[ad_1]

Bond markets have been little modified Friday and equities rallied as a long-awaited key financial report confirmed softer-than-expected inflation final month, bolstering expectations for an October price reduce from the Federal Reserve.

The 2-year muni-UST ratio Friday was at 70%, the five-year at 66%, the 10-year at 68% and the 30-year at 89%, in accordance with Municipal Market Information’s 3 p.m. EDT learn. ICE Information Providers had the two-year at 69%, the five-year at 66%, the 10-year at 68% and the 30-year at 89% at a 4 p.m. learn.

“Buyers weren’t upset,” mentioned John Kerschner, world head of securitized merchandise and portfolio supervisor at Janus Henderson. “Inflation got here in softer than anticipated, resulting in a tepid bond market rally” and guaranteeing a price reduce on the upcoming Federal Open Market Committee assembly.

“Whereas traders might have anticipated a extra strong rally given the information, considerations abound in some corners that these numbers are much less strong than regular, because of the shutdown,” he mentioned.

As a substitute, the market has targeted on Fed governors’ speeches, which have trended “dovish,” Kerschner mentioned.

Friday’s launch of the September CPI knowledge supplied a uncommon look into the financial system amid the federal authorities shutdown, BofA strategists wrote. Within the absence of information from the Bureau of Labor Statistics, the macro market has operated in a “vacuum-like atmosphere.”

The CPI report and “S&P’s flash PMIs for October ought to present some much-needed perception relating to the state of the financial system,” BofA added.

BofA analysts do not anticipate the shutdown to have a cloth influence on state or native munis, though some governments are extra uncovered than others, and the results will probably be depending on the shutdown’s size and scope.

“Public Housing Authority and Part 8 bonds supported by federal housing funds, bonds supported by federal lease funds on amenities leased by municipal entities to federal companies, army housing bonds and GARVEEs are extra uncovered to shutdowns,” BofA’s analysts wrote.

That is now the most important full shutdown in U.S. historical past, BofA’s strategists wrote, and will moderately be anticipated to eclipse the 34-day partial authorities shutdown in 2019. The shutdown has lasted longer than anticipated, they wrote, and there will probably be lingering results.

Total, states are in pretty good situation, however their rainy-day fund balances are declining, mentioned Barclays strategists.

“In the meantime, tariffs will begin affecting states to a bigger diploma, particularly these with robust manufacturing bases and main coastal ports,” they mentioned.

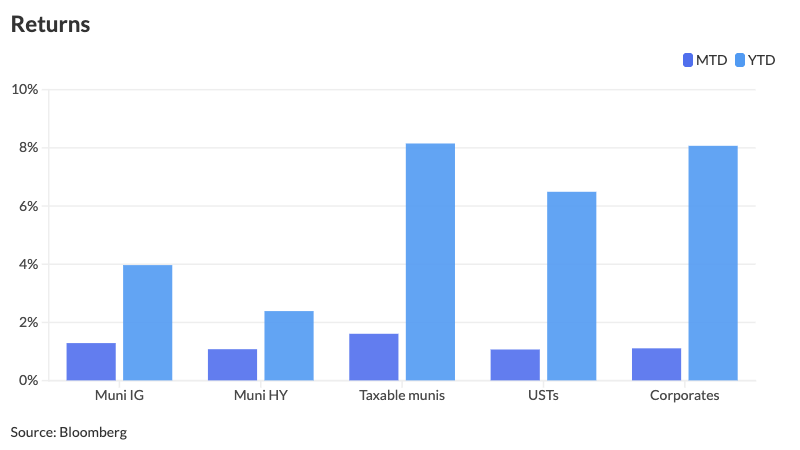

Elsewhere, in comparison with historic efficiency in October, tax-exempts have generated stable numbers this month, with investment-grade munis returning 1.29% and the high-yield munis seeing beneficial properties of 1.08%, they mentioned.

“Yields of the IG index have already dropped to their current lows final reached in February, whereas the HY index has lagged a bit, and the yield differential between the 2 indices has reached the degrees of March 2024,” Barclays strategists mentioned.

Regardless of the lengthy finish’s robust efficiency previously six weeks, they assume it nonetheless has some “room to run,” because it normally does within the final a number of months of the yr.

The muni curve within the zero- to 15-year vary has flattened, and the 15- to 30-year vary has steepened barely, BofA strategists mentioned.

“Tax-exempt cash market yields climbed greater than 40bp because the Fed price reduce in mid-September, which additionally introduced yields in 1-7yr AAA greater. [Seven] to fifteen years are in a bull flattening, and 15 to 30 years are in a bull steepening,” they mentioned.

