[ad_1]

Coverage Heart for the New South

The worldwide financial setting has modified because the U.S.—and to a much less confrontational diploma, the European Union—have clearly established a context of technological rivalry with China. Hindering China’s progress within the sophistication of semiconductor manufacturing has change into a centerpiece of present U.S. international coverage. Whereas the U.S. is clearly successful the semiconductor battle, the image is completely different in terms of clean-energy expertise.

Each expertise wars overlap with entry to and refinement of vital uncooked supplies (CRM), that are key upstream elements of the corresponding worth chains, encompassing mineral-rich rising markets and growing economies. The way in which by which the U.S. and the European Union method the aim of self-sufficiency, in addition to entry to and refinement of CRMs, will make an enormous distinction to their stakes within the expertise wars.

Introduction

Technological progress within the Chinese language economic system in latest many years has mainly concerned a technique of utilizing information and applied sciences made obtainable by globalization. Along side native funding in capability constructing, along with pressured switch in some segments, Chinese language companies have acquired the aptitude to supply and adapt applied sciences, and, in some instances, even to make primary improvements (Canuto, 2021).

The setting has modified because the U.S., and to a much less confrontational diploma the European Union, have clearly put in place a technological rivalry with China. In a September 2022 speech, U.S. White Home nationwide safety adviser Jake Sullivan (2022) talked about superior semiconductor and computing applied sciences, biotechnology, and clean-energy expertise as areas by which the U.S. ought to preserve international management, as “a nationwide safety crucial”.

Hindering China’s progress in rising the sophistication of semiconductor manufacturing has change into a centerpiece of the present U.S. international coverage. Following the success of Chinese language manufacturing and exports within the much less technologically superior segments of the trade, the U.S. has raised limitations in opposition to Chinese language entry to North American tools and applied sciences, stopping China from climbing the technological ladder, and even demanding that customers in different nations don’t facilitate circumvention of the restriction. Regardless of the fragmentation of the provision chain for the highest-end chips, all the essential elements are within the arms of both the U.S. or its allies. The concrete consequence within the case of superior semiconductors is that China should construct the higher rungs of the technological ladder itself.

Whereas the U.S. is clearly successful the semiconductor battle, the image is completely different in terms of clean-energy expertise. Not like for semiconductors, the place the U.S. and allies have the management and present management of bottlenecks in manufacturing chains, China has constructed a really robust place in clean-energy applied sciences. To catch up, the U.S. is relying on the Inflation Discount Act (IRA), accepted by Congress in 2022, and different payments. The European Union, in flip, is launching an investigation into Chinese language state help for makers of electrical autos, as hovering imports of their vehicles stoke fears about the way forward for European auto producers.

Each expertise wars embrace the problem of entry to and refinement of vital uncooked supplies (CRM), that are key upstream elements of the corresponding worth chains, encompassing mineral-rich rising markets and growing economies. Whereas China already has a agency footprint in CRMs domestically and overseas, the U.S. and Europe might want to take steps to safeguard their very own wants. As a report authored by Garcia-Herrero et al (2023) factors out, this may be finest completed via “inexperienced tech partnerships”.

Twin-use Items, Semiconductors and Deglobalization

In 2017, after I was one of many govt administrators of the World Financial institution, I visited the Gaza Strip, in Palestine, on a piece mission. A sanitation undertaking financed by the Financial institution in a residential space topic to flooding with sewage when it rained closely had been halted due to a ban on the entry into Gaza of hydraulic pipes. After we spoke to the Israeli navy authority liable for blocking the tubes, he instructed us that the issue lay of their doable twin use, civil or navy.

I bear in mind this after I see references to nationwide safety in arguments in opposition to free commerce in dual-use items. Of all doable justifications for globalization-reversing nationwide insurance policies, nationwide safety is essentially the most highly effective argument in opposition to unfettered, market-driven globalization (Canuto et al, 2023). It’s also essentially the most troublesome to judge, because it can’t be analyzed straight by researchers, market analysts, or journalists; it’s essential to take what authorities intelligence sources say.

The argument has discovered bipartisan help in the US concerning China. A significant issue can all the time come up if a broad interpretation of ‘twin use’ ends in the restriction of many items and providers—even clothes or medicines utilized by the navy. Because the idea has the potential to result in broad and sweeping restrictions throughout a number of sectors, there’s a threat that it might spur financial wars within the type of retaliation.

The principle class focused thus far is the semiconductor sector. Semiconductors are an integral part of many shopper merchandise, together with vehicles and smartphones, however they will also be utilized in dual-use items resembling civil and navy plane. Moreover, they’re utilized in supercomputing and synthetic intelligence, areas with potential implications by way of nationwide safety.

The dispute considerations essentially the most superior segments within the semiconductor trade. Yoon (2022) distinguished between extra superior semiconductors which are 3-14 nanometers in dimension, and the cheaper and less complicated chips above 14 nanometers.

