[ad_1]

KanawatTH/iStock by way of Getty Pictures

Pricey Traders,

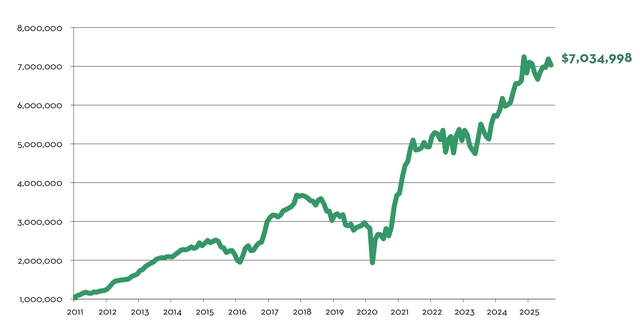

The Portfolio* appreciated +3.0% (web of charges) year-to-date via 9/30/25.

Since inception, Marram has generated +603.5% cumulative return and +14.1% annualized return, web of charges.

For month-to-month particulars, see Historic Efficiency Returns* on the finish of this letter. Additionally, please discuss with your separate account assertion for actual account return figures.

$1,000,000 Funding in Marram (Web Return, Inception 1/1/2011 to 9/30/2025)*

ABOUT MARRAM

Marram is an outsourced long-term funding resolution, targeted on rising wealth for retirement or legacy functions. We started as a service for a small circle of family and friends. Our investor-friendly payment construction (decrease than hedge funds), phrases (separate accounts, no lock-up), and excessive requirements of care and excellence, mirror these origins. Our portfolio supervisor has nearly all of her household’s liquid web price invested in the identical technique – we eat our personal cooking – making certain that we shepherd your funding with the utmost care, as we might our personal.

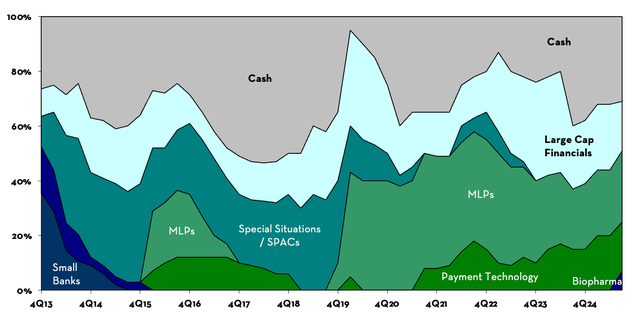

Portfolio Allocations

Under is the goal portfolio allocation – the optimum allocation as of the writing of this letter. Investor separate accounts might differ from this allocation resulting from adjustments in asset costs, availability to accumulate/divest securities within the market, margin & buying and selling capabilities, and tax issues. Over time, all investor separate accounts converge upon the goal portfolio allocation.

- Vitality Infrastructure / Grasp Restricted Partnerships (MLPs): 26% NAV Vitality infrastructure firms with property indispensable to the graceful perform of recent society. These investments have been made in early 2020, profiting from commodity value volatility, shareholder turnover, compelled promoting, and uncertainty associated to the long-term demand of fossil fuels which drove costs to extraordinarily low ranges. Since then, geopolitical strife, inflation, and elevated recognition of the restrictions of renewable power have led market individuals to reembrace fossil fuels, which in flip has lifted the costs of our MLPs. The scale of this allocation peaked at 42% of NAV in late-2021, and has step by step declined resulting from harvested positive factors, trimmed exposures, and M&A exercise. MLPs stay a cornerstone of our portfolio given favorable trade demand dynamics, steady money flows, conservative stability sheets, affordable valuations (at ~10x th Money Circulate), beneficiant money distributions, and inflation safety. See our 2019 4 Quarter and 2021 2 Quarter Letters for our MLP funding thesis.

- Giant-Cap Financials: 18% NAV In March 2023, throughout the temporary U.S. banking disaster, the costs of enormous regional banks fell precipitously as buyers indiscriminately offered shares, permitting us to considerably improve our publicity at fire-sale costs. Since then, our regional financial institution investments have elevated considerably in worth since then, returning on common 31% IRR. Whereas we proceed to view the sector favorably over the long run given its capability to generate regular earnings of ~10%+ yearly, unrealized securities losses have reversed, valuations have expanded, and we’re observing a gradual easing in credit score underwriting requirements throughout the trade. Due to this fact, we prudently moderated our publicity over the previous 15 months, exiting some investments sooner than initially intend. See our 2023 1 Quarter Letter for our Regional Financial institution funding thesis.

- Funds, Monetary, and Know-how Software program: 18% NAV Quick-growing funds, monetary, and expertise software program companies with favorable income tail winds, working in areas with huge untapped complete addressable markets, producing money earnings, actively reinvesting earnings again into the enterprise at excessive incremental margins, and self-funding future development with little/no fairness dilution. We bought these investments at enticing costs that can generate no less than 3X return in 5 years primarily based on affordable topline development & margin assumptions. See our 2022 1 Quarter Letter for extra particulars.

- Biopharma: 7% NAV The biopharma sector is deeply out of favor, weighed down by political and different components which have led to decrease trade $ R&D spend. Taking a long-term view, we imagine society will proceed to want (and demand) new medicine and different well being improvements (weight problems therapies, next-generation vaccines & therapeutics, medical/diagnostic gadgets, and beauty enhancements, and many others.), all of which requires knowledge assortment, rigorous testing, and regulatory validation previous to mass market rollout. With time, we imagine capital will return to the sector and trade $ R&D spend will reaccelerate. We initiated basket diversified allocation by way of ETFs and service-based companies that facilitate knowledge technology, scientific trial design/ implementation, and regulatory navigation. Thereby gaining publicity to restoration of trade $ R&D spend from cyclical lows whereas minimizing adversarial outcomes tied to particular person drug improvement.

