[ad_1]

Unique Submit (Coverage Heart for the New South)

Within the first half of this 12 months, U.S. inventory markets suffered a fall not seen in additional than 50 years. The S&P 500 index on Thursday June 30 was greater than 20% down in comparison with January, a drop not skilled since 1970.

The S&P 1500 index, constructed by Bloomberg and incorporating firms of assorted sizes, has seen greater than $9 trillion in inventory worth disappear since January. Apart from power shares, all sectors have suffered worth reductions. On Wednesday June 29, Citi introduced that it expects the S&P 500 to fall by round one other 11% by the top of the 12 months.

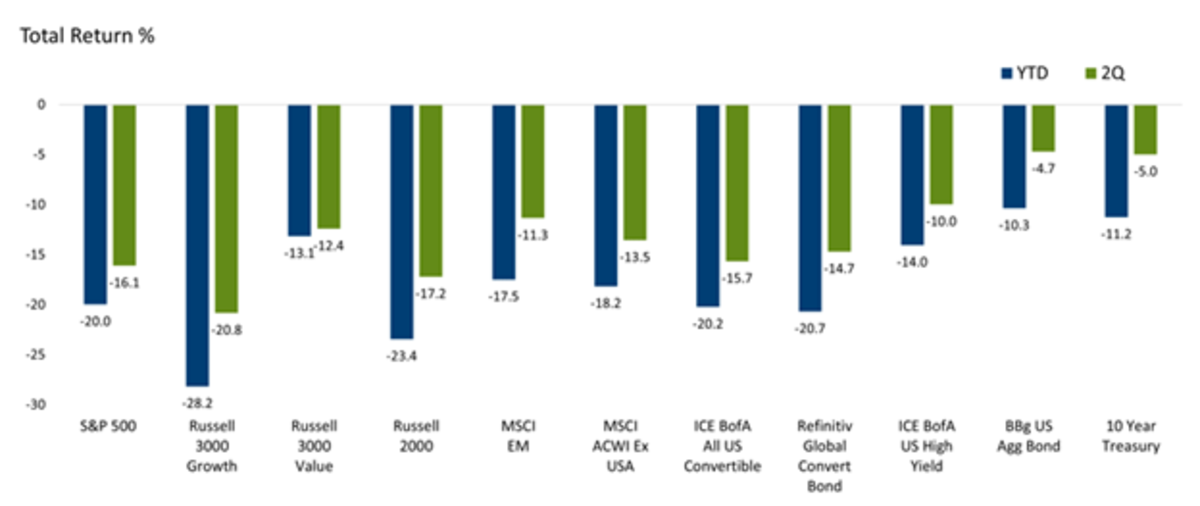

Inventory market declines have additionally occurred in Europe and Asia. The European Stoxx 600 index is down about 17% since January, whereas the MSCI index for Asia-Pacific markets is down 18% in worth in U.S. greenback phrases. The FTSE All World index, which brings collectively shares from superior and rising economies, has additionally shrunk, by simply over 20% thus far this 12 months. Determine 1 exhibits how usually unhealthy the worldwide asset class efficiency has been within the first half of the 12 months.

Determine 1: World Asset Class Efficiency: A Painful 1H22

The notion of recession dangers within the U.S. and Europe has been a significant component on this flight of buyers out of inventory markets. Though the numbers within the U.S. labor market in Should confirmed a excessive diploma of heating, family consumption spending decreased within the month, on prime of the numbers within the earlier months which have been revised downwards. Client confidence indices have plummeted. In housing, the unprecedented rise in mortgage rates of interest since 2010 has strengthened this worsening. An Institute of Provide Administration (ISM) report, launched Friday July 1, confirmed indicators of a pointy drop within the tempo of producing exercise in June within the U.S. economic system.

In Europe, there was additionally a powerful deterioration in indicators of producing exercise and shopper confidence within the German economic system. The European economic system was already anticipated to really feel the total impression of the provision and value shocks ensuing from the battle in Ukraine. In Asia, the impacts of China’s zero-COVID coverage had additionally already led to a downward revision in development forecasts for the 12 months. The actual change now corresponds to earlier indicators that, in reality, the expansion slowdown within the U.S. economic system has joined that of different superior economies.

A significant factor within the withdrawal of fairness buyers has been the notion that indicators of a slowdown is not going to reverse the trajectory of rising rates of interest on either side of the Atlantic—previewed for later this 12 months within the euro space—and tightening of monetary situations. On the annual convention of European central bankers in Portugal on June 30, US Federal Reserve (Fed) Governor Jerome Powell even spoke of “some ache” as a bitter drugs essential to return inflation to nearer to the common 2% established as a goal.

