[ad_1]

Municipals began September barely weaker, as U.S. Treasury yields rose and equities ended down.

The 2-year muni-UST ratio Monday was at 60%, the five-year at 64%, the 10-year at 75% and the 30-year at 93%, in response to Municipal Market Information’s 3 p.m. ET learn. ICE Information Companies had the two-year at 61%, the five-year at 65%, the 10-year at 75% and the 30-year at 94% at a 4 p.m. learn.

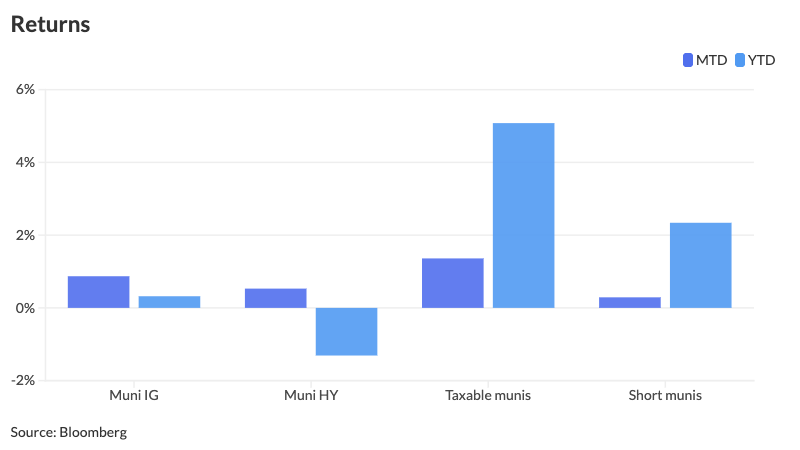

Due to robust technicals and the anticipated rate of interest lower by the Federal Reserve at its September assembly, municipal bonds posted constructive returns of 0.87% in August, reversing their losses of 0.20% in July, in response to Jason Wong, vp municipals at AmeriVet Securities.

That pushed year-to-date returns to 0.32%

“Muni yields noticed bumps of 13 foundation factors within the 2026-2029 maturities for the month,” he stated. “The 2030-2034 maturities noticed bumps of 4 to 10 foundation factors, whereas the 2037-2055 maturities noticed cuts of 1 to 4 foundation factors.”

Munis outperformed Treasuries, Wong stated.

The 2-year muni-UST ratio, which started August at 63.32%, ended the month at 60.95%. Likewise, the five-year ratio ended the month at 64.13% in comparison with 65.59% firstly of August. The ten-year ratio narrowed barely through the month to 75.71% from 75.88%, whereas the 30-year ratio fell to 95.20% from 95.98%.

Secondary buying and selling quantity totaled simply over $41.07 billion for the month, with 54% of secondary buying and selling being supplier sells, Wong stated.

Mutual fund inflows continued to extend final month, each within the investment-grade and high-yield realms, Robert Lind of Lind Capital Companions famous within the agency’s Municipal Market Commentary.

After rising three out of 4 weeks in August, each IG and HY funds “have now skilled weekly inflows in 16 out of the final 18 weeks relationship again to the top of April,” Lind famous. “Each funding grade and high-yield inflows eclipsed $2 billion in August, totaling roughly $4.5 billion.”

September is shaping as much as be a “difficult month for munis,” Wong stated, noting munis have had solely two constructive returns on this month during the last 10 years.

“With buyers anticipating a fee lower later within the month, this might push munis to underperform Treasuries,” though munis should still eke out constructive returns for September, he stated.

When the Fed began its easing cycle September 2024, “munis noticed a median bump of about eight foundation factors throughout the curve,” Wong stated noting it was a 50-basis level lower. “Moreover, munis did present a return of slightly below 1%. We might see comparable outcomes if there’s a fee lower,” he stated.

“In what was largely an in any other case sleepy month, August was outlined by Fed Chair Powell’s dovish commentary,” delivered on the Fed’s Jackson Gap symposium, Lind stated. “Broader volatility was typically range-bound and managed, although fastened revenue yields ended the month principally decrease, because the Fed opened the door to potential fee cuts within the months forward.”

“After a file breaking first-half of the 12 months, municipal provide felt prefer it took a breather in August,” however approached $50 billion, Lind stated.

August quantity was $48.465 billion, a 4.8% lower from $50.933 billion final 12 months, as blended financial information induced Federal Reserve uncertainty and saved issuers on the sidelines whereas the variety of megadeals fell.

