[ad_1]

Processing Content material

Municipals remained rangebound as U.S. Treasuries had been little modified and equities ended down.

The 2-year muni-UST ratio Wednesday was at 69%, the five-year at 66%, the 10-year at 67% and the 30-year at 88%, in response to Municipal Market Information’s 3 p.m. EDT learn. ICE Information Providers had the two-year at 70%, the five-year at 65%, the 10-year at 67% and the 30-year at 87% at a 4 p.m. learn.

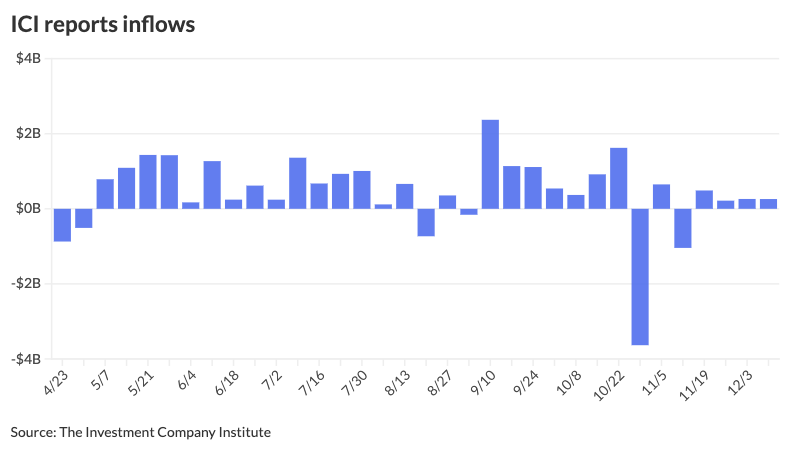

The Funding Firm Institute Wednesday reported inflows of $260 million for the week ending Dec. 10, following $262 million of inflows the earlier week.

Trade-traded funds noticed inflows of $1.119 billion after $392 million of inflows the week prior, per ICI knowledge.

Final week, the new-issue market was “fairly lively” as market members try to get issues carried out earlier than yearend, stated Jeff Timlin, a accomplice at Sage Advisory.

Provide moderated this week as issuance was at $6 billion.

“As soon as this week is finished, that is it for the yr. The next week is Christmas, after which after that, the brand new yr,” Timlin stated.

Throughout these two weeks, there will probably be nearly no exercise that will push the market someway, he stated.

Issuance for this yr will prime $560 billion, and

Capital wants stay sturdy, however for no less than the following three years, many fiscal obligations will doubtless shift to states, localities and nonprofits, she stated.

In the meantime, munis stay secure, in response to Timlin.

From a credit score standpoint, heading into 2026, a few of the lower-rated credit will probably be extra risky. And with these extra risky income streams, some changes to municipalities’ stability sheets and spending will probably be made, he stated.

Most municipalities, although, is not going to cope with the credit score points seen in some, like Chicago, he stated.

“We’re seeing some indicators of financial challenges. I do not assume anyone’s anticipating a recessionary atmosphere, however extra of a low-growth atmosphere,” Timlin stated.

“These municipalities are so used to each, going again 5 years, federal funds then adopted by vital progress of their income due to the sturdy economic system, that making a extra normalized income stream typically appears to be a problem,” he stated.

The secondary market is ok. There are common to barely beneath common bids wanteds, whereas the broker-dealer stock is someplace within the $15 billion vary, Timlin stated.

“That may be a regular sort of seasonal factor that occurs as a result of [fewer] members come to the market on the whole,” he stated.

Establishments will probably be lively till the final minute, whereas retail traders have already began to drag again, in response to Timlin.

“Individuals who you understand both purchase their very own bonds or purchase bonds by means of [financial advisors] or broker-dealers are in all probability extra centered on different issues proper now than reinvesting their munis,” he stated, noting it is not a seasonally excessive interval for reinvestment.

“No matter portfolio that they’ve constructed previous to Thanksgiving, they’re in all probability proud of till year-end,” Timlin stated.

Within the major market Wednesday, Jefferies priced for the New York Metropolis Transitional Finance Authority (Aa1/AAA/AAA/) $2 billion of future tax-secured subordinate refunding bonds. The primary tranche, $500 million of tax-exempt Fiscal 2026 Sequence C bonds, noticed 5s of 11/2027 at 2.58%, 5s of 2030 at 2.75%, 5s of 2035 at 3.12%, 5s of 2040 at 3.70%, 5s of 2045 at 4.30%, 5s of 2050 at 4.59% and 5.25s of 2055 at 4.64%, callable 5/1/2036.

The second tranche, $1.311 billion of tax-exempt Fiscal 2026 Sequence D-1 bonds, noticed 5s of 11/2027 at 2.58%, 5s of 2030 at 2.75%, 5s of 2035 at 3.12%, 5s of 2040 at 3.70% and 5s of 2041 at 3.84%, callable 5/1/2036.

The third tranche, $167.725 million of taxable Fiscal 2026 Sequence D-2 bonds, noticed all bonds value at par: 3.895s of 11/2026 and three.805s of 2027

The fourth tranche, $21.015 million of tax-exempt Fiscal 2026 Sequence E bonds, noticed 5s of 5/2026 at 2.58%, 5s of 2030 at 2.74%, 5s of 2035 at 3.07% and 5s of 2036 at 3.19%.

Piper Sandler priced for the Virgin Island Resort Improvement Financing Corp. $282.27 million of Frenchman’s Reef Resort Acquisition Challenge senior lien resort income bonds. The primary tranche, $272.27 million of Sequence 2025A-1 bonds, noticed 4.5s of two/2033 at 4.70%, 5s of 2038 at 5.25%, 5.75s of 2045 at 6.00% and 6s of 2055 at 6.25%, callable 2/1/2035.

The second tranche, $10 million of taxable Sequence 2025A-2 bonds, noticed 8.875s of two/2034 at 9.25%.

PNC Capital Markets priced for the Metropolitan Water District of Southern California (/AAA/AA+/) $184.225 million of particular variable charge water income refunding bonds, 2025 Sequence B, with 2.2s of seven/2047 priced at par.

AAA scales

MMD’s scale was little modified: 2.46% (-2) in 2026 and a pair of.41% (-2) in 2027. The five-year was 2.43% (unch), the 10-year was 2.76% (unch) and the 30-year was 4.24% (unch) at 3 p.m.

The ICE AAA yield curve was narrowly blended: 2.46% (unch) in 2026 and a pair of.43% (unch) in 2027. The five-year was at 2.40% (unch), the 10-year was at 2.77% (unch) and the 30-year was at 4.20% (+1) at 4 p.m.

The S&P International Market Intelligence municipal curve was unchanged: The one-year was at 2.47% (-1) in 2025 and a pair of.43% (unch) in 2026. The five-year was at 2.43% (unch), the 10-year was at 2.76% (unch) and the 30-year yield was at 4.22% (unch) at 3 p.m.

Bloomberg BVAL was minimize as much as a foundation level: 2.49% (unch) in 2025 and a pair of.44% (unch) in 2026. The five-year at 2.39% (+1), the 10-year at 2.73% (+1) and the 30-year at 4.14% (+1) at 4 p.m.

Treasuries had been little modified.

The 2-year UST was yielding 3.486% (flat), the three-year was at 3.529% (flat), the five-year at 3.696% (flat), the 10-year at 4.152% (+1), the 20-year at 4.783% (+1) and the 30-year at 4.828% (+1) close to the shut.

[ad_2]