")

[ad_1]

We don’t often see the mREITs dramatically outperforming the BDC sector. Nevertheless it certain occurred this yr.

There are a minimum of two components in play:

- Quick-term charges are falling.

- Bankruptcies by a number of debtors are making buyers skittish about different unrelated loans.

We’re going to deal with the latest relative power within the mortgage REITs this time, as we talked about BDCs final time:

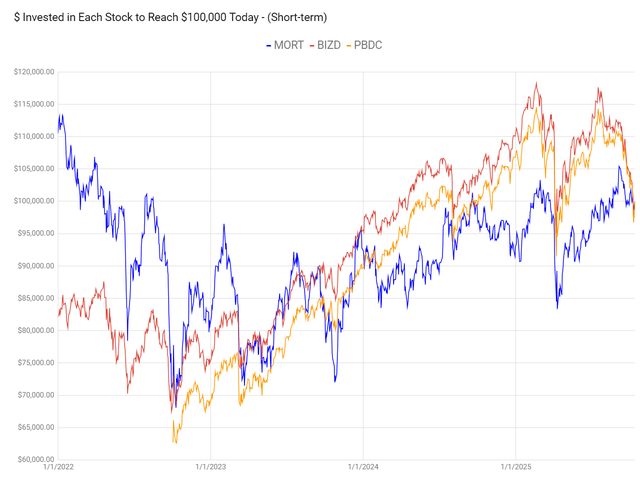

We are able to use the $100,000 chart to match the latest efficiency for some sector-based ETFs:

The REIT Discussion board

As a result of this chart is constructed across the values right now, it does a a lot better job of demonstrating how prior investments would’ve executed based mostly on any doable date vary. Who desires a chart that anchors every part to an arbitrary start line? In our chart the ending level is likely to be arbitrary, however “right now” is often probably the most helpful arbitrary date you will get. Sorry, I can’t offer you two years sooner or later. Nevertheless, our charts do an amazing job of adjusting for the dividends. As a result of once you’re investing in shares with large yields, you really want to issue that into the calculations. Large yields usually are not free. They arrive with dangers, and they’re a serious a part of the return image.

The Mortgage REIT ETF

We’re utilizing the VanEck Mortgage REIT Earnings ETF (NYSEARCA:MORT) to symbolize mortgage REITs and utilizing the VanEck BDC Earnings ETF (BIZD) and Putnam BDC Earnings ETF (PBDC) to symbolize the BDCs. Within the chart above, it is clear that MORT outperformed ranging from any level within the final 12 months. In some instances, the outperformance was substantial.

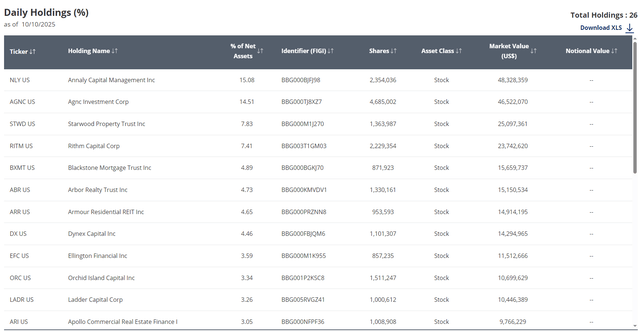

So what’s occurring? Properly, first we must always have a fast take a look at the holdings:

VanEck

The highest two positions are in mortgage REITs targeted on company mortgage-backed securities. Company mortgage REITs are significantly delicate to rates of interest. Nevertheless, many individuals misunderstand the publicity.

The Misperception

Many individuals suppose that mortgage REITs, and particularly company mortgage REITs, merely profit from decrease rates of interest. Nevertheless, that is not the case. If mortgage charges decline dramatically, that has a unfavorable affect on mortgage REITs as a result of it results in a surge in prepayments on mortgages that had increased coupon charges. That may be dangerous for the mortgage REITs.

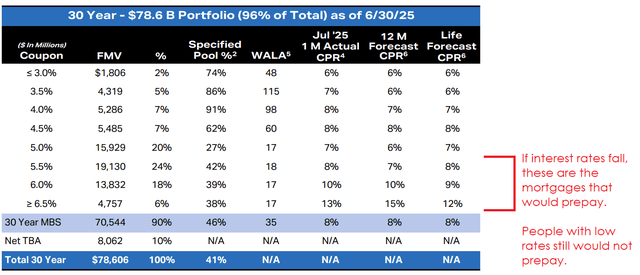

Right here’s an instance utilizing the holdings from AGNC’s portfolio:

AGNC

There are three main methods somebody might prepay their mortgage:

- They pay it off by refinancing.

- They pay it off as a result of they’re promoting the home.

