[ad_1]

Otaviano Canuto and Sebastian Carranza

Unique submit on the Coverage Heart for the New South

A proposal to dollarize Argentina’s financial system reached its Congress in March. As this route sometimes seems as a proposal in Argentina, we summarize right here the potential penalties of such a transfer.

First, we level out broadly the implications of dollarizing an financial system. Then, we examine related Latin American experiences with dollarization. Lastly, we tackle the case of Argentina.

Argentina’s fiscal imbalances is not going to be eradicated by dollarization. Despite the fact that dollarization would forestall the printing of cash, it imposes no constraints on authorities spending and borrowing. The one result’s that financial coverage ceases to be obtainable as an possibility, leaving virtually no response capability in case of exterior shocks. Furthermore, dollarization creates the opportunity of being uncovered to pro-cyclical financial insurance policies unrelated to home requirements. It additionally eliminates seigniorage advantages.

Latin American experiences of dollarization have been adopted by makes an attempt by Ecuador and El Salvador to discover a means out of it. Nonetheless, as soon as dollarization is carried out, this can be very laborious to backtrack. Up to now, there may be not a single related case wherever of profitable de-dollarization.

Argentina’s central financial institution has inadequate greenback reserves to match the financial base. The financial base (or M0) is the entire quantity of a forex both on the whole circulation within the arms of the general public, or within the type of industrial financial institution deposits held within the central financial institution’s reserves. The creation of cash (greenback deposits) by home banks wants M0 to be greenback denominated.

Proposing dollarization below present circumstances would require a selective default of home forex liabilities, a brutal devaluation, and/or unilateral conversion of public deposits. None of those are emphasised by those that have made dollarization proposals.

Primarily based on the final implications, the Latin American experiences, and the implementation difficulties, we talk about how these concepts are unfeasible in Argentina now.

Why Focus on Dollarization of Argentina In the present day?

In 2001, Kenneth P. Jameson printed an article titled ‘Dollarization in Latin America: Wave of the Future or Flight to the Previous?’ He argued that the area was shifting in direction of dollarization and that altering the authorized forex to the U.S. greenback represented the “final gambit” for Argentina’s president at the moment, Fernando De la Rua. Kurt Schuler and Steve H. Hanke (2001) printed an article titled: “How one can dollarize in Argentina now”, by which they proposed 4 steps in direction of dollarization as a way to “assist Argentina return to an financial development path”.

Despite the fact that these proposals by no means materialized, they have been stored on the cabinets, ready for the best second to reemerge. In March 2022, an Argentine lawmaker—Alejandro Cacace—proposed a invoice to dollarize the Argentine financial system. One of many candidates for the subsequent presidential election in 2023, Javier Milei, introduced he supposed to name a referendum to realize this aim (Burns, 2022). Furthermore, native and international economists, together with Nicolas Cachanosky (American Institute for Financial Analysis) and Steve Hanke (Cato Institute), have argued that dollarization for Argentina is “the one means out to keep away from hyperinflation”.

What’s Dollarization?

Generally phrases, ‘dollarization’ is usually used to confer with residents holding a big share of their property in international forex. In Latin America and the Caribbean, the U.S. greenback is the primary forex gravity heart.

It’s vital for instance the distinction between de-jure and de-facto dollarization. The primary refers back to the case by which international forex is given authorized tender standing, which suggests that the international forex is used legally for the three capabilities of cash (retailer of worth, unit of account, and medium of change). Then again, de-facto dollarization represents the state of affairs by which the international forex is getting used alongside the home forex, however not with an equal authorized standing. The commonest case in Latin American international locations is saving in laborious forex. De-facto dollarization could happen to completely different levels. International locations transitioning in direction of de-facto dollarization are referred to as ‘bi-monetary economies’[1].

One other distinction is between home dollarization, when monetary contracts between home residents are made in international forex, and exterior dollarization, which covers monetary contracts between residents and non-residents.

What Are the Implications of Totally Dollarizing an Financial system?

Dollarization is a step past selecting between fastened versus floating change price regimes and full convertibility between home and foreign exchange.

