks gave solution to greater rates of interest and liquidity squeezes in 2022. Quantitative tightening and better primary rates of interest by central banks turned the brand new norm, as a type of ‘normalization’ of financial insurance policies.

Lastly, due to the earlier modifications, there was a powerful devaluation of monetary property in 2022. There are actually fears about a number of prospects forward for monetary shocks.

1. From Insufficiency of Demand to Blockages on the Provide Aspect

Beginning in 2021, inflation within the U.S. and in Europe rose to the very best ranges in many years. U.S. client costs doubtless rose by about 7% in 2022, the very best in 4 many years. In Germany, 2022 ended with an inflation charge of 9.6% per 12 months, very near the primary expertise of double-digit inflation since 1951.

The surge is defined by succession of provide and worth shocks (pandemic, struggle in Ukraine), whereas a strong restoration of post-pandemic demand was going down. Now, rising rates of interest are threatening to push the worldwide financial system into recession in 2023 (Canuto, 2022a).

Many analysts initially interpreted the inflation as ‘transitory’, a consequence of supply-side shocks that may be non permanent and quicky reversible. Such a view has been changed by one other that acknowledges some position performed by extra demand relative to provide capability over an extended time interval, which known as for restrictive central financial institution insurance policies to curtail demand. Now doubts are rising about how excessive and for a way lengthy greater rates of interest must go to melt labor markets, and prevail over the resistance in providers inflation (Canuto, 2022b).

Are these signs of a enterprise cycle like others? Or has some structural change occurred which will lead one to conclude that the period of low inflation and low rates of interest is gone?

Within the years following the 2008-09 international monetary disaster, sluggish financial development was attributed to a persistent insufficiency of combination demand. A number of hypotheses had been established a couple of potential development of secular stagnation current in superior economies: hangovers from the monetary disaster, earnings focus, the exhaustion of the technological waves of earlier many years, demographic dynamics, and others (Canuto, 2021a).

