[ad_1]

TABLE OF CONTENTS

- Navigating the “Wash Sale” rule

- The Betterment resolution

- Tax loss harvesting mannequin calibration

- Greatest practices for TLH

- How we calculate the worth of tax loss harvesting

- Your customized Estimated Tax Financial savings instrument

- Conclusion

There are various methods to get your investments to work more durable for you— diversification, draw back threat administration, and an acceptable mixture of asset lessons tailor-made to your advisable allocation. Betterment does this robotically through its ETF portfolios.

However there’s one other approach that will help you get extra out of your portfolio—utilizing funding losses to enhance your after-tax returns with a technique referred to as tax loss harvesting. On this article, we introduce Betterment’s tax loss harvesting (TLH): a classy, absolutely automated instrument that Betterment clients can select to allow.

Betterment’s tax loss harvesting service scans portfolios repeatedly for alternatives (non permanent dips that outcome from market volatility) for alternatives to understand losses which might be priceless come tax time. Whereas the idea of tax loss harvesting just isn’t new for rich traders, tax loss harvesting makes use of a variety of improvements that typical implementations could lack. It takes a holistic method to tax-efficiency, looking for to optimize user-initiated transactions along with including worth by way of automated exercise, akin to rebalances.

What’s tax loss harvesting?

Capital losses can decrease your tax invoice by offsetting positive aspects, however the one strategy to understand a loss is to promote the depreciated asset. Nevertheless, in a well-allocated portfolio, every asset performs an important position in offering a chunk of whole market publicity. For that cause, an investor shouldn’t need to surrender potential anticipated returns related to every asset simply to understand a loss.

At its most elementary stage, tax loss harvesting is promoting a safety that has skilled a loss—after which shopping for a correlated asset (i.e. one that gives related publicity) to exchange it. The technique has two advantages: it permits the investor to “harvest” a priceless loss, and it retains the portfolio balanced on the desired allocation.

How can it decrease your tax invoice?

Capital losses can be utilized to offset capital positive aspects you’ve realized in different transactions over the course of a yr—positive aspects on which you’d in any other case owe tax. Then, if there are losses left over (or if there have been no positive aspects to offset), you’ll be able to offset as much as $3,000 of unusual earnings for the yr. If any losses nonetheless stay, they are often carried ahead indefinitely.

Tax loss harvesting is primarily a tax deferral technique, and its profit relies upon fully on particular person circumstances. Over the long term, it could add worth by way of some mixture of those distinct advantages that it seeks to supply:

- Tax deferral: Losses harvested can be utilized to offset unavoidable positive aspects within the portfolio, or capital positive aspects elsewhere (e.g., from promoting actual property), deferring the tax owed. Financial savings which are invested could develop, assuming a conservative development charge of 5% over a 10-year interval, a greenback of tax deferred can be value $1.63. Even after belatedly parting with the greenback, and paying tax on the $0.63 of development, you’re forward.

- Pushing capital positive aspects right into a decrease tax charge: If you happen to’ve realized short-term capital positive aspects (STCG) this yr, they’ll usually be taxed at your highest charge. Nevertheless, when you’ve harvested losses to offset them, the corresponding achieve you owe sooner or later might be long-term capital achieve (LTCG). You’ve successfully turned a achieve that will have been taxed as much as 50% right now right into a achieve that will probably be taxed extra flippantly sooner or later (as much as 30%).

- Changing unusual earnings into long-term capital positive aspects: A variation on the above: offsetting as much as $3,000 out of your unusual earnings shields that quantity out of your prime marginal charge, however the offsetting future achieve will seemingly be taxed on the LTCG charge.

- Everlasting tax avoidance in sure circumstances: tax loss harvesting gives advantages now in trade for rising built-in positive aspects, topic to tax later. Nevertheless, beneath sure circumstances (charitable donation, bequest to heirs), these positive aspects could keep away from taxation fully.

Navigating the “Wash Sale” rule

Abstract: Wash sale rule administration is on the core of any tax loss harvesting technique. Unsophisticated approaches can detract from the worth of the harvest or place constraints on buyer money flows with the intention to perform.

At a excessive stage, the so-called “Wash Sale” rule disallows a loss from promoting a safety if a “considerably similar” safety is bought 30 days after or earlier than the sale. The rationale is {that a} taxpayer shouldn’t get pleasure from the good thing about deducting a loss if they didn’t really eliminate the safety.

The wash sale rule applies not simply to conditions when a “considerably similar” buy is made in the identical account, but in addition when the acquisition is made within the particular person’s IRA/401(ok) account, and even in a partner’s account. This broad utility of the wash sale rule seeks to make sure that traders can not make the most of nominally totally different accounts to keep up their possession, and nonetheless profit from the loss.

A wash sale involving an IRA/401(ok) account is especially unfavorable. Usually, a “washed” loss is postponed till the substitute is bought, but when the substitute is bought in an IRA/401(ok) account, the loss is completely disallowed.

If not managed accurately, wash gross sales can undermine tax loss harvesting. Dealing with proceeds from the harvest just isn’t the only real concern—any deposits made within the following 30 days (whether or not into the identical account, or into the person’s IRA/401(ok)) additionally have to be allotted with care.