- They pay it off by paying additional principal together with their cost.

What sort of prepayment surges when charges fall? It’s the primary possibility. Individuals with higher-rate mortgages refinance into lower-rate mortgages.

My condolences to everybody who didn’t have an opportunity to purchase a house within the final 17 years. There have been some fairly good alternatives. I might pay additional on my mortgage, however I gained’t. It’s locked in at 2.125%. Why would I pay additional for that? I simply choose up short-term Treasuries (okay, a Treasury Invoice ETF). I nonetheless get the pliability of getting money, and I get greater than sufficient curiosity to offset the price of the mortgage.

What if Charges Rise?

At present, all the main focus is on charges falling. However we must always a minimum of handle the opposite potential situation. Mortgage REITs don’t need charges to extend considerably as a result of:

- The worth of their MBS holdings would decline.

- The price of financing would improve.

- The prepayments on their MBS would decline an excessive amount of, which might make it take longer to get their a refund to reinvest.

What Mortgage REITs Can Do

If charges reverse and climb increased as an alternative, then mortgage REITs would step by step shift into higher-yielding mortgages, but it surely takes time. They may dump lower-yielding mortgages in that situation, however they’d be compelled to just accept a lot decrease costs. Consequently, they usually desire to be rather less energetic in managing the portfolio. In brief, the mortgage REIT would like that rates of interest not improve or lower dramatically.

What About Fed Funds Charges?

Mortgage REITs do stand to learn from a discount within the Fed Funds Fee. They usually hedge lower than the whole thing of their borrowing prices, and when that occurs, it permits them to learn from decrease short-term charges. Sadly, many buyers appear to suppose that mortgage REITs will solely hedge a really small portion of their publicity to funding prices. That may be horribly inaccurate. They usually hedge the substantial majority, a minimum of for the quick to medium time period. There have been occasions after we’ve seen them hedge greater than 100%.

The best situation for mortgage REITs includes mortgage charges remaining comparatively secure with a really gradual decline within the Fed Funds Fee.

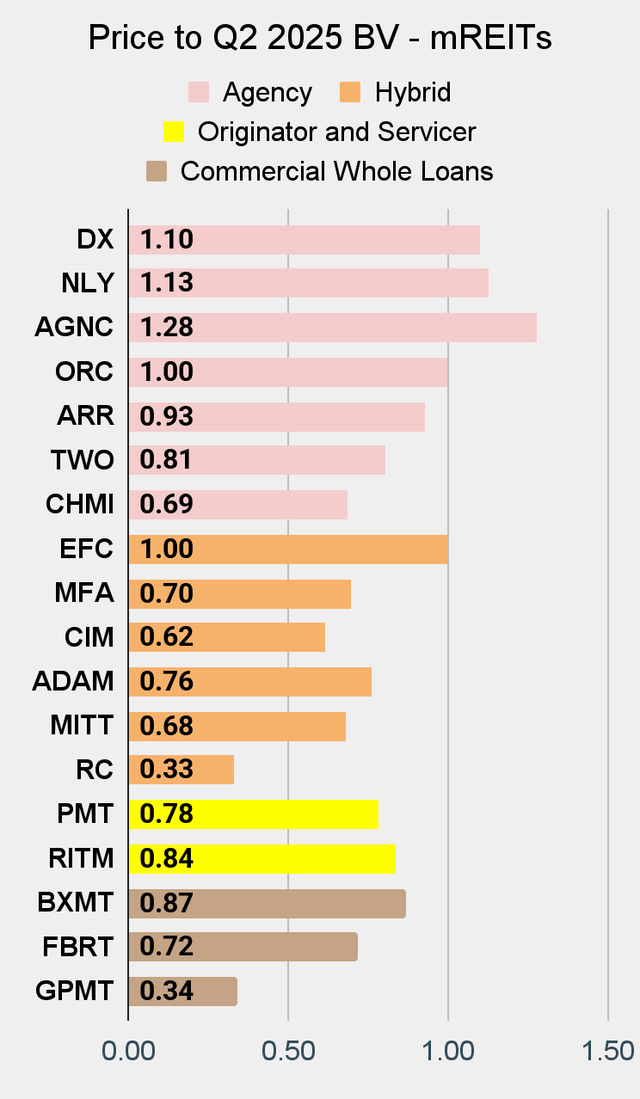

After we take a look at the most important mortgage REITs, that are additionally the highest two holdings in MORT, we see pretty excessive valuations. Their price-to-book worth utilizing our latest estimates is about 1.08x and 1.23x. That’s decrease than the ratio within the chart. By our estimate, ebook values for these mortgage REITs have in all probability elevated by about 4% to five% between 6/30/2025 and final Friday. Sure, we run our estimates fairly often. The modifications in ebook worth we’re projecting all through the sector are materially totally different, although. Whereas Annaly (NLY) and AGNC (AGNC) have been fairly comparable to one another, a number of the mortgage REITs are more likely to report declines in ebook worth per share for Q3 2025.