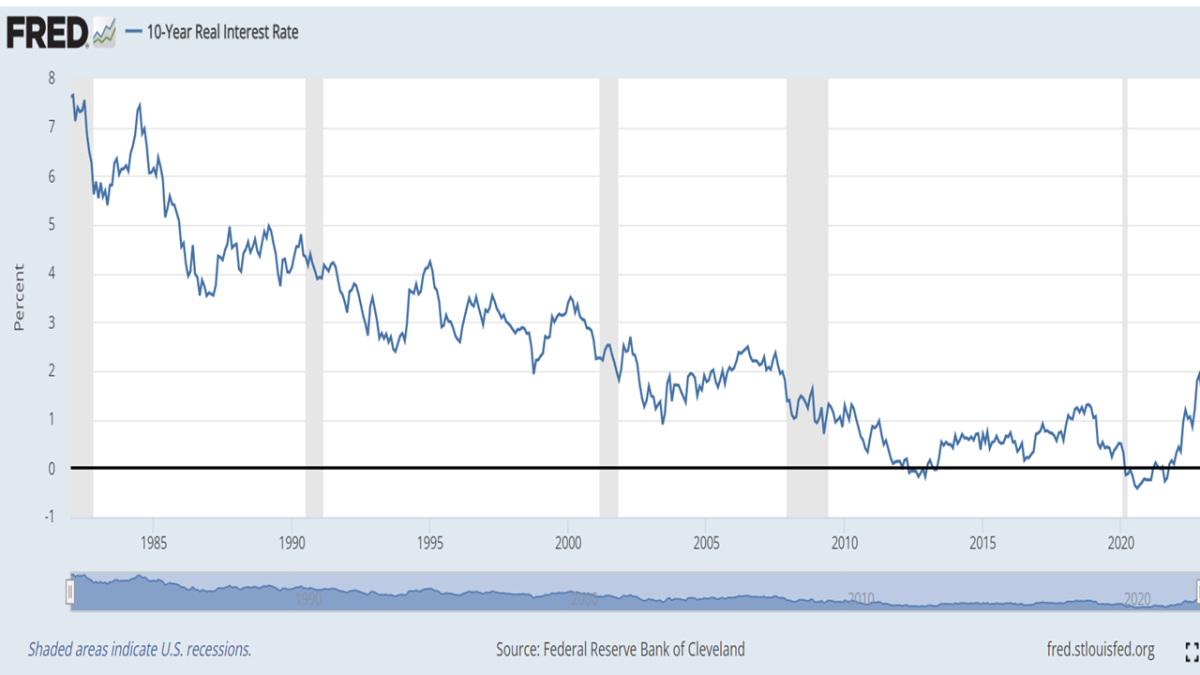

The lengthy interval of low rates of interest (Determine 1), accompanied by a flood of liquidity from central banks by means of their quantitative easing applications (purchases of presidency bonds, mortgages, and, within the euro space, personal property) after the 2008-09 international monetary disaster, offset the comparatively low use of expansive fiscal insurance policies. Alternatively, the fiscal coverage sign modified considerably with the emergency help distributed by governments to households and firms in the course of the pandemic.

Determine 1: U.S. 10-12 months Treasury Actual Curiosity Price

A number of shocks began to position provide as an alternative of demand as a problem. Along with the interruptions in worth chains in the course of the pandemic, there was a decline of labor-market participation, particularly in the USA (‘The Nice Resignation’). Sure segments of the inhabitants have left the labor pressure at unusually excessive charges, both by alternative or necessity, making it more durable for firms to search out employees. This subject has been compounded by disruptions in international labor flows, as fewer overseas employees have obtained visas or are prepared emigrate.

Moreover, Russia’s invasion of Ukraine in February 2022 triggered meals and vitality provide and worth shocks. Moreover, governments intensified their weaponization of commerce, funding, and fee sanctions—a response to Russia’s invasion of Ukraine and worsening tensions between the USA and China.

Such modifications have accelerated the post-pandemic rewiring of some international provide chains with the intention to goal for extra ‘friend-shoring’ and ‘near-shoring’. The notion of geopolitical dangers and the larger frequency of hostile climate phenomena are main firms to pursue resilience even on the detriment of value effectivity. It isn’t clear but how far and large that transfer can be however, relying on the extent to which it happens, much less quantity-responsive and extra price-responsive provide chains may are likely to grow to be the norm (Canuto et al, 2022).

The essential vitality transition can also be intrinsically inflationary (Canuto, 2021b). So, modifications within the scope of globalization, labor shortages, and the results of local weather change have elevated provide challenges and put into query the idea on the continuity of an period of low ranges of inflation and rates of interest.

Wanting forward:

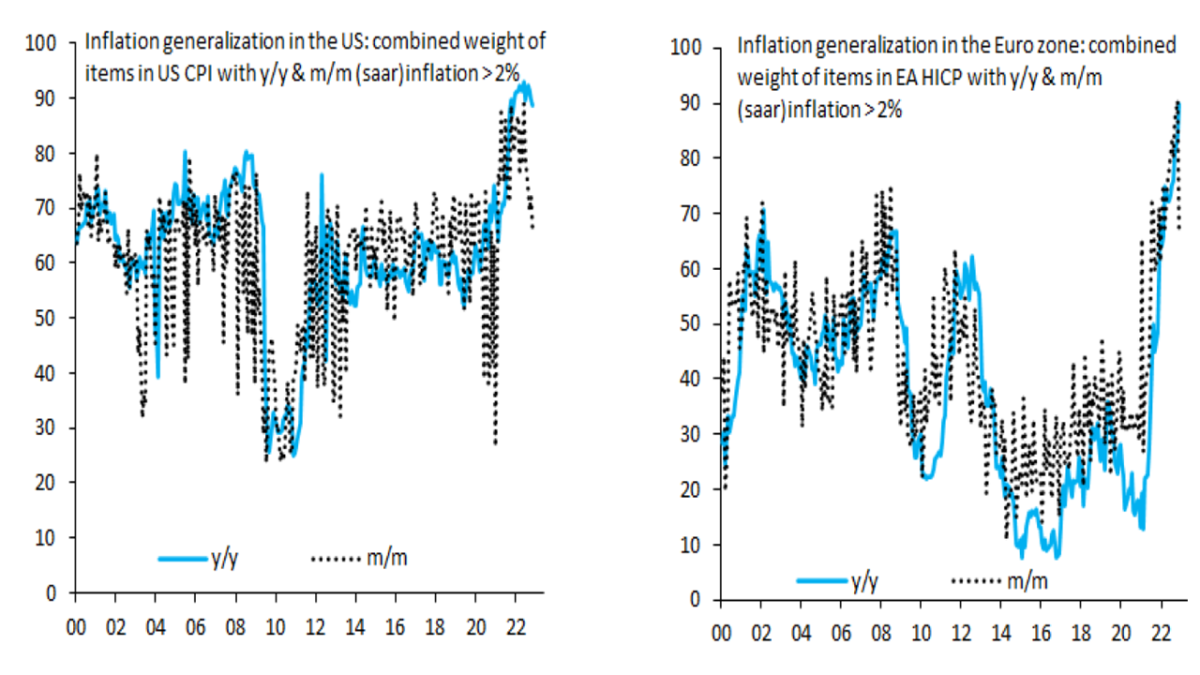

(a) Inflation charges appear to have peaked within the U.S. and Europe (Determine 2). However the tightness of labor markets and the downward resilience of core inflation in providers are potential dampening components enjoying in opposition to a quick and important transfer downward of inflation (Canuto, 2022b).

Determine 2: Much less Generalized Inflation within the U.S. and Europe

Supply: Brooks et al (2022).

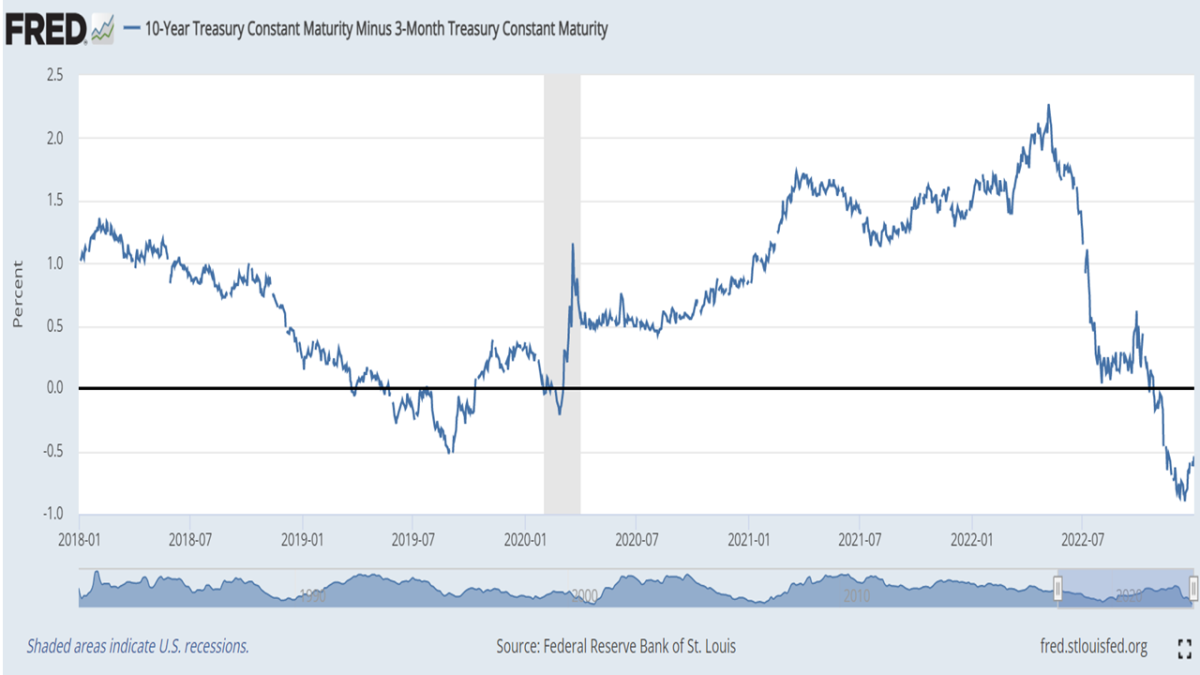

(b) Delicate or exhausting recessions loom forward on each side of the Atlantic. The inversion of the U.S. yield curve (Determine 3) suggests this to be the case.

