[ad_1]

Coverage Heart for the New South

Earlier this month, US Treasury Secretary Janet Yellen instructed congressional leaders that the federal government may run out of money as early as June 1 if the debt ceiling isn’t raised or lifted in time. In January, the Treasury reached the present legally established ceiling in nominal phrases (US$ 31.46 trillion) and the funds at the moment out there to make authorities cost flows are inclined to exhaust by the tip of this month.

Based on the Treasury Division:

“Failing to extend the debt restrict would have catastrophic financial penalties. It might trigger the federal government to default on its authorized obligations – an unprecedented occasion in American historical past. That will precipitate one other monetary disaster and threaten the roles and financial savings of on a regular basis Individuals – placing the USA proper again in a deep financial gap, simply because the nation is recovering from the current recession.”

. Not solely as a result of inflation shrinks its actual worth, but additionally as its rise naturally accompanies the GDP enhance in absolute phrases, the enlargement of presidency capabilities and the need for accumulation of such debt by patrons of bonds thought-about as low-risk “secure haven” for traders on this planet – a minimum of when there is no such thing as a self-imposed harm by the nominal debt restrict.

The truth is, the debt ceiling dates to 1939, when Congress consolidated numerous types of debt into one combination debt ceiling. From then on, the debt restrict has been persistently elevated every time the inventory of public debt approached the restrict.

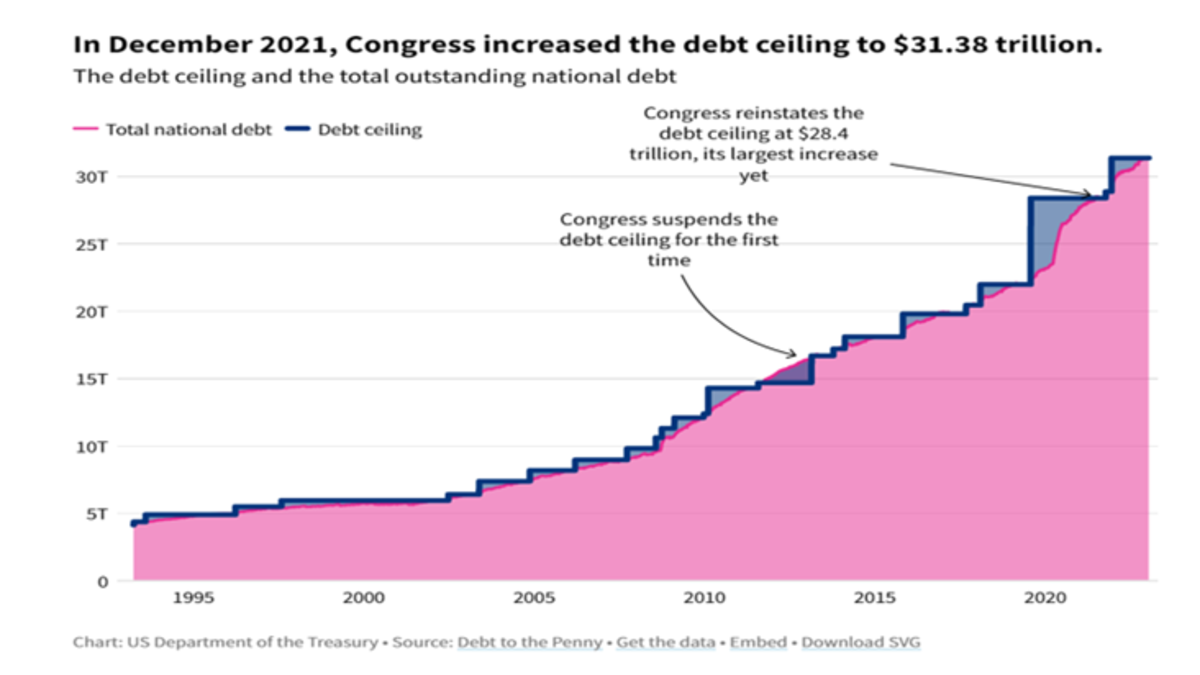

Because the Treasury famous, since 1960 the debt restrict has been raised in some kind 78 instances—49 instances beneath Republican presidents and 29 instances beneath Democratic presidents—to keep away from defaulting on Treasury curiosity funds and preserve the federal government working. Determine 1 depicts such will increase since mid-90s, as much as the newest one in 2021.

Determine 1

Generally with noise and turbulence. In 1979, for instance, the Treasury needed to delay bond funds. A rule was then established permitting the Home to mechanically enhance the debt restrict by finances decision with out requiring a separate vote. This rule was used 15 instances to extend the debt restrict.

Nevertheless, that rule was revoked in 2011, when the Obama administration confronted a Congress with a robust presence of the Republican Tea Get together. It has since seen extended battles over elevating the debt ceiling in 2011, 2013 and 2021. Not in the course of the Trump administration although! It is very important word that the 2011 episode even resulted within the downgrading of the US credit standing by S&P, from the utmost AAA degree to AA+, the place it stays.