Minimizing the wash

The best strategy to keep away from triggering a wash sale is to keep away from buying any safety in any respect for the 30 days following the harvest, conserving the proceeds (and any inflows throughout that interval) in money. This method, nonetheless, would systematically hold a portion of the portfolio out of the market. Over the long run, this “money drag” might harm the portfolio’s efficiency.

Extra superior methods repurchase an asset with related publicity to the harvested safety that isn’t “considerably similar” for functions of the wash sale rule. Within the case of a person inventory, it’s clear that repurchasing inventory of that very same firm would violate the rule. Much less clear is the therapy of two index funds from totally different issuers (e.g., Vanguard and Schwab) that monitor the identical index. Whereas the IRS has not issued any steering to recommend that such two funds are “considerably similar,” a extra conservative method when coping with an index fund portfolio can be to repurchase a fund whose efficiency correlates carefully with that of the harvested fund, however tracks a distinct index.

Tax loss harvesting is mostly designed round this index-based logic and customarily seeks to cut back wash gross sales, though it can not keep away from potential wash gross sales arising from transactions in tickers that monitor the identical index the place one of many tickers just isn’t at the moment a main, secondary, or tertiary ticker (as these phrases are outlined on this white paper). This example might come up, for instance, when different tickers are transferred to Betterment or the place they have been beforehand a main, secondary, or tertiary ticker. Moreover, for some portfolios constructed by third events (e.g., Vanguard, Blackrock, or Goldman Sachs), sure secondary and tertiary tickers monitor the identical index. Sure asset lessons in portfolios constructed by third events (e.g., Vanguard, Blackrock, or Goldman Sachs) wouldn’t have tertiary tickers, such that completely disallowed losses might happen if there have been overlapping holdings in taxable and tax-advantaged accounts. Betterment’s TLH characteristic may additionally allow wash gross sales the place the anticipated tax advantage of the general harvest transaction sufficiently outweighs the affect of anticipated washed losses .

Deciding on a viable substitute safety is only one piece of the accounting and optimization puzzle. Manually implementing a tax loss harvesting technique is possible with a handful of securities, little to no money flows, and rare harvests. Belongings could nonetheless dip in worth however probably recuperate by the top of the yr, subsequently annual methods or rare harvests could go away many losses on the desk. The wash sale administration and tax lot accounting essential to assist extra frequent harvesting rapidly turns into overwhelming in a multi-asset portfolio—particularly with common deposits, dividends, and rebalancing.

An efficient loss harvesting algorithm ought to have the ability to maximize harvesting alternatives throughout a full vary of volatility eventualities, with out sacrificing the investor’s world asset allocation. It ought to reinvest harvest proceeds into correlated alternate property, all whereas dealing with unexpected money inflows from the investor with out ever resorting to money positions. It also needs to have the ability to monitor every tax lot individually, harvesting particular person tons at an opportune time, which can rely on the volatility of the asset. Tax loss harvesting was created as a result of no obtainable implementations appeared to unravel all of those issues.

Current methods and their limitations

Each tax loss harvesting technique shares the identical primary objective: to maximise a portfolio’s after-tax returns by realizing built-in losses whereas minimizing the unfavourable affect of wash gross sales.

Approaches to tax loss harvesting differ primarily in how they deal with the proceeds of the harvest to keep away from a wash sale. Under are the three methods generally employed by guide and algorithmic implementations.

After promoting a safety that has skilled a loss, current methods would seemingly have you ever:

|

Current technique |

Drawback |

|

Delay reinvesting the proceeds of a harvest for 30 days, thereby making certain that the repurchase is not going to set off a wash sale. |

Whereas it’s the best technique to implement, it has a serious disadvantage: no market publicity—additionally referred to as money drag. Money drag hurts portfolio returns over the long run, and will offset any potential profit from tax loss harvesting. |

|

Reallocate the money into a number of fully totally different asset lessons within the portfolio. |

This technique throws off an investor’s desired asset allocation. Moreover, such purchases could block different harvests over the following 30 days by establishing potential wash gross sales in these different asset lessons. |

|

Swap again to authentic safety after 30 days from the substitute safety. Widespread guide method, additionally utilized by some automated investing providers. |

A switchback can set off short-term capital positive aspects when promoting the substitute safety, lowering the tax advantage of the harvest. Even worse, this technique can go away an investor owing extra tax than if it did nothing. |

The hazards of switchbacks

Within the 30 days main as much as the switchback, two issues can occur: the substitute safety can drop additional, or go up. If it goes down, the switchback will understand a further loss. Nevertheless, if it goes up, which is what any asset with a constructive anticipated return is anticipated to do over any given interval, the switchback will understand short-term capital positive aspects (STCG)—kryptonite to a tax-efficient portfolio administration technique.

An try and mitigate this threat might be setting the next threshold based mostly on volatility of the asset class—solely harvesting when the loss is so deep that the asset is unlikely to completely recuperate in 30 days. In fact, there’s nonetheless no assure that it’s going to not, and the worth paid for this buffer is that your lower-yielding harvests can even be much less frequent than they might be with a extra refined technique.

Examples of unfavourable tax arbitrage

Detrimental tax arbitrage with automated 30-day switchback

An automated 30-day switchback can destroy the worth of the harvested loss, and even improve tax owed, somewhat than cut back it. A considerable dip presents a wonderful alternative to promote a whole place and harvest a long-term loss. Proceeds will then be re-invested in a extremely correlated substitute (monitoring a distinct index). 30 days after the sale, the dip proved non permanent and the asset class greater than recovered. The switchback sale leads to STCG in extra of the loss that was harvested, and really leaves the investor owing tax, whereas with out the harvest, they might have owed nothing.

