[ad_1]

Coverage Middle for the New South

The preliminary GDP (Gross Home Product) outcomes of the U.S. for the second quarter, launched by the U.S. Bureau of Financial Evaluation (BEA) on Thursday, July 28, got here with a drop of 0.9% in annualized phrases. Within the first quarter, it additionally confirmed a decline, within the order of 1.6% in annual phrases, after the overheated GDP rising 6.9% a yr within the final quarter of 2021.

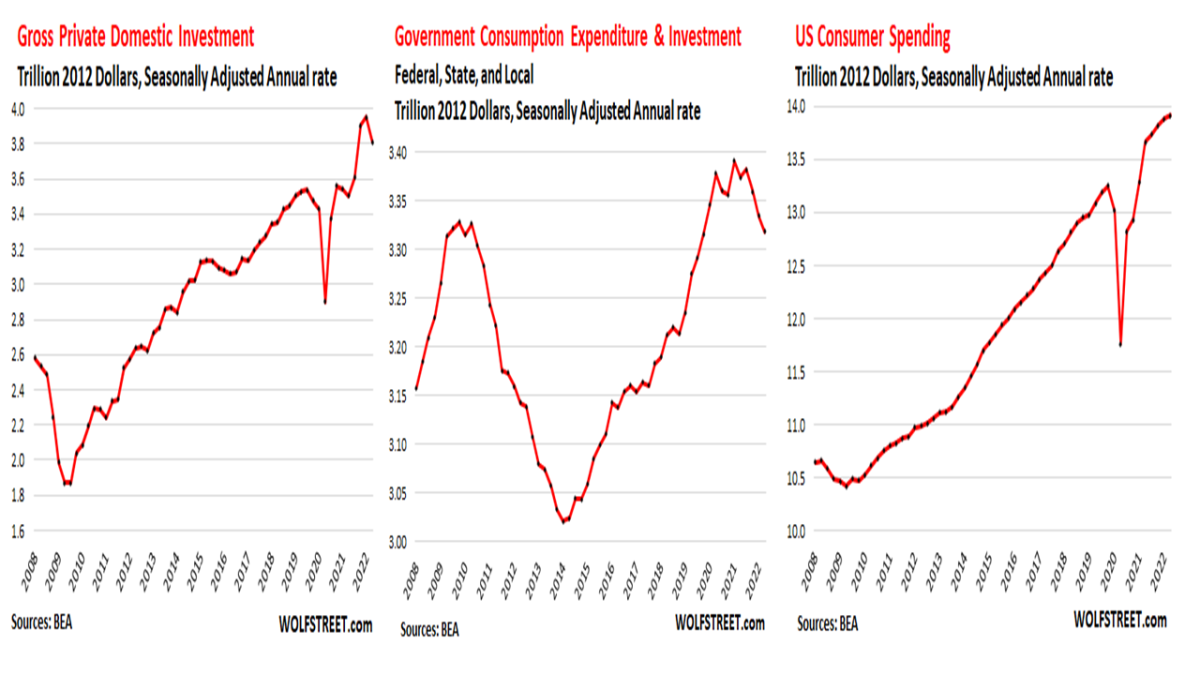

A discount in non-public funding – significantly residential – and public spending within the federal, state, and municipal spheres dragged GDP down within the second quarter. You will need to observe that non-public consumption elevated at an annual charge of 1% within the quarter, discounting inflation (Determine 1).

Determine 1 – U.S. GDP elements

A generally adopted conference is to name it a “technical recession” when there are at the least two consecutive quarters of GDP decline. Nonetheless, there are causes to think about such a press release untimely presently, even recognizing clear and simple indicators of an financial progress slowdown on the margin.