A primary consequence is the lack of seigniorage (the distinction between the price of manufacturing of cash and its face worth)[2], or its corollary: financing different nations’ seigniorage. There are two parts to the seigniorage loss implied by dollarization: 1) A right away ‘inventory’ price. To withdraw home forex from circulation, the financial authority must buy the M0 inventory of home forex in change for U.S. {dollars}, returning the accrued seigniorage earnings accrued over time. 2) The financial authority provides up future seigniorage earnings from the move of recent printing to fulfill cash demand.

A second consequence is that proactive financial coverage ceases to be obtainable, and the dollarized financial system turns into tied to a different nation’s financial coverage selections.

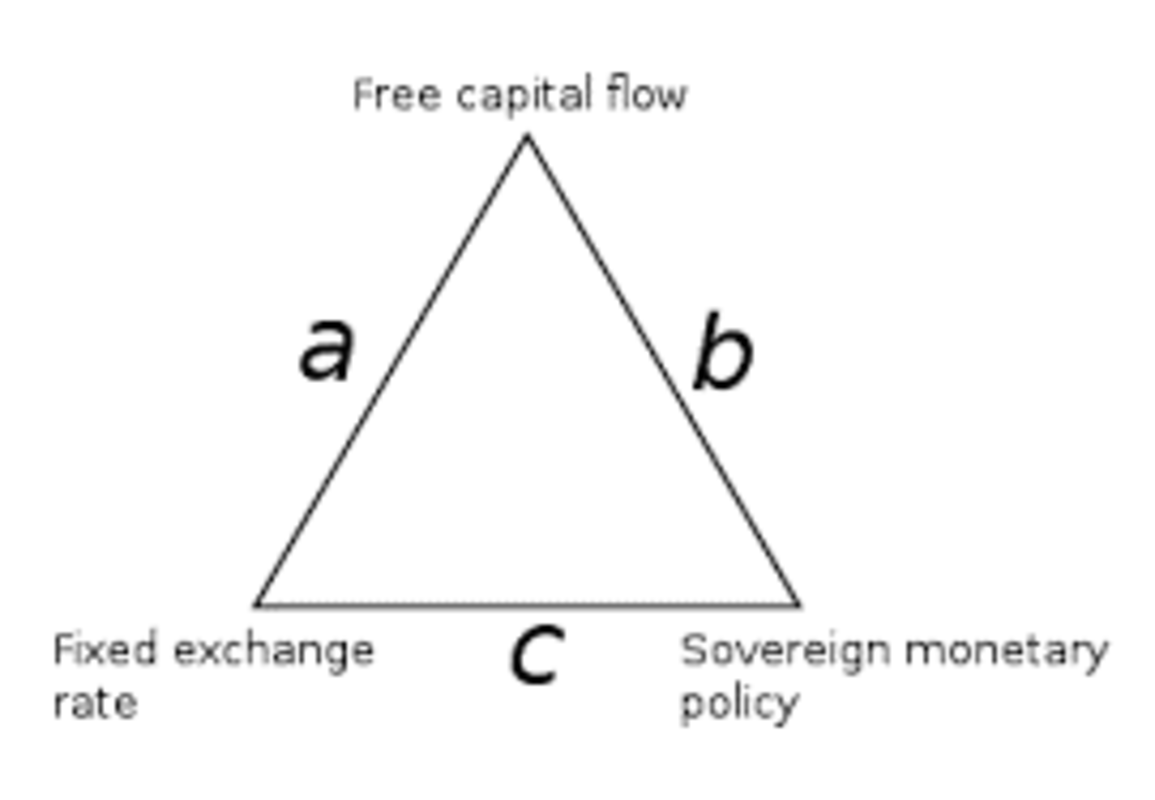

Difficulties in implementing pro-active financial insurance policies are already current with fastened change charges below circumstances of free capital mobility, as stipulated by the trilemma of worldwide finance, also referred to as the ‘not possible trinity’ or the Mundell-Fleming trilemma (Determine 1). There may be at all times a possible battle between the exchange-rate fastened dedication and sovereign financial coverage when capital flows freely to a rustic.

Dollarization is a radical transfer away from any fastened change price regime. Moreover, as M0 strikes past the management of home financial authorities, the latter are not able to implementing proactive financial insurance policies.

