[ad_1]

Munis noticed front-end weak spot and power out lengthy, as U.S. Treasury yields fell and equities ended down after two regional banks — Zions Bancorp and Western Alliance Bancorp — reported points with loans that concerned alleged fraud.

Earlier Thursday, the market was “chugging alongside, doing OK, simply form of nothing, in between slight power to modest upticks, however the narrative modified when that financial institution information got here out. The market actually ran fairly shortly,” mentioned Chris Brigati, managing director and CIO at SWBC.

Treasuries broke by means of 4% for the 10-year, which has been a “large assist space” for the market, he famous.

General, munis are persevering with what’s taking place with USTs and experiencing power within the charges market, Brigati mentioned.

The 2-year muni-UST ratio Thursday was at 69%, the five-year at 66%, the 10-year at 70% and the 30-year at 90%, in response to Municipal Market Information’s 3 p.m. EDT learn. ICE Information Companies had the two-year at 66%, the five-year at 64%, the 10-year at 69% and the 30-year at 89% at a 4 p.m. learn.

October is often a difficult month for the muni market, as issuance surges and reinvestment capital dips, mentioned PIMCO strategists.

“Over the subsequent couple of months, a mix of technical dynamics — reminiscent of refunding exercise, and calendar-driven provide — together with broader charge volatility, may produce a uneven market,” they mentioned.

Regardless of this being a near-term headwind, it could supply an “enticing entry level for opportunistic capital allocators as money yields are anticipated to ease progressively, and as issuance is prone to gradual meaningfully towards year-end and into 2026,” PIMCO strategists mentioned.

The tax-exempt universe stays “exceptionally enticing” on each an absolute and relative foundation, they mentioned.

Moreover, there’s worth on the long-end of the muni curve, mentioned Cooper Howard, a hard and fast earnings strategist at Charles Schwab.

Relative to USTs, longer-term munis — the place yields are prone to stay range-bound — are extra enticing than shorter-terms, he mentioned.

Valuations on the front-end of the curve are traditionally low, principally due to excessive demand from individually managed accounts, Howard mentioned.

Elsewhere, “credit score situations proceed to be broadly optimistic, revenues have proven resilience throughout issuers, and rainy-day funds sit close to 20-year highs, offering a significant fiscal cushion,” PIMCO strategists mentioned.

Furthermore, excessive absolute yields ought to assist anchor future returns, and any charge cuts by the Federal Reserve — which can possible shift retail traders to long-duration — may additional bolster demand for muni funds, they mentioned.

“The mixture of elevated beginning yields, important unfold versus taxable mounted earnings, and strong credit score situations units the asset class up for enticing forward-looking returns, each on an absolute foundation and relative to different mounted earnings investments, over the secular horizon,” PIMCO mentioned.

Presently, munis are seeing positive aspects month- and year-to-date of 0.80% and three.46%, respectively, and longer-duration munis outperformed shorter-term.

The optimistic returns come on the heels of the perfect month for the index in nearly two years, Howard mentioned.

Elevated issuance contributed to weak returns at first of the 12 months, he mentioned, noting that as issuance moderates over the subsequent few months, will probably be supportive of whole returns.

Nevertheless, issuance will stay elevated subsequent week, as there are already 5 billion-dollar-plus offers on the calendar: CPS Vitality with $1.8 billion of electrical and gasoline methods income refunding bonds, Texas with $1.771 billion of GO mobility fund and refunding bonds, the New Jersey Transportation Belief Fund with $1.5 billion of transportation program bonds, the New York Metropolis Transitional Authority with $1.5 billion of future tax secured bonds and the Kentucky State Property and Constructing Fee with $1.2 billion of income and income refunding bonds, in response to CreditSights.

Within the major market Thursday, BofA Securities preliminarily priced for CommonSpirit Well being (A3/A-/A-/) an upsized $2.7 billion of taxable company CUSIPs, Sequence 2025A. Pricing particulars have been unavailable as of three:30 p.m.