Do I Like Mortgage REITs Right here?

There are some alternatives. A couple of are costly, however there are a handful which might be getting fairly low cost. For frequent shares, I’ve been extra energetic within the BDCs than within the mortgage REITs currently. Simply profiting from that massive slide in BDC costs. Nevertheless, I would choose up a number of the mortgage REIT frequent shares as properly. It’s not a foul time, however I might wish to choose these entries fastidiously.

I am usually extra fascinated about discovering alternatives to commerce in most popular shares and child bonds. We nonetheless get a horny yield, however the costs are a lot steadier. That’s nonetheless my normal theme. I’ll hold in search of alternatives to allocate to the popular shares and child bonds, however with the latest weak point, I am beginning to tackle a bit extra frequent share publicity once more.

I will disclose an additional commerce right here. Whereas AGNC and NLY are the largest company mortgage REITs, we have usually been extra fascinated about Dynex (DX). Scott Kennedy initiated a place in DX in late September at $11.95 and bought it slightly below per week in the past at $13.05. Easy buying and selling round price-to-book ratios.

Evaluation Technique

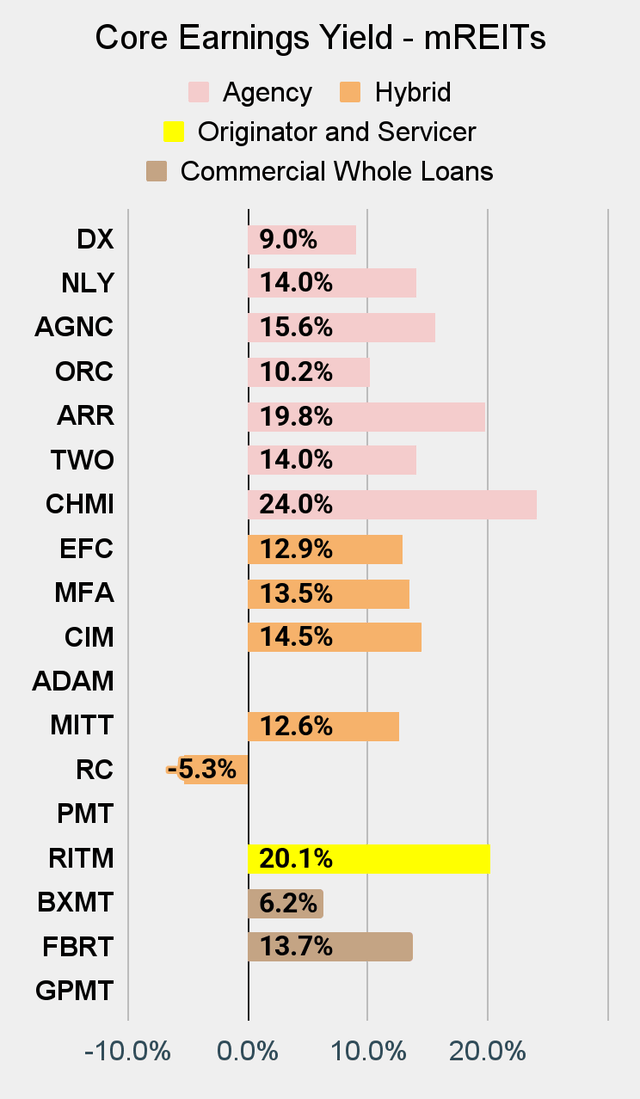

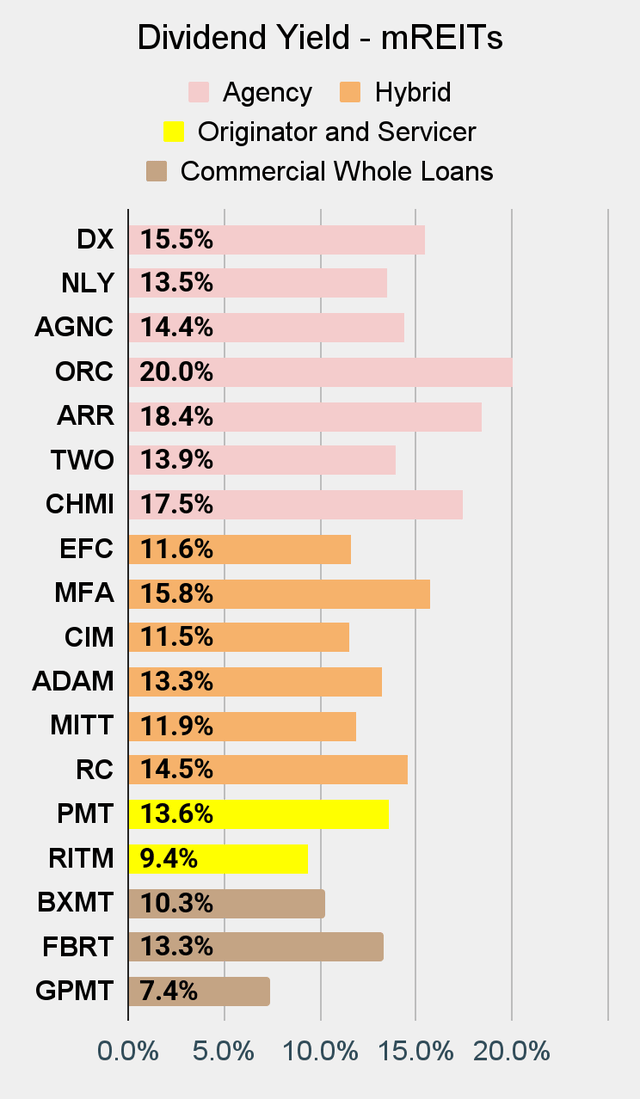

