[ad_1]

Processing Content material

Munis have been regular as U.S. Treasuries noticed small positive factors and equities ended up after an financial report confirmed inflation was cooling.

Following the discharge of the report, “odds of a January charge reduce rose from 24% to 29%,” famous FHN Monetary Chief Economist Chris Low.

Muni yields have been bumped a foundation level, whereas UST yields fell two to 4 foundation factors.

“Whereas one good inflation report might not be sufficient to set off a follow-up charge reduce in late January (certainly, Treasury yields fell [slightly] on the report), a transfer in March is probably going if progress in decreasing inflation continues within the new 12 months,” stated Sal Guatieri, senior economist at BMO.

The 2-year muni-UST ratio Thursday was at 70%, the five-year at 66%, the 10-year at 67% and the 30-year at 88%, based on Municipal Market Information’s 3 p.m. EDT learn. ICE Information Companies had the two-year at 69%, the five-year at 64%, the 10-year at 66% and the 30-year at 87% at a 4 p.m. learn.

“12 months-end dynamics are in impact, with provide winding down and portfolio squaring driving momentum,” stated Kim Olsan, senior mounted revenue portfolio supervisor at NewSquare Capital.

The New York Metropolis Transitional Finance Authority bought $1.83 billion right into a “stable order e-book.”

Closing yields on the final mega deal of the 12 months have been “pared throughout a number of maturities, with a $133 million tranche of 10-year 5s yielding 3.12%, or +37/MMD (for a top-bracket New York purchaser, the tax equal yield can be about 6.35%),” Olsan stated.

Solely premium coupons have been “applied” within the two- to 30-year construction, she stated.

Together with Wednesday’s NYC TFA deal, there have been 45 $1 billion-plus offers this 12 months, Olsan stated.

And with the forecasted improve in provide in 2026, there are more likely to be across the identical variety of billion-plus offers, probably much more, she stated.

“Lengthy-end credit score is exhibiting indicators of a pullback — [unrated] Buckeye, Ohio, Tobacco 5s in 2055 are buying and selling round 6.40%, the very best yield for the bond since August,” Olsan stated. “Secondary exercise factors to portfolios being aligned for the approaching 12 months.”

“Heavier bid-list quantity on the brief finish introduced tighter ranges, with many gadgets going into orders and resetting 1–3-year spot ranges decrease: Ohio [general obligation bond] 5s due 2027 have been bought at 2.44% (+0/MMD), and Wisconsin GO 5s in 2028 traded at 2.46% (+3/MMD),” she stated.

“A section of inquiry is probably going discovering some defensive consolation in excessive grades” till provide “reengages” subsequent month, she stated.

Munis are down 0.16% month-to-date. The 1-2 12 months and the 2-4 12 months ranges are seeing the most important positive factors this month, with returns of 0.20% and 0.19%, respectively.

Elsewhere, muni credit score fundamentals stay robust, largely pushed by substantial COVID-era federal assist and robust financial development, stated Goldman Sachs strategists.

“State and native revenues grew considerably throughout this era and conservative budgeting allowed governments to bolster reserves, cut back debt and enhance pension funding,” they stated.

Since fiscal 12 months 2021, state reserve funds have grown as a proportion of general expenditures, they stated.

Regardless of some latest “spending down” of those reserves, states are estimated to finish fiscal 12 months 2025 with greater than double the reserves held in fiscal 12 months 2020, based on Goldman strategists.

“Some states have additionally improved controls, added protections to restrict spending down rainy-day funds and launched necessities to construct up reserves when income development is robust,” they stated.

Municipal debt as a proportion of gross home product has continued to fall, demonstrating, regardless of surging issuance, a more healthy general fiscal image, Goldman strategists stated.

Moreover, states have improved their pension funding. “The mixture funded ratio for state and native pension plans elevated to an estimated 81.4% in fiscal 12 months 2025,” they stated.

These areas present muni credit score, which can be coming into a interval of slower income development, with a powerful fiscal basis, Goldman strategists stated.