“The muni market strikes don’t appear to counsel there may be provide/demand imbalance within the quick serial market; quite, it’s probably because of traders’ total consensus to increase length alongside the curve,” BofA strategists mentioned.

In the course of the previous four-year bear market, they notice “each retail and institutional traders allotted extra within the quick maturity market, however would prolong length when the market rally turned extra constant.”

This time, after an October Fed price reduce, quick serial yields are anticipated to come back down from present ranges, that means the municurve ought to have a bull flattening after this month, they mentioned.

New-issue calendar

The brand new-issue calendar is at $5.367 billion, with $4.085 negotiated offers on faucet and $1.281 billion of competitives.

The Chicago Board of Schooling leads the negotiated market with $1.093 billion of limitless tax GO refunding bonds.

The aggressive calendar is led by Florence, South Carolina, with $143.645 million of mixed waterworks and sewerage system capital enchancment income bonds.

AAA scales

MMD’s scale was little modified: 2.53% (unch) in 2026 and a pair of.44% (+1) in 2027. The five-year was 2.36% (unch), the 10-year was 2.70% (unch) and the 30-year was 4.10% (unch) at 3 p.m.

The ICE AAA yield curve was little modified: 2.50% (+1) in 2026 and a pair of.42% (+1) in 2027. The five-year was at 2.39% (unch), the 10-year was at 2.73% (unch) and the 30-year was at 4.08% (unch) at 3 p.m.

The S&P World Market Intelligence municipal curve was unchanged: The one-year was at 2.51% in 2025 and a pair of.43% in 2026. The five-year was at 2.36%, the 10-year was at 2.71% and the 30-year yield was at 4.08% at 3 p.m.

Bloomberg BVAL was unchanged: 2.48% in 2025 and a pair of.43% in 2026. The five-year at 2.34%, the 10-year at 2.69% and the 30-year at 4.04% at 4 p.m.

Treasuries have been little modified.

The 2-year UST was yielding 3.48% (-1), the three-year was at 3.484% (-1), the five-year at 3.599% (-1), the 10-year at 3.996% (-1), the 20-year at 4.554% (flat) and the 30-year at 4.584% (flat) close to the shut.

CPI

The market was excited to get any financial knowledge, which has been non-existent because the authorities shutdown started on Oct. 1, however Friday’s launch of the patron worth index was a ho-hum occasion for economists, who mentioned inflation stays too excessive, however with the labor market weakening, the Federal Reserve will proceed its easing cycle.

“Proper now, the markets are seemingly giving the Fed a move to chop charges via the tip of 2025, after which they are going to deal with two issues: 1) who will succeed [Federal Reserve Chairman] Jay Powell and the way dovish will they be and a pair of) how the financial system is faring as soon as market contributors truly get to see and analyze actual knowledge as soon as once more,” Janus’ Kerschner mentioned.

“We perceive that valuations are excessive and there are dangers available in the market, however with the Fed reducing charges — and this report does nothing to cease them from a 25-bps reduce subsequent week — and company income persevering with to extend, it is onerous to see an interruption of this yr’s bull market,” mentioned Chris Zaccarelli, chief funding officer for Northlight Asset Administration.

Whereas tariffs have raised inflation expectations, inflicting traders to take bearish positions, he mentioned, “the market is more likely to preserve squeezing the shorts till they notice that the financial system — and company America — is extra resilient than many anticipated.”

However as Halloween approaches, the September CPI report will not “spook” the Fed, mentioned Lindsay Rosner, head of multi-sector fastened revenue investing at Goldman Sachs Asset Administration, who expects “additional easing” on the upcoming Fed assembly.

“A December price reduce additionally stays probably with the present knowledge drought offering the Fed with little motive to deviate from the trail set out within the dot plot,” she mentioned.

“This report will clearly preserve the Ate up observe to chop charges,” mentioned Artwork Hogan, B. Riley Wealth chief market strategist.

“The Fed has been clear that they’re extra targeted on the softening labor knowledge and can proceed to defend their full employment mandate, even with core CPI nicely above their 2% goal,” he mentioned.

The higher-than-expected studying “is nice information for the markets,” mentioned Jay Woods, chief market strategist at Freedom Capital Markets. Regardless of CPI climbing to “its highest ranges since January,” he mentioned, “the Fed’s focus appears slanted towards the labor facet of its twin mandate.”

Though the report might increase eyebrows, it “should not change [the Fed’s] present path to chop on the subsequent two conferences,” Woods mentioned.