Issuance year-to-date is $386.689 billion, up 14.9% from $336.478 billion over the identical interval in 2024.

Non-rated and below-investment-grade issuance “stays subdued versus the trailing five- and 10-year averages, particularly when in comparison with the numerous [year-over-year] enhance in investment-grade issuance,” Lind famous. “These days, the non-rated major market is seeing a significant proportion of recent offers get hung up through the pricing course of, as underwriters wrestle to acquire anchor orders. Finally, this compels the underwriter and borrower to strengthen credit score covenants, enhance yields, or watch for improved market situations.”

AAA scales

MMD’s scale noticed small cuts: The one-year was at 2.19% (+1, no Sept. roll) and a couple of.21% (+1, no Sept. roll) in two years. The five-year was at 2.38% (+1, no Sept. roll), the 10-year at 3.23% (+1, no Sept. roll) and the 30-year at 4.62% (+1) at 3 p.m.

The ICE AAA yield curve was lower as much as three foundation factors: 2.25% (unch) in 2026 and a couple of.22% (+2) in 2027. The five-year was at 2.42% (+2), the 10-year was at 3.18% (+2) and the 30-year was at 4.62% (+3) at 4 p.m.

The S&P World Market Intelligence municipal curve was lower one to 2 foundation factors: The one-year was at 2.19% (+1) in 2025 and a couple of.21% (+1) in 2026. The five-year was at 2.38% (+2), the 10-year was at 3.24% (+1) and the 30-year yield was at 4.62% (+2) at 4 p.m.

Bloomberg BVAL was lower a foundation level: 2.18% (+1) in 2025 and a couple of.20% (+1) in 2026. The five-year at 2.36% (+1), the 10-year at 3.19% (+1) and the 30-year at 4.59% (+1) at 4 p.m.

Treasuries noticed losses.

The 2-year UST was yielding 3.648% (+3), the three-year was at 3.617% (+4), the five-year at 3.735% (+4), the 10-year at 4.273% (+5), the 20-year at 4.919% (+5) and the 30-year at 4.971% (+4) close to the shut.

Major to return

The Dormitory Authority of the State of New York (Aa1//AA+/) is ready to cost Thursday $2.337 billion of basic function state private revenue tax income bonds, Sequence 2025C. BofA Securities.

The Massachusetts Faculty Constructing Authority (/AA/AA+/) is ready to cost Thursday $1.892 billion of social bonds, consisting of $488.845 million of subordinated devoted gross sales tax bonds, Sequence 2025A, and $1.404 billion of refunding bonds, Sequence 2025B, BofA Securities.

The Michigan State Housing Improvement Authority (/AA+//) is ready to cost Thursday $360.06 million of rental housing income bonds, Sequence 2025A-1. BofA Securities.

The Los Angeles Division of Water and Energy (Aa2//AA-/AA) is ready to cost Thursday $166.045 million of water system income bonds, Sequence 2025B. BofA Securities.

Delray Seashore, Florida, (Aa3/AA-//) is ready to cost Wednesday $149.01 million of water and sewer income enchancment bonds. BofA Securities.

The Regents of the College of Colorado (Aa1//AA+/) is ready to cost Thursday $140.535 million of college enterprise income bonds, consisting of $76.555 million of Sequence C-1 and $63.98 million of Sequence C-2 refunding bonds. Stifel.

The Connecticut Well being and Academic Services Authority (A3/A-//) is ready to cost Thursday $129.66 million of Quinnipiac College situation income refunding bonds, Sequence O. Barclays.

The Riverside Unified Faculty District (Aa2///) is ready to cost Thursday $106.33 million of GOs, consisting of $40 million of Election of 2016 GOs, Sequence D, and $66.33 million of 2025 GO refunding bonds. Piper Sandler.

Aggressive

The Santa Clara Unified Faculty District, California, (Aaa/AAA/) is ready to promote $190 million of Election of 2018 GOs, at 11:05 a.m. Japanese on Wednesday.

Brownsville, Texas, (Aa3/AA+/) is ready to promote $143.86 million of mixture tax and income certificates of obligation, Sequence 2025A, at 11 a.m. on Thursday.

The Hartford County Metropolitan District, Connecticut, set to promote $100 million of GOs at midday on Thursday.

Jessica Lerner contributed to this story.

[ad_2]