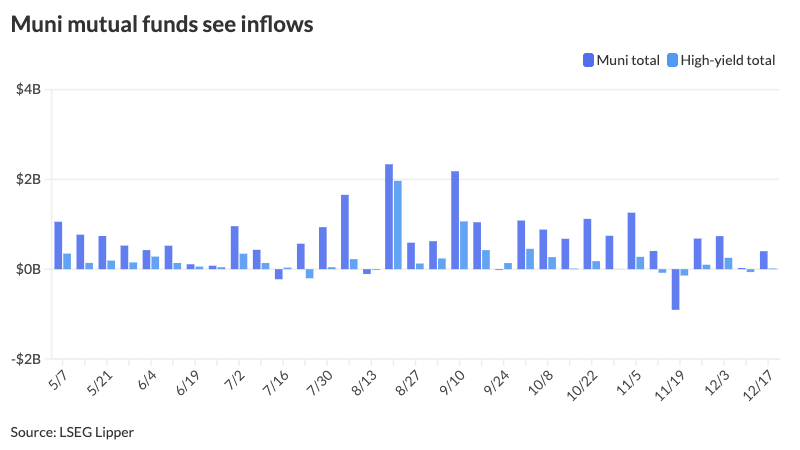

Fund flows

Traders added $400.1 million to municipal bond mutual funds within the week ended Wednesday, following $26 million of inflows the prior week, based on LSEG Lipper information.

Excessive-yield funds noticed inflows of $16.7 million in comparison with outflows of $64.5 million the earlier week.

Tax-exempt municipal cash market funds noticed outflows of $700.2 million for the week ending Dec. 15, bringing whole property to $145.056 billion, based on the Cash Fund Report, a weekly publication of EPFR.

The common seven-day easy yield for all tax-free and municipal money-market funds was 2.44%.

Taxable money-fund property noticed $8.124 billion pulled, bringing the entire to $7.464 trillion.

The common seven-day easy yield was 3.48%.

The SIFMA Swap Index was at 3.26% on Wednesday in comparison with the earlier week’s 3.11%.

AAA scales

MMD’s scale was unchanged: 2.46% in 2026 and a pair of.41% in 2027. The five-year was 2.43%, the 10-year was 2.76% and the 30-year was 4.24% at 3 p.m.

The ICE AAA yield curve was bumped as much as one foundation level: 2.46% (unch) in 2026 and a pair of.43% (-1) in 2027. The five-year was at 2.39% (-1), the 10-year was at 2.77% (-1) and the 30-year was at 4.19% (unch) at 4 p.m.

The S&P World Market Intelligence municipal curve was unchanged: The one-year was at 2.46% in 2025 and a pair of.42% in 2026. The five-year was at 2.43%, the 10-year was at 2.76% and the 30-year yield was at 4.22% at 3 p.m.

Bloomberg BVAL was bumped one foundation level: 2.49% (-1) in 2025 and a pair of.44% (-1) in 2026. The five-year at 2.38% (-1), the 10-year at 2.72% (-1) and the 30-year at 4.13% (-1) at 4 p.m.

Treasuries have been barely firmer.

The 2-year UST was yielding 3.461% (-2), the three-year was at 3.498% (-3), the five-year at 3.659% (-4), the 10-year at 4.117% (-4), the 20-year at 4.755% (-3) and the 30-year at 4.799% (-3) close to the shut.

CPI

Economists have been divided about whether or not the cooler-than-expected client value index report would imply extra charge cuts in 2026, as many pointed to extenuating circumstances that would have led to the drop.

“The canceling of the October report makes month-on-month comparisons not possible,” stated Kay Haigh, international co-head of mounted revenue and liquidity options at Goldman Sachs Asset Administration. “The truncated information-gathering course of, given the shutdown, may have brought about systematic biases within the information.”

As such, he does not count on this report back to have an awesome affect on financial coverage “given how noisy the information is.”