Determine 1: Not possible trinity

That is significantly problematic when the home financial system is just not deeply correlated with the financial system of the nation of the adopted forex. That is the “optimum forex space” argument additionally developed by Robert Mundell (1961). In different phrases, the dollarizing nation not solely loses the opportunity of making use of counter-cyclical financial insurance policies, but in addition is perhaps uncovered to inappropriate financial insurance policies from one other nation. Nonetheless, as acknowledged by Mundell, abdicating from one’s personal counter-cyclical insurance policies wouldn’t be a significant drawback if shocks affecting the realm as an entire are related—a situation favorable to financial integration. Free mobility of labor within the monetarily unified space additionally facilitates the absorption of shocks.

That’s the reason financial unification of areas—akin to when the euro space was created—comes accompanied by a number of different reforms. In addition to labor and capital mobility, a typical fiscal framework must be carried out, as together with harmonization of monetary regulation. To an amazing extent, the euro-area disaster after the worldwide monetary disaster uncovered the incompleteness of the complementary reforms (Canuto, 2021).

A 3rd consequence of dollarization is the restricted scope for lender-of-last-resort operations. Typically, central banks operate as the last word guarantor of the monetary system’s stability in case of a financial institution run. Within the case of a completely dollarized financial system, the central financial institution loses the power to print cash, which means that in a state of affairs of a generalized lack of confidence in banks, the central financial institution can be unable to ensure the entire fee system or to again financial institution deposits totally.

Cachanosky (2022) dismissed this as a weak issue in opposition to dollarization in Argentina. He remarked that financial institution runs within the nation can’t be countered with domestic-currency cash, as greenback exit predominates and operating brokers is not going to take local-currency bonds. He additionally referred to the opportunity of self-administered swimming pools of financial institution deposits complying with that operate with out the necessity for a public pool of reserves. He identified the operation of emergency liquidity funds in Ecuador, El Salvador, and Panama.

In any case, proactive financial insurance policies are given up. Not by likelihood, Cachanosky praises dollarization for precisely doing this. It might be a type of acknowledgment by the nation that it mustn’t have discretionary resolution energy over financial topics.

What can be some great benefits of dollarization? It might in precept resolve virtually instantaneously the home inflation[3] drawback. This doesn’t imply that there shall be no inflation, however—given the absence of change price fluctuations, and assuming financial integration— the gravity heart can be U.S. inflation, which is normally decrease than inflation in Latin American economies[4].

A second optimistic component of dollarization can be the discount of the danger premium related to exchange-rate fluctuations. Subsequently, following the curiosity parity situation, the home rate of interest would diminish, supposedly growing funding and potential GDP ranges.

A 3rd profit, solely observable in the long term, can be the elimination of forex crises and the macroeconomic instability that they bring about.

There may be additionally one related issue from the standpoint of long-term coverage making: dollarization is almost irreversible. As soon as you’re in, this can be very tough to get out. As we are going to see within the subsequent part, many individuals in Ecuador and El Salvador have been attempting unsuccessfully to determine learn how to go away dollarization for greater than a decade.

It needs to be famous that the attribution of stability as a assured consequence of abdicating the native forex and home financial policymaking displays a view that reduces all instability to the financial sphere. Actual-side shocks not have financial coverage as occasional shock absorbers. The bigger a rustic, and the extra dissociated from the mother-currency it’s, the extra unilateral foreign-currency adoption—not accompanied by euro area-like reforms—will go away the adopter topic to the danger of residing with the native transmission of financial coverage choices that aren’t applicable for native circumstances. Eliminating previous financial mismanagement doesn’t imply mechanically that applicable financial settings will exchange it.

Some Latin American Experiences

Ecuador

Ecuador is a case of de-facto dollarization. An financial disaster triggered this course of at first of the century. By evaluating its expertise with different international locations of the area, together with Argentina, we will infer that Ecuador’s macroeconomic disequilibrium might have been resolved with out such a drastic regime change. Nonetheless, a counterfactual evaluation on this case must be made.

Associated to what we identified, the Ecuadorian expertise reveals that dollarization de facto diminished inflation on the expense of accelerating the volatility of the financial cycle.

