[ad_1]

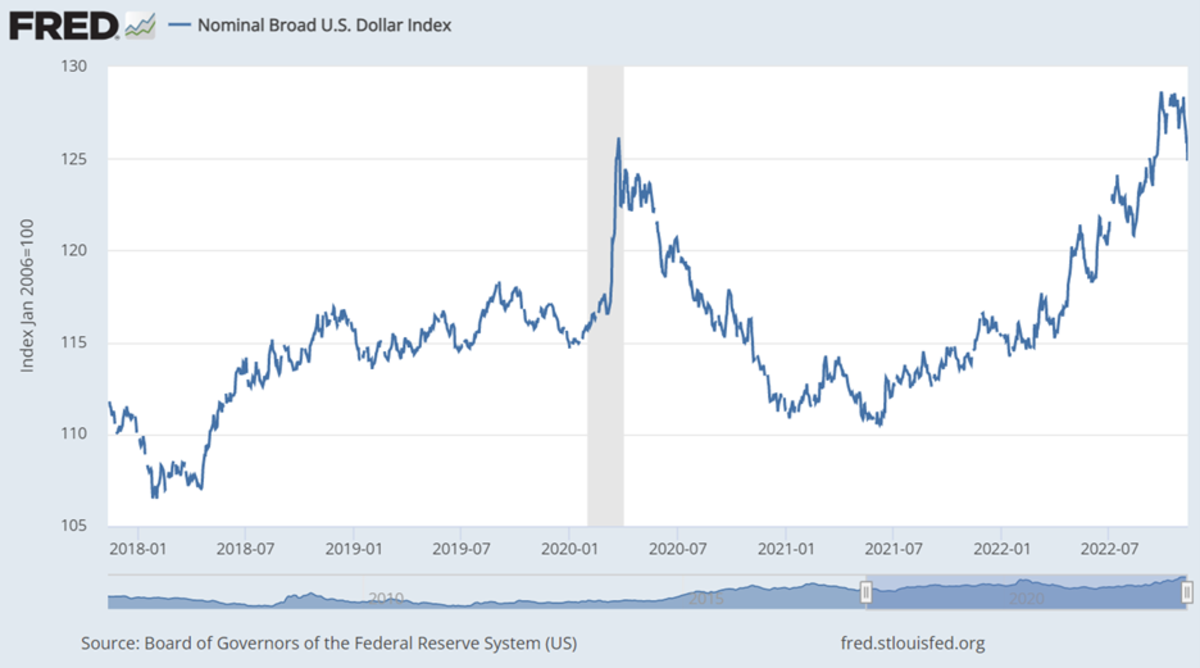

The US greenback worth index towards different international currencies, compiled by the Federal Reserve of Saint Louis, reached its highest degree within the final 20 years on the finish of September, declining this month (Determine 1).

Determine 1 – US Nominal Greenback Worth Index

From January to mid-October, the greenback rose 13% towards the euro, 22% towards the Japanese yen and 6% towards rising market currencies. The greenback appreciation was even steeper towards different superior economies than relative to rising market economies. In Q3, a sell-off in nearly all currencies besides the U.S. greenback, Mexico’s peso, and Brazil’s actual came about (Determine 2).

Determine 2 – Foreign money Values vs US Greenback 12 months-to-Date (left) and in Q3 (proper)

How one can clarify the greenback appreciation

Broadly talking, one could level out three totally different channels by way of which components affecting bilateral alternate charges function and have been pulling up the U.S. greenback (Bitel, 2022):