Determine 3: 10-12 months Treasury Fixed Maturity Minus 3-Month Treasury Fixed Maturity

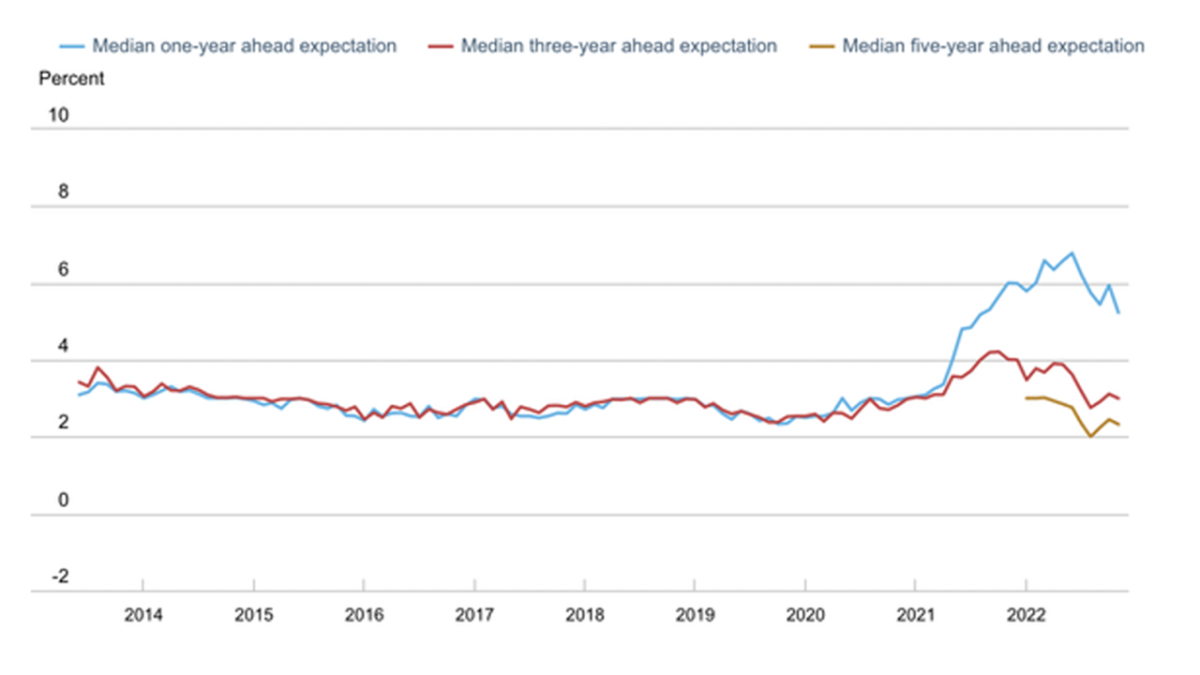

One might discover that inflation is anticipated to stay excessive in 2023. However anticipated medium-term inflation stays low, which can be interpreted as an indication of inflation thus far not changing into entrenched (Determine 4).

Determine 4: U.S. Inflation Expectations

Supply: Federal Reserve Financial institution of New York, Survey of Client Expectations.

A divergence of views in regards to the longevity of the regime change with respect to provide and demand follows. As an illustration, Goodhart and Pradhan (2020) argued that demographic dynamics and a retreat from globalization imply greater inflation and better rates of interest over the long run. In distinction, Blanchard (2022) believes that the components which have led to low actual rates of interest on secure property will return, as soon as the present inflationary shock is over.

The frequency and depth with which (relative) deglobalization, geopolitical occasions, and local weather change carry new shocks will decide whether or not the 2021/2022 reconfiguration of demand-supply interplay will persist. Or whether or not U.S. and Europe return to the trail on which a mismatch between wealth and creation of recent property tends to guide rates of interest once more to low ranges—as argued by Canuto (2021a), a view nearer to Blanchard’s. No matter that, occasions in 2021 and 2022 have already triggered different coverage regime modifications.

