[ad_1]

The “World Financial Outlook” report launched by the Worldwide Financial Fund (IMF) on April nineteenth depicted a worsening within the international financial situation for 2022: decrease financial progress and better inflation, in comparison with the January projections. As director-general Kristalina Georgieva had mentioned within the earlier week, the warfare in Ukraine represented a “substantial setback” for the worldwide financial restoration.

World inflation and progress deceleration

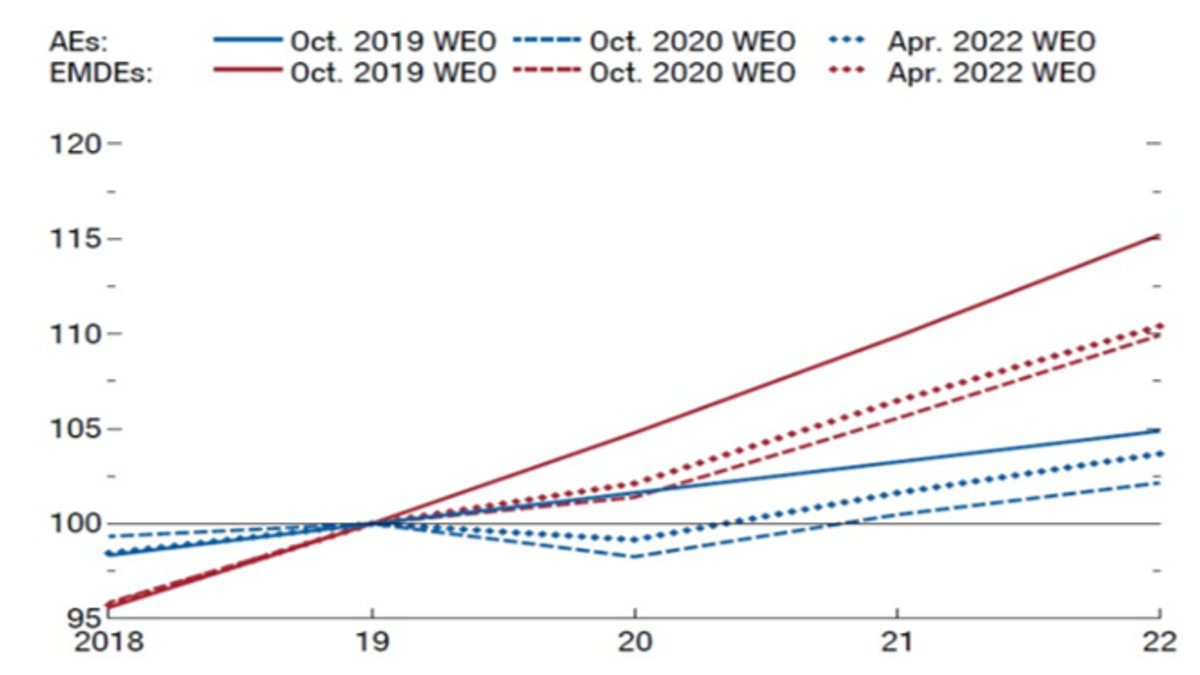

The IMF pinned the worldwide slowdown on Russia’s invasion of Ukraine. It projected a pointy decline in 2022 financial progress worldwide because the warfare drives up power costs and stumbles on pandemic financial recoveries. Now, the IMF forecasts international progress at 3.6% for the yr, decrease than its 4.4% forecast issued in January. Past 2023, it expects progress to slip all the way down to about 3.3%, whereas progress in 2021 was about 6.1% (IMF, 2022). Determine 1 depicts the reviewed paths forecast by the IMF for potential GDP beginning at October 2019.

Determine 1 – Potential GDP (Index, 2019 = 100)

Supply: IMF (2022a).

Observe: Potential actual GDP projections listed to 2019 values. Every line displays a distinct classic of World Financial Outlook (WEO) projections. AEs = superior economies; EMDEs = rising market and growing economies.