Yield differential

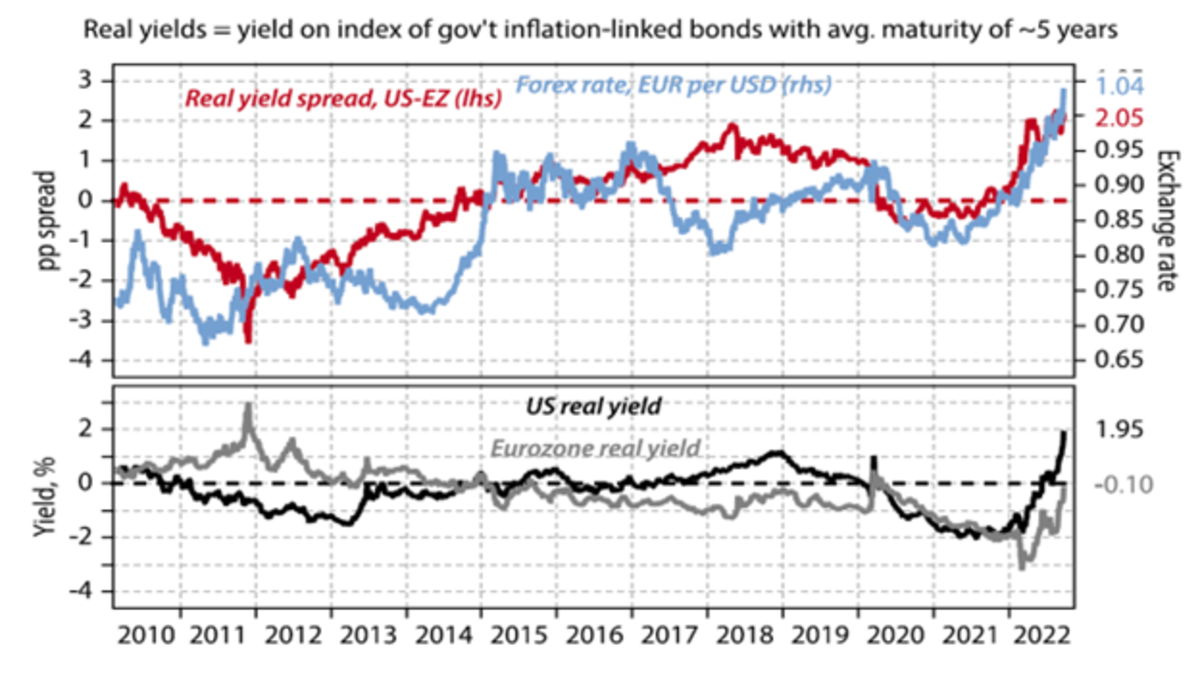

A significant factor underlying the appreciation of the greenback is the upper yield in actual phrases of US belongings relative to others. For instance, the true yield differential between the US and the eurozone, as measured by five-year inflation-linked authorities bond yields, pairs effectively with the euro’s depreciation towards the greenback (Determine 3). This differential mirrored sooner rate of interest actions upward within the US, adopted by the market’s conviction of the Federal Reserve Financial institution’s anti-inflation dedication, which was stronger in comparison with different central banks.

Determine 3 – U.S. and Euro Space: Actual Yields and Change Charges

In line with W. Denyer, an identical image could also be constructed extra broadly for the comparability of risk-adjusted charges of return for different fixed-income belongings. Given the heights already attained by the greenback, additional bouts of greenback appreciation would possibly occur provided that the opposite central banks proceed to lag in setting rates of interest and/or the tempo of adjustment by the Fed accelerates even additional. There are additionally at all times, in fact, one-off occasions, equivalent to the extraordinary depreciation of the British pound brought on by a proposal of unfunded tax cuts in October, a proposal later reversed.

The place taken by liquid investments in {dollars} as a “secure haven”, regardless of low returns, additionally will increase their demand in occasions of upper danger notion and decrease investor urge for food to hold such dangers of their portfolios. That is notably the case relative to nations with high-risk premiums. Within the current interval, geopolitical dangers, equivalent to these arising from the Russian invasion of Ukraine, have contributed to the demand for {dollars}.

There have been additionally, in fact, one-off peculiar occasions. Just like the sharp depreciation of the pound sterling when the British authorities made a proposal – then withdrawn – for tax cuts with out evident funding protection.