The U.S. is, subsequently, at the moment present process a repetition of these moments of rigidity as a consequence of an preliminary deadlock within the congressional resolution on suspending or easing the ceiling restriction. Republicans, with a slight majority within the Home, managed to cross a invoice in late April that will enhance the debt ceiling by US$ 1.5 trillion and kick the danger down the street till subsequent yr. However it got here with the counterpart of lowered bills in packages very excessive in precedence to the Democrats. It might not be accepted by the principally Democratic Senate or the White Home.

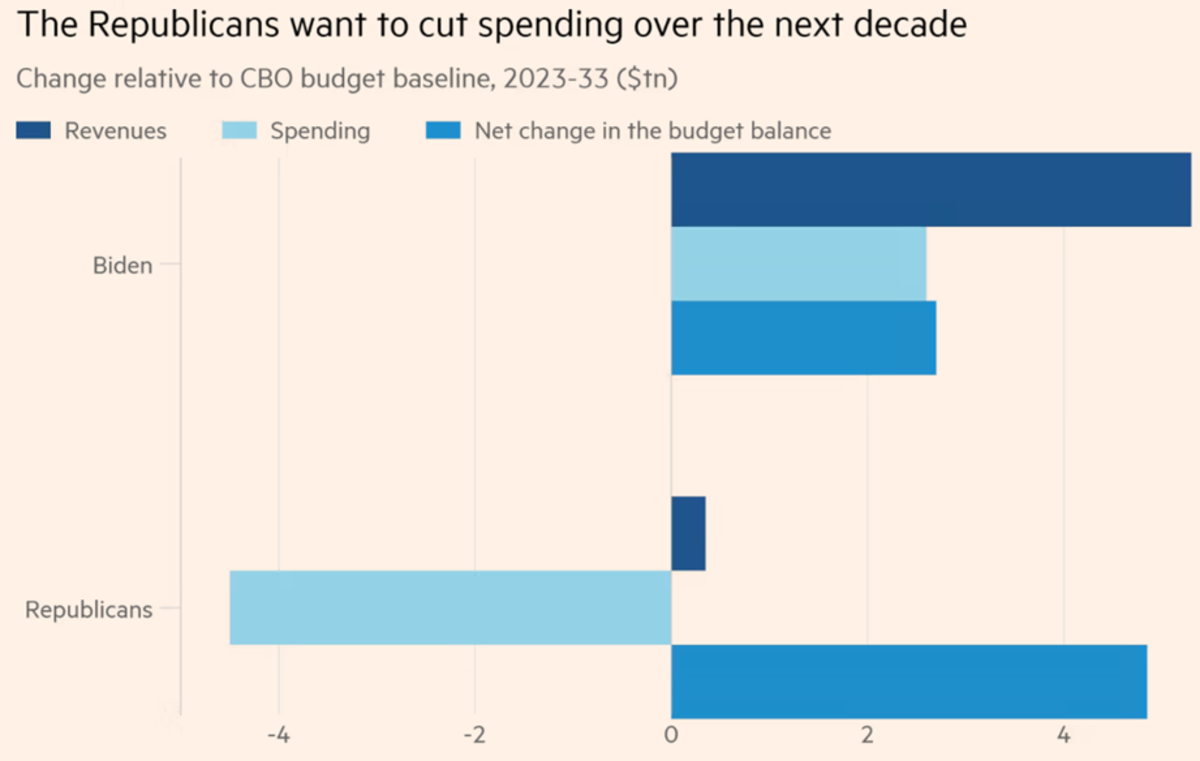

Hope stays that the White Home and Republicans will attain a deal in time to keep away from what Yellen known as “unthinkable” and “catastrophic”. On the coronary heart of the talks are limits on home spending, with Republicans demanding deep cuts in lots of packages over the following 10 years, whereas Democrats settle for extra modest cuts for two years. Determine 2 compares the stances by the 2 primary events.

Determine 2

The White Home rejects the Republican demand for the rollback of unpolluted vitality tax credit that have been handed final yr, with the Inflation Discount Act, in addition to scholar debt aid measures. It additionally doesn’t settle for the institution of labor necessities in packages towards poverty and within the social security internet, because the republicans additional need.

If there is no such thing as a settlement in time, the Treasury can be pressured to delay wage funds, briefly shut some public actions and, on the restrict, default on debt curiosity funds. Within the occasion of any additional downgrading of the credit standing by any company aside from S&P, many asset managers can be pressured to tug US Treasuries out of their AAA asset swimming pools.