The evaluation pairs that of the World Financial institution, which in the day before today slashed its personal international progress forecasts from 4.1% to three.2%. One should take into account that the IMF makes use of Buying-Parity-Parity-adjusted change charges in including GDPs, whereas World Financial institution makes use of nominal change charges. Subsequently, the load of non-advanced nations tends to be greater within the IMF’s international progress figures.

The post-pandemic international financial restoration was already slowing when the Russian invasion of Ukraine triggered new commodity value shocks, on the identical time inflicting a brand new wave of restrictions in provide chains (Canuto, 2022).

The IMF additionally factors out the consequences of financial tightening and monetary market volatility. Even earlier than the warfare, inflation had risen considerably, and lots of central banks began tightening financial coverage. This contributed to a fast improve in nominal rates of interest throughout superior economic system sovereign debtors. Within the months forward, coverage charges are usually anticipated to rise additional, and record-high central financial institution stability sheets will start to unwind, most notably in superior economies. Determine 2 exhibits the WEO forecasts for primary actual rates of interest in superior economies and rising market economies.

Determine 2 – Actual Coverage Charges (%)

Supply: IMF (2022a).

Observe: Euro space’s projection half is estimated by utilizing 16 particular person euro space nations’ projections. Different AEs and different EMs comprise 12 and 10 economies, respectively. AEs = superior economies; EMs = rising markets.

The expectation of tighter financial insurance policies follows the evaluation upward in inflation forecasts. With the impression of the warfare in Ukraine and broadening of value pressures, inflation is predicted to stay elevated for longer than beforehand forecast. The battle is prone to have a protracted impression on commodity costs, affecting oil and fuel costs extra severely in 2022 and meals costs nicely into 2023 (due to the lagged impression from the harvest in 2022). Even with the anticipated will increase in coverage charges, given the outlook for inflation, short-term actual rates of interest on the finish of 2022 are prone to nonetheless be destructive. How excessive will they must go is a wide-open query.