- Money & Money Equivalents: 31% NAV This class will fluctuate relying on funding alternatives out there within the market. We accumulate ~4% curiosity and dividends per 12 months which constantly replenishes our money stability.

Portfolio Return* Evaluation & Future Positioning

The Portfolio* return +0.7% (NET) within the third quarter, bringing our year-to-date (YTD) return to +3.0%.

Giant Financials and Vitality Infrastructure investments have been strong contributors to efficiency this 12 months. Nonetheless, our Cost Know-how investments declined on common ~20% YTD, making a significant drag on total returns. We bought extra PayPal (PYPL) and Shift4 (FOUR) at enticing valuations.

Our Funds Know-how basket consists of companies with distinctive long-term upside potential. These are enduring investments that needs to be evaluated over years, not quarters, as their worth compounds step by step via innovation and scale. Constructed on fashionable expertise stacks and led by forward-thinking administration groups, these companies are steadily taking share from legacy incumbents (by serving to their prospects, each companies and shoppers, function and transact extra effectively, quickly, and affordably) whereas additionally benefiting from secular development in digital transactions and the tailwinds of inflation. Within the years forward, they’re positioned to ship sustained income development and working leverage due to larger $ fee volumes piped over largely mounted infrastructure prices.

Through the quarter, we harvested positive factors from Giant Financials, exiting our place in First Horizon (FHN) and trimming Areas (RF). We started reducing publicity over a 12 months in the past, reducing our complete allocation from 37% NAV in 2Q24 to 18% NAV at present. Since March 2023, our regional financial institution investments have return on ~31% IRR on common. We’re exiting some names sooner than initially intend as a result of, whereas we proceed to view the sector favorably given its capability to generate regular earnings of ~10%+ yearly, valuations have expanded, and we’re observing a gradual easing in credit score underwriting requirements throughout the trade. Due to this fact, now we have prudently moderated our publicity over the previous 15 months. Latest proceeds have been reinvested into within the fee expertise and biopharma sectors.

New Basket Allocation: Biopharma

The biopharma sector is deeply out of favor, weighed down by political scrutiny over drug pricing, analysis funding cuts, uncertainty round FDA regulatory approval frameworks, post-pandemic normalization in healthcare spending, lackluster funding efficiency prior to now 3 years, larger value of capital, and shift of enterprise funding away to different areas like AI. All of this has led to decrease complete trade $ R&D spend, valuations, and investor curiosity.

Taking a long-term view, we imagine society will proceed to want (and demand) new medicine, therapeutics, medical gadgets, and different well being improvements, comparable to weight problems therapies, next-generation vaccines & therapeutics, medical/diagnostic gadgets, and beauty enhancements — all of which require knowledge assortment, rigorous testing, and regulatory validation previous to mass market rollout. With time, we imagine capital will return to the sector and trade $ R&D spend will reaccelerate.

Through the quarter, we initiated a 7% NAV basket allocation via two biopharma ETFs, one contract analysis group (CRO) buying and selling at 8% free money circulate yield, and two bio-simulation software program firms at ~5% free money circulate yield, on at the moment depressed complete trade $ R&D spend. By diversifying throughout ETFs and service-based companies that facilitate knowledge technology, scientific trial design / implementation, and regulatory navigation, we acquire publicity to restoration from cyclical lows whereas minimizing adversarial outcomes tied to particular person drug improvement.

Course of Over Final result

In investing, as in life, it’s unproductive to fixate on components exterior of our direct management, such because the habits of different market individuals, day by day value fluctuations, or the vagaries of luck. As a substitute, we focus our brainpower on what we will immediately management: the method by which we make investments. A constantly disciplined funding course of is the inspiration for long-term success. We can not dictate what others pay for property or how safety costs transfer within the market, however we will decide which companies we wish to personal, the costs we’re keen to pay, and whether or not now we have the money liquidity to behave when alternatives come up.

Guided by our course of, now we have compiled an in depth “wishlist” of companies that we wish to personal and the corresponding costs after we would eagerly purchase them. Our ongoing analysis efforts – drawing from SEC filings, earnings stories, displays, administration interviews, commerce publications and books throughout a variety of topics – ensures that this wishlist is constantly increasing and refined as we establish new alternatives and revisit prior concepts with contemporary views.

By concentrating on what we will management — our analysis course of and decision-making framework — we maximize the percentages of reaching favorable outcomes and superior long-term outcomes. The compounding nature of funding data and expertise additional tilts the percentages in our favor. Every passing 12 months sharpens our capability to acknowledge insights not but appreciated or priced by the market, permitting us to behave decisively when alternative emerges. Combining a well-established base of experience with broad curiosity, a persistent seek for new data, and balanced psychological equanimity, we’re nicely positioned to capitalize on future alternatives at any time when and wherever they emerge.

Marram E-book Membership

Should you’re on the lookout for pleasurable studying (and unconventional knowledge), these books will alter your notion of the seen and invisible world that surrounds us.

Please don’t hesitate to succeed in out with any questions. As at all times, thanks on your belief. We look ahead to persevering with our capital compounding adventures within the years forward.

Yours very actually,

Vivian Y. Chen, CFA | Portfolio Supervisor | Marram Funding Administration

APPENDIX: HISTORICAL PERFORMANCE RETURNS (NET OF FEES)*

Editor’s Word: The abstract bullets for this text have been chosen by Searching for Alpha editors.

[ad_2]