[ad_1]

Municipals have been regular Thursday as U.S. Treasuries cheapened and equities bought off because the upcoming flurry of financial reviews following the top of the federal government shutdown spurred uncertainty over the Federal Reserve’s subsequent transfer.

The 2-year muni-UST ratio Thursday was at 69%, the five-year at 65%, the 10-year at 67% and the 30-year at 88%, in response to Municipal Market Knowledge’s 3 p.m. EDT learn. ICE Knowledge Companies had the two-year at 69%, the five-year at 65%, the 10-year at 67% and the 30-year at 88% at a 4 p.m. learn.

“After six weeks of uncertainty, the federal authorities is funded and operational once more,” mentioned Tom Kozlik, managing director and head of public coverage and municipal technique at HilltopSecurities.

Congress handed and President Donald Trump signed laws to reopen the federal authorities Wednesday evening, as “nationwide parks, passport places of work, and federal packages are resuming, and airport operations ought to stabilize quickly,” he mentioned.

Nevertheless, the settlement solely extends funding by way of Jan. 30, 2026, establishing one other “potential deadline cliff,” Kozlik mentioned.

The tip of the “knowledge blackout” carries better weight for traders because the absence of key financial indicators left markets with no full view, he mentioned.

“With official knowledge returning, portfolios can start to recalibrate utilizing verified numbers,” Kozlik mentioned. “The fog is lifting. Whereas the trail forward is not totally clear, visibility is enhancing.”

There’s a shift for muni traders from “assumption-based planning to data-informed selections,” he mentioned.

Labor market situations, development expectations, and credit score tendencies shall be reassessed as new data comes out, as “every knowledge launch is more likely to sharpen our view, permitting traders to maneuver from cautious positioning towards assured, extra well-informed selections for the rest of 2025,” Kozlik mentioned.

For munis, the top of the shutdown helps regular the backdrop, mentioned James Pruskowski, an investor and market strategist.

“Spreads on bonds tied to federal switch funds ought to tighten as headline threat fades, whereas higher visibility from Washington will encourage extra issuance,” he mentioned.

“With tax-loss swapping season in full swing, volatility and concessions are more likely to rise, creating home windows for extra opportunistic patrons so as to add worth,” Pruskowski added.

Elsewhere, since October, munis have skilled a considerably constructive shift, mentioned John Miller, head and CIO of First Eagle’s high-yield municipal credit score group.

Whereas the asset class has lagged different fixed-income property in whole returns this 12 months, that is extra technicals, sentiment and absorbing report provide than it’s something “essentially unsuitable” with the muni market, he mentioned.

Given all of the occasions which have occurred and the way munis have held up and absorbed all this provide, issues are shaping up for a robust fourth quarter, he mentioned.

October normally is a comfortable month for munis. There was a “great” quantity of provide final month, however the muni market carried out properly, each on a relative and absolute foundation, and this pattern is constant by way of November, in response to Miller.

A mixture of things ought to bode fairly properly for munis, together with an estimated $48 billion of reinvestment proceeds from coupons and calls in November, and an extra estimated $53 billion of reinvestment proceeds in December, he mentioned.

“So even when we have been at a strong run fee of provide, it is not going to be practically that top,” Miller mentioned.

In the meantime, the quantity of inflows year-to-date is much like the quantity final 12 months over the identical time interval, however the “composition” differs, he famous.

This 12 months, the “composition” is extra exchange-traded funds, whereas final 12 months, it was extra mutual fund-driven, Miller mentioned.

Each ETFs and mutual funds are at present taking in cash, he mentioned.

“So that you mix that with strong reinvestment revenue, after which you may take completely different bets on the Federal Reserve assembly for Dec. 10,” Miller mentioned.

Since knowledge has not been launched within the final month, whether or not the Fed will reduce charges once more at its December assembly might rely on the inflow of October knowledge, although Miller believes the Fed will ease.

“Because the Fed heads towards its December assembly, the coverage path stays large open,” mentioned Seema Shah, chief international strategist for Principal Asset Administration. “To our minds, a 25-basis-point reduce taking the Fed funds fee nearer towards the center of the estimated impartial vary appears believable, adopted by a pause in early 2026 whereas officers assess the lagged results of prior tightening.”

Within the main market Thursday, Jefferies preliminarily priced for Chicago (/A+/A+/A+/) on behalf of

The second tranche, $457.745 million of non-AMT Collection F bonds, noticed 5s of 1/2043 at 4.01%, 5s of 2045 at 4.20%, 5s of 2048 at 4.38%, 5.25s of 2055 at 4.51% and 5.25s of 2060 at 4.59%, callable 1/1/2035.

The third tranche, $21.72 million of AMT Collection G refunding bonds, noticed 5s of 1/2026 at 3.25%, 5s of 2030 at 3.25%, 5s of 2035 at 3.50% and 4s of 2037 at par, callable 1/1/2035.

Wells Fargo priced for Miami-Dade County, Florida, (Aa3/AA/AA-/AA/) $993.665 million of water and sewer system income bonds. The primary tranche, $574.525 million of Collection A bonds, noticed 5s of 10/2027 at 2.60%, 5s of 2030 at 2.62%, 5s of 2035 at 2.94%, 5s of 2040 at 3.53%, 5s of 2047 at 4.13%, 4.5s of 2051 at 4.65% and 5s of 2055 at 4.52%, callable 10/1/2035.

The second tranche, $419.14 million of Collection B refunding bonds, noticed 5s of 10/2026 at 2.68%, 5s of 2030 at 2.62%, 5s of 2035 at 2.94%, 4s of 2040 at 4.03% and 4s of 2042 at 4.15%, callable 10/1/2035.