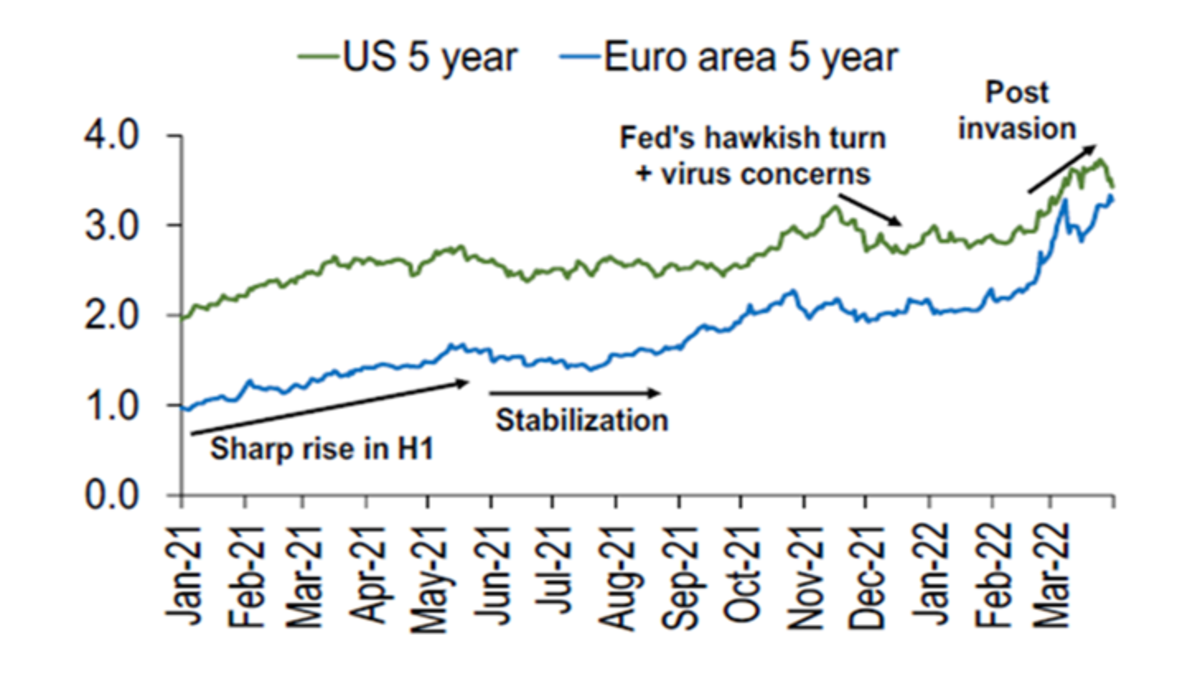

The dilemma confronted by central bankers between accepting inflation or slowing demand was made worse by the shocks triggered by the warfare. In March, US inflation reached 8.5%, its highest annualized degree in 40 years. Inflation expectations have gone up on each U.S. and European sides of the Atlantic, as measured by corresponding breakeven 5-year rates of interest (Determine 3).

Determine 3 – Inflation Expectations Rising (Inflation breakeven, %)

Supply: IMF (2022b).

Chapter 2 of the IMF (2022a) calls consideration to how the document rise in personal debt in recent times may have an effect on the financial restoration, even when the drag on progress tends to differ throughout nations and inside them.

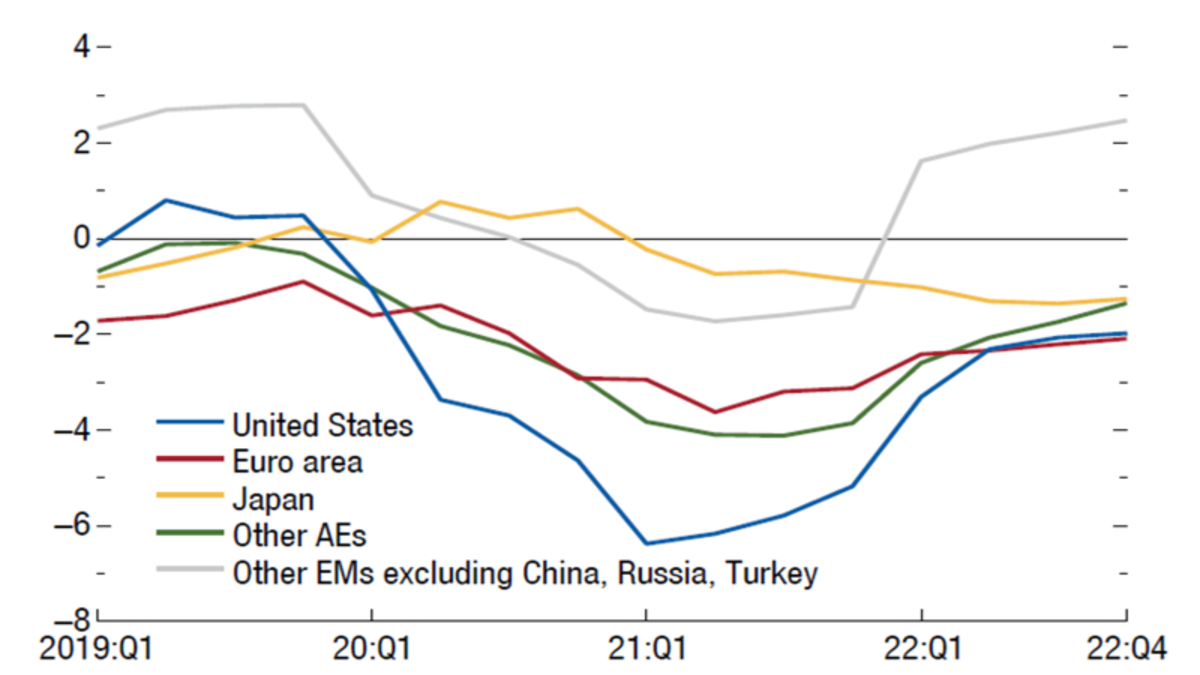

China’s ‘zero-COVID’ coverage, in the meantime, has additionally introduced provide shocks and provide chain disruptions. Chinese language financial information out on April 18th revealed that its economic system has felt the impression as the federal government aggressively fights the worst outbreak of COVID to this point on the mainland. Industrial manufacturing decelerated sharply in March, as did funding within the home actual property sector, which has been a key driver of the nation’s progress (Determine 4). Because it stays an export large and an important cog in international provide chains, Chinese language manufacturing unit shutdowns and logistical disruptions will amplify international supply-chain disruptions and value pressures.