The economic system is more and more hanging on nanometers, or billionths of a meter. The width between particular person transistors on a chip is measured in nanometers. The smaller the hole, the extra transistors will be included in a single silicon chip, making the chip extra highly effective.

And all the pieces relies upon an increasing number of on such chips: smaller and quicker semiconductors are wanted for tools together with computer systems, smartphones, dwelling home equipment, digital video games, medical tools, and telecommunications.

The primary era of electronics within the Seventies had one chip per gadget. Now, an electrical automotive wants greater than 2,000 semiconductors, greater than twice the common variety of chips in at the moment’s fossil fuel-powered vehicles (Yoon, 2022). Chips additionally play a key position in next- era expertise, from 5G web to cloud providers and synthetic intelligence.

Such tiny semiconductors are on the coronary heart of the present rivalry between the US and China. On the finish of 2019, we noticed how the technological chapter of the U.S.-China confrontation, initiated by President Trump, would proceed below President Biden (Canuto, 2019). Certainly, along with President Biden not reversing his predecessor’s commerce measures, new Washington guidelines block China’s entry to chips and prohibit the sale of kit wanted to supply them, along with guaranteeing important applied sciences to supply superior chips unavailable. The principles in drive on this regard are essentially the most restrictive up to now.

Given the vital character of semiconductors in a lot of what’s completed at the moment, their superior variations and their manufactures have change into a type of substitute for the weapons and armies utilized in ‘proxy wars’ through the Chilly Struggle between the U.S. and the Soviet Union. Hindering China’s progress by way of the sophistication of semiconductor manufacturing has change into a centerpiece of U.S. coverage towards the nation.

It was additionally notable how simply Biden’s fiscal bundle devoted to semiconductors obtained bipartisan help within the U.S.

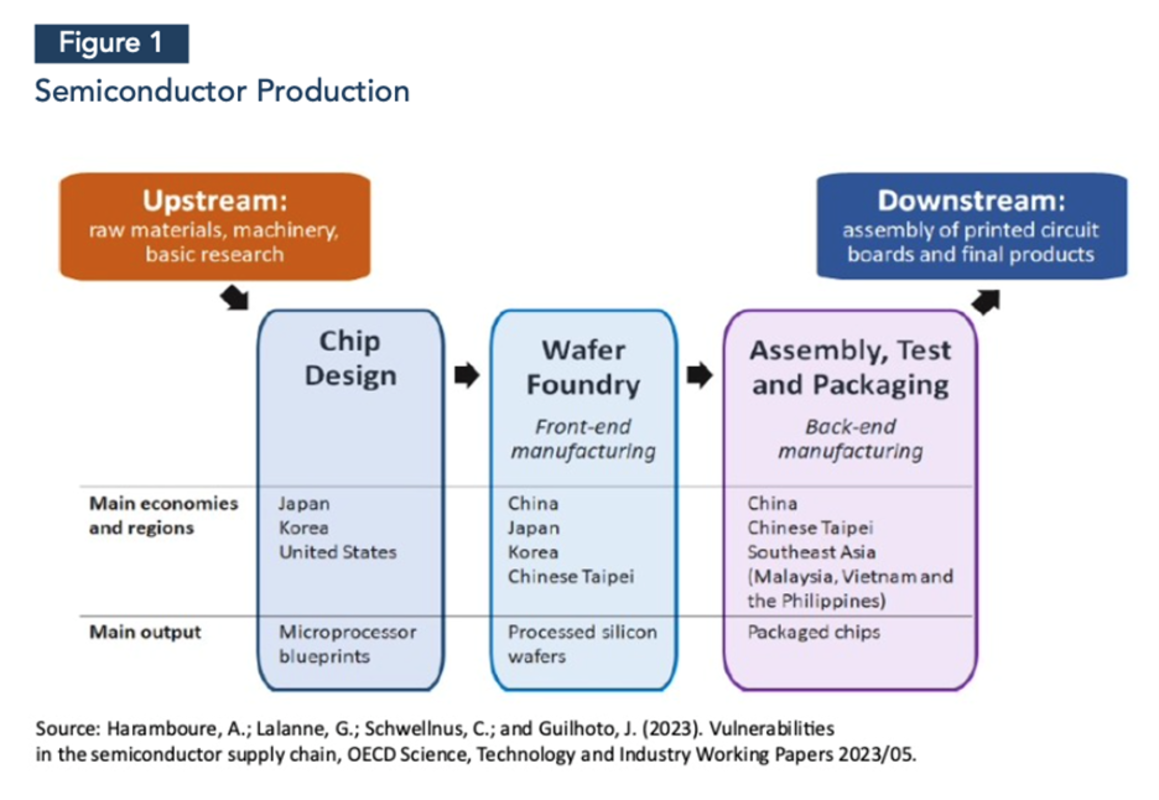

Taiwan and South Korea have mastered cutting-edge chip manufacturing expertise and account for near 50% of the world semiconductor market. The U.S. accounts for 12% of the worldwide market, however its native corporations don’t produce superior chips on a big scale. Then again, many phases of the semiconductor manufacturing course of depend on U.S.-originated applied sciences, together with the tools wanted to supply essentially the most superior chips. Determine 1 shows the worth chain of semiconductor manufacturing.