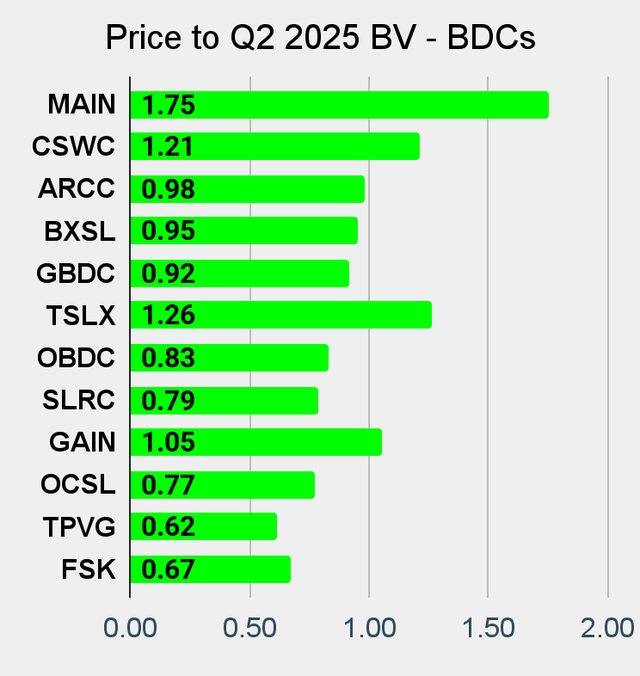

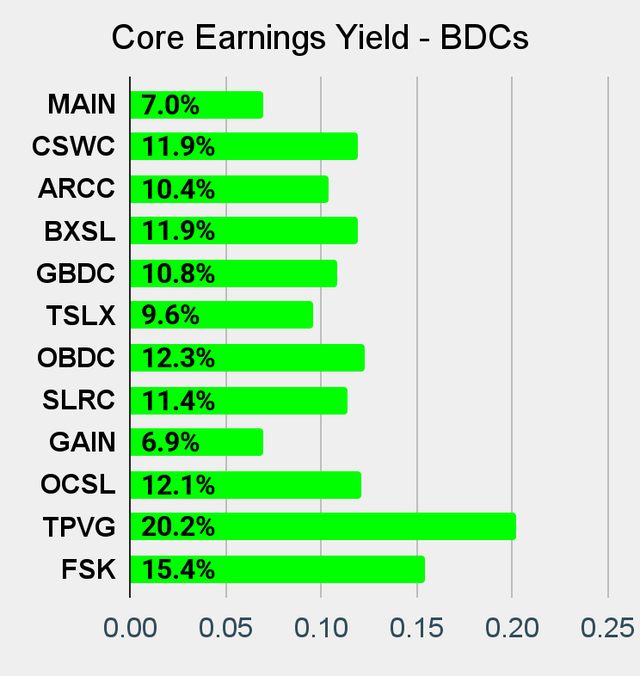

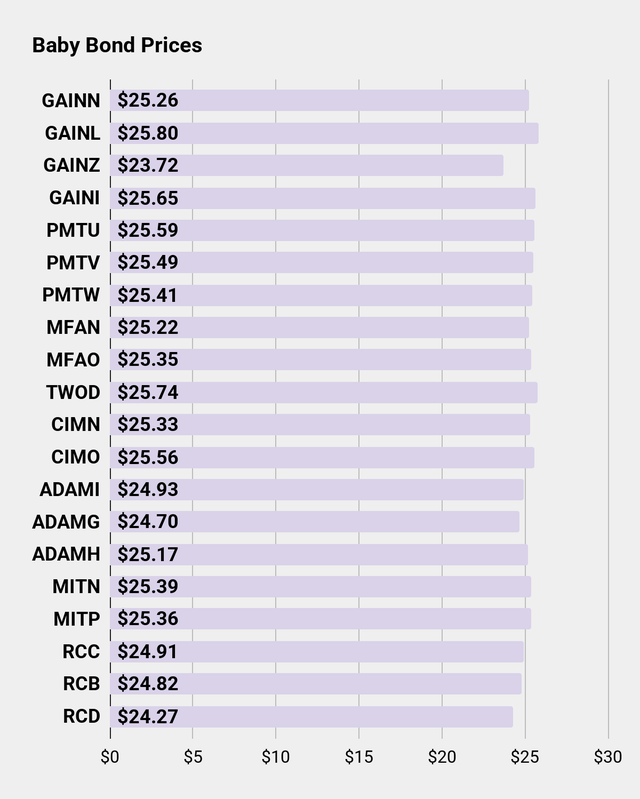

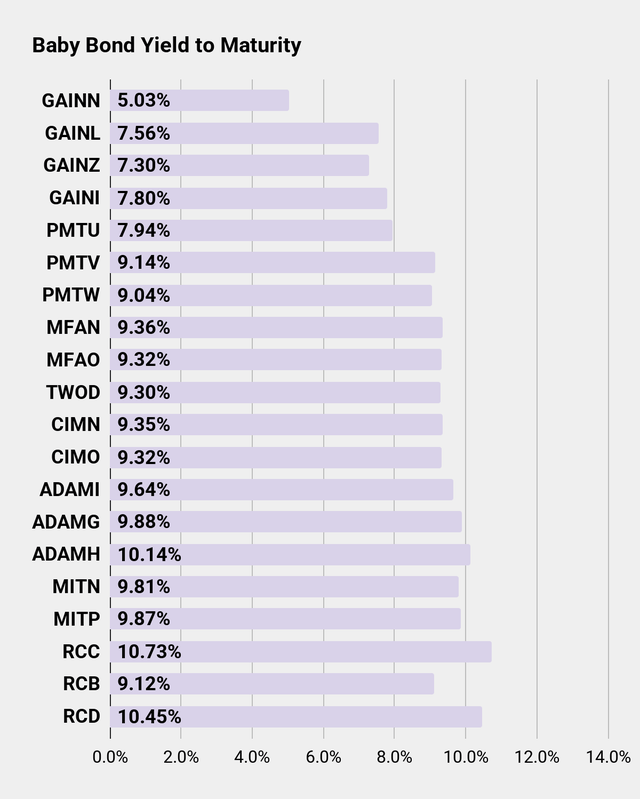

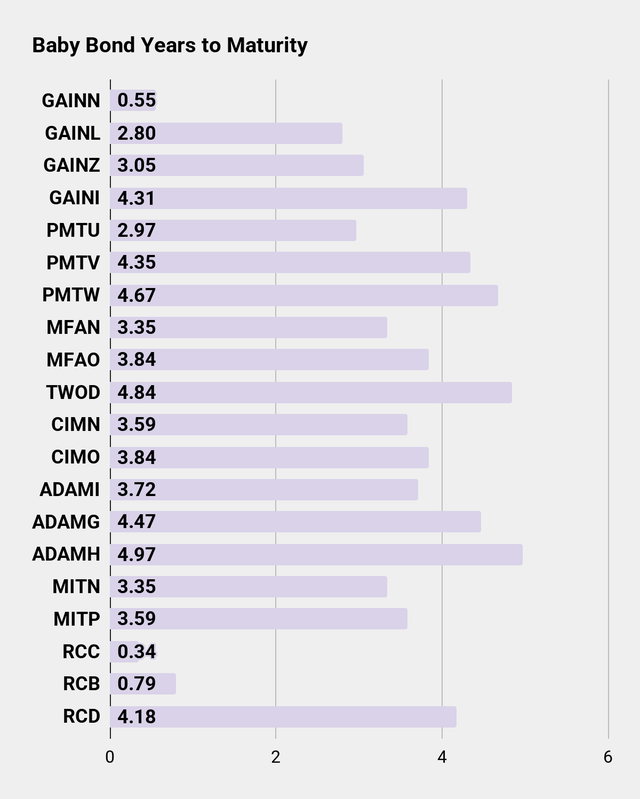

We’re always engaged on offering new up to date estimates for BV (ebook worth) and NAV (internet asset worth) in The REIT Discussion board. Nevertheless, many buyers fail to even examine the trailing values. On this collection, we calculate the price-to-trailing BV or NAV for a lot of mortgage REITs and BDCs in addition to offering a number of metrics on child bonds and most popular shares. Charts for these issues can be found close to the tip of the article.