2. The Finish of Boundless Liquidity from Central Banks

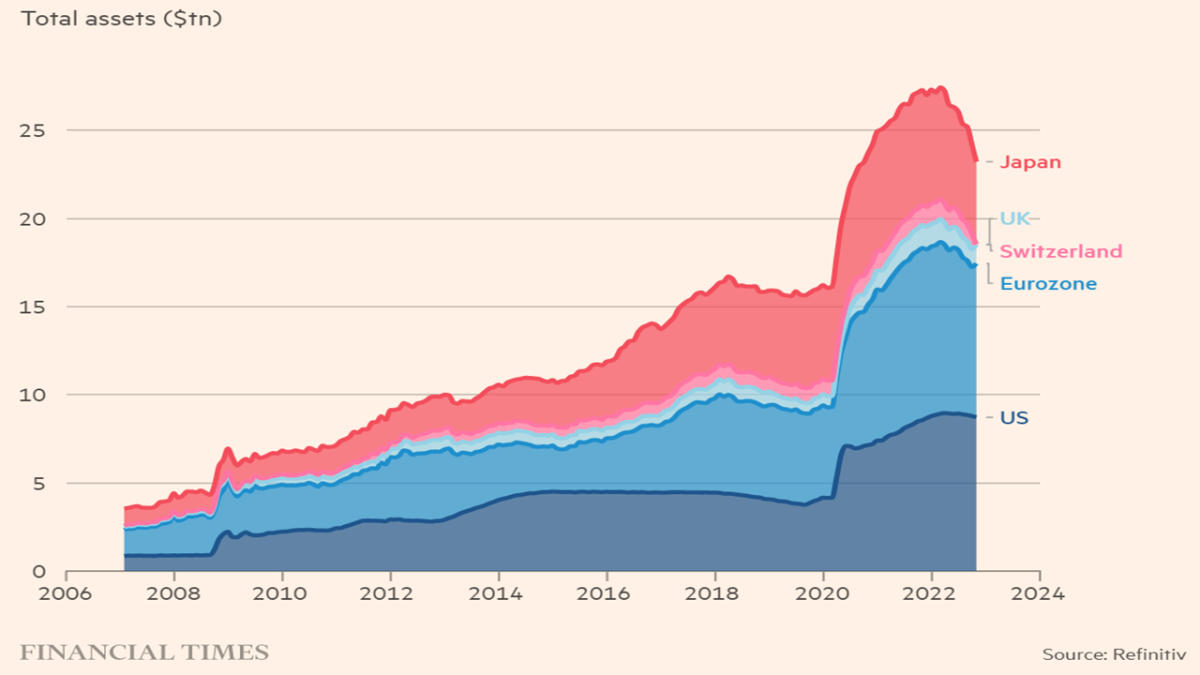

The inflation ensuing from the change within the match between provide and demand explains a second profound change: the tip of the period of limitless liquidity supplied by central banks. For years, central banks in main economies responded to just about any signal of financial weak spot or monetary market volatility by placing more cash in. Throughout the pandemic, central-bank steadiness sheets made enormous extra jumps relative to the development because the international monetary disaster (Determine 5).

Determine 5: Central Financial institution Steadiness Sheets

However as central banks prolonged what had been imagined to be time-limited interventions, some collateral injury was inflicted. Liquidity-laden monetary markets turned dissociated from the actual financial system (Canuto, 2020). As well as, they turned ‘spoiled’, beginning to exhibit ‘tantrums’, with adverse reactions, even to mere indications of discount in central financial institution help (Canuto, 2022c).

It was like this within the U.S. ‘taper tantrum’ in 2013, when the chairman of the Fed on the time, Ben Bernanke, introduced that the establishment would begin planning the tip of quantitative easing, and ended up reversing this course six weeks later. It additionally occurred within the fourth quarter of 2018, when Jeremy Powell, then Fed chairman, needed to make a really embarrassing about-turn from his delicate ‘quantitative tightening’ as a result of the markets received so uneven.

All that modified with rising inflation within the U.S. and Europe. The prognosis of inflation as ‘transient’ gave solution to guarantees of ‘quantitative tightening’ in earnest, and of raised rates of interest. Strictly talking, the Fed continued to inject liquidity into the financial system till March 2022, steadily shrinking its steadiness sheet beginning in June.

It additionally lastly started to boost coverage charges modestly, then switched to a sequence of steeper hikes, together with a document 4 successive hikes of 0.75 proportion factors between June and November 2022, and ending the 12 months with one other 0.50 proportion factors. It ought to elevate the bottom charge by 0.25 proportion factors two or three extra instances within the first few months of 2023, and go away it there for some time.

