[ad_1]

November issuance surged as mega offers and better venture prices pushed provide this 12 months to a report excessive.

Issuance year-to-date is $535.15 billion, up 11.5% from $479.829 billion over the identical interval in 2024. This formally tops 2024’s report $507.585 billion quantity.

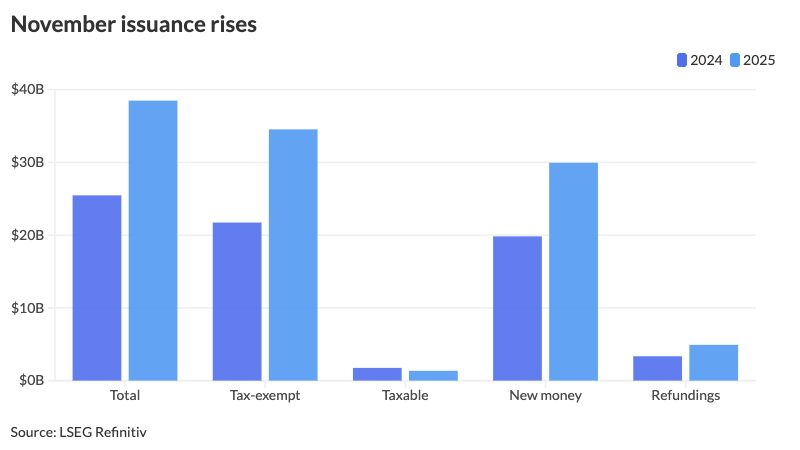

November quantity was $38.487 billion, up 51.1% from $25.47 billion in 2024, and above November’s 10-year common of $33.743 billion.

Whereas issuance rose in November 2025, the determine seems inflated as November 2024 — the one month final 12 months with issuance underneath $30 billion — noticed little issuance, stated Alice Cheng, director of municipal credit score and investor technique at Janney.

In October 2024, issuers tapped the municipal market en masse to get forward of potential election-related volatility, resulting in an acceleration of offers. This meant that within the following month, November 2024, provide was comparatively gentle, thereby skewing the p.c change year-over-year greater, she stated.

Regardless of this, provide has had “good momentum” this 12 months, and given October’s efficiency, “everyone, issuer and investor, each on the provision and demand aspect, [are] attempting to seize the worth. So there’s a variety of curiosity. There’s some huge cash that must be invested and to play,” Cheng stated.

Moreover, November nonetheless boasted sizable offers, together with an estimated $3.48 billion from Ascension, a Catholic nonprofit well being system, throughout 4 offers.

This was one of many greatest offers of the month, contributing to the rise in healthcare and basic objective issuance, which have been up 39.6% and 119.4% respectively.

The previous was additionally impacted by the acceleration of healthcare issuance, as vital cuts to Medicaid, which might influence hospital profitability, have led to frontloading of issuance to get forward of the matter, a theme that has been ongoing this 12 months, stated Invoice Delahunty, a portfolio supervisor at Morgan Stanley Funding Administration.

Moreover, rising inflation performed a task within the surge of provide, each in November and for the 12 months general. The buyer value index is up 23%, whereas the nationwide freeway development value index is up over 60%, Delahunty stated.

“There may be a variety of deferred infrastructure on this nation and if you do go to subject debt to fund a few of that tasks simply value much more and that is what’s driving issuance up as effectively,” he stated.

Provide this month has been effectively absorbed, particularly on the retail aspect, stated Invoice Walsh, president of Hennion & Walsh.

November is generally a “bizarre” month for consumers and the road can decelerate slightly, however there was demand from retail consumers in November, he stated.

For the previous 10 to fifteen years, there was retail demand even when there should not be, as exercise slows down across the holidays, Walsh stated.

For the rest of the 12 months, issuance will principally be “rolled” into the primary two weeks of the month, Delahunty stated.

Afterward, issuance will gradual. “This can be a time the place all of the motion ought to be taking place, after which as we enter into the vacation season it is simply going to drop off,” Cheng stated.

For 2026, issuance predictions vary from Barclays’ forecast of $520 billion to $530 billion to investor and strategist James Pruskowski’s estimate of over $750 billion. Cheng, for her half, sees issuance between $605 billion and $650 billion.

New-money issuance will tick up subsequent 12 months by $20 billion to $30 billion, partially as a result of estimated lack of federal grants to states and native governments, together with greater development prices, she stated.

Refundings can even be up subsequent 12 months, as decrease and extra favorable rates of interest are creating extra refunding alternatives, she stated.

November particulars

Tax-exempt issuance surged 58.9% to $34.537 billion in 726 points from $21.731 billion in 623 points a 12 months in the past. Taxable issuance dropped 23% to $1.346 billion in 52 points from $1.747 billion in 68 points in 2024. AMT issuance was $2.605 billion, up 30.7% from $1.992 billion in 2024.

New-money issuance rose 51.1% to $29.949 billion from $19.827 billion, whereas refundings have been up 46.9% to $4.92 billion from $3.349 billion.

Income bond issuance elevated 59.4% to $29.322 billion from $18.397 billion in November 2024, and basic obligation bond gross sales rose 29.6% to $9.165 billion from $7.073 billion in 2024.

Negotiated deal quantity jumped 62% to $32.474 billion from $20.045 billion a 12 months prior. Aggressive gross sales rose 28.2% to $5.834 billion from $4.55 billion in 2024.

Bond insurance coverage elevated 38.8% to $3.854 billion from $2.776 billion.

Financial institution-qualified issuance was up 15.8% to $1.041 billion in 241 offers from $898.8 million in 198 offers a 12 months prior.

Texas claimed the highest spot year-to-date amongst states.

Issuers within the Lone Star State accounted for $77.91 billion, up 17% year-over-year. California was second with $76.171 billion, up 9.9%. New York was third with $57.537 billion, up 7%, adopted by Florida in fourth with $22.732 billion, down 11%, and Illinois in fifth with $17.741 billion, a 23% enhance from the identical interval in 2024.

Rounding out the highest 10: Alabama with $16.829 billion, up 33.1%; Massachusetts with $16.153 billion, up 20.3%; Wisconsin with $16.076 billion, up 50.1%; Pennsylvania with $15.69 billion, down 3.6%; and Colorado with $12.993 billion, up 28.4%.

[ad_2]