BofA Securities priced for Washington Well being Care Services Authority (A3/A-/A-/) on behalf of CommonSpirit Well being $518.76 million of income bonds, Sequence 2025A, with 5s of 9/2026 at 3.11%, 5s of 2030 at 3.03%, 5s of 2035 at 3.51%, 5s of 2040 at 4.02%, 5s of 2045 at 4.50%, 5.25s of 2050 at 4.71% and 5.5s of 2055 at 4.71%, callable 9/1/2035.

BofA Securities priced for the Colorado Well being Services Authority (A3/A-/A-/) on behalf of CommonSpirit Well being $455.33 million of income bonds, Sequence 2025A, with 5s of 9/2029 at 3.00% and 5s of 2035 at 3.47%, noncall.

Fund flows

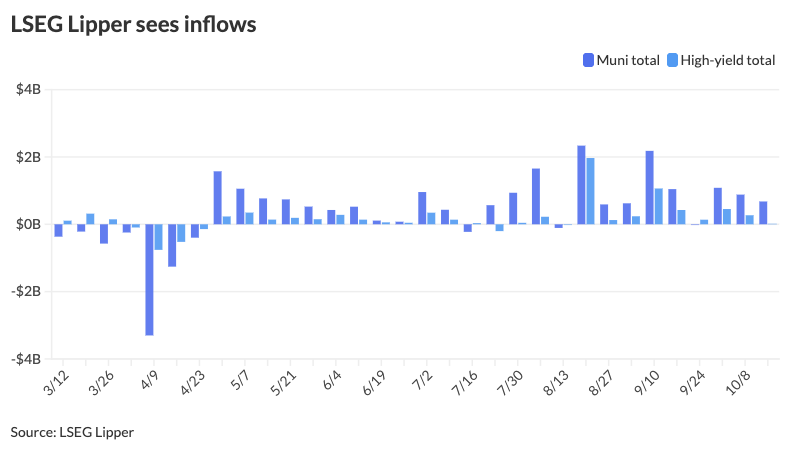

Buyers added $678.1 million to municipal bond mutual funds within the week ended Wednesday, following $882 million of inflows the prior week, in response to LSEG Lipper information.

Excessive-yield funds noticed inflows of $15.1 million in comparison with inflows of $268.5 million the earlier week.

Tax-exempt municipal cash market funds noticed inflows of $474 million for the week ending Oct. 14, bringing whole belongings to $140.591 billion, in response to the Cash Fund Report, a weekly publication of EPFR.

The typical seven-day easy yield for all tax-free and municipal money-market funds fell to 2.29%.

Taxable money-fund belongings noticed $20.799 billion pulled, bringing the entire to $7.182 trillion.

The typical seven-day easy yield was at 3.78%.

The SIFMA Swap Index was at 2.31% on Wednesday in comparison with the earlier week’s 2.70%.

AAA scales

MMD’s scale noticed cuts on the entrance finish and bumps outdoors of 5 years: 2.45% (+5) in 2026 and a couple of.35% (+2) in 2027. The five-year was 2.34% (unch), the 10-year was 2.78% (-4) and the 30-year was 4.13% (-3) at 3 p.m.

The ICE AAA yield curve was bumped as much as 5 foundation factors: 2.43% (unch) in 2026 and a couple of.33% (unch) in 2027. The five-year was at 2.34% (-1), the 10-year was at 2.78% (-3) and the 30-year was at 4.10% (-2) at 4 p.m.

The S&P International Market Intelligence municipal curve was bumped three foundation factors six years and out: The one-year was at 2.44% (+4) in 2025 and a couple of.36% (+4) in 2026. The five-year was at 2.33% (unch), the 10-year was at 2.79% (-3) and the 30-year yield was at 4.12% (-3) at 3 p.m.

Bloomberg BVAL noticed cuts on the entrance finish and bumped out lengthy: 2.39% (+5) in 2025 and a couple of.35% (+4) in 2026. The five-year at 2.25% (unch), the 10-year at 2.77% (-3) and the 30-year at 4.08% (-3) at 4 p.m.

Treasuries have been firmer.

The 2-year UST was yielding 3.423% (-8), the three-year was at 3.429% (-7), the five-year at 3.551% (-7), the 10-year at 3.975% (-5), the 20-year at 4.551% (-4) and the 30-year at 4.582% (-4) close to the shut.

[ad_2]