Attributable to a technical nuance in the way in which positive aspects and losses are netted, the 30- day switchback can lead to unfavourable tax arbitrage, by successfully pushing current positive aspects into the next tax charge.

When including up positive aspects and losses for the yr, the principles require netting of like towards like first. If any long-term capital achieve (LTCG) is current for the yr, it’s essential to web a long-term capital loss (LTCL) towards that first, and solely then towards any STCG.

Detrimental tax arbitrage when unrelated long-term positive aspects are current

Now let’s assume the taxpayer realized a LTCG. If no harvest takes place, the investor will owe tax on the achieve on the decrease LTCG charge. Nevertheless, when you add the LTCL harvest and STCG switchback trades, the principles now require that the harvested LTCL is utilized first towards the unrelated LTCG. The harvested LTCL will get used up fully, exposing the complete STCG from the switchback as taxable. As an alternative of sheltering the extremely taxed achieve on the switchback, the harvested loss obtained used up sheltering a lower-taxed achieve, creating far larger tax legal responsibility than if no harvest had taken place.

Within the presence of unrelated transactions, unsophisticated harvesting can successfully convert current LTCG into STCG. Some traders repeatedly generate vital LTCG (as an example, by steadily diversifying out of a extremely appreciated place in a single inventory). It’s these traders, actually, who would profit probably the most from efficient tax loss harvesting.

Detrimental tax arbitrage with dividends

Detrimental tax arbitrage can lead to reference to dividend funds. If sure circumstances are met, some ETF distributions are handled as “certified dividends”, taxed at decrease charges. One situation is holding the safety for greater than 60 days. If the dividend is paid whereas the place is within the substitute safety, it is not going to get this favorable therapy: beneath a inflexible 30-day switchback, the situation can by no means be met. Because of this, as much as 20% of the dividend is misplaced to tax (the distinction between the upper and decrease charge).

The Betterment resolution

Abstract: Betterment’s tax loss harvesting approaches tax-efficiency holistically, looking for to optimize transactions, together with buyer exercise.

The advantages tax loss harvesting seeks to ship, embody:

- No publicity to short-term capital positive aspects in an try to reap losses. By our proprietary Parallel Place Administration (PPM) system, a dual-security asset class method enforces choice for one safety with out needlessly triggering capital positive aspects in an try to reap losses, all with out placing constraints on buyer money flows.

- No unfavourable tax arbitrage traps related to much less refined harvesting methods (e.g., 30-day switchback), making tax loss harvesting particularly fitted to these producing massive long-term capital positive aspects on an ongoing foundation.

- Zero money drag. With fractional shares and seamless dealing with of all inflows throughout wash sale home windows, each greenback of your ETF portfolio is invested.

- Tax loss preservation logic prolonged to user-realized losses, not simply harvested losses, robotically defending each from the wash sale rule. In brief, person withdrawals all the time promote any losses first.

- No disallowed losses by way of overlap with a Betterment IRA/401(ok). We use a tertiary ticker system to eradicate the potential for completely disallowed losses triggered by subsequent IRA/401(ok) exercise.² This makes TLH best for individuals who spend money on each taxable and tax-advantaged accounts.

- Harvests additionally take the chance to rebalance throughout all asset lessons, somewhat than re-invest solely throughout the identical asset class. This additional reduces the necessity to rebalance throughout unstable stretches, which suggests fewer realized positive aspects, and better tax alpha.

By these improvements, tax loss harvesting creates vital worth over manually-serviced or much less refined algorithmic implementations. Tax loss harvesting is accessible to traders —absolutely automated, efficient, and at no further value.

Parallel securities

To make sure that every asset class is supported by optimum securities in each main and alternate (secondary) positions, we screened by expense ratio, liquidity (bid-ask unfold), monitoring error vs. benchmark, and most significantly, covariance of the alternate with the first.1

Whereas there are small value variations between the first and alternate securities, the price of unfavourable tax arbitrage from tax-agnostic switching vastly outweighs the price of sustaining a twin place inside an asset class.

Tax loss harvesting contains a particular mechanism for coordination with IRAs/401(ok)s that requires us to select a 3rd (tertiary) safety in every harvestable asset class (besides in municipal bonds, which aren’t within the IRA/401(ok) portfolio). Whereas these have the next value than the first and alternate, they don’t seem to be anticipated to be utilized usually, and even then, for brief durations (extra beneath in IRA/401(ok) safety).

Parallel place administration

As demonstrated, the unconditional 30-day switchback to the first safety is problematic for a variety of causes. To repair these issues, we engineered a platform to assist tax loss harvesting, which seeks to tax-optimize person and system-initiated transactions: the Parallel Place Administration (PPM) system.

PPM permits every asset class to comprise a main safety to signify the specified publicity whereas sustaining alternate and tertiary securities which are carefully correlated securities, ought to that lead to a greater after-tax consequence.

PPM gives a number of enhancements over the switchback technique. First, pointless positive aspects are minimized. Second, the parallel safety (might be main or alternate) serves as a protected harbor to cut back potential wash gross sales—not simply from harvest proceeds, however any money inflows. Third, the mechanism seeks to guard not simply harvested losses, however losses realized by the shopper as effectively.