Determine 4 – China: industrial manufacturing and new building

Supply: Axios (2022). China’s economic system is sputtering, April 19.

Rising monetary stability dangers

The World Monetary Stability Report additionally launched by the IMF on April 19th addresses one other dilemma: accepting inflation or dangers of economic instability arising from sharp rises in rates of interest. Necessary element: the 2 dilemmas intersect. Within the case of the US, many analysts consider the Fed is late on its price adjustment route. If it finds itself pressured into a lot steeper rises forward, the bumps on high-leverage personal company buildings will likely be substantial.

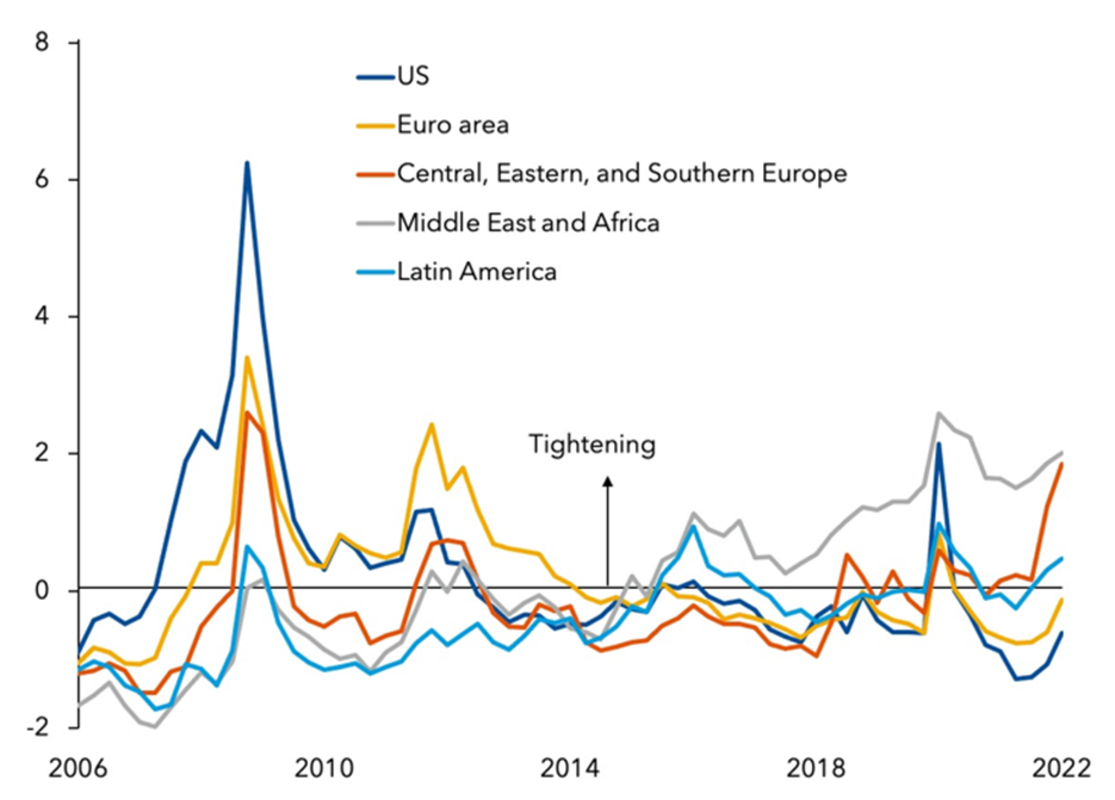

Because the starting of the yr, monetary situations have tightened considerably throughout a lot of the world, notably in Japanese Europe (Determine 5). Given rising inflation, the interest-rate evolution that we noticed on Determine 2 have led to a tightening in superior economies within the weeks following the Russian invasion of Ukraine. Even with that tightening, monetary situations are near historic averages, and actual charges stay accommodative in most nations.