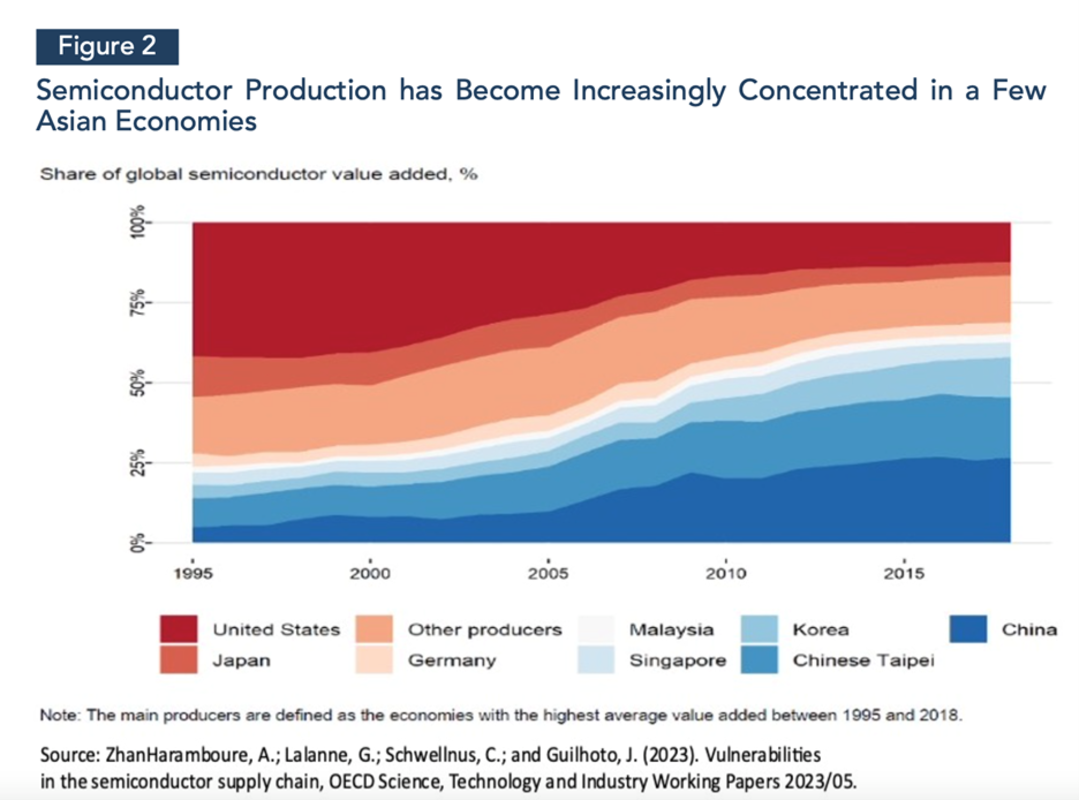

Determine 2 depicts the evolution of world market shares, with none breakdown of figures by ranges of sophistication and technological necessities. Within the latest previous, China has occupied a big share of the markets for affordable semiconductors with greater nanometers. One can see on this case an try to repeat the trajectory by which the nation made good use of globalization to extend added worth, and consequently to climb the ladder of per-capita revenue.

