[ad_1]

Authentic at Coverage Middle for the New South

Summary

The warfare in Ukraine is bringing substantial monetary, commodity worth, and provide chain shocks to the worldwide financial system. Sanctions on Russia are already having a major impression on its monetary system and its financial system. Value shocks may have a world impression. Power and commodity costs—together with wheat and different grains—have risen, intensifying inflationary pressures from provide chain disruptions and the restoration from the pandemic. The push towards relative deglobalization obtained from the pandemic will get stronger. One could count on an growing weight of geopolitics in worldwide funds and within the entry to particular commodities.

Along with the human toll and injury to the native financial system, the warfare in Ukraine is bringing substantial monetary, commodity worth, and provide chain shocks to the worldwide financial system.

The sanctions established towards the Central Financial institution of the Russian Federation have already restricted its entry to worldwide reserves and made it more durable to again its foreign money and monetary system. Worldwide sanctions on Russia’s banking system and the exclusion of some banks from SWIFT have considerably disrupted Russia’s means to obtain funds for exports, pay for imports and interact in cross-border monetary transactions. Sanctions are already having a major impression on the Russian monetary system and its financial system. They can even convey some spillovers to different economies.

. As poor households spend a excessive proportion of revenue on meals and gasoline, they are going to be notably damage.

The warfare additionally introduced a adverse shock to each inflation and financial exercise in lots of international locations, amid already excessive inflationary pressures. Central banks have been already dealing with a must stroll on a tightrope between curbing inflation and sustaining monetary stability. The warfare in Ukraine has made such a rope thinner.

The Weaponization of finance

The warfare might be devastating for Ukraine. The financial sanctions towards Russia, in flip, introduced by the US and Europe following the navy invasion of Ukraine are having a profound impression on the Russian financial system whereas additionally having repercussions in every single place. As in a boxing match, the expectation is that blows to the opponent can knock them out, regardless of the publicity on the punching facet.

America has utilized some sectoral and restricted financial sanctions towards Russia because the annexation of Crimea in 2014 and the navy clashes in jap Ukraine. Nothing comparable, nevertheless, to what was introduced within the weekend after the entry of Russian troops into Ukraine.

Between February twenty second and twenty seventh, we had bulletins by the US, the 27 members of the European Union and the G7 international locations of freezing belongings of enormous Russian banks, some Russian people, and controls on the export of expertise merchandise. Culminating with eradicating some Russian banks from the SWIFT system and banning transactions with the Central Financial institution of Russia.

SWIFT is a messaging community connecting banks worldwide that’s thought-about a spine of worldwide finance. SWIFT is a consortium managed by workers of member banks, together with the USA’s central banks, Europe, Belgium, England, and Japan. Based mostly in Belgium, it’s a consortium linking greater than 11,000 monetary establishments in additional than 200 international locations and territories, working as a hyperlink that makes worldwide funds attainable. To offer you an concept, in 2021, the system recorded a mean of 42 million messages per day, together with requests and confirmations of funds, negotiations and foreign money exchanges. Over 1% of those messages are believed to have concerned Russian funds.

Would there be any alternate options for Russians to switch and normalize their operations outdoors of SWIFT? Russia has another community, the System for Switch of Monetary Messages, however it can’t be a alternative. By the tip of 2020, the system solely included 400 individuals from 23 international locations. Additionally, China’s Cross-Border Interbank Cost System couldn’t be an ideal alternative, no less than quickly, because it doesn’t incorporate SWIFT members.

The banning of transactions with the Russian central financial institution is the main jab. In addition to being the lender of final resort to industrial banks in its home foreign money, it’s also the lender of final resort in overseas change. Overseas change reserves matter not just for avoiding change charge crises but additionally as a result of they forestall runs on banks and make attainable funds of the overseas debt of state and personal firms. And there was an growing digitalization of worldwide finance.

The majority of nations’ overseas reserves now not is made from not bodily certificates of presidency bonds or shares of money in {dollars}, euros, kilos, and yen. They’re now digital guide entries on the pc ledgers of the Federal Reserve Financial institution of New York, the European Central Financial institution, European nationwide central banks, the Financial institution of England, the Financial institution of Japan, and Swiss industrial banks.

Digitalization creates a wedge between possession and management of overseas change reserves, as western issuers and computerized holders of those belongings management entry to belongings regardless of Russia’s proudly owning them. The closure of Russia’s entry to those belongings, freezing them, and prohibiting all personal transactions with the Russian central financial institution immediately halted any attainable sale of securities and money withdrawal from western banks. As nicely summarized by Michael Bernstam (Monetary Instances, March 22):

“In lower than sooner or later, the Russian central financial institution and Russians misplaced entry to 60 per cent of .X.F.X. reserves, $388bn out of a complete $643bn. They misplaced entry to total arrays of belongings: securities and deposits in western central banks ($285bn) and in western industrial banks and brokerages ($103bn). The Russian central financial institution is left with $135bn price of gold in its vaults, $84bn of Chinese language securities denominated in renminbi, a $5bn place within the IMF and a residual $30bn in precise money, {dollars} and euros. (These are my calculations from central financial institution information).

With 60 per cent of .X.F.X. reserves out of fee, Russia has to depend on the remaining 40 per cent, however there isn’t any freedom to function there both. The central financial institution can’t promote gold for {dollars} and euros as a result of all transactions with it are prohibited and overseas bankers and sellers don’t need to invite western wrath. The IMF reserve place is untouchable. Some $84bn in Chinese language securities might, hypothetically, have been offered again to China, with a reduction, to be paid in {dollars}, minimize to $50bn, however China’s state banks have already refused monetary offers with Russia. Which leaves solely $30bn in money — too little to forestall monetary and financial smash.“

Sanctions are already having a major impression on the Russian monetary system and its financial system. The Ruble’s worth collapsed, shedding over 30% of its worth within the following week. The Central Financial institution of Russia was led to place rates of interest up excessive to restrict the transmission of foreign money devaluation to inflation. The financial institution run by the inhabitants started over the weekend by ATMs. Restrictive capital controls and financial institution holidays have grow to be are the brand new regular.