“The troubling factor concerning the knowledge is that the pattern is shifting away from their said 2% purpose,” he mentioned. “The excellent news is that whereas inflation is ticking greater, it’s not operating away.”

Olu Sonola, head of U.S. financial analysis at Fitch Scores, mentioned the Fed “will probably be joyful” if inflation stays close to 3% within the coming months, that means the tariff passthrough stays muted. This reduce “will probably be framed as an insurance coverage reduce, with hopes that by December the shutdown is over and the Fed has a clearer learn on jobs.”

“Inflation worrywarts on the Fed should reply to the majority of the FOMC already rallying across the realization tariffs triggered much less inflation than feared and tariff-related worth pressures are already abating below the load of disinflationary momentum below the floor in classes like shelter and medical care companies,” mentioned FHN Monetary Chief Economist Chris Low.

“The inflation pressures seen within the August CPI report seem to have dissipated in September,” mentioned BMO Chief U.S. Economist Scott Anderson. “The Fed now has every little thing it must make a price reduce resolution subsequent week regardless of the dearth of well timed financial knowledge because of the federal authorities shutdown.”

Eric Teal, chief funding officer for Comerica Wealth Administration, mentioned this “report mixed with a weaker job market supplies cowl for added price cuts in 2025 and into subsequent yr.”

However Gina Bolvin, president of Bolvin Wealth Administration Group, mentioned, “Inflation is cooling, however not convincingly sufficient.”

The Fed “will keep cautious,” she mentioned. These numbers do not “slam the door on price cuts, however [they] slender the trail.”

“Markets are digesting this as a sign to mood expectations,” Bolvin mentioned. “It isn’t time to chase danger, however it’s not time to cover both. Buyers ought to lean into high quality names, corporations with margin power, and sectors that may climate cussed inflation. The Fed’s subsequent transfer will depend upon how sturdy this disinflation pattern actually is.”

Major to come back

The Chicago Board of Schooling (/BB+//BBB-/) is about to cost Tuesday $1.093 billion of limitless tax GO refunding bonds, consisting of $829.175 million of Sequence 2025B and $264.035 million of Sequence 2025C. BofA Securities.

The Virginia Housing Growth Authority (Aaa/AAA//) is about to cost Tuesday $450 million of commonwealth mortgage bonds, consisting of $75 million of non-AMT Sequence E bonds, $150 million of taxable Sequence F bonds and $225 million of non-AMT Sequence G bonds. BofA Securities.

The Connecticut Housing Finance Authority (Aaa/AAA//) is about to cost Tuesday $289.975 million of social housing mortgage finance program bonds, consisting of $20 million of Subseries E-1 bonds and $269.975 million of taxable Subseries E-2 bonds. BofA Securities.

The Colorado Housing and Finance Authority (Aaa/AAA//) is about to cost $200.48 million of taxable single-family mortgage Class I bonds, 2025 Sequence O-1. RBC Capital Markets.

The North Carolina Housing Finance Company (Aa1/AA+//) is about to cost Tuesday $200 million of non-AMT house possession income bonds, Sequence 59-A. BofA Securities.

The Harris County Cultural Schooling Amenities Finance Corp., Texas, (/AA//) is about to cost Wednesday $200 million of Houston Methodist income bonds, Sequence 2025G. Jefferies.

North Carolina (Aa1/AA+/AA+/) is about to cost Thursday $178.375 million of restricted obligation refunding bonds, Sequence 2025B. Wells Fargo.

Clemson College, South Carolina, (Aa2//AA/) is about to cost Tuesday $174.635 million of upper training refunding income bonds, Sequence 2025A. Morgan Stanley.

The Glendale Industrial Growth Authority, Arizona, (/AA-/AA/) is about to cost Tuesday $150 million of Midwestern College income bonds. Raymond James.

The California Housing Finance Company is about to cost Wednesday $134.015 million of non-AMT sustainability inexpensive housing income bonds, 2025 Sequence B. RBC Capital Markets.

Broward County, Florida, (A1/A//) is about to cost Tuesday $132.765 million of AMT port amenities income bonds. Jefferies.

The River Islands Public Financing Authority Enchancment Space No. 3, California, is about to cost $112.375 million of Group Amenities District No. 2023-1 particular tax bonds. HilltopSecurities.

Aggressive

Florence, South Carolina, (Aa2/AA-//) is about to promote $143.645 million of mixed waterworks and sewerage system capital enchancment income bonds, at 11 a.m. Japanese Wednesday.

The Virginia Public Faculty Authority is about to promote $104.75 million of particular obligation college financing bonds at 10:45 a.m. Thursday.

Gary Siegel contributed to this story.

[ad_2]