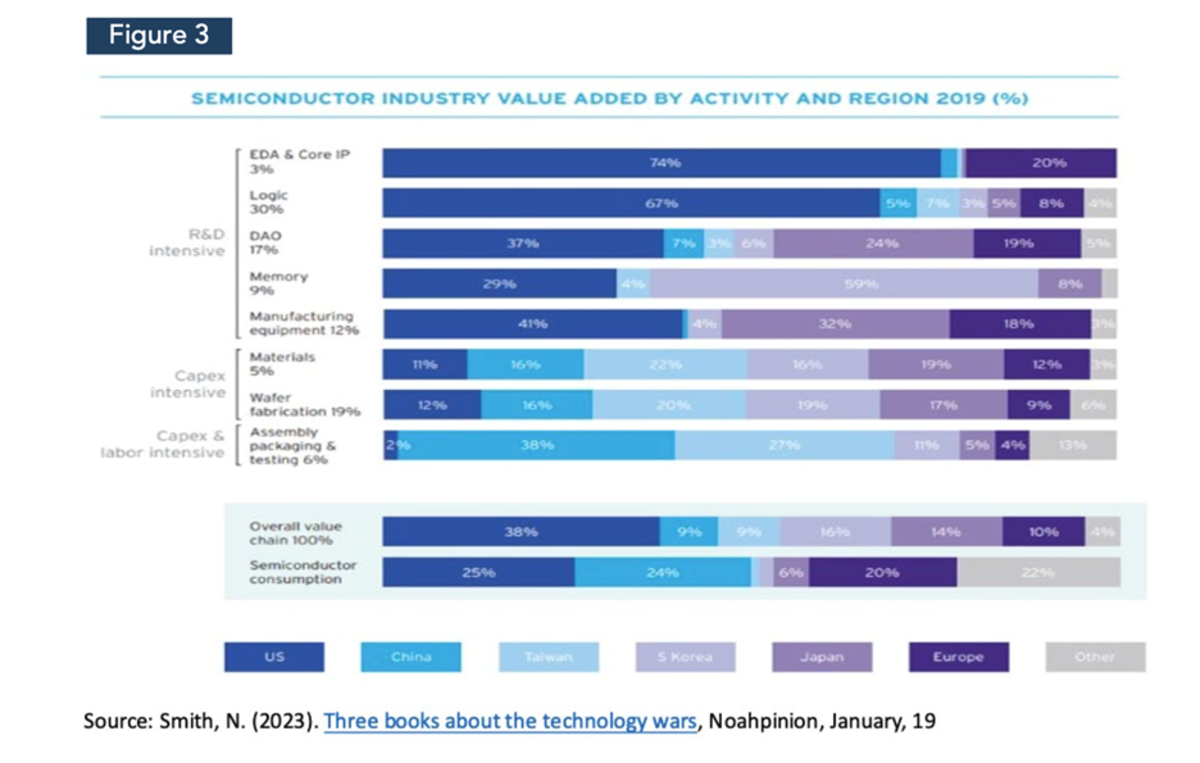

The U.S. semiconductor ‘proxy battle’ consists exactly of reducing off entry to the upper rungs of the ladder for some economies. China should construct them itself. Determine 3 reveals at which phases of semiconductor manufacturing completely different nations predominate.

In October 2022, the US introduced broad export controls on the semiconductor trade, focusing on China. Below the restrictions, any semiconductor made with American expertise to be used in supercomputing or synthetic intelligence can solely be bought to China with an export license issued by the US, a license that’s troublesome to acquire. Given that just about all semiconductors are produced utilizing U.S. expertise, this rule successfully covers the complete international trade.

The USA doesn’t export many semiconductors on to China. Nevertheless, the export controls focused chip-making nations that use U.S. software program and/or machines of their manufacturing amenities. Customers/companions exterior the U.S. have been pressured to abide by these restrictions.