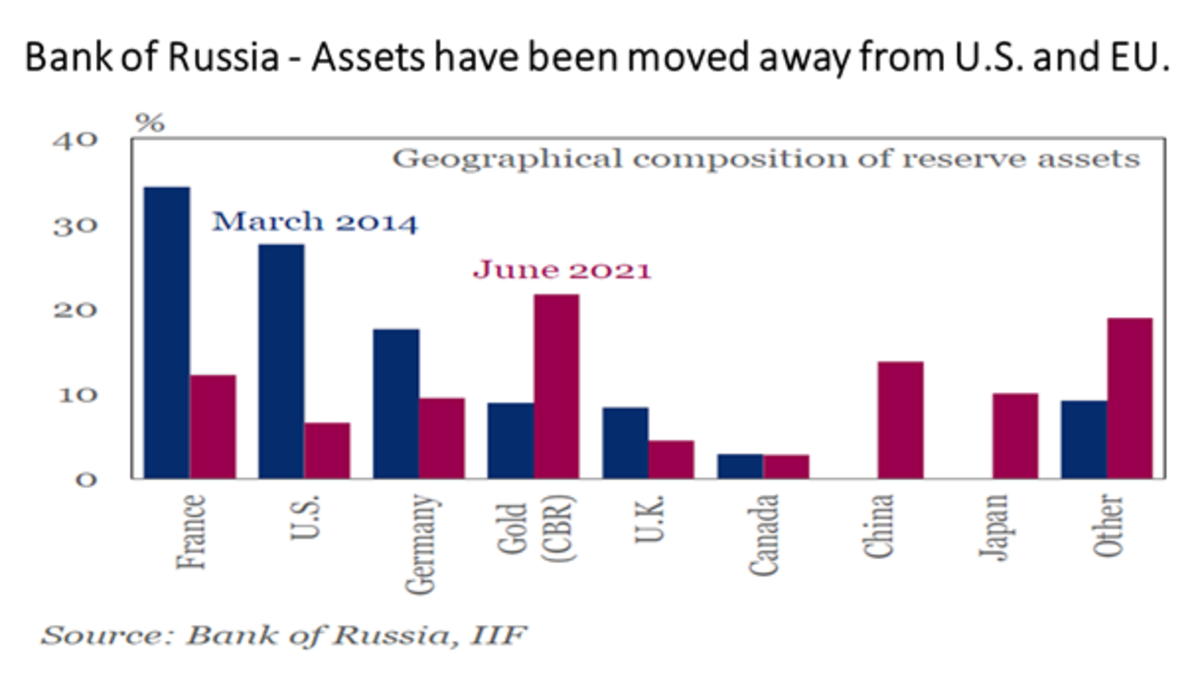

Regardless of the technique of lowering publicity because the starting of sanctions in 2014, by way of geographic relocation of reserves and acquisition of gold, and altering currencies in industrial transactions – a type of “de-dollarization” – Russia has not grow to be invulnerable and the impression might be vital – Determine 1. The GDP contraction is not going to be mild, given the tightening of monetary situations accompanying ultra-high rates of interest and banks with out entry to overseas foreign money.

Determine 1

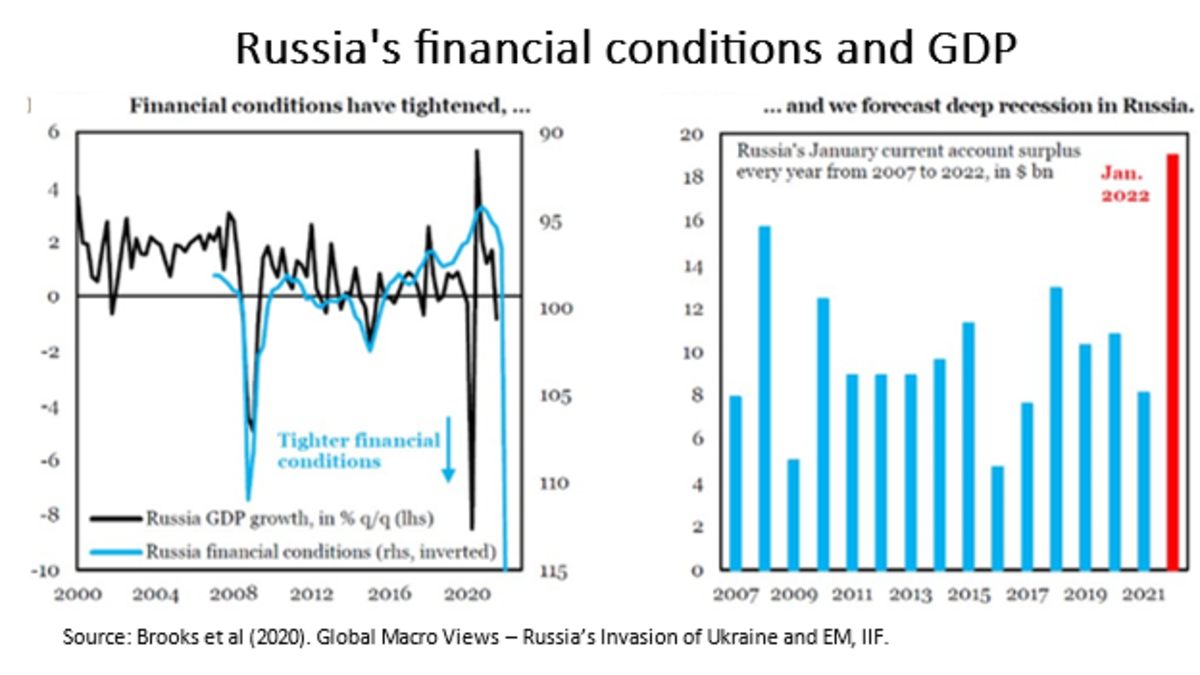

Determine 2 reveals the impression on Russia’s monetary situations – as measured by a composite of the falling Ruble, the inventory market collapse, rising bond yields plus credit score spreads – and on GDP. JPMorgan is forecasting a GDP downfall by 35% within the 12 months’s second quarter. A authorities debt default in March is predicted.

Determine 2

The sanctions have been tentatively designed to attenuate their impact on Russian fuel imports into Europe. The sanctions introduced on February 26 have been extra restricted in scope than the broader concentrating on advocated by different international locations to win Germany’s assist. They don’t impression ‘Russia’s vitality sector transactions, and the .U.E.U. has not sanctioned a few of Russia’s largest banks. Consequently, euro- and dollar-denominated funds can proceed to circulation by Russia’s vitality exports.

Europe and the U.S. appear to be reluctant to implement such measures. That would change with further rounds of sanctions, and Russian corporations are extensively disconnected from SWIFT. And even when Russia’s banking sector is primarily unplugged from SWIFT, Beijing and a few in Europe could use various funds channels to maintain euro and renminbi funds flowing to Russia; already, greater than half of Russian exports usually are not greenback denominated.

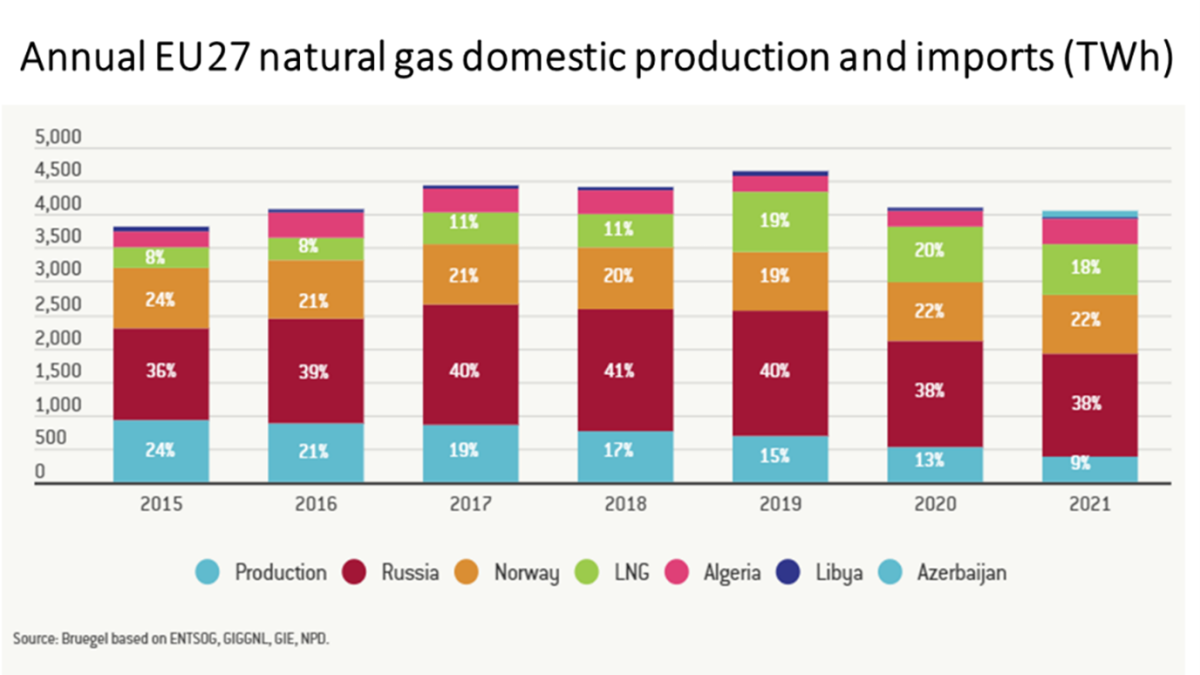

The Bruegel Institute, a Brussels-based suppose tank, tackles eventualities of how Europe would undergo from a halt within the circulation of Russian fuel (Determine 3). Regardless of the self-inflicting ache, halting fuel imports instantly would nonetheless be attainable.