PPM not solely facilitates efficient alternatives for tax loss harvesting, but in addition extends most tax-efficiency to customer-initiated transactions. Each buyer withdrawal is a possible harvest (losses are bought first). And each buyer deposit and dividend is routed to the parallel place that would cut back wash gross sales, whereas shoring up the goal allocation.

PPM has a choice for the first safety when rebalancing and for all money circulate occasions—however all the time topic to tax issues. That is how PPM behaves beneath varied circumstances:

|

Transaction |

PPM conduct |

|

Withdrawals and gross sales from rebalancing |

Gross sales default out of the alternate place (if such a place exists), however not on the expense of triggering STCG—in that case, PPM will promote a lot of the first safety first. Rebalancing will try and cease in need of realizing STCG. Taxable positive aspects are minimized at each resolution level—STCG tax tons are the final to be bought on a person withdrawal. |

|

Deposits, buys from rebalancing, and dividend reinvestments |

PPM directs inflows to underweight asset lessons, and inside every asset class, into the first, until doing so incurs larger wash sale prices than shopping for the alternate. |

|

Harvest occasions |

TLH harvests can come out of the first into the alternate, or vice versa, relying on which harvest has a larger anticipated worth. After an preliminary harvest, it might make sense sooner or later to reap again into the first, to reap extra of the remaining main into the alternate, or to do nothing. |

Wash sale administration

Managing money flows throughout each taxable and IRA/401(ok) accounts with out washing realized losses is a posh drawback.

Tax loss harvesting operates with out constraining the way in which that clients desire contributing to their portfolios, and with out resorting to money positions. With the good thing about parallel positions, Betterment weighs wash sale implications of deposits,withdrawals and dividend reinvestment This technique protects not simply harvested losses, but in addition losses realized by way of withdrawals.

Minimizing wash sale by way of tertiary tickers in IRA/401(ok)

As a result of IRA/401(ok) wash gross sales are significantly unfavorable—the loss is disallowed completely—tax loss harvesting ensures that no loss realized within the taxable account is washed by a subsequent deposit right into a Betterment IRA/401(ok) with a tertiary ticker system in IRA/401(Ok) and no harvesting is finished in IRA/401(ok).

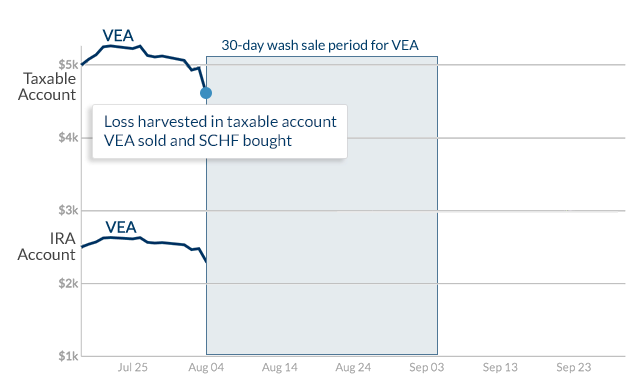

Let’s take a look at an instance of how tax loss harvesting handles a probably disruptive IRA influx with a tertiary ticker when there are realized losses to guard, utilizing actual market information for a Developed Markets asset class.

The client begins with a place in VEA, the first safety, in each the taxable and IRA accounts. We harvest a loss by promoting the complete taxable place, after which repurchasing the alternate safety, SCHF.

Loss harvested in VEA

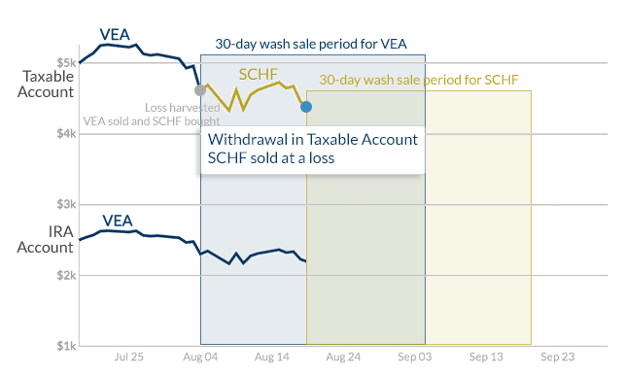

Two weeks cross, and the shopper makes a withdrawal from the taxable account (the complete SCHF place, for simplicity), desiring to fund the IRA. In these two weeks, the asset class dropped extra, so the sale of SCHF additionally realized a loss. The VEA place within the IRA stays unchanged.

Buyer withdrawal sells SCHF at a loss

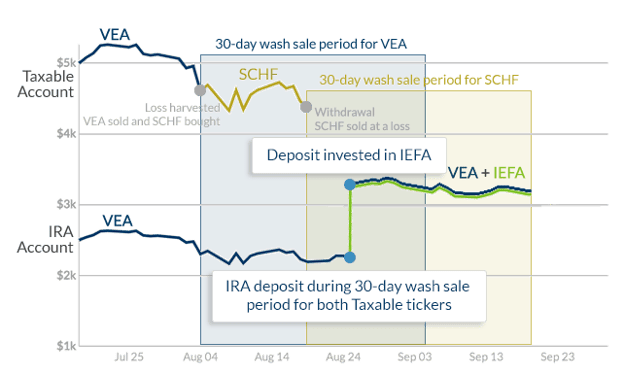

A number of days later, the shopper contributes to his IRA, and $1,000 is allotted to the Developed Markets asset class, which already incorporates some VEA. Even supposing the shopper now not holds any VEA or SCHF in his taxable account, shopping for both one within the IRA would completely wash a priceless realized loss. The Tertiary Ticker System robotically allocates the influx into the third choice for developed markets, IEFA.