Tighter monetary situations assist to sluggish demand, in addition to to forestall a lack of anchoring of inflation expectations and, subsequently, anticipation of continued value will increase sooner or later changing into the norm. Many central banks could have to maneuver additional and quicker than what’s at present priced in markets to include inflation. This might carry coverage charges above impartial ranges (a “impartial” degree is one at which financial coverage is neither accommodative nor restrictive and is in step with the economic system sustaining full employment and secure inflation). That is prone to result in even tighter international monetary situations.

Determine 5 – Monetary situations

Supply: IMF (2022b).

Rising economies: frequent elements, however differentiated impacts

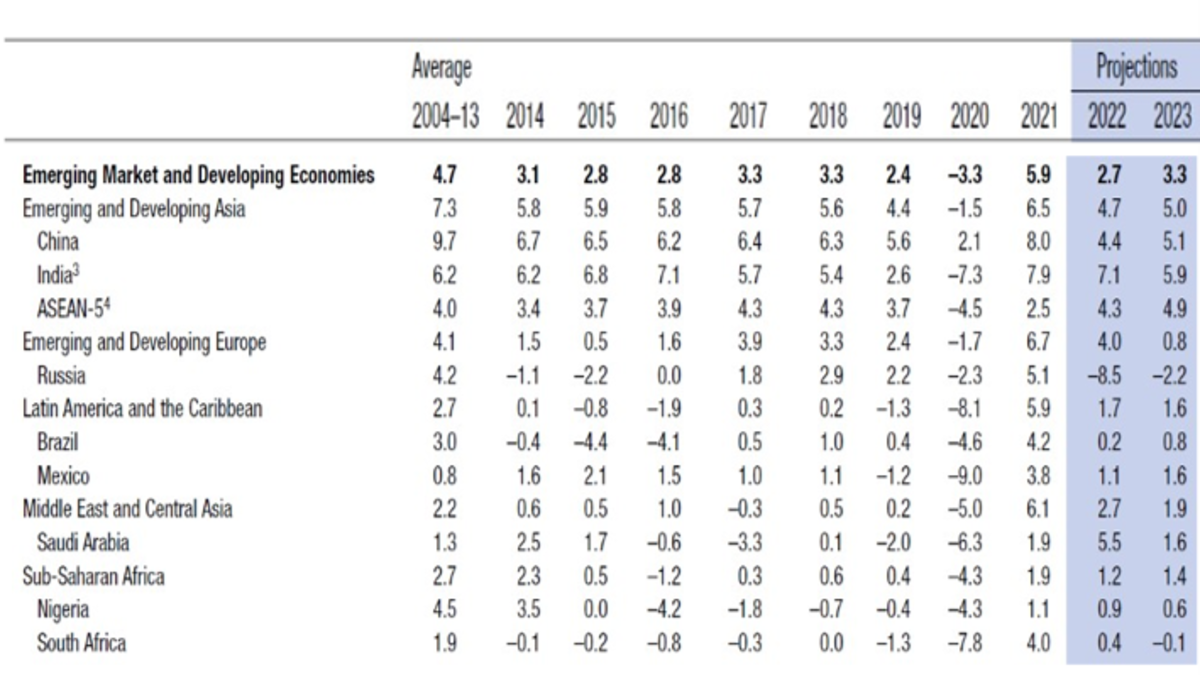

The IMF forecast for the rising market and growing Economies (EMDE) cluster was additionally downgraded as in comparison with January projections. On this case, nonetheless, with a lot better heterogeneity. From the inflationary spike, however, nobody escapes, bringing with it stress to boost rates of interest.

Desk 1 – EMDE Actual per Capita Output

(Annual % change; in fixed 2017 worldwide {dollars} at buying energy parity)

Supply: IMF (2022a).

In EMDE, a number of central banks have not too long ago tightened financial insurance policies, including to those who had already began to take action in 2021. Expectations of tighter coverage in superior economies and worries in regards to the warfare have contributed to monetary market volatility and threat repricing for EMDE. One exception is China, the place inflation stays low, and the central financial institution reduce coverage charges in January 2022 to assist the restoration.