Determine 3

With some collateral injury

And outdoors Russia? In fact, the receiving facet of funds – collectors, asset buyers – can even be impacted. Russian defaults are virtually inevitable. The implications of that may solely be prolonged if the devaluation of the corresponding belongings results in some contagion impact – for instance, withdrawal of funds by buyers in mutual funds forcing their managers to liquidate different belongings of their portfolios to pay for the withdrawal of funds.

How about fears and threat aversion in monetary markets? In fixed-income markets, the week after sanctions, U.S. government-bond yields began buying and selling round 25 foundation factors decrease than earlier than the invasion. Whereas half of this drop could possibly be attributed to uncertainties generated by Russia’s invasion, the opposite half has been taken as because of a downward motion of expectations in regards to the Fed’s pace of financial tightening forward. The Fed is predicted to boost its primary charge solely by 0.25% in March 15-16, reasonably than 0,5% as beforehand anticipated. Additionally, the variety of anticipated rate of interest hikes this 12 months has declined to five as an alternative of seven.

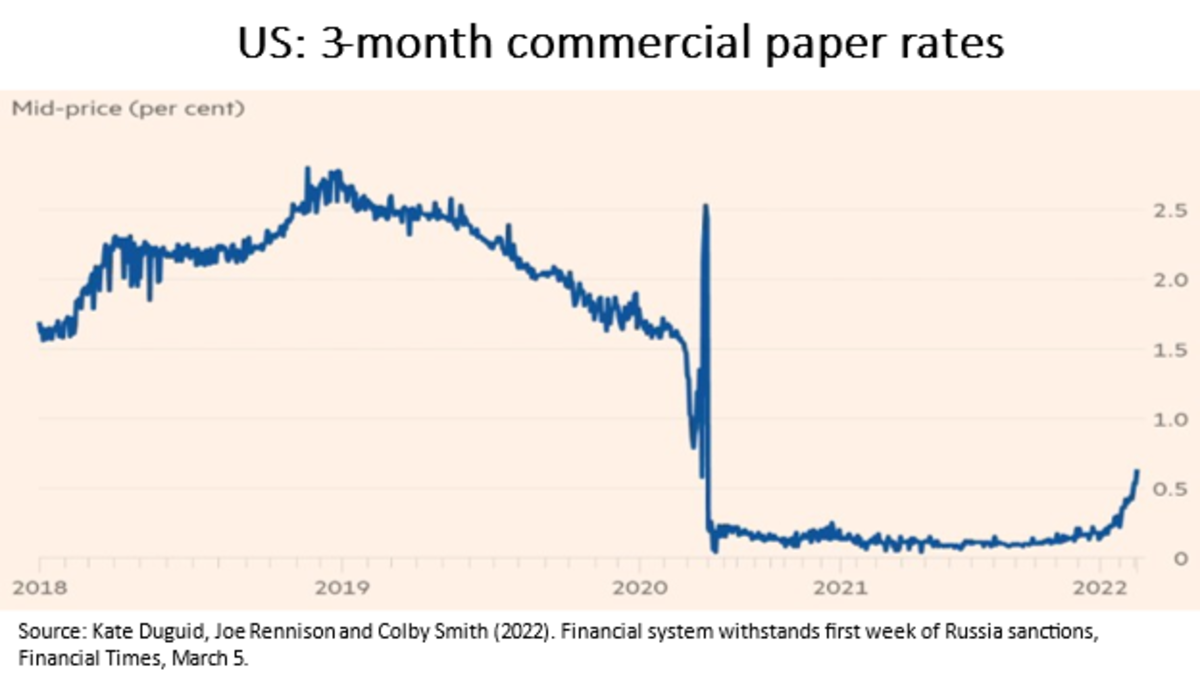

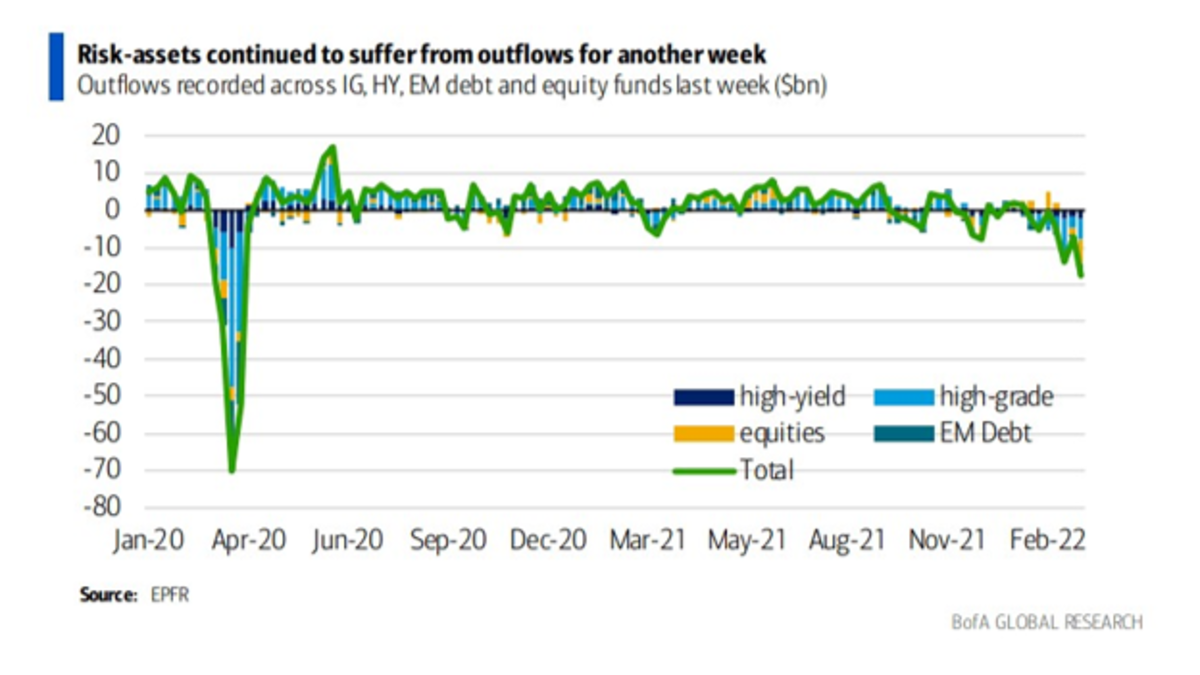

Ranges of short-term borrowing stress have gone up. Determine 4 reveals charges on three-month industrial papers, and there may be nothing comparable to date to moments of crises up to now. The Federal Reserve services boosted throughout the pandemic to assist overseas central banks haven’t been used. At the very least within the first week after sanctions on Russia, there was no worry of illiquidity and “sprint for money”. It’s price noticing, then again, an uptick on the exit from threat belongings that had been within the course earlier than the invasion and sanctions (Determine 5)

Determine 4

Determine 5

It’s too early to make any definitive name – amongst different causes as a result of huge defaults in funds from Russia haven’t kicked in but, with corresponding results on chains of securities that depend upon Russian belongings. However one could acknowledge that there was an enormous blow to the system of world funds. The precedent of concentrating on a significant nation’s overseas reserves tends to have long-term enduring impacts.

Almost definitely, China – and Russia – will speed up any plans it might have on disconnecting from U.S.- and EU-led funds channels. Beijing is poised to seek for boosting a China-led, renminbi-denominated funds channels throughout Asia—together with in Russia—which can be primarily out of attain of U.S. sanctions and fewer depending on SWIFT.

Nonetheless on the sanctions on Russia, one related challenge might be to outline how and when sanctions can be reversed. To work successfully as a way of strain, sanctions have to be built-in into a transparent pathway indicating what Russia must do for sanctions to be lifted (Greene, 2022).

Commodity worth shocks.