Liquidity differential

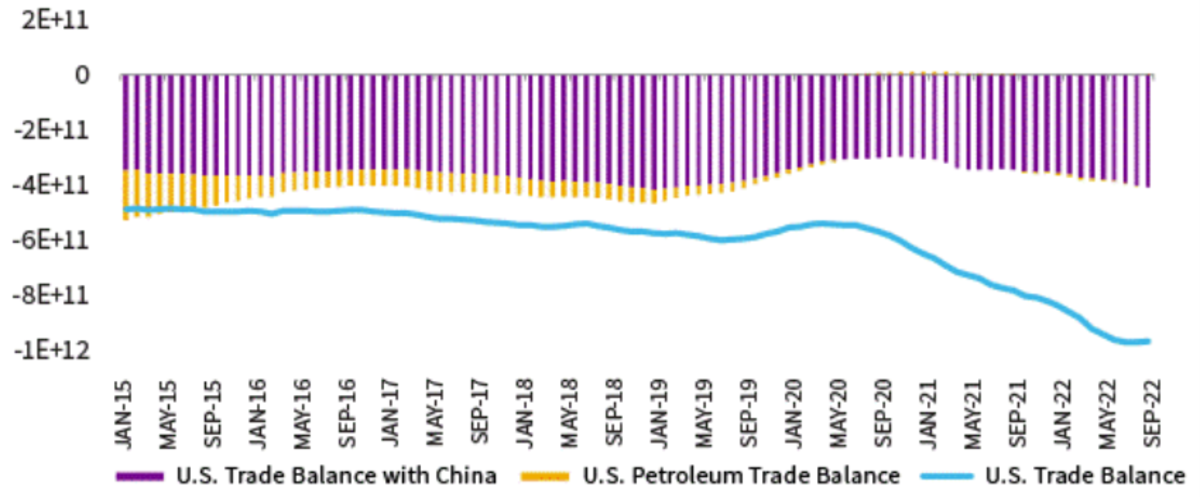

Ranges of U.S. greenback liquidity have additionally mattered, no matter whether or not it has just lately turn out to be dearer. There isn’t a official metric for the provision of {dollars}, and Bitel (2022) proposes a proxy utilizing the cumulative U.S. commerce deficit, measured by the U.S. commerce stability minus the U.S. petroleum stability and the U.S. commerce stability with China. She justifies subtracting the commerce deficit of the U.S. with China as a result of the Folks’s Financial institution of China hoards the {dollars} accompanying them, and China’s capital account is closed (Canuto, 2022a). China’s U.S. {dollars} don’t flow into as broadly within the international economic system as {dollars} held by different nations.

Rising (lowering) U.S. commerce deficits imply extra (much less) {dollars} are flowing out, depreciating (appreciating) the U.S. greenback relative worth. The U.S. commerce deficit as adjusted by Bitel (2022) has shrunk this yr, which means much less greenback abundance and its appreciation (Determine 4).

Determine 4 – U.S. {dollars} accessible

Progress differentials

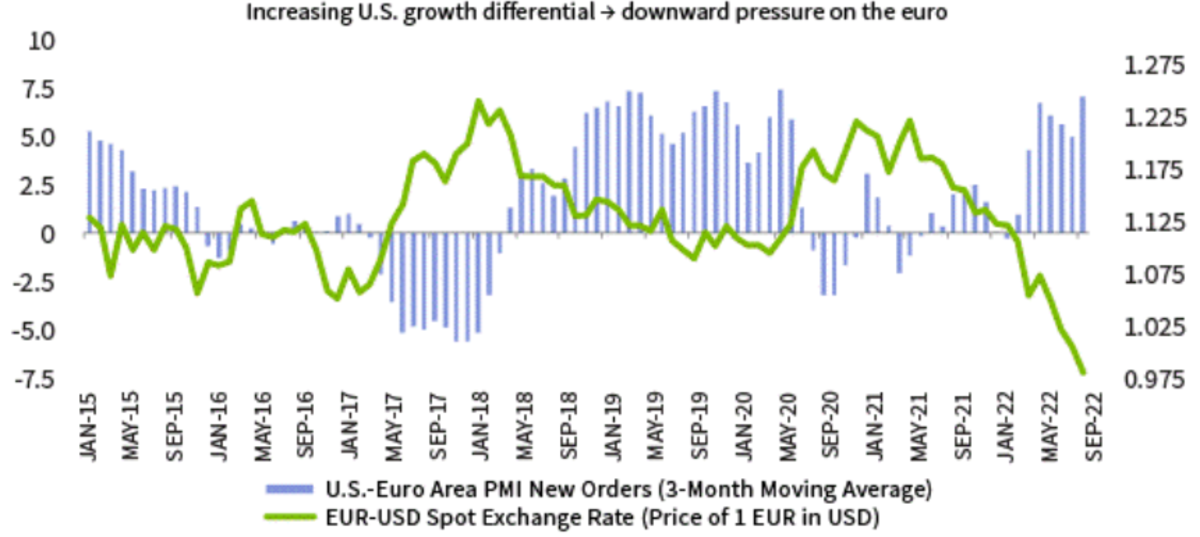

Comparative development paces additionally have an effect on alternate charges. Greater development charges imply larger probabilities of larger earnings from variable-income belongings. On this regard, the U.S. economic system grew extra strongly relative to different economies, with extra important earnings help and sooner pandemic restoration.