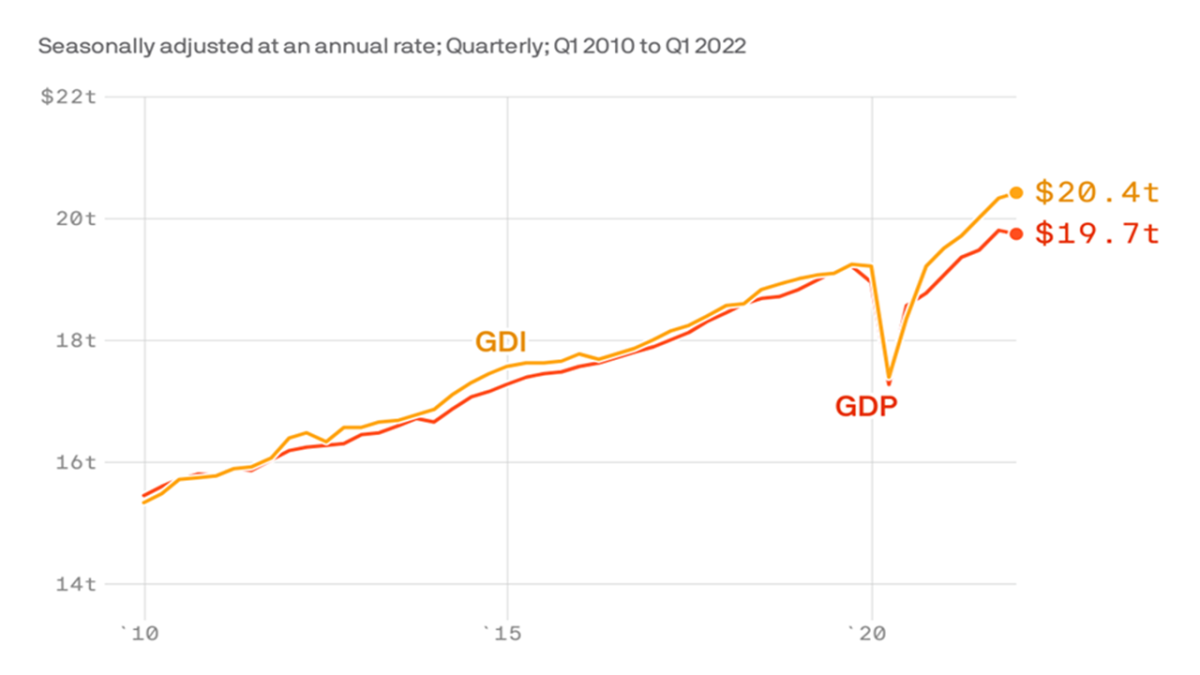

First, these preliminary GDP figures are continuously revised. It needs to be famous the present discrepancy between GDP and GDI (Gross Home Earnings) figures. Theoretically the 2 numbers needs to be equal, as GDP measures the sum of ultimate expenditures in an financial system, whereas GDI provides all incomes (wages, earnings, and curiosity funds). In follow, imperfections in statistical collections and variations in knowledge sources enable variations between them, even when adjusted someday later.

Nicely then! At this second, the distinction between them has no historic precedents and the GDI, within the first quarter, got here with a optimistic quantity, whereas the GDP fell (Determine 2). In accordance with a research by Jeremy Nalewaik, former economist on the Fed (Federal Reserve), estimates of GDI normally level to the place GDP is revised.

Determine 2 – Measures of financial progress

Along with the revision of GDP knowledge, it should be thought of that economists want to have a look at a set of indicators broader than the 2 quarterly GDPs of the “technical recession”. As advised by the resilience of personal consumption within the second quarter, the labor market remained tight. This tightening, by the way in which, was cited by Fed President Jeremy Powell, when denying that the financial system is already in recession, throughout the interview, Wednesday July 27, after the Fed assembly that determined to lift its primary rate of interest by 75 foundation factors to the vary of two.25-2.5%.