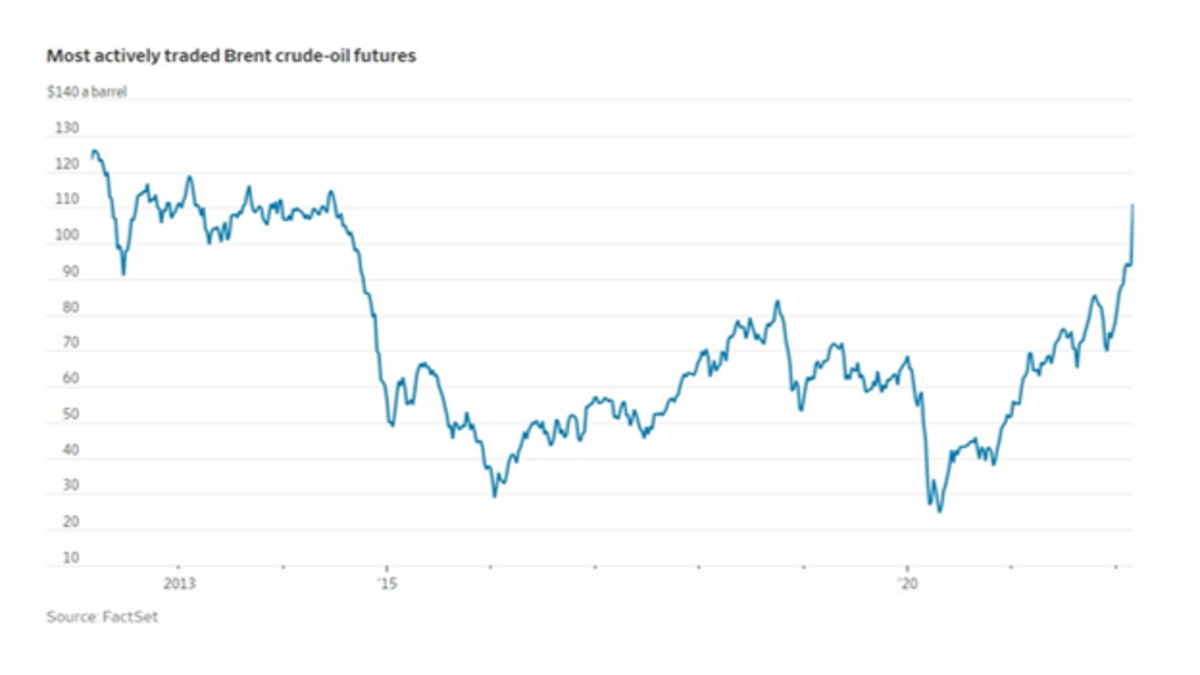

Within the week after the invasion, commodity costs rose at a tempo with out precedent within the final 50 years. Oil costs rose to $120 a barrel, the very best degree since 2012, whereas wheat costs climbed by nearly 50%.

The sanctions package deal introduced on February 26 was designed to spare oil and fuel funds to Russia. Nevertheless, with merchants now afraid of the dangers related to coping with any Russian counterparties, many have chosen to not buy Russian oil this week, resulting in a brand new rise in oil costs.

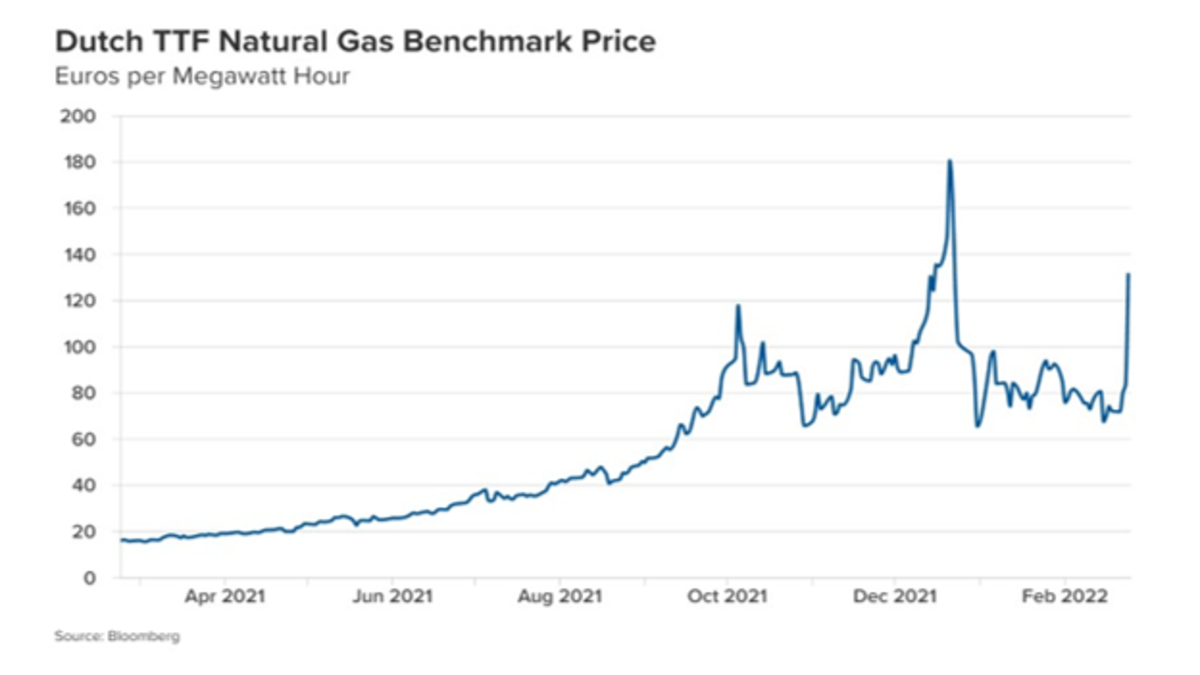

Via the rise in vitality commodity costs – along with attainable restrictions on the logistics of Russian merchandise – the warfare in Ukraine will have an effect on most economies in the remainder of the world. Determine 6 shows the current evolutions of the Dutch TTF pure fuel worth, and Determine 7 depicts the current evolution of oil costs.

Determine 6

Determine 7

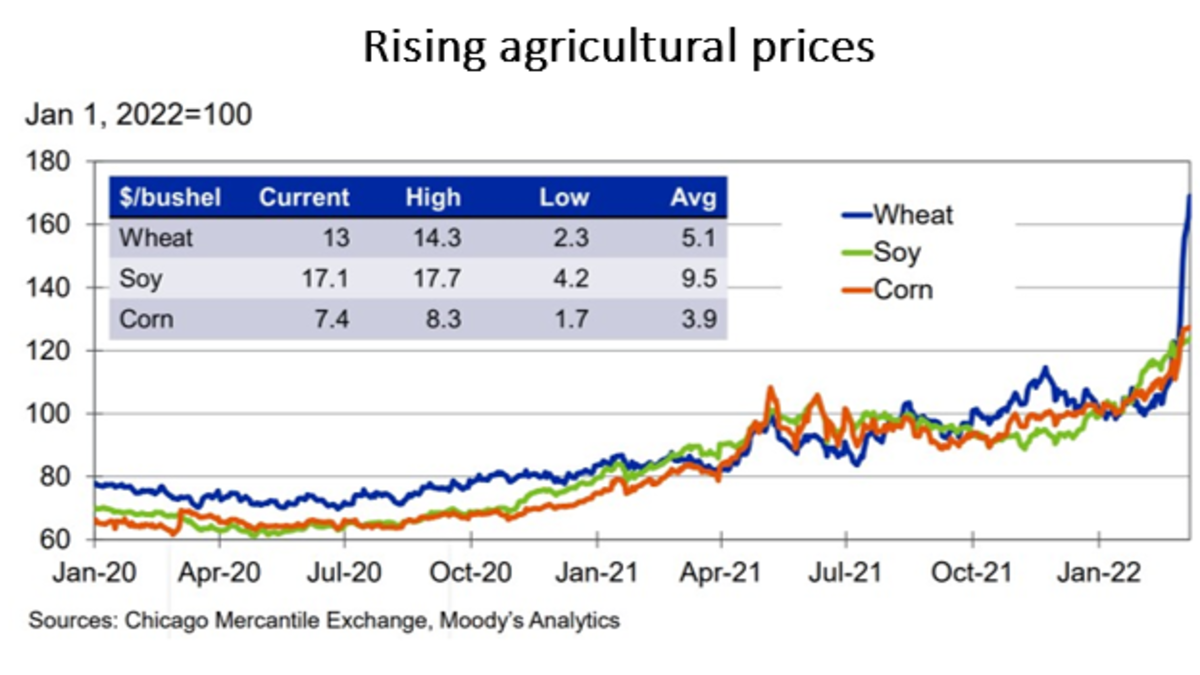

Moreover, there’s a statistically confirmed asymmetry: what occurs within the subgroup of vitality commodities impacts the others, akin to meals and metals (Yang et al., 2021). Meals costs have been going up (Determine 8).