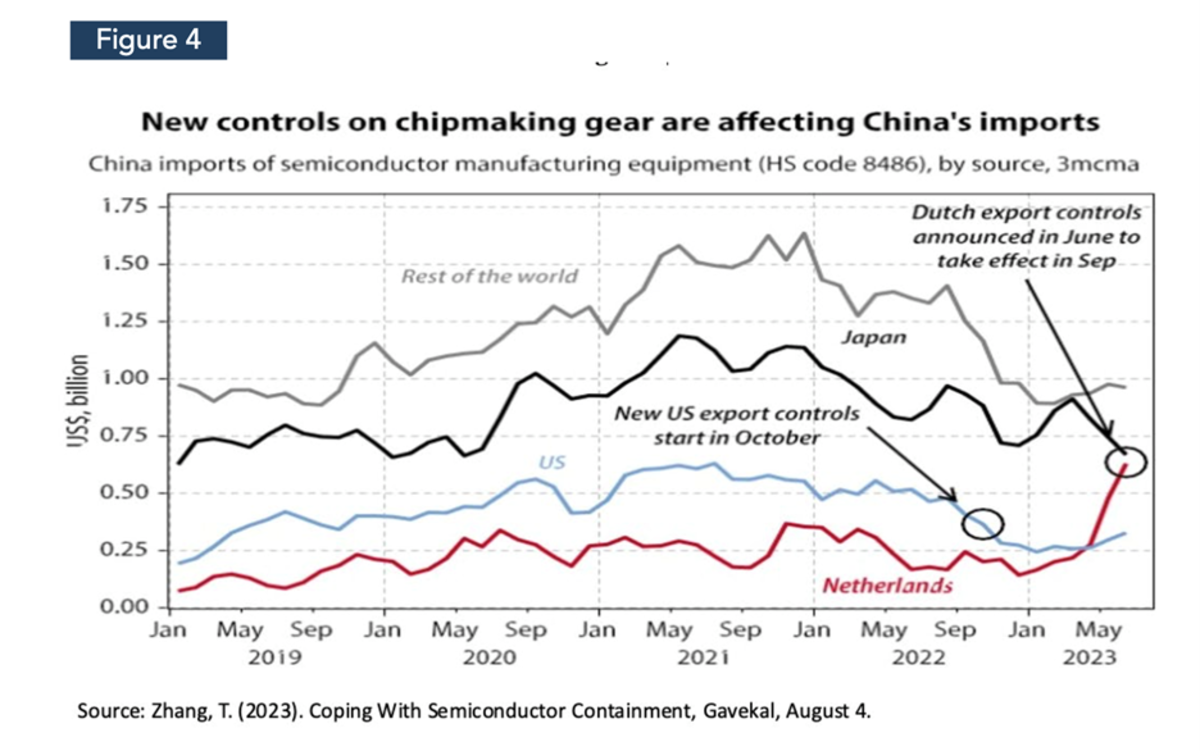

Third nations face the next selection: search the export licenses required by the US or cease utilizing their expertise and tools. Therefore there may be rising use of the phrase ‘armed interdependence’ to characterize how the US has used the interdependence inherent in international commerce and provide chains to drive its buying and selling companions to align with its expertise battle in opposition to China. Moreover, its residents are prohibited from working with Chinese language chip producers except they’ve particular approval. With these measures, the U.S. seeks to forestall China from advancing technologically utilizing what already exists on the frontier on the American facet in sectors essential to nationwide safety. Determine 4 means that the impact of such restrictions has been vital.

Another interpretation of latest semiconductor export restrictions is that they’ve little to do with nationwide safety however are geared toward curbing China’s path of financial growth via the inventive absorption of expertise obtainable overseas. If that’s the case, the brand new restrictions mark the top of an period of globalism and financial cooperation, and the start of one other chilly battle.

The case of semiconductors suits effectively with what we observe to be a partial reversal of globalization in high-technology segments that thought-about delicate from the viewpoint of nationwide safety, with prices nonetheless thought-about justifiable by authorities authorities (Canuto, 2022). As within the case of the hydraulic pipes within the sanitation undertaking within the Gaza Strip, all the pieces will rely upon which of the twin makes use of is taken into account a precedence.

The outcomes of U.S. authorities activism on home manufacturing are nonetheless to be seen. In the meantime, semiconductor producers in Taiwan and South Korea are grateful as a result of the U.S. has made it more durable for mainland Chinese language producers to enter the segments they dominate.

The U.S. is successful the semiconductor battle. Regardless of the fragmentation of the provision chain for the highest-end chips, all the essential elements are within the arms of both the U.S. or its allies. The concrete consequence within the case of superior semiconductors is that China should construct the higher rungs of the technological ladder itself.

Proxy Struggle on Clear-energy Applied sciences

The scenario with clean-energy applied sciences seems opposite to that with semiconductors. In clean-energy applied sciences, China has constructed a really robust place.

