[ad_1]

Processing Content material

A number of components, corresponding to rates of interest and macroeconomic coverage, will affect 2026 bond issuance, however continued infrastructure wants and inflation-induced added prices will impression authorities borrowing essentially the most, analysts stated.

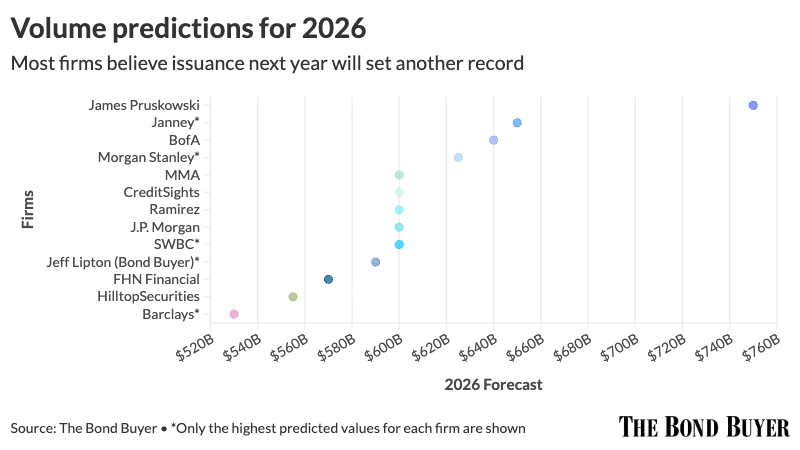

Municipal bond provide projections for subsequent yr vary from a excessive of $750-plus billion to a low of $520 billion, with most corporations anticipating issuance subsequent yr to be not less than $600 billion, simply surpassing 2025’s file.

Many anticipated

Most forecasts have been

Issuance is at $544.967B billion year-to-date, having already topped 2024’s file $507.585 billion by mid-November.

On the excessive finish of 2026 predictions is investor and market strategist James Pruskowski’s greater than $750 billion. Issuance will likely be pushed by “mega-infrastructure, housing, local weather initiatives, with new knowledge facilities and their supporting infrastructure including gasoline,” in accordance with Pruskowski.

Conventional normal obligation bonds will “fade,” as project-specific financings, tax increment financings and particular assessments “push the boundaries” of market absorption, he stated.

Whereas headlines will “rattle consensus,” the actual story for subsequent yr will likely be about what’s conventional muni provide, Pruskowski stated.

Janney sees issuance between $605 billion and $650 billion, stated Alice Cheng, director of municipal credit score and investor technique on the agency.

New-money issuance will tick up subsequent yr by $20 billion to $30 billion, partially as a result of estimated lack of federal grants to states and native governments, together with larger development prices, she stated.

Refundings can even be up subsequent yr, as decrease and extra favorable rates of interest will create extra refunding alternatives, Cheng stated.

BofA Securities sees issuance subsequent yr at $640 billion, up 10% from its 2025 projected issuance of $580 billion.

There will likely be lighter issuance for the primary and final two months of the yr and over $50 billion of provide monthly from March 2026 via October 2026, BofA strategists predict.

New-money will likely be at $470 billion, up 8% year-over-year, pushed by “the depletion of federal COVID stimulus funding; an insatiable demand for public infrastructure; a booming economic system and labor market; and sticky inflation,” which pushes the “nominal greenback quantity of financing for an infrastructure mission considerably larger than it will have been again in 2020 and 2021,” they stated.

There will likely be a “resurgence” in refunding exercise, forecast at $170 billion, up 17% from 2025, BofA strategists stated.

“The pool of refundable candidates for 2026 is roughly 13% bigger than for 2025, however the backlog of bonds which might be eligible for refunding and stay unrefunded is 24% bigger than the backlog for 2025; and … common muni charges throughout 2026 will likely be considerably decrease than throughout 2025, thus supporting a greater refunding setting,” they stated.

Moreover, following “two years of sturdy new cash progress and expanded web debt masses, issuers will doubtless spend extra time executing refundings than previously 4 years when muni charges flip considerably decrease,” BofA strategists stated.