Determine 8

A selected meals commodity to really feel the impression of the warfare might be wheat – which is especially impactful in some areas, akin to North Africa and the Center East, as seen in Determine 8. Russia and Ukraine are sources of just about a 3rd of the worldly traded wheat.

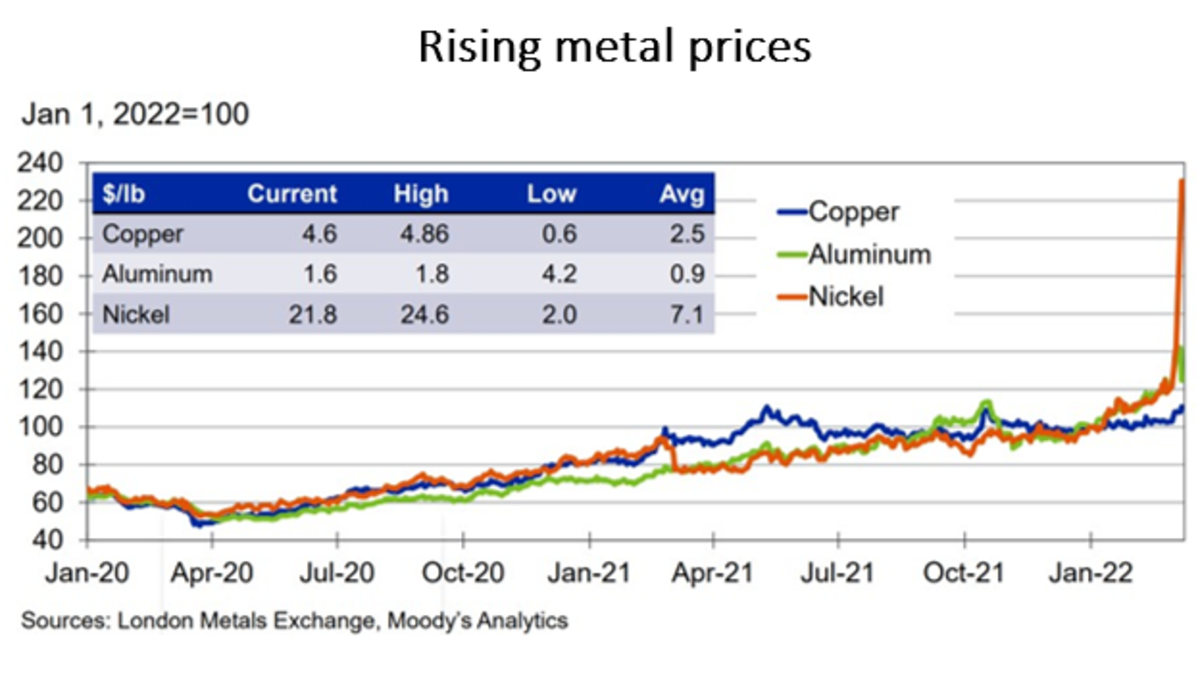

Russia can also be a major provider of fertilizers, palladium, aluminum, and different merchandise which can be affected by logistic “provide chain restrictions” provoked by navy battle, sanctions, and voluntary restrictions to commerce. The aluminum and metal produced by Russia is utilized in a variety of manufactured items, from beverage cans to smartphones to automobiles. Ukraine and Russia are substantial sources of palladium and platinum, and each used to fabricate catalytic converters for the auto business. Platinum, copper, and nickel are important inputs for electrical autos’ batteries. Ukraine can also be the supply of fifty% of the world’s neon fuel, which is used for lasers employed in manufacturing semiconductor chips – one could guess that the worldwide semiconductor chip scarcity is unlikely to finish quickly.

Belarus, a detailed Russian ally, is a superb producer of potash, a key fertilizer enter. Sanctions on the nation will negatively have an effect on its availability. Meals commodity exporters could accrue a acquire— if they don’t depend upon Belarusian potash — however importers that depend on shopping for important meals and gasoline on worldwide markets might face dire situations.

Market costs (Determine 9) are reflecting a perception {that a} provide discount for a while could be taken with no consideration time, and injury could have already got been carried out to potential yields. Costs are reflecting a geopolitical threat premium. The impression of the warfare on commodities tends to remain for a while, even when it often eases barely.

Determine 9

Provide chain disruptions

These provide shocks intermingle with the availability chain disruptions which have affected macroeconomic efficiency and inflation throughout the pandemic (Canuto, 2021a). Army conflicts are certain to convey further challenges.

Transportation and logistics industries are being affected: flight cancellations, greater strain on cargo capability due to re-routings, closure of Ukrainian ports, the banishment of Russian ships from U.Okay. ports, and the suspension of Russian cargo bookings by the world’s most distinguished transport teams (Moody’s, 2022). Already lengthy supply instances and transport and producer prices are rising.

Moreover, the navy battle and sanctions on Russia additionally impression the worldwide provide of these commodities exported by Russia and Ukraine beforehand talked about. Power and commodities commerce with Russia has not been sanctioned but, however commerce with Ukraine has paralyzed.

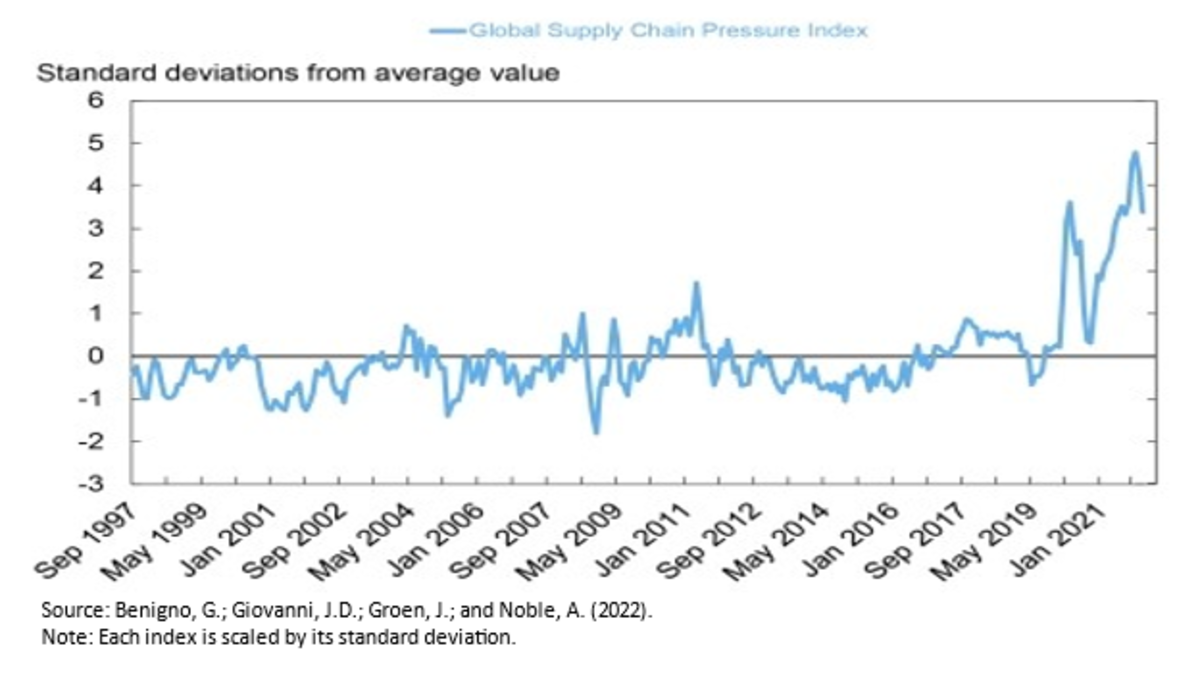

The availability chain disruptions have been but a major problem earlier than Russia’s invasion of Ukraine. Determine 10 reveals an index of world provide chain strain developed by the Federal Reserve Financial institution of New York by February 2022, pointing to an easing since December 2021, although remaining at traditionally excessive ranges with numbers (Benigno et al., 2022). The following figures will doubtless convey index hikes.