A very powerful conclusion relating to Ecuador’s expertise is that modifications within the financial regime don’t resolve structural financial issues, akin to lack of productiveness development or—in Ecuador’s case—extreme oil dependence. After dollarizing an financial system, if the previous financial construction stays, it could nonetheless have debt crises, as Ecuador just lately did. Subsequently, it’s not a shock that many political leaders have analyzed methods to de-dollarize Ecuador. Paradoxically, leaving this regime may need extra brutal penalties than these which motivated its adoption.

El Salvador

This de-facto dollarization occurred after a unilateral resolution of the Salvadorian authorities throughout the first 12 months of the brand new millennium. The anticipated outcomes have been monetary integration, decrease inflation, and diminishing home rate of interest volatility. As an alternative, a few of these variables confirmed modest enhancements however at a excessive price.

After dollarizing, El Salvador confirmed a optimistic impact when it comes to industrial integration. However, correlation doesn’t indicate causation. Levy Yeyati (2012) confirmed that the entire Caribbean area raised its ranges of commerce openness throughout these years. Furthermore, he utilized a gravity mannequin by which the dummy widespread forex with the U.S. had a damaging and vital impact on the anticipated commerce features.

By way of inflation, El Salvador stood under different international locations within the area each earlier than and after dollarization.

One of many principal prices of dollarization was seen in fragility to exterior shocks. Evaluating El Salvador’s response to the 2008 monetary disaster to its regional neighbors, each in exercise and monetary phrases, El Salvador seems to be amongst these most affected by the disaster.

Lastly, when it comes to development and volatility, any easy comparability of the 1990-2000 (earlier than dollarization), and 2000-2010 (after dollarization), intervals reveals that El Salvador’s development sample when it comes to each ranges and volatility has not differed visibly from these of its neighbors.

Argentina: Dollarization Forward?

In the beginning of every semester, the Nobel Prize-winning economist Simon Kuznets used to say to his Harvard college students: “There are 4 varieties of nations on this planet: developed international locations, undeveloped international locations, Japan, and Argentina.”

Argentina has been via one of many biggest financial reversals of the previous century. A rustic with considerable pure assets and excellent human capital that when had GDP per capita increased than the U.S. has deteriorated constantly to its present degree.

Argentina has been coping with inflation for nearly seven a long time. After peaking in 1989 (with hyperinflation), the federal government of Carlos Saul Menem opted for a forex board, impressed by the Hong Kong expertise throughout the Nineteen Eighties. It was a set change price regime with the equivalence of 1 U.S. greenback = 1 Argentine peso. Regardless of its speedy effectiveness in coping with inflation, this regime created macroeconomic difficulties that ended with the best financial disaster in Argentina’s historical past. Despite the fact that the financial regime didn’t trigger the disaster, it contributed to hiding the macroeconomic disequilibrium beneath it.

As we’ve already remarked, it is rather difficult to desert any ultra-rigid change price regime. It creates a dissociation between the technical diagnostics and the inhabitants’s beliefs. In 2000, surveys in Argentina confirmed {that a} vital majority of the inhabitants wished to maintain the 1-to-1 parity, regardless of having misplaced any sustainability.

The primary argument in opposition to dollarization in Argentina is linked to the thought expressed above. Dollarization creates a dissociation between what the financial system wants and what voters demand. Dollarization influences politicians in direction of short-term options as a substitute of what technical evaluation would possibly counsel.

The second argument is that dollarization wouldn’t resolve the actual drawback behind Argentina’s steady decline: productiveness. As Nobel Prize-winner Paul Krugman as soon as mentioned, “Productiveness isn’t all the pieces, however in the long term, it’s virtually all the pieces”. Despite the fact that somebody would possibly argue that the discount within the home rate of interest (much less threat premium) will assist funding, and due to this fact productiveness, this isn’t ample. Argentina’s productiveness drawback has two roots associated to 1 one other: lack of competitors due to protectionism, and authorities inefficiencies transferred to the personal sector. Neither of those shall be solved by merely dollarizing the financial system. Furthermore, the issue would possibly worsen for a 3rd purpose, as follows:

Argentina’s fiscal deficit will not be coated partially by the inflation tax. By dropping management of financial coverage, the federal government will lose one among its main sources of financing. Despite the fact that it’s a wholesome coverage to restrict financial financing via fiscal deficits, the end result might go in one among two instructions. If the federal government decides to cut back its spending, Argentina would possibly comply with a ‘good equilibrium’ path[5]. However there’s a extra engaging answer for politicians, which is more cost effective in political phrases: elevating taxes. If Argentina takes this second various, it’s going to enter a ‘unhealthy equilibrium’ path, and productiveness will decline moderately than improve.