EMDEs face a typical set of exterior shocks: rising power and meals costs, aggravated by Russia’s invasion of Ukraine (Determine 6); tightening in international monetary situations attributable to the prospect of sharper rate of interest hikes and anticipation of “quantitative tightening” (as we noticed in Determine 5); and return of restrictions on mobility in China, on account of the Covid zero coverage, resulting in hunch in progress and weakening one of many most important progress drivers for EMDE (Determine 4 above). Fiscal stimulus in China factors in the other way, however there are doubts in regards to the sustainability of this coverage.

Determine 6 – Commodity costs: greenback value of S&P GSCI international commodity market index

Supply: Sandbu (2022).

Nevertheless, the impacts of frequent shocks have been heterogeneous. 4 subgroups might be distinguished amongst EMDE.

First, in fact, Ukraine struggling the destruction of the warfare, Russia underneath sanctions and the opposite economies within the area built-in to them. Along with greater inflation, Russia will expertise a recession worse than the 1998 disaster and the worldwide monetary disaster in 2008, albeit, paradoxically, with the best present account surplus within the final 20 years.

In Russia, the sanctions and the impairment of home monetary intermediation have led to giant will increase in its sovereign and credit score default swap spreads. Rising market economies within the area, in addition to Caucasus, Central Asia, and North Africa, have additionally seen their sovereign spreads widen. The IMF forecasts GDP declines in Russia of 8.5% and a couple of.2%, respectively, in 2022 and 2023 (Desk 1).

A second group of EMDE is comprised by commodity exporters (excluding Russia), that are benefiting from extra favorable phrases of commerce. Whereas this isn’t sufficient to totally defend them, strengthened public revenues present fiscal leeway for measures to clean the rise in home power costs. Bigger present account balances can even cushion the impact of tightening international monetary situations. International locations which can be extra superior within the financial tightening cycle, reminiscent of Brazil, are benefiting from the appreciation of their currencies. Commodity exporters – excluding Russia – was the one group of nations for which the IMF lifted its progress prospects for 2022 as in comparison with January projections.

Nonetheless, the inflation problem has additionally risen for them. Due to the pandemic and the warfare in Ukraine, the inflation price in Latin America’s largest economies – Brazil, Chile, Colombia, Mexico, and Peru – has been the best inflation in 15 years (Appendino et al, 2022). The load of import and commodity costs on Latin American inflation is larger than that of superior economies.

A 3rd group corresponds to commodity importers, for whom manufacturing exports weigh, which can be struggling each the impression of upper power and meals costs and the slowdown in international progress. Slower progress, greater inflation, deteriorating public accounts and decrease present account balances are forecast.

The fourth subgroup is that of growing economies grappling with the indebtedness inherited from the pandemic. Greater debt and fewer favorable international monetary situations are already making it troublesome to roll over exterior debt service and finance present account deficits. Right here, the quantity of the present name by multilateral establishments —World Financial institution and IMF— for them to contemplate the potential for debt restructuring processes with exterior collectors will get even louder.

A wave of EMDE debt crises appears to be coming, remarks Estevão (2022), from the World Financial institution:

“On the eve of the warfare, lots of them had been already on shaky floor. Following up on a decade of rising debt, the COVID-19 disaster expanded whole indebtedness to a 50-year excessive—the equal of greater than 250 % of presidency revenues. Near 60 % of the poorest nations had been already in debt misery or at excessive threat of it. (…) The Ukraine warfare instantly darkened the outlook for a lot of growing nations which can be main commodity importers or extremely depending on tourism or remittances. (…) Over the following 12 months, as many as a dozen growing economies may show unable to service their debt.”

