[ad_1]

In his presentation final Wednesday (November 30) on the Brookings Establishment, in Washington-DC, Jerome Powell, president of the Federal Reserve (Fed), signaled a smaller enhance within the US primary rate of interest as a choice for the subsequent FOMC assembly on December 14. Expectations now converge to a rise of solely 50 foundation factors this time, after 4 consecutive conferences with will increase of 75 foundation factors. From virtually zero in March of that yr, the essential fee would finish the yr within the vary between 4.25% and 4.5% each year.

Alternatively, Powell famous that inflation within the US stays excessive. He talked about an estimate that, within the 12 months as much as October, inflation in private client spending was at 6% per yr. Rates of interest should attain restrictive ranges sufficient to deliver inflation all the way down to 2% a yr. He talked about that there’s nonetheless extra floor to cowl by the Fed, what means that there might be some extra enhance of rates of interest in 2023.

Financial tightening is aimed toward slowing demand development relative to combination provide, he mentioned, which would require a sustained interval of below-trend US financial development. Regardless of the financial tightening and slower tempo of development this yr, he was nonetheless not seeing clear progress in curbing inflation.

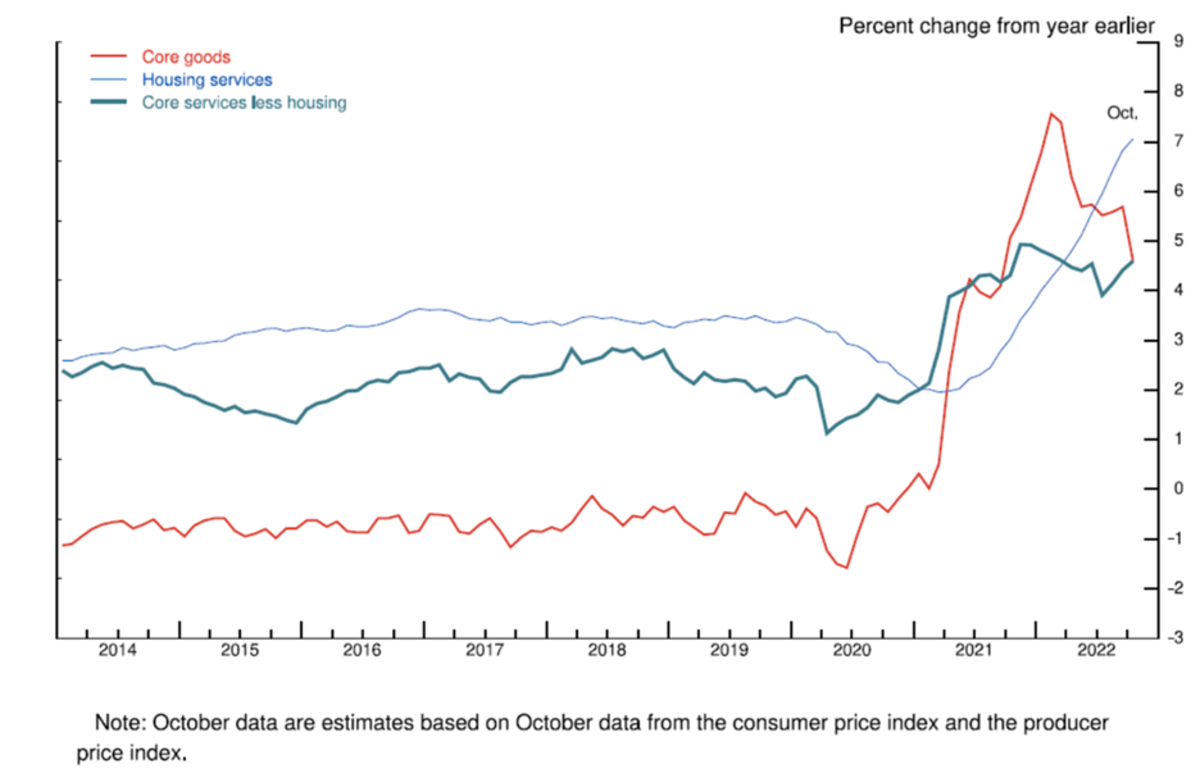

Powell’s presentation divided the main target between inflation and the job market. The motivation for this was evident when he addressed the three core parts of the inflation fee: items, housing, and companies aside from housing (Determine 1). Whereas the core inflation of products declined from excessive ranges all year long, housing companies continued to rise at a fee of seven.1% within the final 12 months. Powell famous, nevertheless, the substantial drop within the tempo of worth rise in new leases because the center of the yr.

Determine 1 – Elements of Core PCE Inflation

Powell highlighted the companies much less housing part, the most important one, making up greater than half of the core worth index. It contains schooling, well being companies, haircuts, hospitality and so forth. He attributed a really massive position to this part in projecting the evolution of the core of the index.

As salaries represent the primary value in these companies, it follows the significance of observing the labor market to investigate inflation on this class. In response to Powell, in the intervening time the demand for employees far exceeds the availability of obtainable labor, which has been accompanied by an increase in nominal wages effectively above what can be in step with 2% inflation over time. Due to this fact, a restoration of stability between provide and demand within the labor market can be a related merchandise to think about inflation to be contained.