Up to now, the primary good thing about changing the home forex with a international forex can be using the latter as a nominal anchor of expectations. Fiscal self-discipline is a requirement of dollarization processes. However then, why is dollarization wanted within the first place? Isn’t fiscal self-discipline ample to calm expectations and return to the expansion path? Is it price dropping financial coverage for this further lock-in?

Cachanosky (2022) argued that dollarization has helped Ecuador keep away from falling into the lure of populist and unsustainable fiscal insurance policies that led Venezuela to its collapse. In reality, as he acknowledged, a dollarization of Argentina can be a part of a recognition that the nation is incapable of managing itself fiscally and monetarily.

Shutting down financial coverage would depart Argentina defenseless in opposition to exterior shocks (except someway dollarization by itself managed to generate reserves and debt capability, which isn’t apparent). A transparent instance of this case was the inadequate fiscal response to COVID-19 in dollarized economies. For international locations the scale of Argentina, adopting a passive stance to international shocks could also be removed from optimum.

In contrast to some European experiences, Argentina has neither sufficient reserves nor credit score help from developed economies akin to France or Germany to offset the implications of exterior shocks. Subsequently, is it smart to surrender the one device left? Abdicating from financial and monetary coverage autonomy could also be too exaggerated a transfer due to earlier coverage mismanagement.

Argentina has proved Simon Kuznets proper once more in terms of imposing self-discipline to financial coverage. In 2001, when Argentina was struggling a liquidity disaster and the forex board restricted financial issuance, the treasury and a few provinces determined to challenge native bonds[6] that, in apply, labored as forex. These ‘bonds’, colloquially referred to as ‘quasi currencies’, have been utilized by governments to pay public-sector wages, and inject liquidity into the system in the course of the disaster. This expertise confirmed that ‘necessity is the mom of invention’ and that fiscal self-discipline is just not assured below a set financial regime, and far much less so in a dollarized financial system.

One other argument is the problem of reversing such a change as soon as it occurs. Take the case of the Argentine expertise of forsaking the forex board. Dollarization is an much more excessive measure, via which the home forex can be fully eradicated. However, if the idea is just not sufficient to persuade the reader, two completely different circumstances (Ecuador and El Salvador) are nonetheless now, 20 years later, attempting to determine learn how to abandon their regimes. El Salvador is experimenting with cryptocurrencies, whereas Ecuador has not discovered another but.

A last argument is expounded to implementation. Typically the implementation is ignored, however it’s a basic challenge. The central financial institution should soak up all its liabilities in home forex in change for U.S. {dollars}. However this isn’t solely M0; it contains debt titles (Pases, LELIQ y NOTALIQ, and many others.) and deposits. Subsequently, the apparent questions are: how? And, at what price would the absorption be?

In 1990, earlier than the forex board, the Argentine authorities transformed public deposits to ‘Bonex 89’ bonds to be repaid ten years later, which meant a drastic lower in M2, and facilitated the set up of the forex board just a few months later. Are promoters of dollarization contemplating any of those measures?

The state of affairs now is just not very completely different. Argentina’s central financial institution has no reserves, the financial base was 3.661 trillion pesos, and the official change price in March 2022 was 110 pesos per greenback. Because of this Argentina would want a $33 billion {dollars} mortgage to not devalue[7] (assuming no further reserves for banking system liquidity). In a really optimistic state of affairs, Argentina receives a mortgage of $12 billion (utilizing $5 billion as a reserve for the banking system and $7 billion to dollarize the financial base), the change price of the dollarization can be at 523 pesos per greenback[8]. A devaluation of 375% can have worse penalties than the issues dollarization is meant to resolve. Argentine salaries in U.S. {dollars} can be among the many lowest globally, and poverty would rise to unprecedented ranges. Not by likelihood, some analysts say that hyperinflation must come earlier than any dollarization plan is perhaps put into motion.

Backside line

Paul Krugman wrote a ebook titled Arguing with Zombies: Economics, Politics, and the Battle for a Higher Future, with the purpose of understanding why some concepts hold reappearing despite the fact that they’ve been proved incorrect empirically and theoretically.