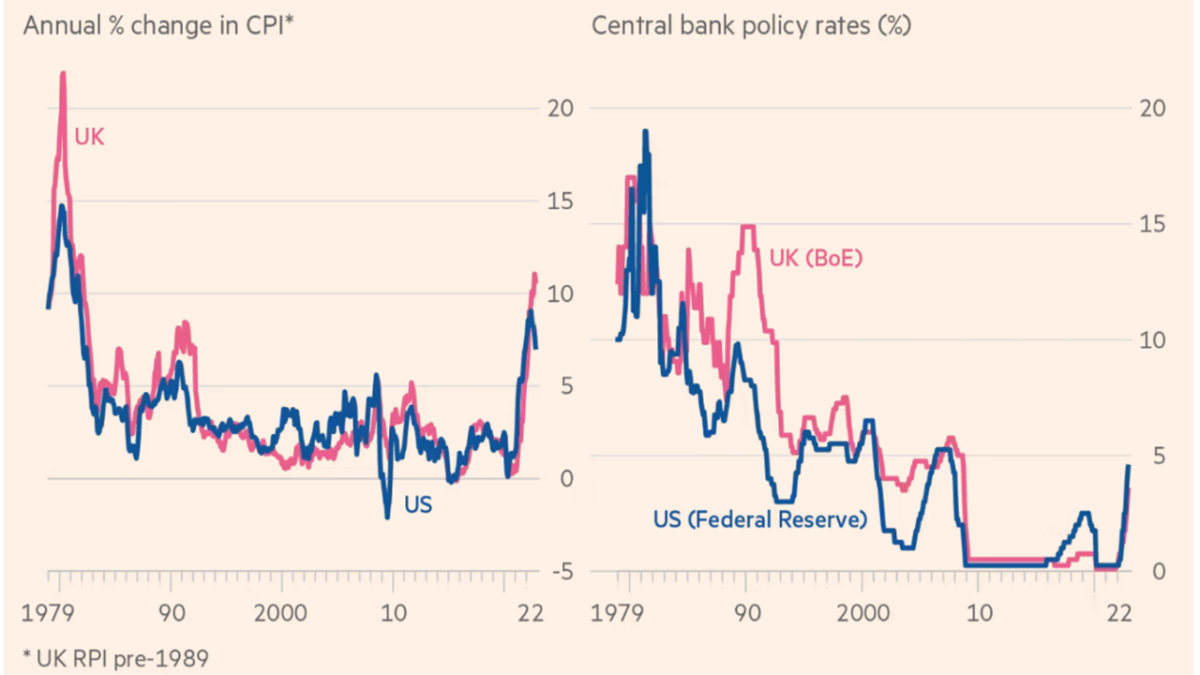

U.S. low inflation and ultra- low rates of interest have been changed—for nevertheless lengthy a time interval—with greater inflation and rates of interest (Determine 6). The European Central Financial institution is transferring in the identical course, although with much less depth.

Determine 6: U.S. CPI inflation and Fed Coverage Charges

Supply: Keith Fray, Steven Bernard, Matthew Brayman and Justine Williams (2022). Struggle, inflation and tumbling markets: the 12 months in 11 charts, Monetary Occasions, December 29.