IRA deposit into tertiary Ticker

Each losses have been preserved, and the shopper now holds VEA and IEFA in his IRA, sustaining desired allocation always. As a result of no capital positive aspects are realized in an IRA/401(ok), there isn’t a hurt in switching out of the IEFA place and consolidating the complete asset class in VEA when there isn’t a hazard of a wash sale.

The outcome: Clients utilizing TLH who even have their IRA/401(ok) property with Betterment can know that Betterment will search to guard priceless realized losses every time they deposit into their IRA/401(ok), whether or not it’s lump rollover, auto-deposits and even dividend reinvestments.

Good rebalancing

Lastly, tax loss harvesting directs the proceeds of each harvest to rebalance the complete portfolio, the identical approach {that a} Betterment account handles any incoming money circulate (deposit, dividend). Many of the money is anticipated to remain in that asset class and be reinvested into the parallel asset, however a few of it could not. Recognizing each harvest as a rebalancing alternative additional reduces the necessity for extra promoting in occasions of volatility, additional lowering tax legal responsibility. As all the time, fractional shares enable the inflows to be allotted with precision.

Tax loss harvesting mannequin calibration

Abstract: To make harvesting selections, tax loss harvesting optimizes round a number of inputs, derived from rigorous Monte Carlo simulations.

The choice to reap is made when the profit, web of value, exceeds a sure threshold. The potential advantage of a harvest is mentioned intimately beneath (“Outcomes”). In contrast to a 30-day switchback technique, tax loss harvesting doesn’t incur the anticipated STCG value of the switchback commerce. Subsequently, “value” consists of three elements: buying and selling expense, execution expense, and elevated value of possession for the substitute asset (if any).

Buying and selling prices are included within the wrap payment paid by Betterment clients. Tax loss harvesting is engineered to issue within the different two elements, configurable on the asset stage, and the ensuing value approaches negligible. Bid-ask spreads for the majority of harvestable property are slender. We search funds with expense ratios for the most important main/alternate ETF pairs which are shut, and within the case the place a harvest again to the first ticker is being evaluated, that distinction is definitely a profit, not a value.

There are two common approaches to testing a mannequin’s efficiency: historic backtesting and forward-looking simulation. Optimizing a system to ship the most effective outcomes for less than previous historic durations is comparatively trivial, however doing so can be a traditional occasion of information snooping bias. Relying solely on a historic backtest of a portfolio composed of ETFs that enable for 10 to twenty years of dependable information when designing a system meant to supply 40 to 50 years of profit would imply making a variety of indefensible assumptions about common market conduct.

The superset of resolution variables driving tax loss harvesting is past the scope of this paper—optimizing round these variables required exhaustive evaluation. Tax loss harvesting was calibrated through Betterment’s rigorous Monte Carlo simulation framework, spinning up 1000’s of server situations within the cloud to run by way of tens of 1000’s of forward-looking eventualities testing mannequin efficiency. We’ve calibrated tax loss harvesting in a approach that we imagine optimizes its effectiveness given anticipated future returns and volatility, however different optimizations might lead to extra frequent harvests or higher outcomes relying on precise market circumstances.

Greatest practices for tax loss harvesting

Abstract: Tax loss harvesting can add some worth for many traders, however excessive earners with a mix of very long time horizons, ongoing realized positive aspects, and plans for some charitable disposition will reap the most important advantages.

This can be a good level to reiterate that tax loss harvesting delivers worth primarily attributable to tax deferral, not tax avoidance. A harvested loss might be useful within the present tax yr to various levels, however harvesting that loss usually means creating an offsetting achieve sooner or later sooner or later. If and when the portfolio is liquidated, the achieve realized will probably be larger than if the harvest by no means happened.

Let’s take a look at an instance:

Yr 1: Purchase asset A for $100.

Yr 2: Asset A drops to $90. Harvest $10 loss, repurchase related Asset B for $90.

Yr 20: Asset B is value $500 and is liquidated. Positive aspects of $410 realized (sale worth minus value foundation of $90)

Had the harvest by no means occurred, we’d be promoting A with a foundation of $100, and positive aspects realized would solely be $400 (assuming related efficiency from the 2 correlated property.) Harvesting the $10 loss permits us to offset some unrelated $10 achieve right now, however at a worth of an offsetting $10 achieve sooner or later sooner or later.

The worth of a harvest largely is determined by two issues. First, what earnings, if any, is obtainable for offset? Second, how a lot time will elapse earlier than the portfolio is liquidated? Because the deferral interval grows, so does the profit—the reinvested financial savings from the tax deferral have extra time to develop.

Whereas nothing herein must be interpreted as tax recommendation, inspecting some pattern investor profiles is an effective strategy to admire the character of the good thing about tax loss harvesting.

Who advantages most?