We emphasize price-to-BV and price-to-NAV as a result of these metrics present perception into valuations.

All of the Shares

The charts examine the next corporations and their most popular shares or child bonds:

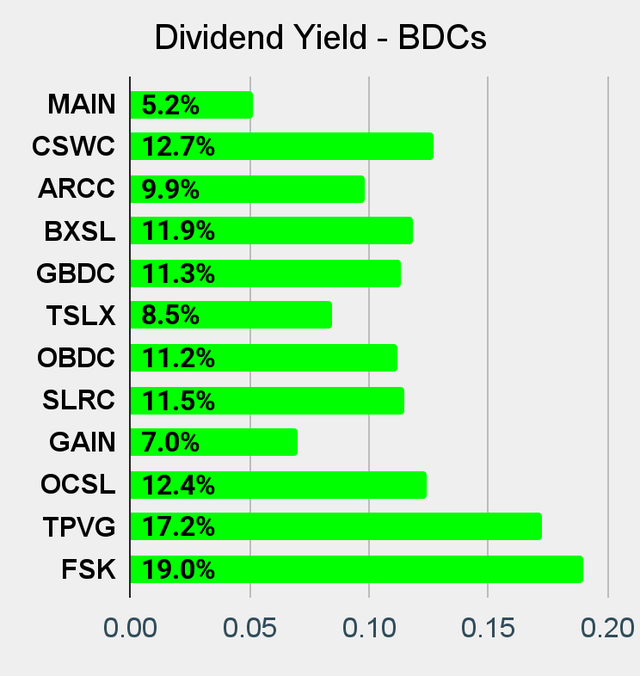

- BDCs: (CSWC), (BXSL), (TSLX), (OCSL), (GAIN), (TPVG), (FSK), (MAIN), (ARCC), (GBDC), (OBDC), (SLRC)

- Business mREITs: (GPMT), (FBRT), (BXMT)

- Residential Hybrid mREITs: (MITT), (CIM), (RC), (MFA), (EFC), (ADAM)

- Residential Company mREITs: (NLY), (AGNC), (CHMI), (DX), (TWO), (ARR), (ORC)

- Residential Originator and Servicer mREITs: (RITM), (PMT)

Observe: NYMT not too long ago modified their ticker to ADAM. The brand new ticker is included in our charts. The newborn bonds and most popular shares additionally modified tickers, with NYMT being changed by ADAM inside every ticker. For example, NYMTZ grew to become ADAMZ.