3. Looming Fragility of Monetary Markets

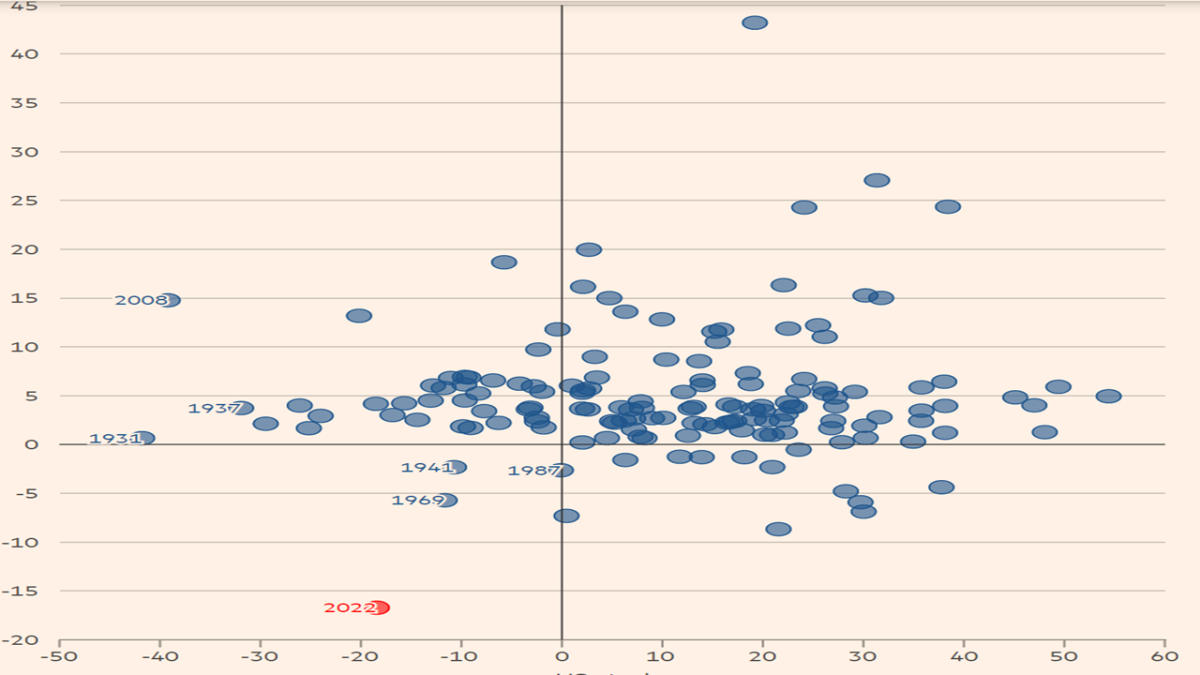

The 2 earlier coverage regime modifications have led to a 3rd: a looming fragility in monetary markets. 2022 was a 12 months of fairness and fixed-income devaluation: the monetary 12 months ended with losses of greater than $30 trillion in equities and fixed-income bonds. Determine 7 exhibits how adverse a 12 months 2022 was for traders, in each shares and bonds. The macroeconomic slowdown in 2023 is more likely to additionally result in decrease total asset yields, particularly from shares.

Determine 7: Whole Nominal Return in U.S. Shares and Bonds, 1871 to 2022 (%)

Supply: Keith Fray, Steven Bernard, Matthew Brayman and Justine Williams (2022). Struggle, inflation and tumbling markets: the 12 months in 11 charts, Monetary Occasions, December 29.

Company debt elevated within the years of low rates of interest and ample liquidity. Though analysts recommend that there is no such thing as a generalized vulnerability by way of mismatches of charges between property and liabilities, it’s acknowledged that there are a number of factors at which some sudden disappearance of liquidity may result in dramatic changes and insolvencies.

OECD (2022) highlighted main monetary market developments, spillovers to credit score danger, and rising vulnerabilities in a number of market segments, as a mirrored image of tighter financial situations, slower international development, greater inflation, and geopolitical tensions. Allow us to focus right here on a peculiar supply of dangers that has acquired prominence within the latest previous.

A metamorphosis in monetary flows passed off in the course of the period of simple cash, with a big a part of international monetary exercise shifting after the worldwide monetary disaster from highly-regulated banks to much less regulated and constrained entities, together with asset managers, personal fairness funds, and hedge funds. Non-bank monetary establishments changed banks in monetary intermediation, and a morphing and migration of danger passed off (Canuto, 2021c).

The 2008 monetary disaster was finally in regards to the banking system and in regards to the funds and settlement system. Excessive capital necessities had been established subsequently, limiting the varieties of actions that banks may take part in, and the banking system was de-risked. Alternatively, the newly distinguished intermediaries should not more likely to keep sturdy resilience in opposition to sudden and sharp modifications in the price of borrowing, or entry to finance.

The post-2008 disaster reforms, whereas focused at reinforcing monetary stability, might have, in some areas, merely changed counterparty danger with liquidity danger. Shocks on asset costs could also be propagated by intermediaries being obliged to shrink their holdings, exacerbating these shocks by way of transmission and contagion.

The displacement of counterparty danger into liquidity danger seems in a number of varieties. As an illustration:

(a) In U.S. Treasury markets, banks used to carry out a essential warehousing position, particularly within the short-term lending ‘repo’ market. Stricter capital guidelines have led them to maneuver to different, higher-margin enterprise traces, whereas different market individuals haven’t but appeared prepared to fill the void completely. As an alternative, when volatility rises, hedge funds and high-frequency merchants preserve a sure distance. Volatility rose dramatically in U.S. Treasury markets final 12 months in autumn, resulting from vanishing liquidity.

