[ad_1]

In case you’re self-employed, you probably put on a number of ill-fitting hats: accountant, admin, HR rep. And that final one is low-key necessary, as a result of it means nobody is organising a retirement plan for you.

So what’s a gig employee, small enterprise proprietor, or solo practitioner to do?

There’s the trusty IRA, after all. However its tax advantages part out at sure earnings ranges, and its $7,000 annual contribution restrict fills up quick. You might have considered trying—or want—to save lots of extra to appreciate your retirement objective.

Fortunately, two lesser-known retirement accounts provide self-employed staff 10x extra capability for tax-advantaged investing: the solo 401(ok) and the SEP IRA.

They’re related in that sense (excessive contribution limits), however additionally they differ in some necessary methods. We’ve discovered that for a lot of self-employed staff, selecting between the 2 usually hinges on their hiring or lack thereof:

👉 No workers past a partner, and no plans to rent?

- Think about a solo for those who prioritize Roth entry and a slight edge in contribution limits.

- Think about a SEP for those who prioritize much less administrative work.

👉 See your self hiring a couple of workers within the not-so-distant future?

- Think about beginning with a solo 401(ok), then transitioning to a bunch 401(ok) plan for those who prioritize Roth entry and extra flexibility in the way you construction worker contributions.

- Think about a SEP for barely simpler admin, and the flexibility to pause contributions to your workers’ SEPs throughout down years.

👉 Planning to develop past 5-10 workers in some unspecified time in the future?

- Think about the solo-to-group 401(ok) transfer for extra flexibility in the way you construction worker contributions. You may max out your personal retirement financial savings, for instance, whereas letting workers resolve their very own contribution charges.

That’s the TL;DR model. For a deeper dive, let’s examine the 2 accounts throughout a couple of classes:

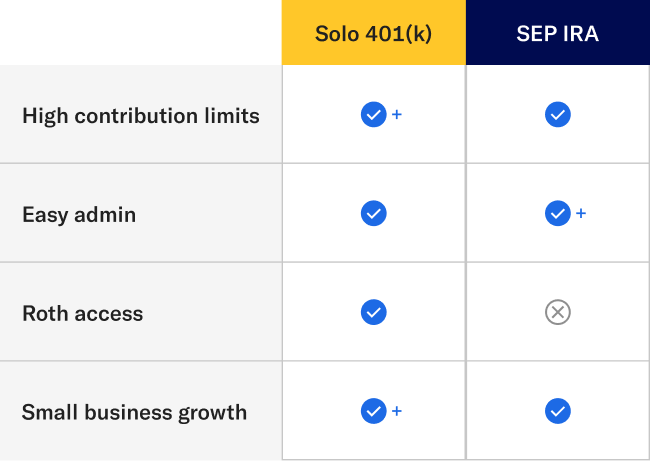

Excessive contribution limits

Each accounts allow you to save a lot for retirement—upwards of $70,000 a yr—however solos provide you with a few methods to stretch that even additional:

Case #1: You’re enjoying catch-up

In case you’re age 50 or older and catching up in your retirement financial savings, a solo 401(ok) affords further “catch-up” contributions of $7,500 annually, or $11,250 for these 60-63.

Notice that beginning in 2026, any catch-up contributions should go right into a Roth solo particularly (extra on these beneath) for those who obtained greater than $145,000 in FICA wages (salaries, commissions, and so on.) the prior yr out of your solo’s sponsoring firm.

Case #2: You’re a center class tremendous saver

Say you earn lower than $280,000, however you save effectively above the usual recommendation of 10-15% for retirement. On this situation, it’s possible you’ll run up towards the SEP’s 25% compensation cap earlier than you attain its total $70,000 restrict. However with solos, you’ll be able to contribute as each an employer (as much as 25% of compensation) and an worker (as much as $23,500) till you hit the general restrict.

⚖️ Benefit: solo 401(ok)

Straightforward admin

Each a solo 401(ok) and SEP IRA, assuming they’re streamlined digital choices reminiscent of ours, are easy to arrange. You may open a Betterment SEP totally on-line, whereas a Betterment solo requires a fast name with our Licensed Concierge group to get the ball rolling.

Every account kind is comparatively low upkeep as effectively. Neither a SEP nor a solo require annual paperwork, with the one exception being for solo 401(ok) balances that exceed $250,000. In that case, the IRS requires solo homeowners (aka “sponsors”) to file Kind 5500-EZ. Whereas we’re not a tax advisor, and at all times advocate working with one, the shape is comparatively simple to fill out.

⚖️ Benefit: SEP IRA

Suss out a solo vs. SEP with the assistance of an advisor.

Roth entry

Solos and SEPs are designed for retirement, so the IRS offers particular tax therapy to each account sorts. However in apply, solos provide you with not one however two totally different flavors of tax therapy to select from:

- You may contribute with pre-tax {dollars} through a standard solo 401(ok), reducing your taxes now and releasing up more cash to speculate.

- You even have the flexibility to contribute with after-tax {dollars} through a Roth solo 401(ok), having fun with tax-free withdrawals in retirement. And Roth solo 401(ok)s include two added bonuses:

- Not like conventional retirement accounts, they’re not topic to Required Minimal Distributions (RMDs) in retirement.

- Not like Roth IRAs, they arrive with no earnings limits of any type.

Roth SEP IRAs, in the meantime, have technically been allowed by the IRS since 2023, however few suppliers have rolled them out but.

⚖️ Benefit: Solo 401(ok)

Small enterprise progress

In some unspecified time in the future in your self-employed journey, it’s possible you’ll deliver on employed assist. On this case, it’s potential to transition each account sorts to accommodate workers. Some SEP suppliers allow you to shift from a solo practitioner to an employer who contributes to workers’ SEP IRAs on their behalf. However there’s a catch: you need to contribute the identical quantity to their SEPs as you do your personal, which can show difficult relying on your small business.

With solo 401(ok)s, then again, you’ll be able to embody a partner from the get-go, offered they’re an worker or co-owner of the enterprise. And for those who see the potential for increasing past a handful of workers down the street, it could make sense to merely transition your solo 401(ok) to a bunch 401(ok) plan and revel in extra flexibility in the way you construction contributions to your group. Our assist group handles strikes like this usually and may also help you when the time comes.

⚖️ Benefit: Solo 401(ok)

So which account is best for you?

The excellent news is each SEP IRAs and solo 401(ok)s provide wonderful tax benefits that may enable you attain retirement faster. We provide each at Betterment, and make it straightforward to open both one. As a result of if you’re self-employed, you’re busy operating your small business. Optimizing your retirement financial savings? Go away that to us for one much less hat in your wardrobe.

[ad_2]