(the place I *don’t* equate 2 consecutive quarters to a recession, as that’s what rookies do…):

Determine 1: Annualized GDP progress in 2025H1, calculated as log variations. Supply: BEA and creator’s calculations.

The states with adverse progress are Arizona, Arkansas, Idaho, Maine, Maryland, Mississippi, Montana, Oregon, Vermont, West Virginia, and Wyoming, with Oregon hardest hit (-1.4% annualized). The US progress price over this similar interval was 1.6%. These negative-growth price states account for about 8% of complete US GDP.

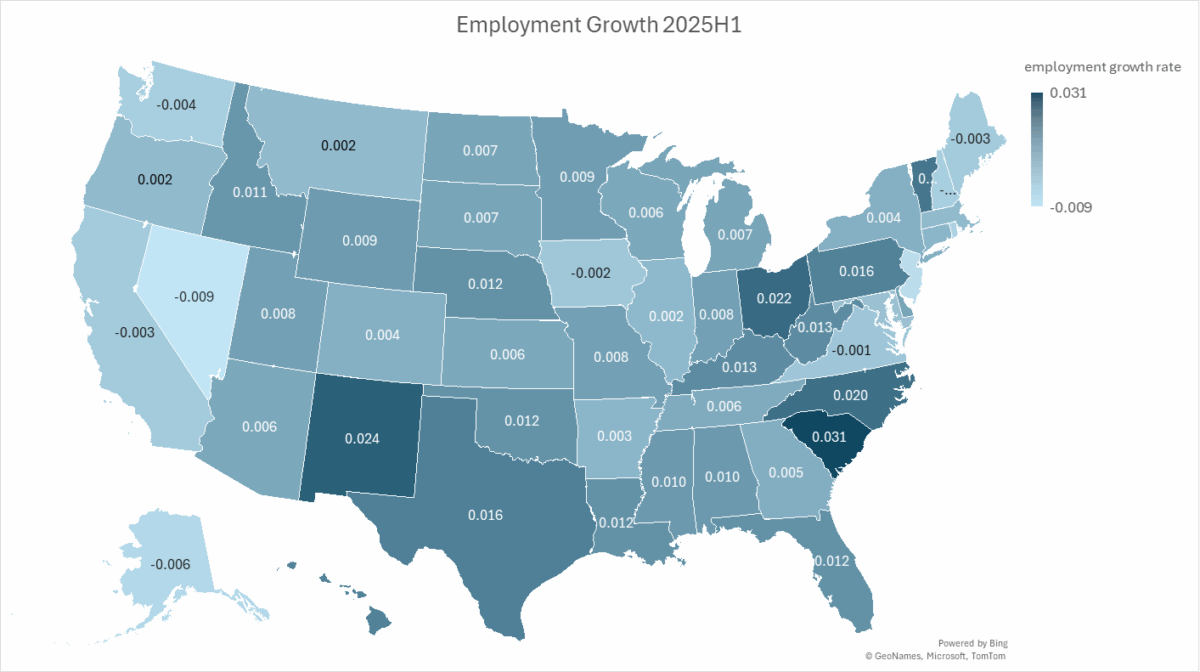

A fairly completely different image is proven utilizing employment progress by state over the 6 month interval as much as June 2025, corresponding roughly to the interval proven in Determine 1.

Determine 2: Nonfarm payroll employment progress in 2025H1, calculated as log variations. Supply: BEA and creator’s calculations.

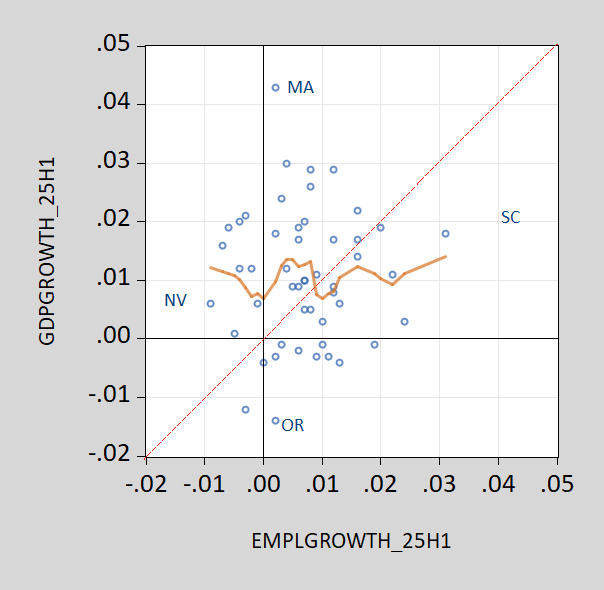

Ten states have adverse progress charges, however not the identical. In 2025H1, the correlation between the 6 month change in employment and the quarter change in GDP is just 0.03.

Determine 3: 2025H1 GDP progress annualized vs. 2025H1 employment progress annualized. Nearest neighbor match is tan line. Supply: BEA, BLS and creator’s calculations.

This poor mapping from employment to GDP progress on the cross part is according to the divergence in progress charges of GDP and employment within the combination.

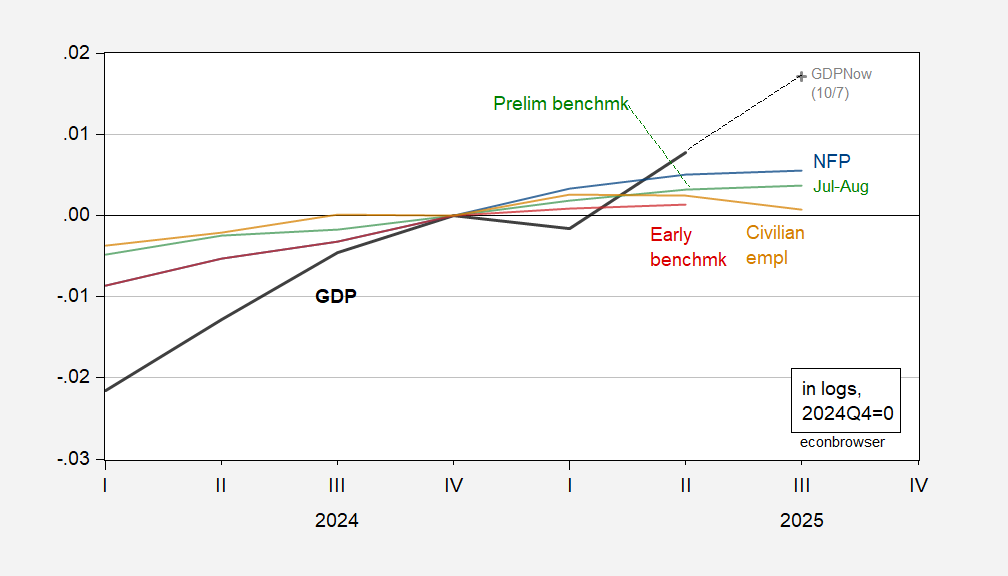

Determine 4: GDP (black), GDPNow (grey +), NFP (blue), implied preliminary benchmark (inexperienced), early benchmark (purple), civiian employment – analysis sequence (tan), all in logs 2024Q4=0. Q3 is July and August. Supply: BEA, BLS, Atlanta Fed, Philadelphia Fed, and creator’s calculations.

Observe that each maps differ from Zandi’s recession map, proven right here.