Determine 10

Like within the case of finance, the warfare in Ukraine has raised consideration to the best way that many uncooked supplies have the potential for use as weapons of overseas coverage — primarily if a brand new chilly warfare develops that divides Russia, and doubtlessly China, from the west. Geopolitics will convey commodities to its heart. To some extent, this brings some echoes from the period of Imperialism.

Dangers of Stagflation

In most superior economies, inflationary acceleration has been going down. Japan was an exception. Shopper worth inflation ended 2021 at annualized charges of 6,7% within the U.S., 4.6% within the Euro space, 4.9% in U.Okay., and 5.1% as a mean of developed economies.

This has already led financial authorities to challenge indicators of shifting in the direction of much less accommodative insurance policies. Extra regularly within the Euro space, whereas bets amongst analysts on the U.S. Federal Reserve’s future selections even included, earlier than the warfare in Ukraine, 6 or 7 will increase in its base charges this 12 months, maybe together with even the start of the shrinkage of the asset portfolio on its stability sheet – a “quantitative tightening (Q.T.)” following the tip of “quantitative easing (Q.E.)”. An increase in March – 25 or 50 foundation factors – grew to become taken with no consideration.

To various levels throughout international locations, this rise in inflation charges has mirrored an unexpectedly sturdy restoration in demand, notably within the case of superior economies which were in a position to resort to beneficiant fiscal packages to assist households and companies. This isin a context of restricted entry to low cost vitality items and inputs. The inflationary shock coming from greater commodity costs and new restrictions on provide chains because of warfare in Ukraine will intensify the present dilemma confronted by central banks on either side of the Atlantic. How rapidly and intensively to tighten monetary situations within the face of inflation that may now not be seen as merely non permanent and reversible whereas searching for to not convey down the tempo of financial exercise or set off monetary shocks (Canuto, 2021a). As we now have remarked, the deteriorating macroeconomic outlook has prompted analysts to foretell that the Federal Reserve is not going to determine on a 50-basis level hike at its March assembly, opting as an alternative for 25 foundation factors.

There’s a worry that these economies returned to situations like these of the early Eighties when the second oil shock occurred whereas inflation was already excessive. The wager is that Jerome Powell and his colleagues usually are not like Paul Volcker, chairman of the Federal Reserve on the time, whose choice was to convey down inflation at any value.

Rising inflation has been broad-based within the U.S. and Germany (And this was earlier than the warfare in Ukraine, and the shocks approached heretofore. The rise in U.S. inflation has been broad-based to an extent unprecedented in current historical past.. Although this does not deal with how persistent excessive inflation would are typically, it does lean away from its view as reflecting relative worth adjustments in favor of broad, demand-led inflation. Eurozone inflation additionally seemed generalized, although primarily because of Germany.