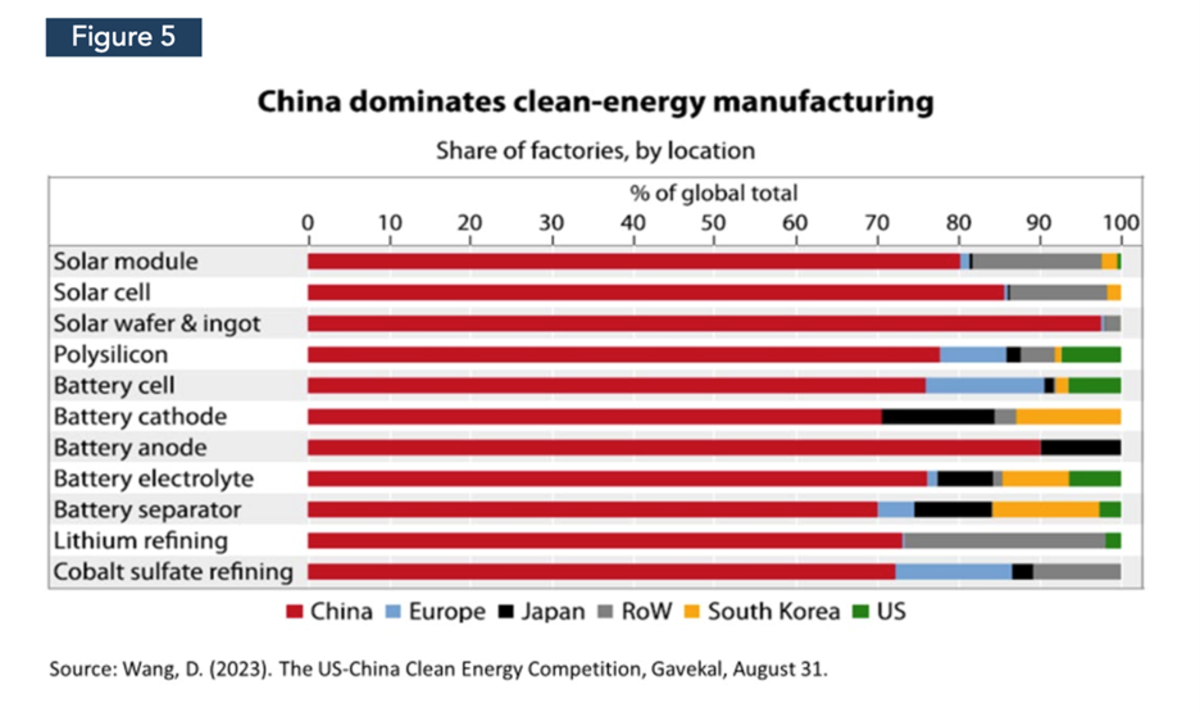

The transition to wash power is requiring each scientific innovation and large-scale growth of established applied sciences. The U.S. stays glorious on the former, together with scientific work on carbon seize, storage, and removing. The U.S. can also be exploring frontiers in geothermal power, benefiting from hydraulic fracturing experience within the shale oil and fuel trade (Wang, 2023). Then again, in business industries which are within the growth part, the U.S. lags China in essentially the most vital decarbonization applied sciences: photo voltaic, wind, batteries, and hydrogen (Determine 5). The upper tempo of funding in clear power by China within the final decade has given it a bonus in studying and expertise domains.

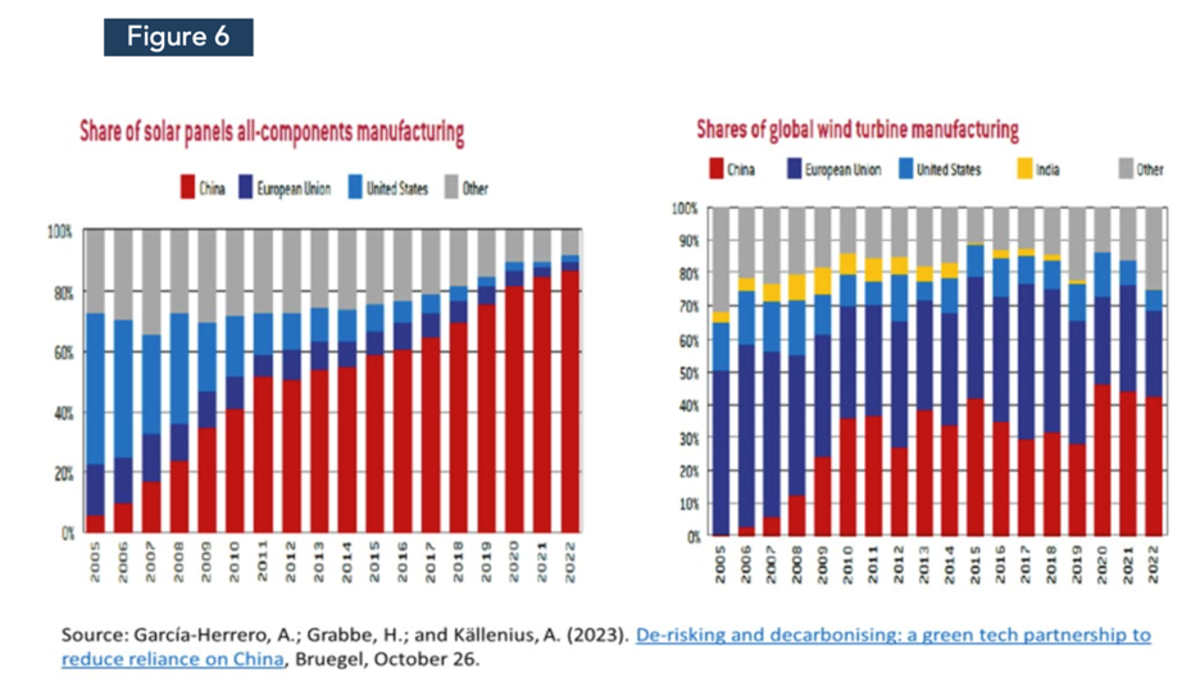

Chinese language dominance is obvious in photo voltaic power (Determine 6). The 90% decline in the price of photo voltaic power era during the last decade got here primarily from there, with Chinese language corporations being liable for 75% to 95% of every part of the worth chain. Tariffs and import bans haven’t prevented the scenario that, at the moment, U.S. imports of photovoltaic cells come largely from Chinese language producers situated in Southeast Asia.