There will likely be $565 billion of tax-exempt bonds, $50 billion of taxable bonds and AMT bonds, they stated.

Taxable issuance may obtain a “enhance if there’s a interval of flight-to-quality trades to Treasuries, both resulting from danger asset declines or credit score considerations; that scenario is unlikely in 1H26, although the chance could improve throughout 2H26,” BofA strategists stated.

Morgan Stanley predicts provide will fall between $600 billion and $625 billion.

There will likely be “bonds to purchase” as a result of prices have risen. The upside of inflation, although, is that governments have extra tax {dollars} to spend, the agency stated.

Municipal Market Analytics believes quantity will likely be not less than $600 billion.

New-money issuance will proceed to develop — although at a slower tempo than this yr — resulting from “deferred upkeep, the scheduling of pandemic-delayed conventional initiatives, M&A exercise throughout enterprises and governments, local weather change adaptation, and the withdrawal of federal assist for baseline state and native coverage supply,” stated Matt Fabian, president of MMA.

Moreover, if inflation stays elevated, mission prices will improve quicker than out there revenues, resulting in extra borrowing, whereas the potential volatility of the November mid-terms could trigger state and native governments to get forward of that by front-loading issuance subsequent yr and/or accelerating 2027 points into 2026, he stated.

For refundings, the baseline assumption is that “a newly appointed [Federal Reserve] chair spearheads extra aggressive price slicing whilst inflation stays elevated or rises. The previous would enable extra present name exercise, particularly if debtors assume (not unreasonably) that materially decrease charges may very well be very short-term,” Fabian stated.

It is also attainable that governments once more “look to reschedule near-term bond maturities to enhance money circulate flexibility,” he stated.

CreditSights sees quantity at $600 billion subsequent yr, up 5% from 2025’s anticipated complete.

New cash borrowing will improve by 10% to about $385 billion, although the precise determine may very well be larger, “given the latest surge in borrowing for power pre-pay bonds and the nation’s wanted funding in energy technology,” stated Pat Luby, head of municipal technique at CreditSights.

Refunding exercise can even develop, “fueled partly by a need to refinance the $135 billion of bonds with coupon charges of 5% or larger that can develop into callable in 2026,” he stated.

Ramirez additionally predicts provide will likely be at $600 billion, up 4% year-over-year, as “constructive web provide at $100-plus billion may present a headwind for complete returns vs. Treasuries, just like 2025,” stated Peter Block, managing director of credit score technique on the agency.

J.P. Morgan anticipates one other yr of file provide with a complete gross provide of $600 billion — $545 billion of tax-exempt and $55 billion of taxable/muni company CUSIPs — up 7% from the anticipated 2025 quantity of $560 billion, stated strategists led by Peter DeGroot.

Subsequent yr, new-money tax-exempt issuance is estimated at $420 billion, pushed by increasing infrastructure wants and rising prices for development, upkeep, and new improvement, they stated.

The muni market can even see a “rising share of quantity within the infrastructure area associated to knowledge heart load demand from the AI increase,” J.P. Morgan strategists stated.

Tax-exempt refunding quantity is predicted to achieve $125 billion, they stated.

“This improve will not be pushed by the next chance of bonds being known as, as we don’t anticipate decrease yields within the intermediate or lengthy finish of the curve. Somewhat, it displays a bigger pool of refunding candidates,” J.P. Morgan strategists stated.

If charges decline considerably, refunding provide may exceed present projections, they famous.

SWBC sees provide between $580 billion and $600 billion for subsequent yr.

A part of the rise in issuance this yr was inflation and better development and mission prices and these components will carry over into 2026, stated Chris Brigati, managing director and CIO at SWBC.

Moreover, provide will rise as a result of ongoing infrastructure wants should be met, he stated.

Quantity may exceed $600 billion if the economic system improves. Constructive gross home product progress may spur the “shopper facet of the equation,” Brigati stated.