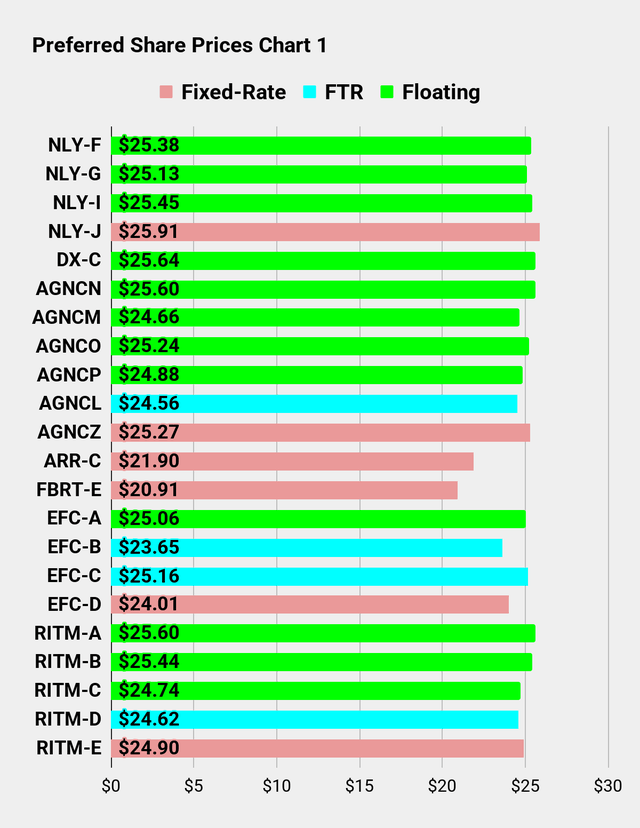

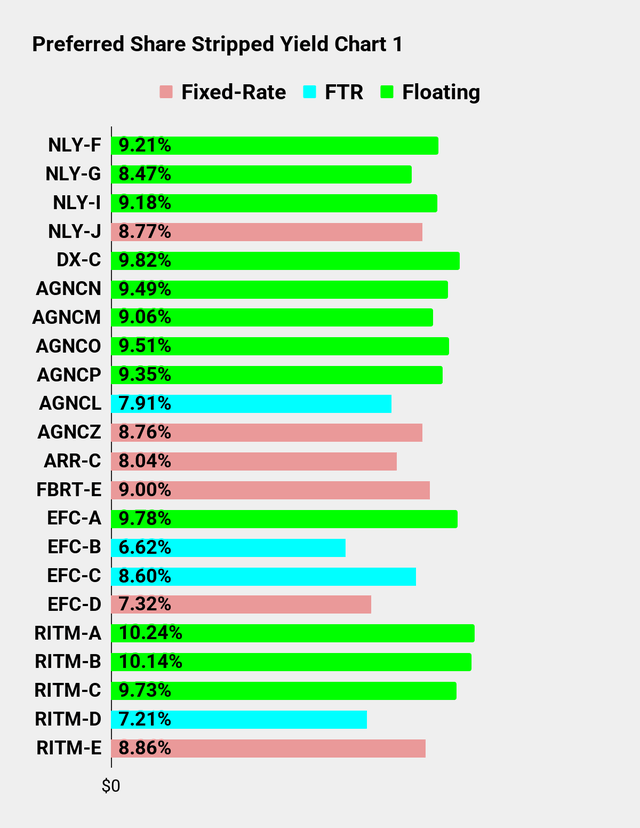

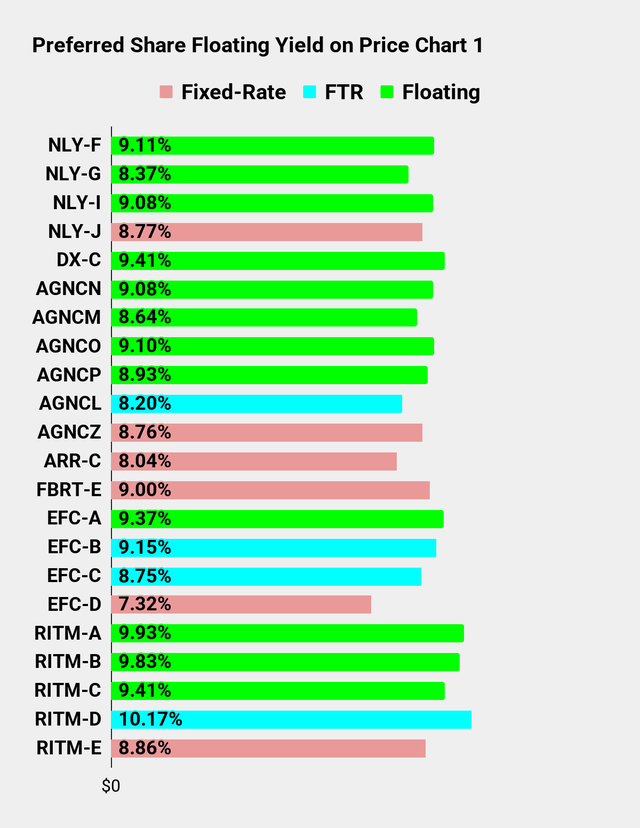

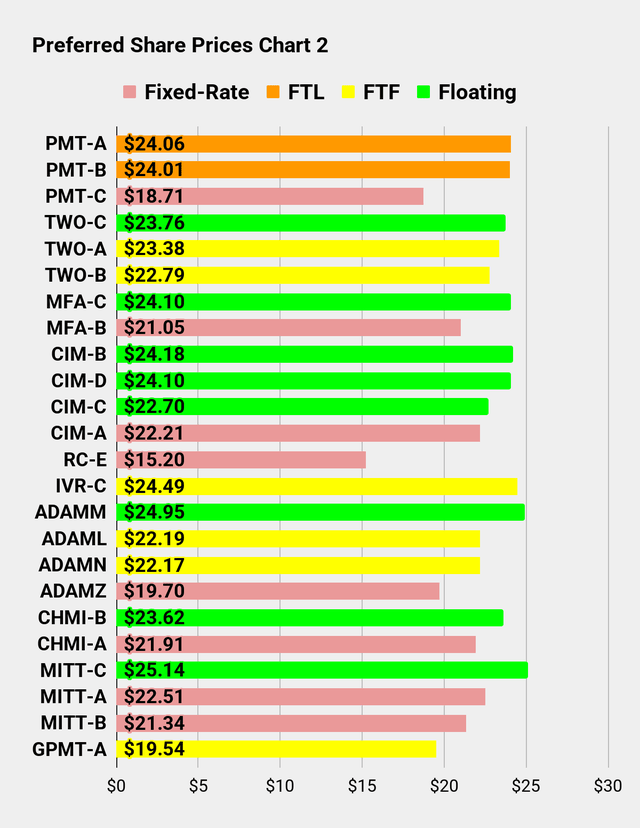

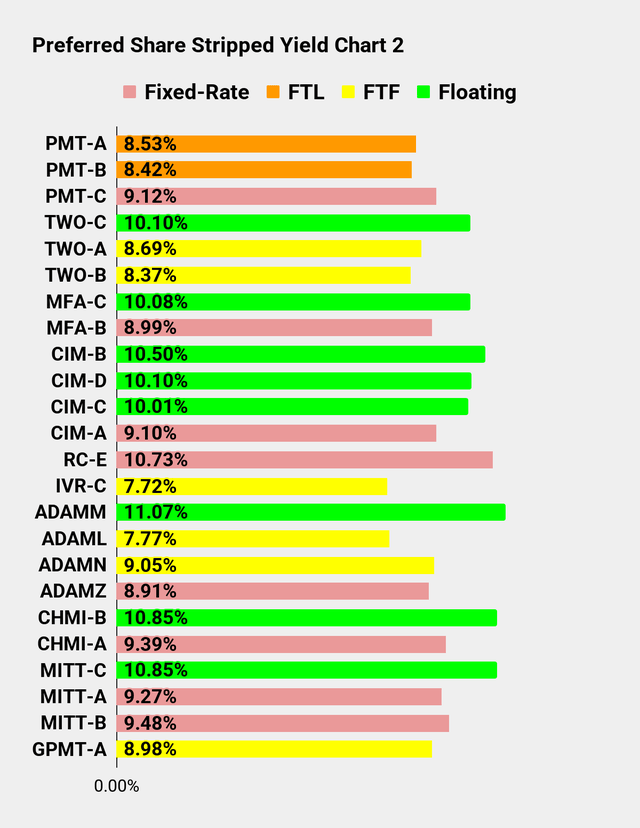

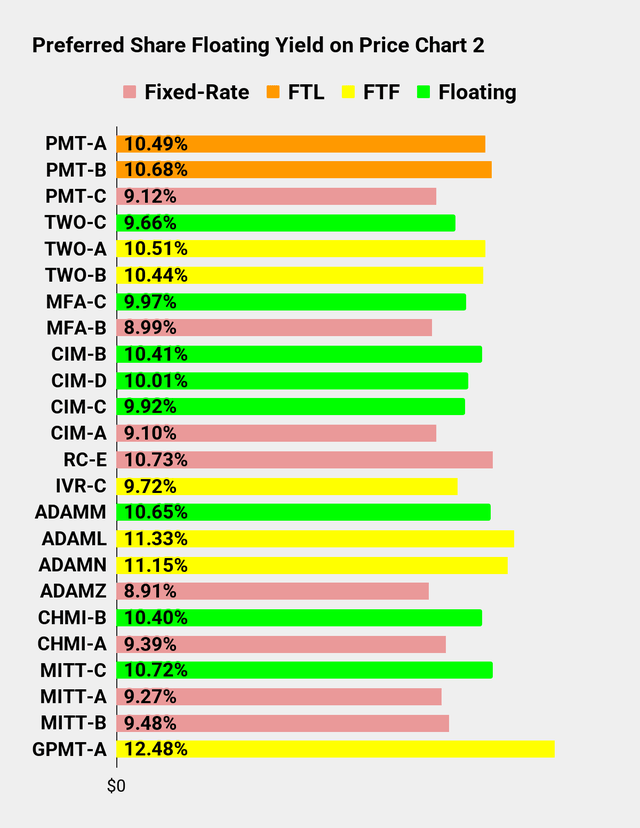

Embedded Charts

Mortgage REITs and BDCs:

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

Most popular shares and child bonds:

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

The REIT Discussion board |

Thanks for studying, and I hope you loved the charts.

Some terminology:

- FTF = Fastened-to-floating. Share is presently mounted however will start floating based mostly on SOFR. We might reference LIBOR, however that is assumed to be SOFR + 0.26161%.

- FTR = Fastened-to-reset. Share is presently mounted. It is going to finally start resetting each 5 years based mostly on the 5-year Treasury price.

- FTL = Fastened-to-lawsuit. The corporate determined that their FTF shares could possibly be “fixed-to-fixed” regardless of clearly violating the unique intent of the contract.

- Floating = A share that was FTF however is now floating. The dividend price is up to date each three months.

Thank You

Editor’s Observe: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

[ad_2]