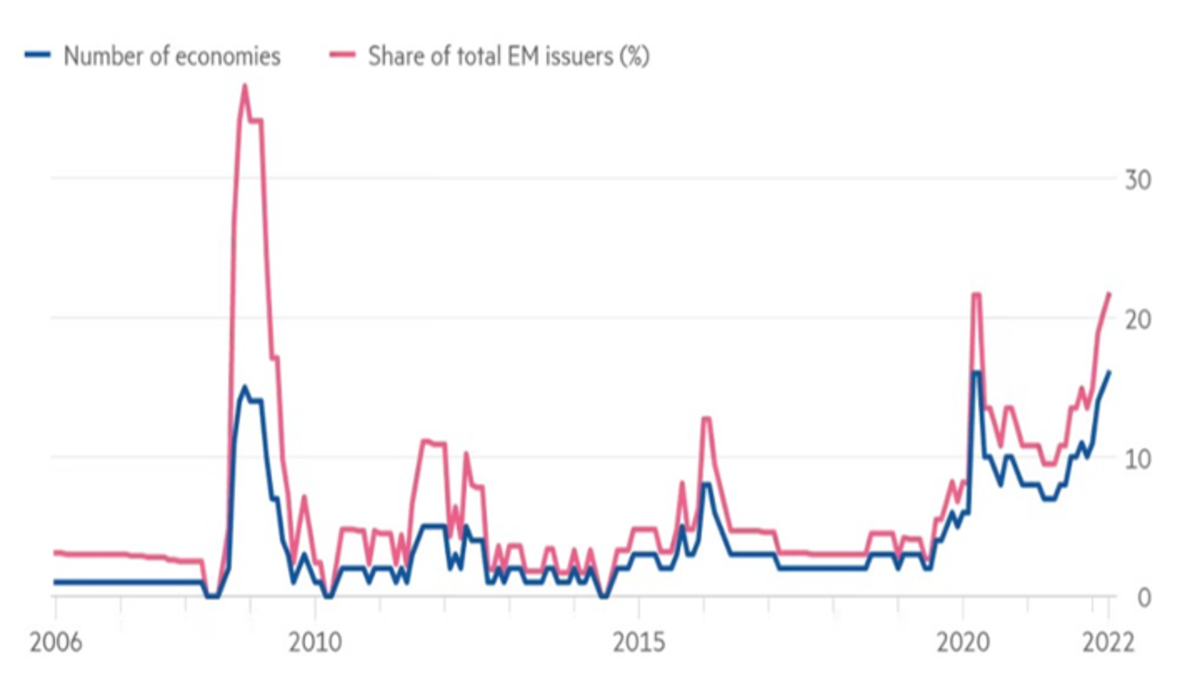

Ranges of misery are susceptible to rising a lot greater if central banks in superior economies really feel compelled to maneuver too abruptly or aggressively to unwind the financial coverage stimulus injected for the reason that onset of the pandemic, as a response to the inflation surge forecast by the IMF.

Determine 7 – Distressed EMDE hard-currency sovereign issuers

Supply: IMF; Smith and Platt (2022).

Observe: distressed: spreads over US Treasuries above 1,000 foundation factors

Backside line

The warfare in Ukraine and China’s progress deceleration have introduced a typical set of exterior shocks for EMDE. In addition to rising power and meals costs and tightening in international monetary situations attributable to the prospect of sharper rate of interest hikes and anticipation of “quantitative tightening”, the return of restrictions on mobility in China, on account of the Covid zero coverage.

The impacts of these frequent shocks on EMDE have been heterogeneous, with some commodity exporters even barely enhancing GDP efficiency, whereas economies underneath debt misery will face an much more difficult setting. What’s plain is that the expansion prospects and the phrases of the coverage trade-off between financial exercise and inflation have deteriorated, in addition to looming dangers related to tightening international monetary situations.

References

Appendino, M.; Goldfajn, I.; and Pienknagura, P. (2022). Latin America Hit By One Inflationary Shock On High of One other, IMF Weblog, April 15.

Canuto, O. (2022). Conflict in Ukraine and Dangers of Stagflation, Coverage Heart for the New South, March.

Estevão, M. (2022). Are we prepared for the approaching spate of debt crises? Voices – Views on growth, World Financial institution, March 28.

IMF – Worldwide Financial Fund (2022a). World Financial Outlook, April.

IMF – Worldwide Financial Fund (2022b). World Monetary Stability Report, April.

Sandbu, M. (2022). Central bankers ought to assume twice earlier than urgent the brake even more durable, Monetary Occasions, April 19.

Smith, C. and Platt, E. (2022). Rising markets threat monetary misery as charges start to rise, IMF warns, Monetary Occasions, April 19.

Coverage Heart for the New South

[ad_2]