The Bottomless Positive aspects Investor: A capital loss is simply as priceless because the tax saved on the achieve it offsets. Some traders could incur substantial capital positive aspects yearly from promoting extremely appreciated property—different securities, or maybe actual property. These traders can instantly use all of the harvested losses, offsetting positive aspects and producing substantial tax financial savings.

The Excessive Revenue Earner: Harvesting can have actual advantages even within the absence of positive aspects. Every year, as much as $3,000 of capital losses might be deducted from unusual earnings. Earners in excessive earnings tax states (akin to New York or California) might be topic to a mixed marginal tax bracket of as much as 50%. Taking the complete deduction, these traders might save $1,500 on their tax invoice that yr.

What’s extra, this deduction may gain advantage from constructive charge arbitrage. The offsetting achieve is more likely to be LTCG, taxed at round 30% for the excessive earner—lower than $1,000—an actual tax financial savings of over $500, on prime of any deferral worth.

The Regular Saver: An preliminary funding could current some harvesting alternatives within the first few years, however over the long run, it’s more and more unlikely that the worth of an asset drops beneath the preliminary buy worth, even in down years. Common deposits create a number of worth factors, which can create extra harvesting alternatives over time. (This isn’t a rationale for conserving cash out of the market and dripping it in over time—tax loss harvesting is an optimization round returns, not an alternative to market publicity.)

The Philanthropist: In every state of affairs above, any profit is amplified by the size of the deferral interval earlier than the offsetting positive aspects are ultimately realized. Nevertheless, if the appreciated securities are donated to charity or handed right down to heirs, the tax might be averted fully. When coupled with this consequence, the eventualities above ship the utmost advantage of TLH. Rich traders have lengthy used the twin technique of loss harvesting and charitable giving.

Even when an investor expects to principally liquidate, any gifting will unlock a few of this profit. Utilizing losses right now, in trade for built-in positive aspects, provides the partial philanthropist a variety of tax-efficient choices later in life.

Who advantages least?

The Aspiring Tax Bracket Climber: Tax deferral is undesirable in case your future tax bracket will probably be larger than your present. If you happen to count on to attain (or return to) considerably larger earnings sooner or later, tax loss harvesting could also be precisely the mistaken technique—it could, actually, make sense to reap positive aspects, not losses.

Specifically, we don’t advise you to make use of tax loss harvesting when you can at the moment understand capital positive aspects at a 0% tax charge. Below 2025 tax brackets, this can be the case in case your taxable earnings is beneath $48,350 as a single filer or $96,700 if you’re married submitting collectively. See the IRS web site for extra particulars.

Graduate college students, these taking parental go away, or simply beginning out of their careers ought to ask “What tax charge am I offsetting right now” versus “What charge can I moderately count on to pay sooner or later?”

The Scattered Portfolio: Tax loss harvesting is rigorously calibrated to handle wash gross sales throughout all property managed by Betterment, together with IRA property. Nevertheless, the algorithms can not take note of info that isn’t obtainable. To the extent {that a} Betterment buyer’s holdings (or a partner’s holdings) in one other account overlap with the Betterment portfolio, there might be no assure that tax loss harvesting exercise is not going to battle with gross sales and purchases in these different accounts (together with dividend reinvestments), and lead to unexpected wash gross sales that reverse some or all the advantages of tax loss harvesting. We don’t advocate tax loss harvesting to a buyer who holds (or whose partner holds) any of the ETFs within the Betterment portfolio in non-Betterment accounts. You’ll be able to ask Betterment to coordinate tax loss harvesting along with your partner’s account at Betterment. You’ll be requested to your partner’s account info after you allow tax loss harvesting in order that we will help optimize your investments throughout your accounts.

The Portfolio Technique Collector: Electing totally different portfolio methods for a number of Betterment objectives could trigger tax loss harvesting to establish fewer alternatives to reap losses than it would when you elect the identical portfolio technique for your entire Betterment objectives.

The Fast Liquidator: What occurs if all the further positive aspects attributable to harvesting are realized over the course of a single yr? In a full liquidation of a long-standing portfolio, the extra positive aspects attributable to harvesting might push the taxpayer into the next LTCG bracket, probably reversing the good thing about tax loss harvesting. For individuals who count on to attract down with extra flexibility, sensible automation will probably be there to assist optimize the tax penalties.

The Imminent Withdrawal: The harvesting of tax losses resets the one-year holding interval that’s used to differentiate between LTCG and STCG. For many traders, this isn’t a difficulty: by the point that they promote the impacted investments, the one-year holding interval has elapsed and so they pay taxes on the decrease LTCG charge. That is significantly true for Betterment clients as a result of our TaxMin characteristic robotically realizes LTCG forward of STCG in response to a withdrawal request. Nevertheless, if you’re planning to withdraw a big portion of your taxable property within the subsequent 12 months, it is best to wait to activate tax loss harvesting till after the withdrawal is full to cut back the potential for realizing STCG.

Different impacts to think about

Traders with property held in numerous portfolio methods ought to perceive the way it impacts the operation of tax loss harvesting. To be taught extra, please see Betterment’s SRI disclosures, Versatile portfolio disclosures, the Goldman Sachs sensible beta disclosures, and the BlackRock goal earnings portfolio disclosures for additional element. Shoppers in Advisor-designed customized portfolios by way of Betterment for Advisors ought to seek the advice of their Advisors to know the restrictions of tax loss harvesting with respect to any customized portfolio. Moreover, as described above, electing one portfolio technique for a number of objectives in your account whereas concurrently electing a distinct portfolio for different objectives in your account could cut back alternatives for TLH to reap losses, as TLH is calibrated to hunt to cut back wash gross sales.