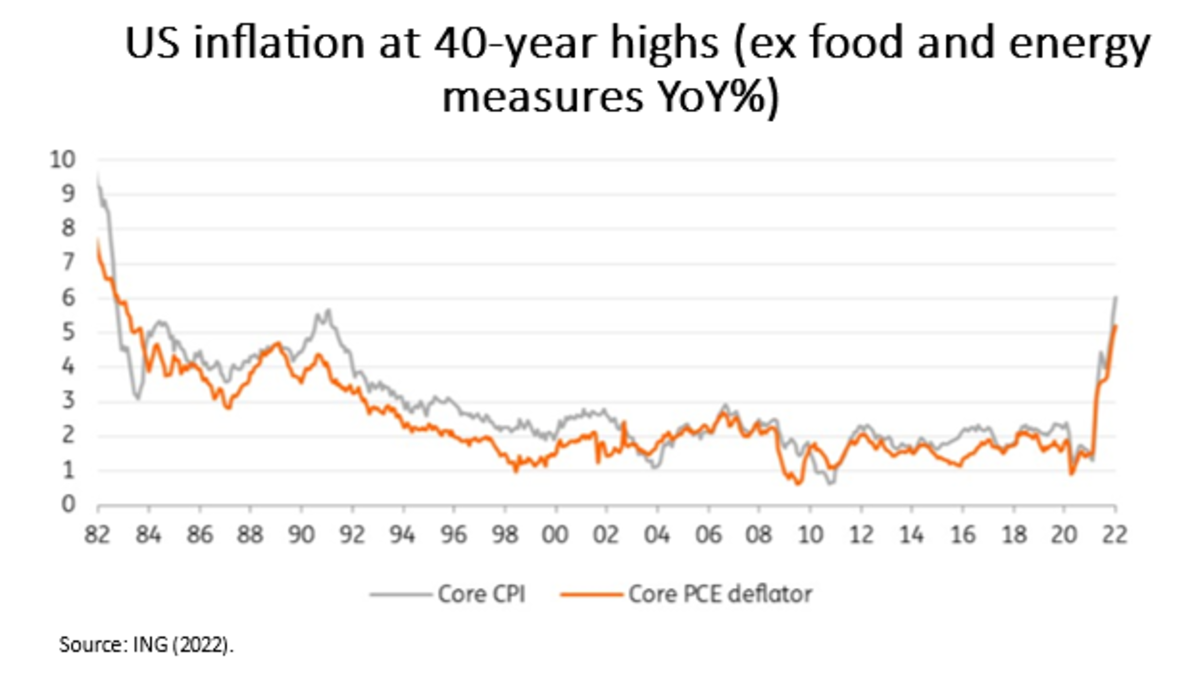

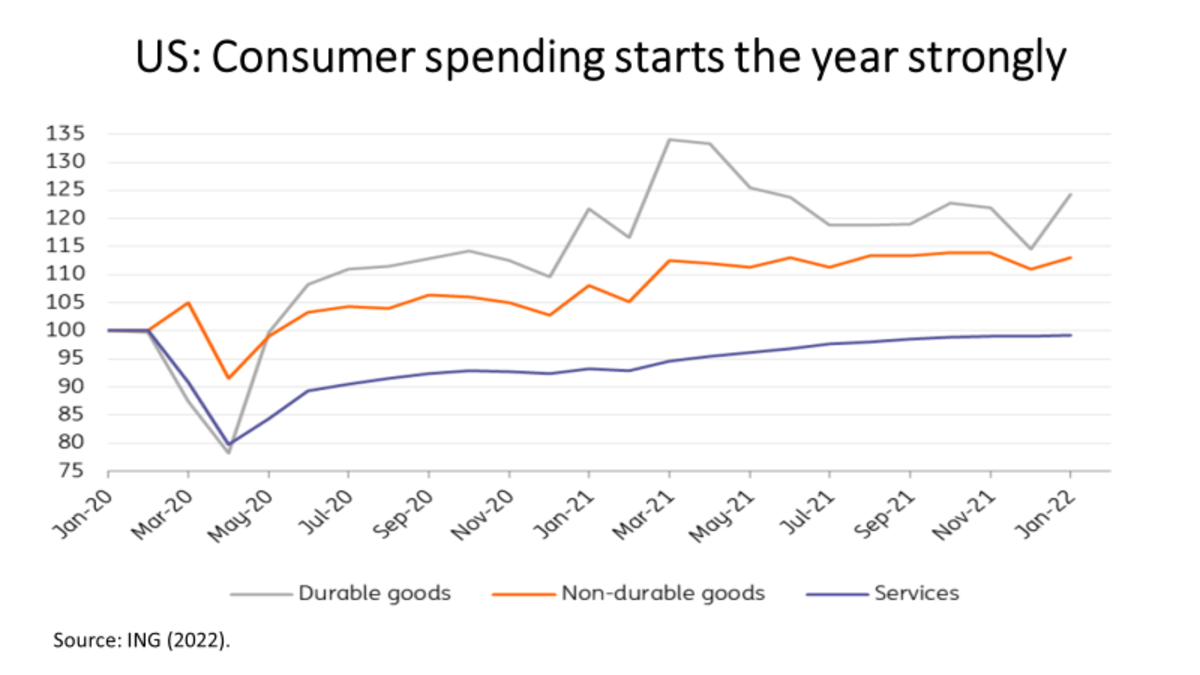

The U.S. inflation has been at 40-year highs, reaching an annual charge of seven.9% in February (Determine 11). The power of shopper spending originally of the 12 months (Determine 12) favors the notion that inflation displays a mixture of provide shocks and overheating demand, rising above potential GDP progress. It has grow to be onerous to argue that inflation is transitory and reversible after the unwinding of provide chain disruptions with out crucial tightening of financial situations. The purpose of debate grew to become the pace and depth of tightening monetary situations forward.

Determine 11

Determine 12

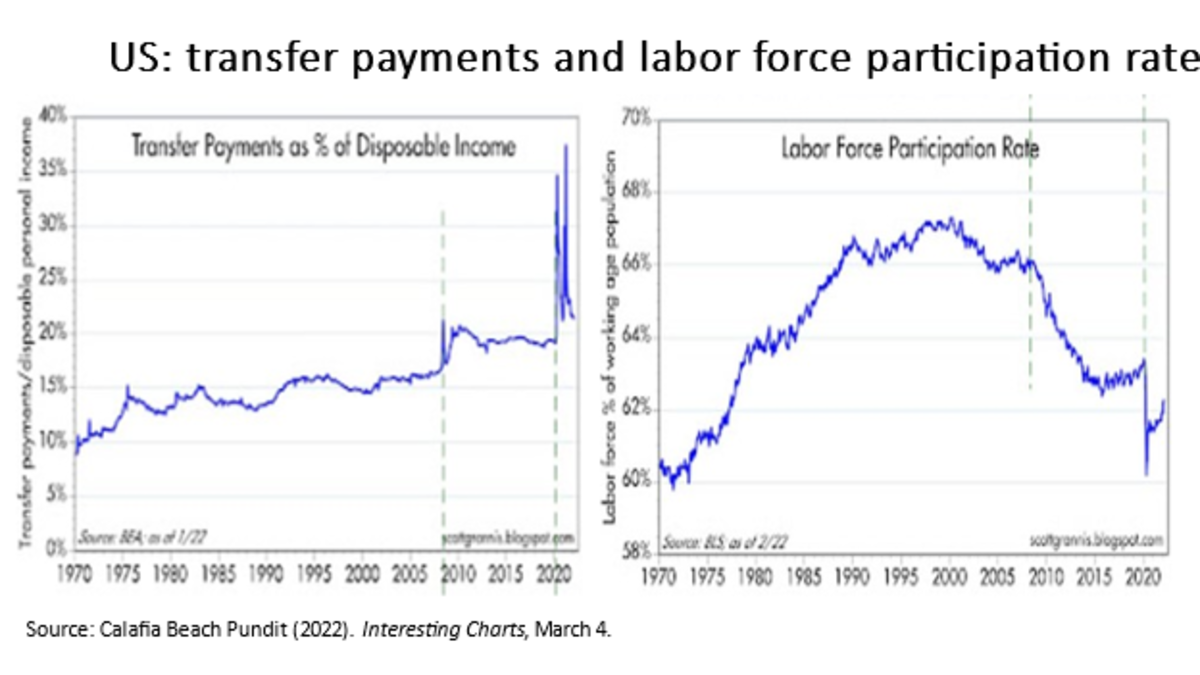

TheU.S. February jobs report got here sturdy, additionally signaling that the “nice resignation” has been succeeded by greater labor drive participation charges after the decline in switch funds (see Determine 13).

Determine 13

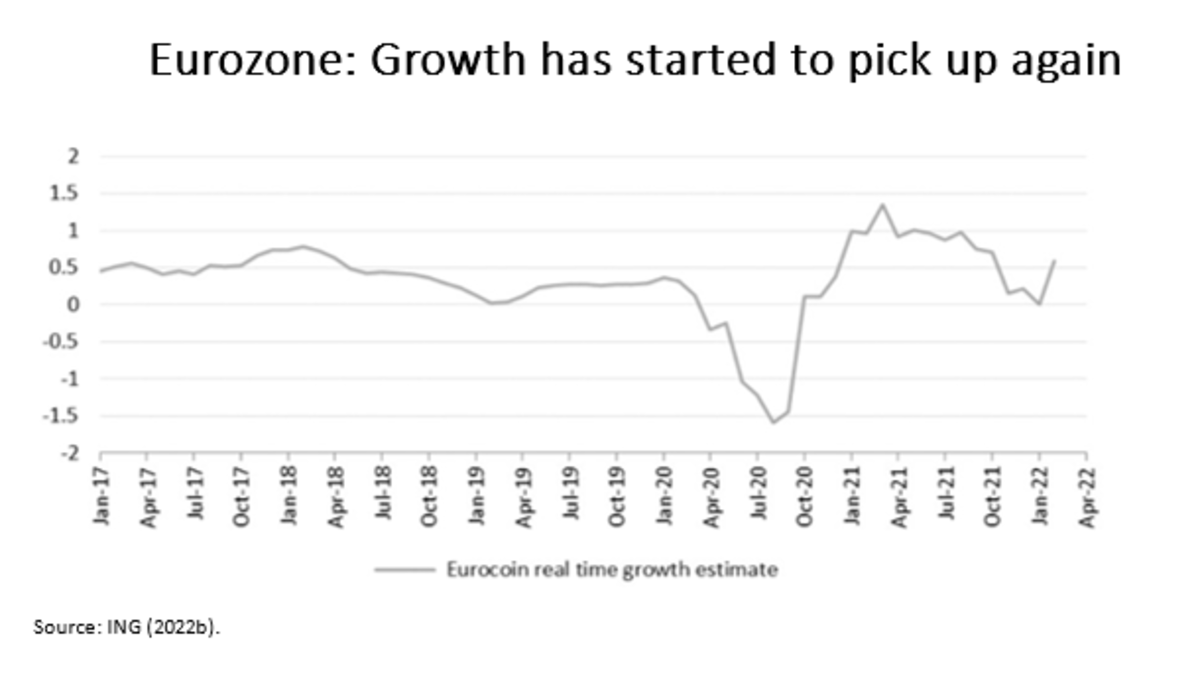

In Europe, an IMF Working Paper launched in February estimated that offer shocks accounted for half of the rise in European producer costs in 2021, with the remaining linked to sharp will increase in demand (Celasun et al., 2022). Whereas progress momentum seemed selecting up extra lately (Determine 14), inflation has been on the rise (Determine 15). Then comes the warfare in Ukraine and the additional spherical of worth and provide chain shocks highlighted.