Europe can’t enhance GDP with out a important enhance in the price of power. The battle in Ukraine due to Russia’s invasion and following sanctions on the latter have led to an eightfold enhance in gasoline and electrical energy costs in Europe. The idiosyncratic character of the European power disaster and the very excessive chance of a deep recession have negatively affected the euro.

The expansion differential between U.S. and Europe has additionally exercised some corresponding influence on alternate charges (Determine 5). Each are sturdy, trusted currencies underpinned by massive economies with well-developed establishments and deep monetary markets. Nevertheless, development prospects have favored the greenback relative to the euro.

Determine 5 – Progress differentials

Whither the U.S. greenback?

What might then occur to the U.S. greenback forward, judging by these determinants of bilateral alternate charges?

The on-going Fed’s tightening could result in a U.S. recession, with three attainable eventualities as now we have approached earlier than (Canuto, 2022b). Nevertheless, related paths of development deceleration are probably in different areas, as it’s clearly the case of Europe, UK, Japan and others.

China, in flip, faces its personal challenges to ramp up development charges (Canuto, 2022c). Not by likelihood, the US greenback index weakened at first of the month as rumors a few China reopening circulated, because the stiff zero-COVID coverage pursued in China has been a dampening issue upon its macroeconomic efficiency (Westbrook and John, 2022).

Yield differentials, in flip, could enhance or lower relying on how inflation charges evolve in numerous zones. If the Fed decides to pause its marketing campaign of interest-rate will increase at first of 2023, that may imply yield differentials cease enhancing. The U.S. greenback would not seem so enticing relative to different currencies and carry trades might unwind. However that may also rely upon what occurs with inflation and financial insurance policies elsewhere.

What concerning the availability of U.S. greenback liquidity? That may rely upon the evolution of the U.S. current-account deficit, which in flip will rely upon development differentials.

Whither the U.S. greenback goes will due to this fact rely upon relative financial development and the choices of central bankers. Divergence from present developments in development, liquidity, and yields might set the greenback on a unique course. Finally, the “flip” or “pivot” of the greenback will more than likely happen when a “flip” or “pivot” happens in US financial coverage, given the latter’s key weight on the willpower of development and yield differentials. Then the decline to date in November would possibly point out that the U.S. greenback has left its peak behind.

Implications of the greenback appreciation

The sturdy appreciation of the US greenback towards different currencies within the current previous bolstered the contractionary pressures current within the international economic system. On the one hand, within the US, alternate fee appreciation acted within the course of mitigating native inflation. Nevertheless, contemplating the low relative weight of commerce within the US GDP, nothing near stopping home inflation by itself.

Then again, economies already going through rising home inflation had moreover to expertise the native value enhance of tradable merchandise brought on by the appreciated greenback and, due to this fact, larger strain for financial tightening. In fact, finally, the devaluation has expansive results on commerce balances. There’s nonetheless the phenomenon generally known as the “J-curve” impact: an preliminary loss earlier than a achieve follows. A rustic’s commerce stability initially deteriorates after a devaluation of its forex, earlier than recovering and sooner or later, outperforming its preliminary efficiency. Provide restrictions – together with power – tended to elongate the underside of this “J-curve” in lots of circumstances of devaluation towards the greenback. There was, due to this fact, a predominance of the speedy contractionary and inflationary impact of forex depreciation towards the U.S. greenback.

The appreciation of the greenback additionally has a compressive impact on economies which have excessive publicity to liabilities denominated in that forex. The greenback’s rise was extra intense towards the currencies of different superior economies. Nevertheless, even with out going by way of such intense devaluation, rising and creating economies with exterior liabilities in {dollars} discovered themselves extra susceptible.

This was the case for nations in Latin America, the Caribbean and Europe with private and non-private debt in {dollars} – not for Brazil, the place the federal government has constructive web belongings in {dollars} and there aren’t any important forex mismatches on non-public stability sheets, along with the nation being a web exporter of commodities. Nevertheless it was the case of a number of different rising and low-income nations coping with exterior indebtedness (Sri Lanka, Zambia, Pakistan, Argentina, Turkey, and plenty of others).