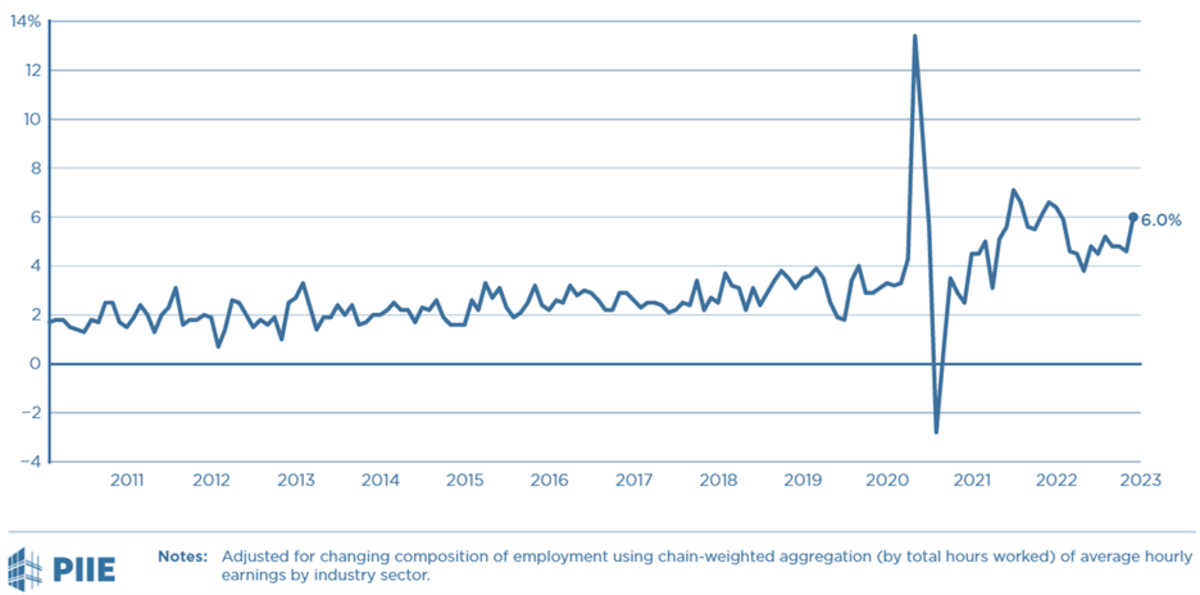

The report on non-farm payrolls – often called the “jobs report” – launched final Friday corroborated Powell’s factors in regards to the job market, displaying better-than-expected job creation and accelerating wage development. Regardless of slowing in November, U.S. jobs development beat expectations. Common wage beneficial properties registered an annualized enhance within the final three months above the one which occurred within the final twelve months (Determine 2).

Determine 2 – 3-month p.c change in common hourly earnings in all personal industries

The unemployment fee remained steady at 3.7%, however the labor drive participation fee fell barely from 62.2% to 62.1%, down from 63.4% in February 2020, earlier than the pandemic. The “nice resignation”, because the mass exit of employees from the labor market in the course of the pandemic grew to become recognized, has not been largely reversed.

Within the Brookings presentation, Powell talked about a “shortfall” of about 3.5 million individuals within the workforce in comparison with pre-pandemic developments. Greater than two million of these absent would correspond to an “extra of pensions” in relation to what might be anticipated as a consequence of an growing older inhabitants. Among the many causes for this, along with better concern for well being by older individuals and difficulties in adapting to modifications within the work surroundings, he cited beneficial properties in inventory markets and property values within the first two years of the pandemic as elements rising private wealth and facilitating early retirements. In regards to the remaining one and a half million employees absent from the supply, he cited the rise in deaths within the pandemic and the deep decline within the internet influx of immigrants.

He additionally mentioned that the Fed doesn’t have the instruments to extend the workforce, leaving it with devices that function on its demand to attain stability. With the opening of jobs being at a degree of 1.7 for every particular person in search of work, the compression in demand would nonetheless be comparatively distant.

Powell justified upfront the discount within the tempo of enhance within the primary rate of interest in December, mentioning the time lag between financial coverage choices and their results on the economic system, which is kind of unsure, and the truth that the fast and intense tightening to this point this yr has but to be felt. Nevertheless, he famous that what issues most is how a lot it nonetheless should rise and the size of time it ought to stay tight.

The stakes are break up between those that assume FOMC charges will go as much as 5% or extra earlier than a break. If the pause is untimely, there’s a threat of a future spike in inflation and a fair better tightening afterwards, as occurred within the Volcker period. If it passes the purpose, the macroeconomic slowdown and the rise within the unemployment fee might be accentuated.

Eyes will evidently even be turned to the monetary repercussions of rising rates of interest. On this regard, consideration is drawn to the truth that longer rates of interest – resembling these for 10-year Treasury bonds – are removed from reflecting the extent of the rise in primary rates of interest.

Nevertheless, it’s within the labor market that the Fed’s financial coverage script might be written. Judging by Powell’s presentation and given excellent fears of price-wage spirals.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]