(b) The emphasis on collateral has additionally exacerbated instability by rising promoting stress. The UK gilt market meltdown in October 2022 is a first-rate instance: UK pension funds had purchased derivatives as a part of a method generally known as liability-driven investing. Then, after Liz Truss’s newly inaugurated authorities introduced a plan for large unfunded tax cuts, authorities bond yields soared, abruptly hitting a few of the nation’s extremely leveraged pension funds. When gilt costs fell sharply, they obtained margin calls requiring them to put up extra collateral, so that they offered gilts, additional driving down the worth, resulting in extra margin calls in a vicious circle. Have been it not for the emergency intervention of the Financial institution of England, the withdrawal of the Truss authorities’s proposal, and the federal government’s eventual downfall, the compelled sale of bonds by pension funds may have become a significant monetary disaster.

(c) One other type of dangers of illiquidity has probably risen lately as traders seeking greater returns have moved past financial institution accounts, shares, and bonds. In instances of market stress, funds centered on actual property, personal credit score, and others have been hit by extra redemption requests than they’ll simply deal with.

(d) BIS (2022) examined how poor liquidity situations throughout market segments have stored asset worth volatility elevated, and have contributed to swings in international monetary situations. The report focuses consideration on indicators of fragility within the markets for company mortgage-backed securities (MBS), dedicating a field to the danger of liquidity disruptions.

There are additionally non-transparent off-balance sheet dangers in each the financial institution and non-bank monetary sectors. The BIS Quarterly Assessment of December additionally contained a chapter by Claudio Borio, Robert N McCauley, and Patrick McGuire on “enormous, lacking and rising” greenback debt in overseas trade swaps, forwards, and foreign money swaps.

The fragility of the monetary system has implications for the work of central banks. As an alternative of dealing with solely their primary dilemma—decreasing inflation, or sustaining financial development and employment—they now face a trilemma: decreasing inflation, sustaining development and jobs, or guaranteeing monetary stability. As development slows, financial tightening is extended, and illiquidity bouts exacerbate monetary fragility, central banks could be compelled to attempt to reconcile their quantitative tightening and rate of interest hikes with interventions to supply liquidity at key factors of the system. Some type of mixture of QT and centered quantitative easing …

—————

Regardless of the period of the brand new coverage regime could also be, we’re not in Kansas with respect to provide versus demand, financial coverage, and monetary stability.

References

BIS (2022). BIS Quarterly Assessment, December 2022.

Blanchard, O. (2022). Past the present struggle in opposition to inflation: Fiscal coverage beneath low charges, PIIE – Peterson Institute for Worldwide Economics, December 1.

Brooks, R.; Fortun, J.; and Pingle, J. (2022). World Macro Views: Disinflation within the US and Euro Zone, Institute of Worldwide Finance,

Canuto, O. (2020). Dependency and disconnect of U.S. monetary markets, , September 22.

Canuto, O. (2021a). U.S. Bubble-Led Macroeconomics, Coverage Heart for the New South, PB-21/29, August.

Canuto, O. (2021b). Decarbonization and “Greenflation”, Coverage Heart for the New South PB-51/21, December.

Canuto, O. (2021c). The Metamorphosis of Finance and Capital Flows to Rising Market Economies, Coverage Heart for the New South PP-24-21, November.

Canuto, O. (2022a). Whither the Phillips Curve?, Coverage Heart for the New South PP – 17/22, October.

Canuto, O. (2022b). The Fed’s Give attention to the Labor Market, Heart for Macroeconomics and Improvement, December 8.

Canuto, O. (202c). Quantitative Tightening and Capital Flows to Rising Markets, Coverage Heart for the New South PB – 42/22, June.

Canuto, O.; Ali, A.A.; and Arbouch, M. (2022). Pandemic, Struggle, and World Worth Chains, Jean Monnet Atlantic Community 2.0., October.

Goodhart, C., and Pradhan, M. (2020). The Nice Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, Palgrave Macmillan, 2020.

OECD (2022), Deteriorating situations of worldwide monetary markets amid excessive debt, OECD Enterprise and Finance Coverage Papers, OECD Publishing, Paris, November.

[ad_2]