The Chinese language are additionally on the forefront in terms of electrical automobile batteries, gaining floor even from rival companies in Japan and South Korea that have been on the technological forefront. On this case, bodily proximity to automotive producers issues. Chinese language producers benefited from the explosion within the manufacturing of electrical vehicles in China, whose native consumption was sponsored by the federal government. The outcomes by way of productiveness and competitiveness meant that China surpassed Germany in automotive exports in 2022.

The problem is extra advanced within the case of wind power. China at the moment has the vast majority of the world’s 10 largest producers of wind generators, however they primarily serve the home market. Generators, with massive towers and blades, require help and providers at set up websites, and Chinese language companies face difficulties on this case.

Lastly, Chinese language corporations are taking the lead in producing clear hydrogen merchandise, an power supply that might develop over the subsequent decade. One downside with hydrogen is that its manufacturing makes use of vital power, to interrupt down water molecules via electrolysis. The sharp drop in the price of photo voltaic and wind power might finally change the cost-benefit ratio of large-scale clear hydrogen manufacturing.

It’s price noting that Chinese language clean-energy expertise has superior partly due to huge investments in its utility. In 2022, as in different years of the last decade, spending on renewable power capability in China was better than within the U.S. and Europe mixed.

And the U.S.? The Inflation Discount Act, handed by Congress in 2022, will present $400 billion to $1 trillion in help for photo voltaic power, high-capacity batteries, hydrogen manufacturing tools, and different types of renewable power. Jake Sullivan (2023) referred to this and different payments from the Biden Administration as pillars of the nation’s fashionable industrial and innovation technique.

If the U.S. seeks to be completely self-sufficient in clear tech, partly by together with ‘pleasant’ nations and excluding China completely, will probably be more durable to climb the ladder of productiveness and competitiveness. In the event that they attempt to observe the trail symmetrically to what they search to do to the Chinese language in superior semiconductors, on the very least their power transition will probably be dearer.

The Crucial Position Performed by Crucial Uncooked Supplies (CRM)

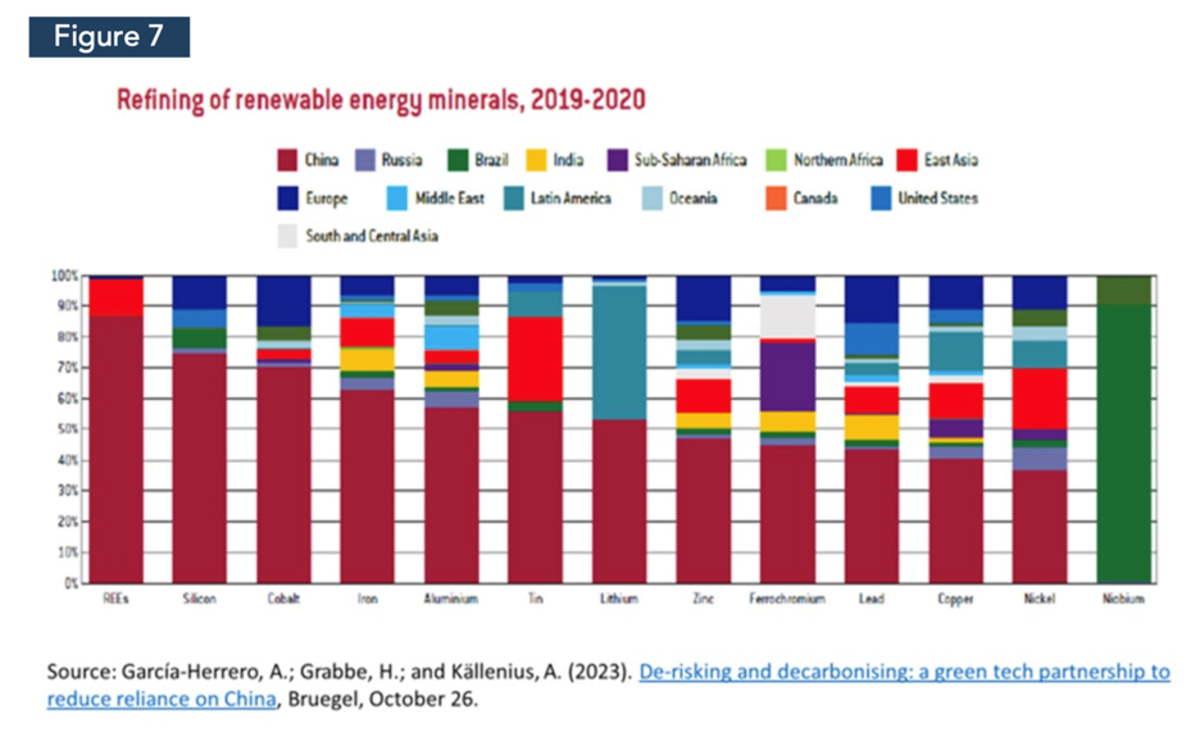

Lastly, it’s price mentioning one other level: mining and refining of vital minerals upstream of the renewable power provide chain. China’s territory is ample in mineral assets, lots of that are central to the manufacturing of clean-tech items, together with 72% of the world’s pure graphite and 66% of uncommon earth parts (Garcia-Herrero et al, 2023).