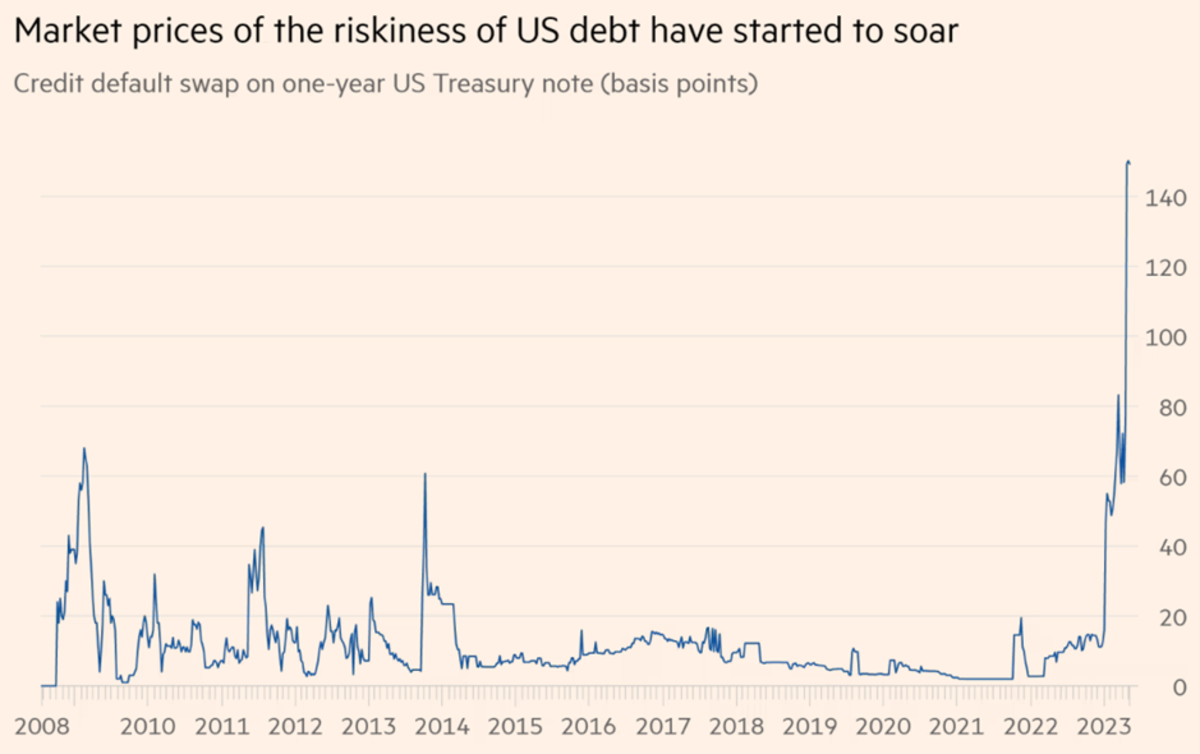

To provide you an thought of the notion of default dangers by the markets, credit score default swaps (CDS) – derivatives that work as insurance coverage and pay if an organization, or nation, defaults on its loans – for one-year Treasury bonds have been, final week, increased than the equivalents for Greece, Mexico, and Brazil (Determine 3). For longer titles, corresponding to 5 years, the scenario was not so irregular. However spreads between 1-month and 3-month Treasuries hit a document excessive of as much as 180 foundation factors. Not by probability, this week’s information about constructive conversations between the 2 sides led to US futures and European equities rising on Thursday as traders grew extra assured {that a} US authorities default can be averted.

Determine 3

On Thursday of final week, the Worldwide Financial Fund (IMF) drew consideration to the intense penalties of any default by the US public sector, even when non permanent, for the nation and the worldwide economic system. Nobody can say what the chain reactions of a shock to the very low threat “secure haven” of worldwide finance can be.

As if the shocks suffered in the course of the “excellent storm” of current years weren’t sufficient! With the distinction that, on this case, it isn’t a matter of markets suspending debt rollover as a result of they contemplate it bancrupt, however of a politically self-imposed barrier by the nation itself. The occasional references by Republicans – together with former President Trump – {that a} default and market turbulence could also be an satisfactory worth to acquire public spending cuts are of concern.

There are authorized gadgets that correspond to methods to avoid the ceiling and keep away from what can be the primary default by the federal authorities within the historical past of the nation: issuing platinum forex value US$ 1 trillion, with its deposit on the Federal Reserve; or an enchantment to the 14th Modification to the Structure, the place there may be point out of the opportunity of issuing debt to pay commitments with out passing by Congress. Such gadgets, nevertheless, being legally contestable, have been thought-about as “dangerous choices” by Secretary Yellen and as “loathsome” by Fed Governor Jerome Powell. An settlement with Congress on the debt ceiling stays the one appropriate choice.

Concern with the trajectory of the US public debt was contained whereas the interval of low rates of interest lasted, significantly when these have been decrease than the GDP development charge, as Olivier Blanchard has all the time emphasised. Now, it is smart what a number of voices like Glen Hubbard and others have advocated, specifically, the institution of some fiscal framework to take care of the matter, as a substitute of nominal spending caps. However this transition needn’t occur by way of monetary shocks and a doable default on public debt. Subsequent week stays a deadline for an settlement on lifting the nominal debt ceiling to keep away from “unthinkable” upheavals.

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement. He’s a former vice chairman and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund, and a former vice chairman on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil.

[ad_2]