The Bond Purchaser’s market intelligence strategist Jeff Lipton predicts issuance will fall between $570 billion and $590 billion.

The upper year-over-year quantity is “supported by a average decline in anticipated inflation, a decrease price setting, larger 2016 issuance over 2015 issuance (which offers indications for present refunding exercise within the forecast yr), beforehand permitted bond ballots, the pipeline of critically wanted ‘bedrock’ financing, and credit score and general financial situations,” he stated.

New-money and refunding issuance will rise, given the speed setting and the universe of refundable candidates, Lipton stated.

With decrease charges, elevated taxable advance refundings are anticipated, he stated.

In the meantime, policy-driven volatility will doubtless be “tempered” subsequent yr earlier than the November mid-terms, and Lipton believes issuance is extra prone to be front-loaded within the first half of the yr.

FHN Monetary sees issuance basically flat subsequent yr at a forecasted $570 billion, stated strategists Abby Urtz and Ryan Henry.

Many of the surge of latest issuance has come from new initiatives and has been pushed by “sturdy credit score situations, pent-up demand after years of deferring initiatives, and the spend down of stimulus funds that had supported infrastructure funding up till 2024,” they stated.

The impression of the situations, although, is “fading,” indicating that new cash may fall in 2026, which FHN predicts will lower 7% to $399 billion.

Refundings, although, are anticipated to rise 16% year-over-year to $171 billion, Urtz and Henry stated.

“With tax-exempt advance refundings nonetheless off the desk and charges nonetheless too excessive to carry a lot taxable advance refunding provide, most of 2026 refinancing exercise will proceed to return from present refundings,” they stated. “With candidates up 13% over this yr and a forecast for a gradual bull steepening within the curve, we’re prone to see a significant uptick in refunding exercise.”

On the decrease finish, HilltopSecurities sees $555 billion in issuance: $440 billion in new-money issuance and $115 billion in refundings.

“We might be very stunned to see market exercise leap meaningfully over $600 billion,” stated Tom Kozlik, managing director and head of public coverage and municipal technique at HilltopSecurities, noting “not one of the signposts we watch — credit score situations, price range flexibility, financial momentum — are pointing to a different improve, a lot much less a surge.”

“Steadiness sheets have to stabilize earlier than issuers can shoulder extra fastened prices at the next stage,” he stated.

Subsequent yr appears to be one the place quantity eases considerably whereas “staying sturdy” in comparison with long-term expertise, he stated.

“A number of pressures are nudging issuers to sluggish the tempo reasonably than add new fastened prices to their steadiness sheets: the ‘sugar rush’ is over, coverage danger pulled transactions ahead, credit score high quality is normalizing, rising price range pressures, economic system deceleration, steady refunding exercise; and inflation, labor prices and decrease federal help are pressuring budgets,” Kozlik stated.

Barclays expects provide of $520 billion to $530 billion, which might end in one more yr of wholesome web issuance of $190 billion to $200 billion, stated strategists led by Mikhail Foux.

Traits from 2025 will proceed subsequent yr: “2025’s file provide has been pushed largely by new cash; refunding exercise has not elevated that a lot regardless of barely decrease charges, whereas BAB refundings have been additionally slowing till lately and the share of refundings has declined barely,” they stated.

Charges, that are anticipated to “marginally” decline subsequent yr, are the large unknown, Barclays strategists stated.

There will likely be $360 billion of new-money and $165 billion of refundings in 2026, they stated.

“If charges do decline marginally, we’d count on refundings to extend barely in contrast with 2025, with new cash provide taking a small step again because the file excessive exercise this yr has doubtless partially pre-funded issuer wants for 2026,” Barclays strategists stated.

New-money may very well be negatively impacted. The “quantity of bond proposals on ballots handed in early November was the smallest in latest historical past,” they stated.

Taxable issuance is predicted to be just like this yr’s determine of $35 billion to $40 billion, and $10 billion to $15 billion of company CUSIP issuance is predicted, Barclays strategists stated.

[ad_2]