The extra correct December CPI can be launched two weeks earlier than the subsequent Federal Open Market Committee assembly, Haigh famous.

“All informed, it is a constructive report that comes with an asterisk,” stated Artwork Hogan, B. Riley Wealth chief market strategist. Changes have been made on account of the dearth of October numbers, he stated.

“The November report additionally contains the Black Friday phenomenon that appears to have grown into your entire month of November,” Hogan added. Future experiences, he stated, “will possible clean out the statistical errors that may have been current in as we speak’s report.”

“It is only one month of information, and distortions cannot be dominated out, however the sharp drop in annual inflation leaves the Fed with little excuse not to reply to rising unemployment,” stated Seema Shah, chief international strategist at Principal Asset Administration.

With extra experiences anticipated earlier than the subsequent FOMC assembly, she stated, these “numbers tilt the steadiness firmly in direction of the doves.”

Though Principal nonetheless expects two cuts in 2026, this report “raises the chances that they’re going to land within the first half of the 12 months relatively than the second,” Shah stated.

Whereas the numbers have been better-than-expected, Chris Zaccarelli, chief funding officer at Northlight Asset Administration, famous, “it is just one month’s information factors and they’re going to possible fluctuate within the upcoming months, however the principle concern of Fed officers who’re reluctant to maintain slicing is that inflation is persistently excessive and will not come down in the event that they hold decreasing rates of interest, and at this level that does not seem like it is the case.”

The Fed “clearly” can hold slicing charges, he stated.

“The inflation bump from tariffs is behind us, so the trail is now clear for the Fed to decrease charges once more in January,” stated Jamie Cox, managing accomplice for Harris Monetary Group. “There is no such thing as a longer a case for restrictive financial coverage.”

And whereas the report seems constructive, Olu Sonola, head of U.S. financial analysis at Fitch Rankings, stated, “the dearth of element and the absence of information assortment throughout the shutdown introduce a level of skepticism that is arduous to disregard.”

The report might clarify why Fed Chair Jerome Powell appeared “relaxed” about inflation at his post-meeting press convention, stated James Knightley, chief worldwide economist at ING. “He means that the tariff affect will peak within the first quarter and we agree, thereafter, falling gasoline costs, slowing housing rents and weaker wage development imply we’re on monitor to get towards 2% far sooner than the Fed [was]forecasting final week.”

ING expects quarter-point cuts in March and June, “however the dangers appear skewed towards the Fed with the ability to ship extra until the roles market begins to stabilize,” he stated.

Nonetheless, traders have been happy by the prospect of decrease inflation, stated Jennifer Timmerman, senior funding technique analyst at Wells Fargo Funding Institute. “S&P 500 futures (have been) rising in hopes the discharge will pave the way in which for a year-end Santa Claus rally. The U.S. Treasury yield curve is bull steepening because the surprisingly subdued inflation studying ought to put extra charge cuts again on the Fed’s radar for 2026.”

Inflation experiences could also be “bumpy” for the subsequent few months, stated Jeffrey Roach, chief economist for LPL Monetary. “We might have some extra scorching readings as demand ticks increased from larger-than-expected tax returns in early 2026, however we should always count on inflation to chill within the latter a part of subsequent 12 months.”

“Inflation has misplaced its grip — and the Fed is aware of it,” stated Gina Bolvin, president of Bolvin Wealth Administration Group. “At present’s CPI print offers the market what it wanted: affirmation that disinflation is sturdy and coverage reduction is coming. For traders, that is the time to lean into development with guardrails — be selective, be strategic, and keep forward of the curve.”

The Fed can be “particularly inspired by the multi-year low in core CPI,” stated Invoice Adams, chief economist at Comerica Financial institution. “The cool November inflation report additional bolsters the case for extra charge cuts in 2026.”

Comerica expects 75 foundation factors of easing subsequent 12 months, he stated, “with most of that discount more likely to come after Chair Powell’s time period ends in Could.”

[ad_2]