Attributable to Betterment’s month-to-month cadence for billing charges for advisory providers, by way of the liquidation of securities, tax loss harvesting alternatives could also be adversely affected for purchasers with significantly excessive inventory allocations, third occasion portfolios, or versatile portfolios. Because of assessing charges on a month-to-month cadence for a buyer with solely fairness safety publicity, which tends to be extra opportunistic for tax loss harvesting, sure securities could also be bought that would have been used to tax loss harvest at a later date, thereby delaying the harvesting alternative into the long run. This delay can be as a result of TLH instrument’s effort to cut back situations of triggering the wash sale rule, which forbids a safety from being bought solely to get replaced with a “considerably related” safety inside a 30-day interval.

Elements which can decide the precise advantage of tax loss harvesting embody, however will not be restricted to, market efficiency, the scale of the portfolio, the inventory publicity of the portfolio, the frequency and measurement of deposits into the portfolio, the supply of capital positive aspects and earnings which might be offset by losses harvested, the tax charges relevant to the investor in a given tax yr and in future years, the extent to which related property within the portfolio are donated to charity or bequeathed to heirs, and the time elapsed earlier than liquidation of any property that aren’t disposed of on this method.

All of Betterment’s buying and selling selections are discretionary and Betterment could determine to restrict or postpone TLH buying and selling on any given day or on consecutive days, both with respect to a single account or throughout a number of accounts.

Tax loss harvesting just isn’t appropriate for all traders. Nothing herein must be interpreted as tax recommendation, and Betterment doesn’t signify in any method that the tax penalties described herein will probably be obtained, or that any Betterment product will lead to any specific tax consequence. Please seek the advice of your private tax advisor as as to if TLH is an acceptable technique for you, given your specific circumstances. The tax penalties of tax loss harvesting are advanced and unsure and could also be challenged by the IRS. You and your tax advisor are answerable for how transactions performed in your account are reported to the IRS in your private tax return. Betterment assumes no duty for the tax penalties to any consumer of any transaction.

See Betterment’s tax loss harvesting disclosures for additional element.

How we calculate the worth of tax loss harvesting

Over 2022 and 2023, we calculated that 69% of Betterment clients who employed the technique noticed potential financial savings in extra of the Betterment charges charged on their taxable accounts for the yr.

To succeed in this conclusion, we first recognized the accounts to think about, outlined as taxable investing accounts that had a constructive stability and tax loss harvesting turned on all through 2022 and 2023. We excluded belief accounts as a result of their tax remedies might be highly-specific and so they made up lower than 1% of the information.

For every account’s taxpayer, we pulled the quick and long run capital achieve/loss within the related accounts realized in 2022 and 2023 utilizing our buying and selling and tax information. We then divided the achieve/loss into these attributable to a TLH transaction and people not attributable to a TLH transaction.

Then, for every tax yr, we calculated the short-term positive aspects offset by taking the larger of the short-term loss realized by tax loss harvesting and the short-term achieve attributable to different transactions. We did the identical for long-term achieve/loss. If there have been any losses leftover, we calculated the quantity of unusual earnings that might be offset by taking the larger of the shopper’s reported earnings and $3,000 ($1,500 if the shopper is married submitting individually) after which taking the larger of that quantity and the sum of the remaining long-term and short-term losses (after first subtracting any non-tax loss harvesting losses from unusual earnings). If there have been any losses leftover in 2022 in spite of everything that, we carried these losses ahead to 2023.

At this level, we had for every buyer the quantity of short-term positive aspects, long-term positive aspects and unusual earnings offset by tax loss harvesting for every tax yr. We then calculated the short-term and long-term capital positive aspects charges utilizing the federal tax brackets for 2022 and 2023 and the reported earnings of the taxpayer, their reported tax submitting standing, and their reported variety of dependents. We assumed the usual deduction and conservatively didn’t embody state capital positive aspects taxes as a result of some states wouldn’t have capital positive aspects tax. We calculated the unusual earnings charge together with federal taxes, state taxes, and Medicare and Social Safety taxes utilizing the person’s reported earnings, submitting standing, variety of dependents, assumed normal deduction, and age (assuming Medicare and Social Safety taxes stop on the retirement age of 67). We then utilized these tax charges respectively to the offsets to get the tax invoice discount from every sort of offset and summed them as much as get the entire tax discount.

Then, we pulled the entire charges charged to the customers on the account in query that have been accrued in 2022 and 2023 from our payment accrual information and in contrast that to the tax invoice discount. If the tax invoice discount was larger than the charges, we thought-about tax loss harvesting to have not directly paid for the charges within the account in query for the taxpayer in query. This was the case for 69% of consumers.2

Your customized Estimated Tax Financial savings instrument

Overview: Betterment’s TLH Estimated Tax Financial savings Instrument is present in your on-line account and designed to quantify the tax-saving potential of our tax loss harvesting (TLH) characteristic. By leveraging each transactional information from Betterment accounts and your self-reported demographic and monetary profile info, the instrument generates dynamic estimates of realized and potential tax financial savings. These calculations present each current-year and cumulative (“all-time”) tax financial savings estimates.