Nevertheless, total, the extraction of clean-tech minerals is unfold throughout the globe, following the locational dispersion of deposits. Chinese language corporations have been making acquisitions overseas, buying a big a part of the cobalt and lithium provide. Minerals are distributed throughout the globe, however a lot of the refining is in China. Latest threats by China to limit exports of gallium and germanium signify an escalation in international competitors for vital minerals and metals, i.e. yet one more subject for ‘proxy wars’.

Along with the home extraction of key minerals, China has constructed up overseas a community of mineral provide agreements to provide its home refining trade, together with cross-border acquisitions and commerce agreements. These are primarily in southern and western Africa, Oceania, Latin America, and regional neighbors. Globally, China has a particular place by way of processing of uncommon earth parts, with a market share above 85%, and of silicon and cobalt, all of that are integral to the manufacturing of high-energy-density batteries, wind generators, and photo voltaic panels (Determine 7).

China’s share of metals processing is way greater than its share of extraction of these metals. That displays how strategic the Chinese language authorities has been in its long- standing intention to realize dominance of the clean-tech trade.

There is no such thing as a equal initiative on the facet of the U.S., European Union, and different superior economies. Domestically, environmental challenges and dangers—together with depletion of groundwater assets—have been a stumbling block. It could not be straightforward to re-shore processing on a big scale.

This illustrates how pricey and ineffective by way of clean-energy competitors a seek for self-sufficiency can be for the U.S. and different superior economies. An apparent response can be partnerships with rising markets and growing nations (EMDEs) that would come with native refining and a few insertion up within the worth chain by these nations, supplied that environmental dangers and others are correctly handled. By the identical token, as a substitute of reacting to China’s present dominance in clean-energy expertise by taking an inward-oriented, self-contained industrial method, superior economies ought to improve the seek for complementarities and synergies with these EMDEs which have vital potential to be clean-energy suppliers. This might embrace Latin America and the Caribbean (Zhang and Canuto, 2023) and its capability to supply alternatives of ‘powershoring’ (Arbache, 2023), in addition to Africa and different areas.

Concluding remarks

The worldwide economic system at present faces dangers of fragmentation, with nationwide safety among the many causes for nationwide insurance policies of ‘de-risking’ of provide chains, or ‘decoupling’ with China (Canuto, 2023). Such an setting encompasses technological wars as ‘proxy wars’, with sectoral landscapes differing, e.g. with respect to semiconductors and clear power. The methods the U.S. and the European Union method the aim of self-sufficiency, in addition to entry to and refinement of vital uncooked supplies, will make an enormous distinction for his or her stake within the expertise wars.

References

Arbache, J. (2023). What inexperienced and truthful transition? CAF – Growth Financial institution of Latin America, September 13.

Canuto, O. (2019). The US-China Commerce Struggle Is Accelerating China’s Rebalancing, Coverage Heart for the New South, November 8.

Canuto, O. (2021). Climbing a Excessive Ladder – Growth within the International Economic system, Coverage Heart for the New South.

Canuto, O. (2022). Slowbalization, Newbalization, Not Deglobalization, Coverage Heart for the New South, June 1.

Canuto, O. (2023). Development Implications of a Fractured Buying and selling System, Coverage Heart for the New South.

Canuto, O.; Arbouch, M.; Zhang, P.; and Ait Ali, A. (2023). GVCs, Resilience, and Effectivity Concerns: Enhancing Commerce and Industrial Coverage Design and Coordination, G20/T20, June.

García-Herrero, A.; Grabbe, H.; and Källenius, A. (2023). De-risking and decarbonising: a inexperienced tech partnership to cut back reliance on China, Bruegel, October 26.

Sullivan, J. (2022). Remarks by Nationwide Safety Advisor Jake Sullivan on the Particular Aggressive Research Undertaking International Rising Applied sciences Summit, Washington, D.C., September 16.

Sullivan, J. (2023). Remarks by Nationwide Safety Advisor Jake Sullivan on Renewing American Financial Management on the Brookings Establishment, Washington, D.C., April 27.

Wang, D. (2023). The US-China Clear Power Competitors, Gavekal, August 31.

Yoon, J. (2022). Lex in-depth: the price of America’s ban on Chinese language chips, Monetary Instances, November 24.

Zhang, T. (2023). Coping With Semiconductor Containment, Gavekal, August 4.

Zhang, P. and Canuto, O. (2023). International Management for Latin America and the Caribbean, Undertaking Syndicate, September 12.

[ad_2]