Dollarization of Argentina is a ‘zombie’ financial concept that reappears at occasions of uncertainty. It has been confirmed inefficient as an answer to structural issues. Furthermore, it creates new issues as advanced as the unique ones. As soon as dollarization is pursued, there isn’t a straightforward means out. Subsequently, governments should suppose correctly earlier than selecting such a drastic financial regime change.

Any dollarization proposal has beneath a trade-off between the quick time period and long run. Whereas it has the advantage of lowering inflation virtually instantaneously, it will have vital and everlasting penalties in the long term, as we’ve proven.

The rationale these concepts hold reappearing in Argentina is a mix of nostalgia and short-term reminiscences. Some folks yearn for these years when the forex board introduced excessive returns in {dollars}. The concept that the clock could be turned again to revive a previous that when momentarily existed is just not solely an Argentine phenomenon; it’s also why nationalism has reemerged, and populist leaders have gained energy worldwide. Paradoxically, the proposal for dollarization in Argentina would imply an abdication of nationwide self-determination.

Bibliography:

× Burns, Nick (2022). “Javier Milei’s Sudden Rise”, Americas Quarterly, April 11.

× Cachanosky, N. (2022): “Dolarización: algunas lecciones Internacionales”, INFOBAE, April 10..

× Calvo, Guillermo A., (1999) “On Dollarization,” mimeo, College of Maryland, April.

× Canuto, Otaviano, (2021): “Climbing a excessive ladder: growth within the international financial system”, Coverage Heart for the New South.

× Ize, A. y A. Powell (2004): “Prudential Responses to De Facto Dollarization”. IMF Working Paper 04/66 (Washington, D.C. Fondo Monetario Internacional). Journal of Coverage Reform, vol. 8, n.º 4 (2005), pp. 241-62

× Jameson, Okay. P. (2003). Dollarization in Latin America: Wave of the Future or Flight to the Previous? Journal of Financial Points, 37(3), 643–663

× Krugman (2020) Arguing with Zombies : Economics, Politics, and the Battle for a Higher America. Norton & Firm, Included,

× Levy Yeyati, E., and F. Sturzenegger (2002): “Dollarization: A Primer,” in Dollarization, Levy Yeyati, E. and F. Sturzenegger, eds., MIT Press.

× Levy Yeyati, E. (2012). Stability de la dolarización en El Salvador. Elypsis / UTDT / Brookings.

× Levy Yeyati, (2021). “Monetary dollarization and de-dollarization within the new millennium,” Division of Economics Working Papers wp_gob_2021_02, Universidad Torcuato Di Tella.

× Mundell, Robert (1961). A Idea of Optimum Forex Areas. The American Financial Overview, Vol. 51, No. 4 pp. 657-665

× Schuler & Hanke (2001). “How one can dollarize in Argentina now”. Cato Institute Net paper

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

Sebastian Carranza is a pupil on the MA in Worldwide Financial Coverage at GWU. He holds a BA in Economics on the College of Buenos Aires, and MA in Worldwide Research at College Torcuato Di Tella.

[1] Time period additionally used to explain economies with cash demand for 2 currencies.

[2] Economists perceive seigniorage as a type of inflation tax, returning assets to the forex issuer. Issuing new forex, moderately than accumulating taxes paid with current cash, is taken into account a tax on holders of current forex.

[3] Inflation is a regressive phenomenon which means it impacts comparatively extra to those that have the much less. Because of this ceteris paribus, dollarization is perhaps seen as a progressive coverage.

[4] With just a few exceptions akin to Peru, Chile, Colombia, and many others.

[5] Leaving apart all of the difficulties to cut back spending, Argentina’s authorities expenditure is principally with pensions and subsidies to vitality and transport. Unpopular structural reforms stay obligatory regardless of dangers of political instability.

[6] Treasury bonds: “Lecops”; Buenos Aires bonds: “Patacones”; Cordoba bonds: “Lecor”, and many others

[7] It’s useful to recollect Argentina faces very excessive premium dangers and a program with the IMF that merely rolls-over earlier debt with the establishment.

[8] and that is simply to soak up M1. If we take into account all of the liabilities the devaluation would have to be greater than double.

[ad_2]