Morgan Stanley priced for the Los Angeles Municipal Enchancment Corp. (/A+/AA//) for the Los Angeles Conference Heart $960.645 million of lease income bonds. The primary tranche, consisting of $844.475 million of tax-exempt Collection 2025-A, noticed 5s of 5/2034 at 2.60%, 5s of 2035 at 2.74%, 5s of 2040 at 3.47%, 5s of 2045 at 4.08%, 5.25s of 2050 at 4.37%, 5.5s of 2055 at 4.44% and 5s of 2055, callable 5/1/2035.

The second tranche, $116.17 million of taxable Collection 2025-B bonds, noticed all bonds value at par: 4.051s of 5/2029, 4.101s of 2030 and 4.745s of 2034.

Barclays priced for the College of Delaware (Aa1/AA+//) $309.83 million of tax-exempt bonds, Collection 2025A, with 5s of 11/2026 at 2.59%, 5s of 2030 at 2.51%, 5s of 2035 at 2.88%, 5s of 2040 at 3.42%, 5s of 2045 at 3.99%, 5s of 2050 at 4.27% and 5s of 2055 at 4.34%, callable 11/1/2034.

BofA Securities priced for the Central Florida Expressway Authority (Aa3/AA-//) $276.995 million of senior lien income bonds, Collection 2025A, with 5s of seven/2029 at 2.63%, 5s of 2030 at 2.59%, 5s of 2035 at 2.93% and 5s of 2039 at 3.39%, callable 7/1/2035.

Morgan Stanley priced for the Massachusetts Improvement Finance Company (Aa1/AA+//) $144.6 million of Wellesley School Problem income bonds, Collection N, with 5s of seven/2026 at 2.56%, 5s of 2030 at 2.42%, 5s of 2036 at 2.90%, 5s of 2040 at 3.39% and 5s of 2042 at 3.65%, callable 7/1/2035.

Within the aggressive market, the Virginia Housing Improvement Authority (Aa1/AA+//) bought $102.78 million of non-AMT rental housing bonds, 2025 Collection F, to Raymond James, with all bonds priced at par: 2.75s of 6/2028, 2.8s of 6/2030, 2.9s of 12/2030, 3.45s of 6/2035, 3.5s of 12/2035, 4s of 12/2040, 4.45s of 12/2045, 4.6s of 12/2050, 4.625s of 12/2056, 4.7s of 12/2061 and 4.75s of 12/2067.

Fund flows

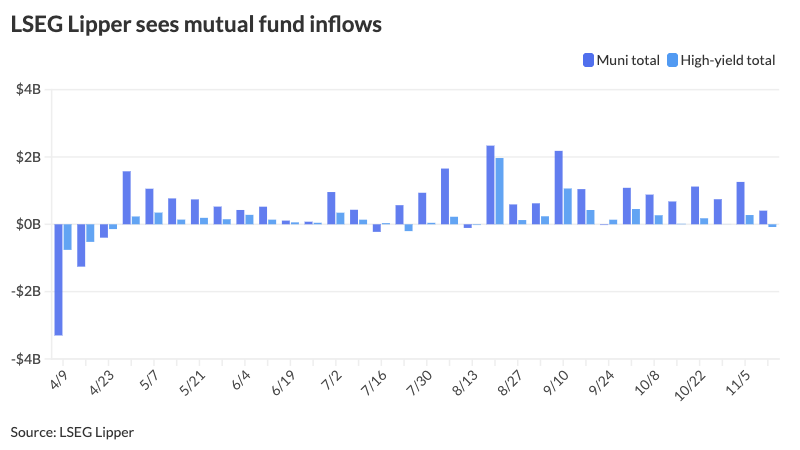

Buyers added $405.3 million to municipal bond mutual funds within the week ended Wednesday, following $1.259 billion of inflows the prior week, in response to LSEG Lipper knowledge.

Excessive-yield funds noticed outflows of $80.6 million in comparison with inflows of $275.2 million the earlier week.

Tax-exempt municipal cash market funds noticed inflows of $2.194 billion for the week ending Nov. 11, bringing whole property to $143.041 billion, in response to the Cash Fund Report, a weekly publication of EPFR.

The typical seven-day easy yield for all tax-free and municipal money-market funds fell to 2.30%.

Taxable money-fund property noticed $18.279 billion pulled, bringing the overall to $7.341 trillion.

The typical seven-day easy yield was at 3.63%.

The SIFMA Swap Index was at 2.45% on Wednesday in comparison with the earlier week’s 2.68%.

AAA scales

MMD’s scale was unchanged: 2.54% in 2026 and a pair of.46% in 2027. The five-year was 2.41%, the 10-year was 2.75% and the 30-year was 4.14% at 3 p.m.

The ICE AAA yield curve was little modified: 2.55% (unch) in 2026 and a pair of.46% (unch) in 2027. The five-year was at 2.40% (unch), the 10-year was at 2.75% (unch) and the 30-year was at 4.10% (+1) at 4 p.m.

The S&P World Market Intelligence municipal curve was unchanged: The one-year was at 2.54% in 2025 and a pair of.45% in 2026. The five-year was at 2.40%, the 10-year was at 2.75% and the 30-year yield was at 4.12% at 3 p.m.

Bloomberg BVAL was unchanged: 2.52% in 2025 and a pair of.47% in 2026. The five-year at 2.37%, the 10-year at 2.71% and the 30-year at 4.04% at 4 p.m.

Treasuries have been weaker.

The 2-year UST was yielding 3.592% (+2), the three-year was at 3.59% (+3), the five-year at 3.706% (+3), the 10-year at 4.114% (+4), the 20-year at 4.68% (+4) and the 30-year at 4.707% (+4) close to the shut.

[ad_2]