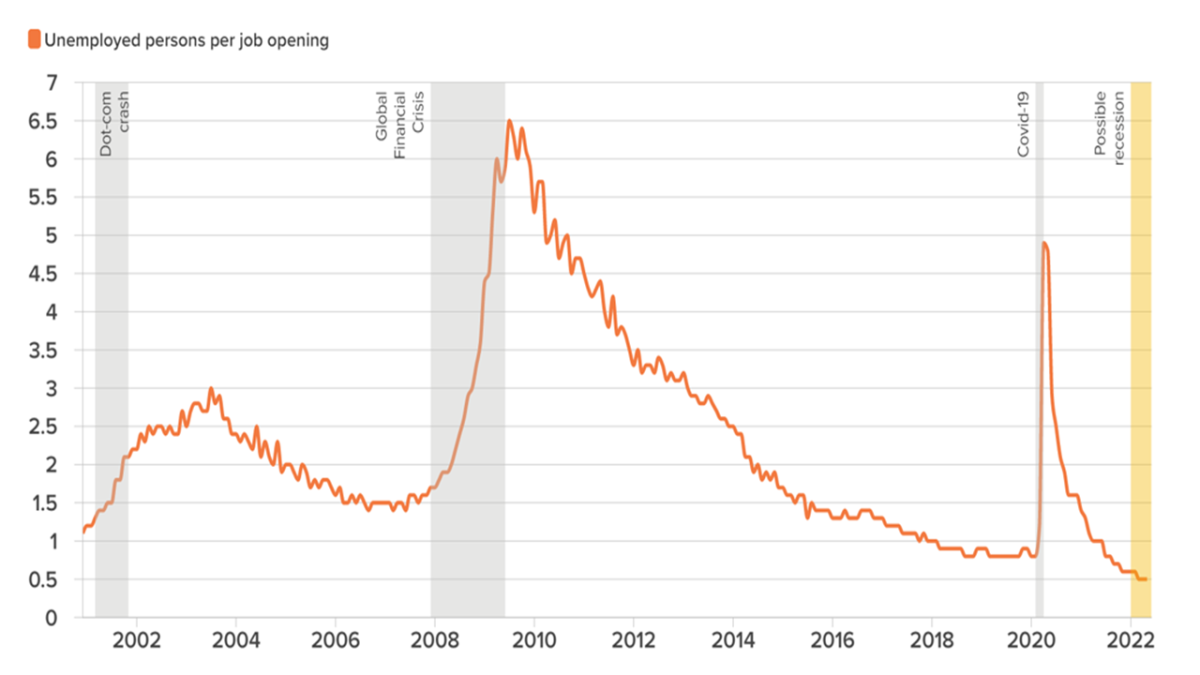

In June, 372,000 new jobs have been added, and the unemployment charge stabilized at a traditionally low degree of three.6%. For each unemployed individual, there have been roughly two vacancies accessible, making this one of many tightest job markets in latest historical past (Determine 3). We should contemplate the truth that the labor pressure participation, though elevated in comparison with the interval of the pandemic, stays low.

Determine 3 – Present U.S. labor market a lot tighter than prior to now three recessions

Two different indicators launched Friday, July 29, reinforce the purpose concerning the tight scenario within the labor market, whereas additionally indicating causes for the Fed to be involved about the necessity to tighten its financial coverage additional. The Employment Price Index (ICE) report, which tracks wages and advantages paid by U.S. employers, confirmed that complete pay for civilian staff throughout the second quarter elevated by 1.3%, up by about 5.1% in twelve months. As well as, the “core” value index of primary private consumption expenditures (PCE), which leaves out risky gadgets like meals and power and serves because the Fed’s essential benchmark, rose 0.6% in June, up 4.8% year-on-year.

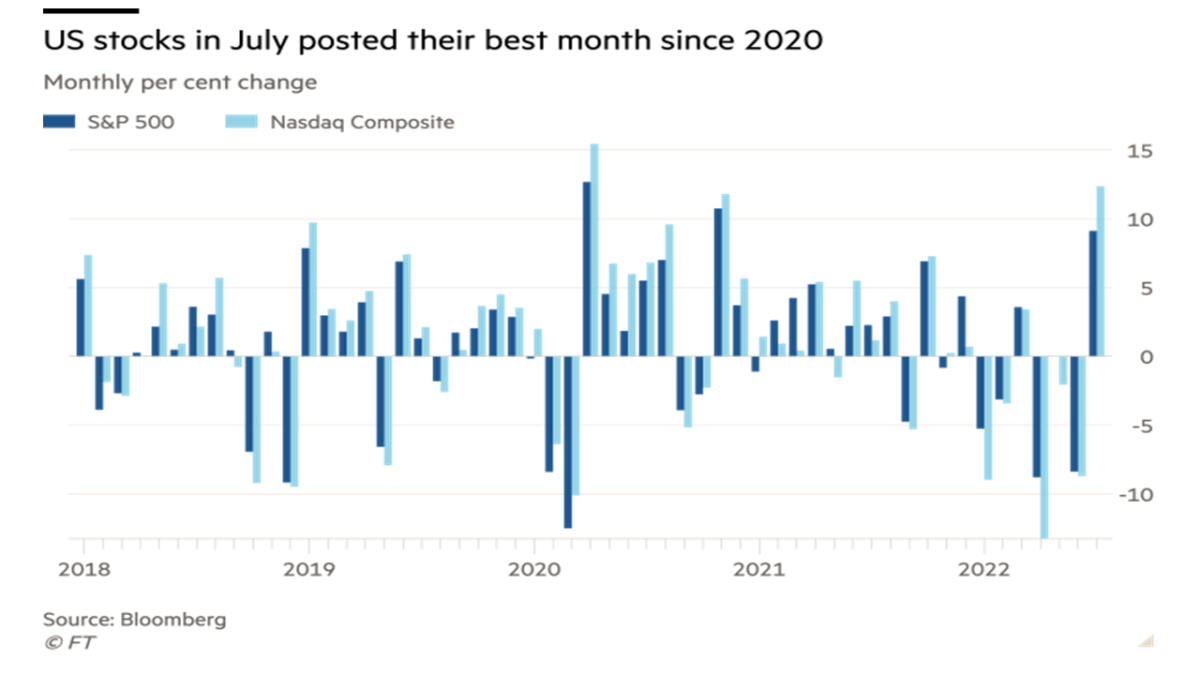

Final week additionally had, after all, the Fed assembly and Powell’s subsequent interview on Wednesday, after which fairness markets went up regardless of the rate of interest hike. The month of July ended up optimistic in these markets, after a primary half of the yr by which US shares suffered a decline not seen in half a century (Determine 4). Easy methods to clarify?