It is usually price noting the detrimental impact on the profitability of U.S. corporations for which the earnings obtained overseas is important. Along with harming the earnings of U.S. multinationals overseas, in addition to the dollar-denominated overseas liabilities of rising markets, a technique or one other the appreciation of the greenback can result in inflationary shocks in different nations and, thus, to tighter financial insurance policies. Restrictive coverage suggestions loops can at all times be triggered by a drastic and sudden appreciation of the greenback, and the rally of the greenback has evidently reminded everybody of such dangers.

A quickly appreciating U.S. greenback is especially precarious for rising market economies, to the extent that they conduct a big quantity of their enterprise in U.S. {dollars}.

What to do within the face of alternate fee strain

There’s an intrinsic problem to the globalized economic system. Every central financial institution seems to its personal nation, deciding financial insurance policies in accordance with what it deems essential in relation to the native dilemma between unemployment and inflation. However in such an interdependent economic system, the repercussions of any massive nation’s selections go far past its borders. And are available again. The chance of suggestions from restrictive financial insurance policies is even larger after they all reply to a typical inflationary downside, as it’s presently the case.

Transmission by way of alternate charges is a part of this interdependence. Greater rates of interest within the U.S. find yourself imposing on others the selection between additionally elevating rates of interest and/or permitting capital outflows and forex devaluation to happen.

Some nations are turning to direct alternate fee interventions as a substitute of elevating home rates of interest – or as a complement. Japan opted to promote reserves of US Treasuries to attempt to neutralize the yen’s forex devaluation towards the greenback. Switzerland additionally mentioned it was contemplating promoting overseas forex to help the Swiss franc, in addition to elevating rates of interest between its central financial institution conferences.

The interval after the 2008-2009 international monetary disaster noticed “forex wars”, when nations accused one another of exporting their unemployment issues by way of important reductions in home rates of interest and devaluation of their currencies. May a “reverse forex battle” be brewing proper now, because the appreciation of the US greenback exports inflation to others?

Broad coordination came about in 1985, when, as now, the greenback grew to become overvalued. The “Plaza Settlement”, then signed between France, West Germany, the UK, Japan and the USA, had as a profitable dedication the devaluation of the greenback.

Nevertheless, at the moment US inflation was already on the decline after a protracted interval of excessive home rates of interest, whereas the present tightening of financial and monetary situations within the US remains to be ongoing. The more than likely state of affairs is the absence of equal agreements, with some nations striving to keep away from pure rate of interest changes by way of direct intervention in overseas alternate markets. The impact shall be restricted if the underlying components driving capital flows and alternate fee strain don’t change.

Subsequently, the “flip” or “pivot” of the U.S. greenback will more than likely happen when a “flip” or “pivot” occurs within the U.S. financial coverage.

Within the meantime, as really helpful by Gopinath and Gourrinchas (2022), the Fed ought to reopen the faucet on precautionary strains of credit score with different central banks – as in the course of the pandemic – to keep away from the dangers of those being put towards the wall in conditions of sudden illiquidity when it comes to {dollars}.

References

Bitel, O. (2022). What’s Driving U.S. Greenback Power? William Blair, November 3.

Canuto, O. (2022a). Greenback dominance will stay, Coverage Middle for the New South, March 29.

Canuto, O. (2022b). Whither the Phillips Curve? Coverage Middle for the New South, Coverage Paper PP – 17/22, October.

Canuto (2022c). Whither China’s Financial Progress, Coverage Middle for the New South, Coverage Transient PB – 53/22, August.

Denyer, W. (2022). The Key Drivers for Currencies, Gavekal Analysis, September 28 (www.gavekal.com).

Gopinath, G. and Gourrinchas, P-O. (2022). How International locations Ought to Reply to the Robust Greenback, IMF Weblog, October 14.

De, I. and Yang, Z. (2022), Why did the Brazilian Actual and Mexican Peso outperform the super-strong US greenback this yr? FTSE Russell, October 28.

Westbrook, T. and John, A. (2022). Greenback stems losses as buyers eye U.S. midterms, Reuters, November 8

Coverage Middle for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Improvement. He’s a former vice chairman and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund, and a former vice chairman on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil.

[ad_2]