[ad_1]

Municipal bond issuance declined year-over-year for the third consecutive month, as provide moderated in comparison with the surge in issuance in October 2024, when market members issued bonds with a purpose to keep away from potential election-related volatility.

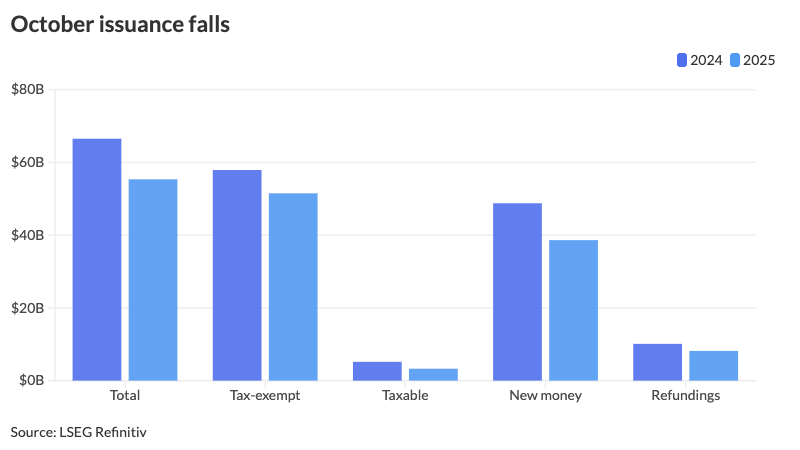

October quantity was $55.348 billion, down 16.8% from $66.513 billion in 2024. Nevertheless, that is nonetheless above October’s 10-year common of $49.033 billion.

Issuance year-to-date is $493.063 billion, up 9.3% from $451.079 billion over the identical interval. With subsequent week’s issuance estimated at $13.118 billion, quantity is more likely to surpass 2024’s $513.652 billion report by the center of November.

“Regardless of a softer October, provide has been sprinting forward of report ranges all yr. And by any measure, $55 billion is substantial, particularly contemplating final October was huge,” stated James Pruskowski, an investor and market strategist.

Issuance was sturdy in October 2024, the heaviest month of that yr, as issuers flocked to market forward of potential election-related volatility and to keep away from doable issues tapping the capital markets by way of yearend, stated Jamie Iselin, head of the municipal mounted earnings staff and a senior portfolio supervisor at Neuberger Berman.

Due to this fact, it is unsurprising that issuance fell in October 2025 — which was nonetheless a good month for provide — from the mass inflow of provide final yr, he stated.

October noticed uneven issuance. Some weeks noticed elevated quantity, together with the second-to-last week of the month, which recorded $16 billion in tax-exempt issuance — the fifth-largest on report, in line with J.P. Morgan strategists.

Nevertheless, others, like the ultimate week of the month, noticed decrease issuance because of the Federal Open Market Committee assembly. Iselin was shocked that a number of the larger offers from the primary week of November, together with the most important pay as you go fuel deal ever, with $2.7 billion in power provide income bonds from the Southeast Vitality Authority, didn’t attempt to “pull” themselves up every week to reap the benefits of the smaller calendar.

The dip in issuance in October was not “about fading demand; it was about issuers selecting to not worth into chaos,” Pruskowski stated.

“Washington’s shutdown, geopolitical shockwaves, and a Treasury market that whipsawed on each headline turned October right into a no-fly zone for public finance officers,” he stated. “Volatility is the enemy of execution, and in October it was operating the present.”

Then there may be additionally the off-year election cycle, the place market members are not looking for a “billion-dollar bond deal competing with marketing campaign flyers,” so a “tactical pause, not a structural shift,” ensues, Pruskowski stated.

“The basics have not modified. Issuers are watching ageing infrastructure, waning federal incentives, and a good financing window. The pipeline is lengthy, the demand base is deep, and the run into yearend is poised to warmth again up shortly,” Pruskowski stated.

October particulars

Tax-exempt issuance fell 11.1% to $51.497 billion in 786 points from $57.905 billion in 1,059 points a yr in the past. Taxable issuance dropped 36.5% to $3.284 billion in 57 points from $5.171 billion in 97 points in 2024. AMT issuance was $566.5 million, down 83.5% from $3.437 billion in 2024.

New-money issuance fell 20.8% to $38.63 billion from $48.765 billion, whereas refundings had been down 19.2% to $8.172 billion from $10.114 billion.

Income bond issuance dropped 13.7% to $37.508 billion from $43.476 billion in October 2024, and normal obligation bond gross sales decreased 22.6% to $17.84 billion from $23.037 billion in 2024.

Negotiated deal quantity was down 10.6% to $46.561 billion from $52.094 billion a yr prior. Aggressive gross sales fell 31.7% to $8.745 billion from $12.813 billion in 2024.

Bond insurance coverage decreased 56.3% to $3.326 billion from $7.606 billion.

Financial institution-qualified issuance fell 32.7% to $686.2 million in 162 offers from $1.019 billion in 263 offers a yr prior.

Texas claimed the highest spot year-to-date amongst states.

Issuers within the Lone Star State accounted for $73.153 billion, up 21.3% year-over-year. California was second with $71.578 billion, up 10.5%. New York was third with $55.953 billion, up 4.6%, adopted by Florida in fourth with $20.029 billion, down 19.1%, and Wisconsin in fifth with $15.676 billion, a 56.6% enhance from 2024.

Rounding out the highest 10: Massachusetts with $15.322 billion, up 17.5%; Pennsylvania with $14.657 billion, down 3.5%; Illinois with $13.038 billion, down 7.2% Alabama with $12.7 billion, up 11.7%; and Washington with $12.092 billion, down 5.2%.

[ad_2]