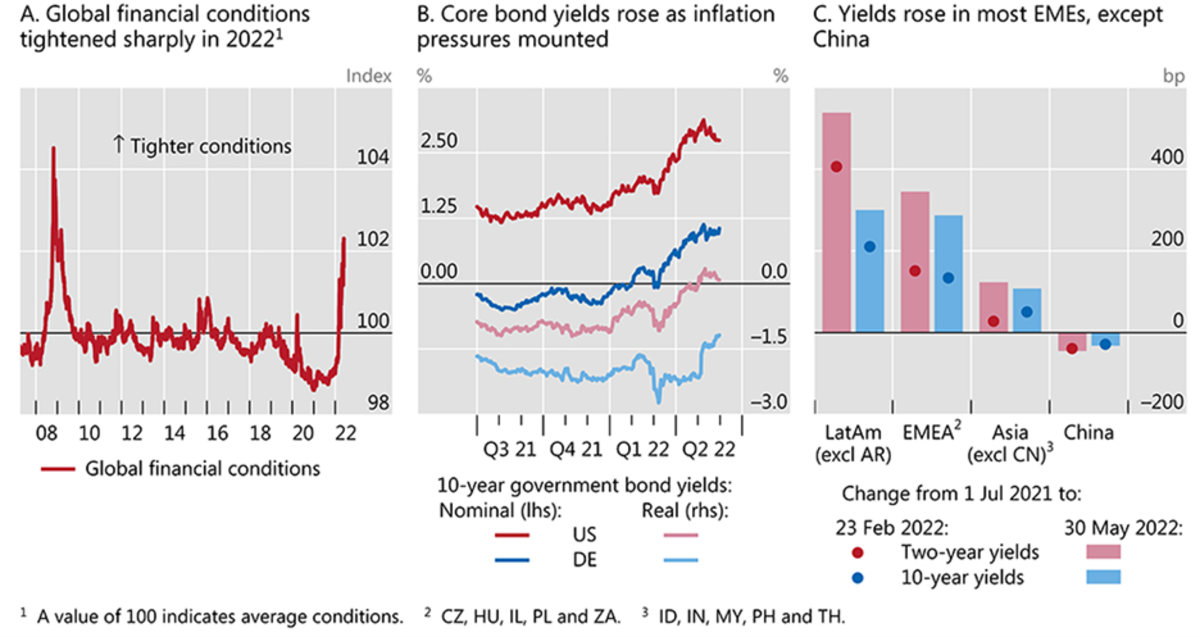

As Determine 2 exhibits, monetary situations have tightened as authorities bond yields have risen globally, together with in most emerging-market economies, besides China. Such tightened situations are anticipated to worsen as central banks maintain shifting alongside that path.

Determine 2: Monetary Situations Have Tightened as Authorities Bond Yields Have Risen

On this context, the inventory devaluation suits in with different objects of U.S. financial coverage within the pursuit of decrease inflation charges. Along with the ‘quantitative tightening’—the gradual discount of the Fed’s stability sheet, and not using a replenishment of the property within the portfolio that mature as of this month—the unfavorable ‘wealth impact’ of the autumn within the worth of shares will assist to comprise mixture demand, which corresponds exactly to the Fed’s coverage goal.

It is a important distinction from different moments within the latest historical past of the connection between Fed insurance policies and asset markets. In 1987, after an nearly 30% drop in U.S. inventory costs, then-Fed President Alan Greenspan minimize rates of interest in what turned often known as a ‘Greenspan put’: a sort of insurance coverage towards losses, much like a put choice bought as safety towards sudden losses in worth, solely on this case offered by the Fed and freed from cost to asset holders. Within the years that adopted, the expectation of bailouts by way of Fed financial insurance policies as a response to asset devaluations ended up being included as a premium in asset values.

That was the case, for example, in 2018. However not this time. The dedication to scale back inflation by containing mixture demand now sounds just like the precedence.

Strictly talking, the Fed can ignore falling shares whereas keeping track of credit score markets, not least as a result of there’s a direct relationship between credit score and financial institution cash creation, and subsequently implications for mixture demand and inflation. However the Fed can’t ignore systemic dangers that monetary intermediaries will go bancrupt.

And the way are costs within the credit score markets behaving? Danger spreads have widened each for high-risk bonds—rated CCC—and ‘funding grade’ circumstances. Along with the dangers arising from the rise in rates of interest, consideration has now turned to the dangers of credit score and liquidity disappearance.

Judging by studies from credit standing businesses, U.S. non-financial firms have taken benefit of the power opened by the Fed, in March 2020 within the wake of the monetary disaster triggered by the pandemic, to elongate debt maturities on favorable phrases. The obvious scope for charge hikes, with little concern for his or her impression on company fairness constructions, supplies consolation for the Fed to proceed elevating charges. Moreover, charges are nonetheless low in actual phrases when discounted by anticipated inflation charges this 12 months and subsequent.

How far the Fed will go is an open query. It’ll rely on the indicators of inflation as rates of interest transfer up. A foul signal was the truth that the index that serves because the official reference—the Private Consumption Expenditures (PCE) Value Index—rose in Might and reached a degree 6.3% greater than a 12 months in the past. Within the euro space, inflation in June hit a report 8.6%.

Lengthy-term inflation expectations expressed in 10-year inflation-protected U.S. Treasury bonds are round 2.36% every year, remaining within the vary between 1.5% and a pair of.5% that has been a trademark for the final twenty years. If inflation exhibits clear indicators of slowing within the months forward, the Fed might not attain the three.5%-3.75% vary at present anticipated for the center of subsequent 12 months. The issue is that, even realizing that there’s a time lag between rate of interest choices and their results, the Fed will be unable to disregard what occurs to month-to-month inflation charges within the interval till subsequent 12 months, even when that poses a danger to a mushy touchdown of the economic system.

After all, important unfavorable surprises on the corporate-finance facet may additionally result in some type of ‘Powell put’. What appears extra doubtless, nevertheless, is the mixture of a worldwide financial slowdown and continued tightening of world monetary situations. Fairness markets in superior economies will proceed to exhibit downward slides till the monetary-financial grip eases.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]