Determine 4

Markets have come to assign a excessive likelihood that the Fed will “pivot”, and reverse its tightening course, given indicators of an financial slowdown. “Dangerous information for the financial system is nice information for the markets”, turned a motto.

On the one hand, Powell fueled this perception when he mentioned within the interview that the fundamental rate of interest was coming into its “impartial” vary, that’s, the one which, in a broader time horizon, doesn’t take away or add demand stimulus to financial exercise. Then again, such a “impartial” charge assumes that inflation converges to the two% that constitutes the Fed’s common inflation goal, along with clearly nonetheless needing one thing between 0.50% and 1% extra to get there. Moreover, in the identical interview, Powell mentioned that the extent of financial exercise must undergo a interval beneath its potential for inflation to evolve to the goal, which might require rates of interest to stay above the “impartial” degree for a while.

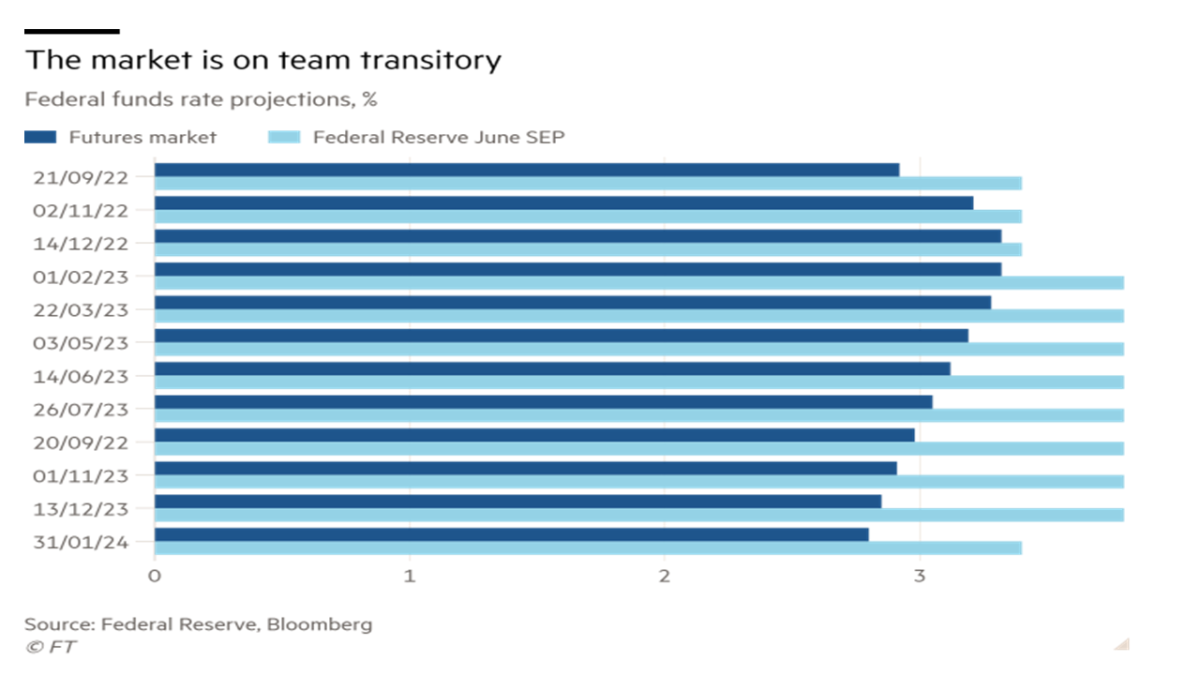

A chart offered by Robert Armstrong in his Monetary Instances article of July 28 illustrates the mismatch between Fed and market projections of the Federal funds charge (Determine 5). It compares what the Fed members projected final June for the Fed funds charge with market expectations as derived from the futures market. The market seems to be rather more dovish than members of the Federal Open Market Committee.

Determine 5 – Fed funds charge projections

The paradox is that, with the development in monetary circumstances expressed in inventory costs, along with the indicators of downward rigidity in core inflation proven final Friday, the Fed needs to be pressured to tighten extra, provided that its precedence is to decrease the inflation even at the price of a recession. It appears untimely to wager on such a “pivot” by the Fed, and this latest refreshment of inventory and bond markets tends to be reversed.

Strictly talking, the tug-of-war between the Fed and the markets will stay fierce sooner or later forward, with two factors remaining unclear: if the financial system does certainly fall right into a recession, how shallow or deep will it’s? How inflexible downward will the inflation charge measured by its core grow to be?

Rather a lot will occur between now and the following Fed assembly in September, together with information on inflation (and GDI, on the finish of August). In my view, as of at this time, the query is whether or not the Fed will elevate its charge by 0.50% or 0.75%. Keep tuned!

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Middle for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Growth. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]