Consumer-centric tax modeling: To personalize estimates, the instrument takes into consideration consumer monetary profile info: your self-reported annual pre-tax earnings, state of residence, tax submitting standing (e.g. particular person, married submitting collectively), and variety of dependents. This info helps Betterment create a complete tax profile, estimating your federal and state earnings tax charges, long-term capital positive aspects (LTCG) charges, and relevant normal deductions. Betterment’s estimated tax financial savings methodology additionally incorporates the IRS’ cap on unusual earnings offsets for capital losses—$3,000 for most people or $1,500 if married submitting individually, and likewise incorporates any obtainable carryforward losses.

Tax lot evaluation and offsetting hierarchy: On the coronary heart of Betterment’s estimated tax financial savings instrument is an in depth evaluation of tax-lot stage buying and selling information. Betterment tallys TLH-triggered losses (short- and long-term) from different realized capital positive aspects or losses, grouping them by yr, and calculates your potential tax profit by offsetting losses and positive aspects by sort in accordance with IRS guidelines, and permitting extra losses to offset different earnings varieties or carry ahead to future years. The IRS offset order is utilized:

- Brief-term losses offset short-term positive aspects

- Lengthy-term losses offset long-term positive aspects

- Remaining short-term losses offset long-term positive aspects

- Remaining long-term losses offset short-term positive aspects

- Remaining short-term losses offset unusual earnings

- Remaining long-term losses offset unusual earnings

- Any additional losses are carried ahead

Present yr estimated tax financial savings: Betterment calculates your present yr estimated tax financial savings from TLH based mostly on the IRS numbered offset record above, which is the sum of:

- Brief-term offset represents the tax financial savings from subtracting your short-term harvested losses and cross-offset long-term harvested losses from current-year short-term capital positive aspects (numbers 1 and 4 above), then multiplying by your estimated federal plus state tax charge.

- Lengthy-term offset represents the financial savings from subtracting long-term harvested losses and cross-offset short-term harvested losses from current-year long-term capital positive aspects (numbers 2 and three above), multiplied by your estimated long-term capital positive aspects charge.

- Peculiar earnings offset captures the financial savings from making use of any remaining harvested losses to your unusual earnings as much as the allowable restrict (numbers 5 and 6 above), multiplied by your estimated federal plus state tax charge.

- Each short-term and long-term harvested losses could embody banked losses from prior years that couldn’t be used on the time. These carryforward losses (quantity 7 above) are utilized in the identical approach as current-year harvested losses when calculating your tax financial savings.

For the instrument, Harvested Losses are all time short- and long-term harvested losses i.e., all harvested losses so far by way of TLH. Financial savings from the Brief-term offset, long-term offset, and unusual earnings offset are summed to yield the present yr estimated tax financial savings.

All-time estimated tax financial savings : Betterment calculates your all-time estimated tax financial savings from TLH based mostly on the sum of:

- All-time Lengthy-term harvested losses × LTCG charge

- All-time Brief-term harvested losses × (Federal + State tax charge)

For the all-time estimated tax determine, the all-time figures used are all of your harvested losses by way of Betterment’s TLH characteristic to the current date, and somewhat than calculate offsets, Betterment assumes that you’ll be able to absolutely offset your long-term harvested losses and short-term harvested losses with positive aspects. Subsequently, we apply the long run capital positive aspects charges and marginal unusual earnings charge (which is the sum of your federal and state tax charges) by your whole long-term harvested losses and short-term losses, respectively. There is no such thing as a unusual earnings offset within the All-Time Estimate. This simplification doesn’t monitor when the loss occurred, and subsequently, assumes present estimated tax charges have been relevant all through prior years.

Assumptions: Whereas this instrument gives a robust estimate of your potential tax advantages from tax loss harvesting, it is very important perceive the assumptions and limitations underlying the estimated tax financial savings calculations. Estimated tax financial savings figures introduced are estimates—not ensures—and depend on the knowledge you’ve offered to Betterment. Precise tax outcomes could fluctuate based mostly in your precise tax return and scenario when submitting. The instrument evaluates solely the exercise inside your Betterment accounts and doesn’t take note of any funding exercise from exterior accounts. For the present yr calculation, the instrument additionally assumes that you’ve got enough unusual earnings to completely profit from capital loss offsets, and for the all-time calculation, the instrument gives a tax-dollar estimate of all harvested losses, based mostly on sort (short- or long-term) and present tax charges.

Moreover, the estimated tax financial savings calculation simplifies the therapy of sure entities; for instance, trusts, enterprise accounts, or different specialised tax constructions will not be dealt with distinctly. State-level tax estimates exclude metropolis tax charges and municipal taxes, which can additionally have an effect on your total tax scenario. The “all-time estimate” proven displays an approximation of the entire tax affect of harvested losses so far—together with advantages that haven’t but been realized or claimed.

Whereas the estimate has its limitations, it gives a transparent and actionable view into how tax-smart investing can add worth over time. It helps present how harvested losses could decrease your tax invoice and increase after-tax returns—bringing transparency to a method that’s usually onerous to see in greenback phrases. For a lot of traders, it highlights the long-term monetary advantages of managing taxes proactively.

Conclusion

Abstract: Tax loss harvesting might be an efficient approach to enhance your investor returns with out taking further draw back threat.

[ad_2]