Determine 14

Determine 15

Though the U.S. job efficiency and (no less than till lately) Europe’s progress prospects seemed shiny, the Worldwide Financial Fund (IMF, 2022) word to the G20 Finance Ministers and Central Financial institution Governors’ Conferences of February 17–18 highlighted a slowdown within the tempo of the worldwide financial restoration. Having revised its forecast for international financial progress this 12 months downwards (4.4%) in January, the IMF cited indicators pointing to the continued weakening of the restoration. Because the Russian invasion of Ukraine, not by probability forecasts for the U.S. financial progress this 12 months have been barely downgraded, as a consequence of worsening monetary situations, greater oil costs, and decrease shopper sentiment.

In keeping with the IMF word, the principle draw back dangers recommended earlier have materialized, affecting the restoration prospects. Mismatches between demand and provide availability in a number of sectors, bottlenecks in freight transport, and will increase in vitality and meals costs pushed inflation up.

In a number of economies, this worth enhance prolonged to all classes of consumption. Whereas supply-side shocks could possibly be thought-about non permanent and regularly reversible all year long, the notion grew to become that the mismatches between provide and demand would even be reflecting excesses in combination demand.

The IMF surveillance word remarked that fiscal assist towards the pandemic disaster is regularly being withdrawn. It even talked about prospects for a fiscal package deal in the US that will be smaller than beforehand envisioned.

It couldn’t be anticipated that the unprecedented tempo of world progress final 12 months, after the drop in 2020, could possibly be replicated in 2022. Nevertheless, the word highlights that a lot of the accountability for the downward revision of projections in January stemmed from slower progress estimates for the US and China. Within the case of China, they listed the continuity of stress in the actual property market, the low dynamism in personal consumption, and the restrictive character of the “COVID-zero” coverage.

Effectively then. How rapidly reversible will these shocks be? And what in regards to the degree of attribution to offer to extra demand relating to the mismatch between demand and provide, even underneath situations of normalization of the second? Which variable to take a look at to see if “non permanent” inflation will depart penalties that may require a financial tightening higher than that then signaled by central banks?

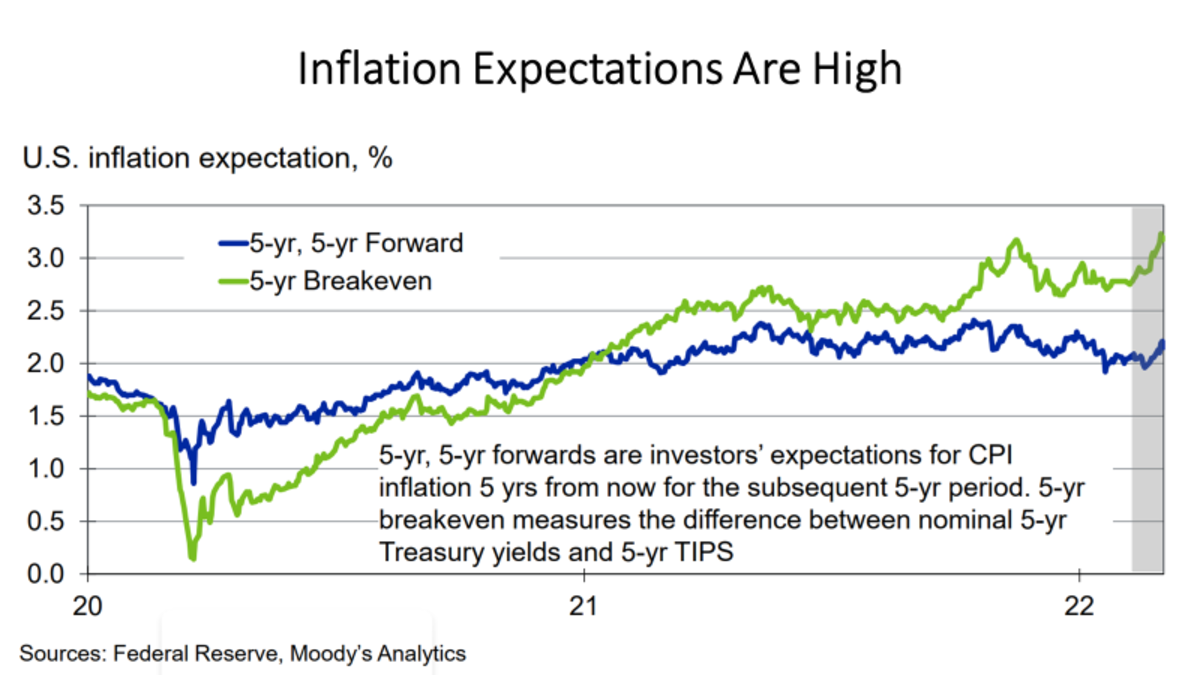

Consideration have to be paid to 2 key variables. First, expectations of inflation by personal brokers. The U.S. inflation forecast for 2022, compiled by Consensus Economics, has proven a rise this 12 months from 2% to three.7%, barely above the inflation that serves as a mean goal for the Federal Reserve. The doubtless hikes of gasoline and meals costs because of warfare in Ukraine will doubtless raise these inflation expectations – no less than in response to simulations made by Moody’s (2022). Determine 16 shows U.S. inflation expectations going up.

Determine 16

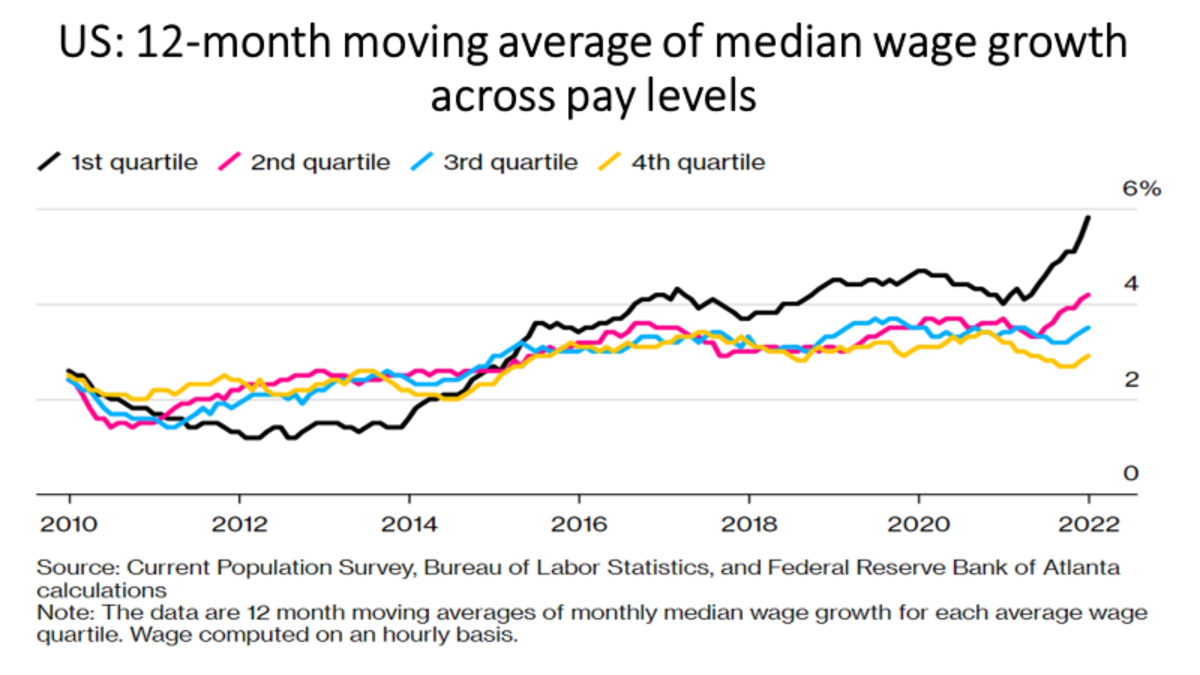

The opposite variable to be careful for is how costs and wages start to be readjusted based mostly on earlier inflation (Determine 17). The mix of unanchored inflationary expectations and a race between costs and wages would reveal the “transient” as turning into “everlasting”. In any other case, it is smart for the Federal Reserve and the European Central Financial institution to not speed up their financial tightening.

Determine 17

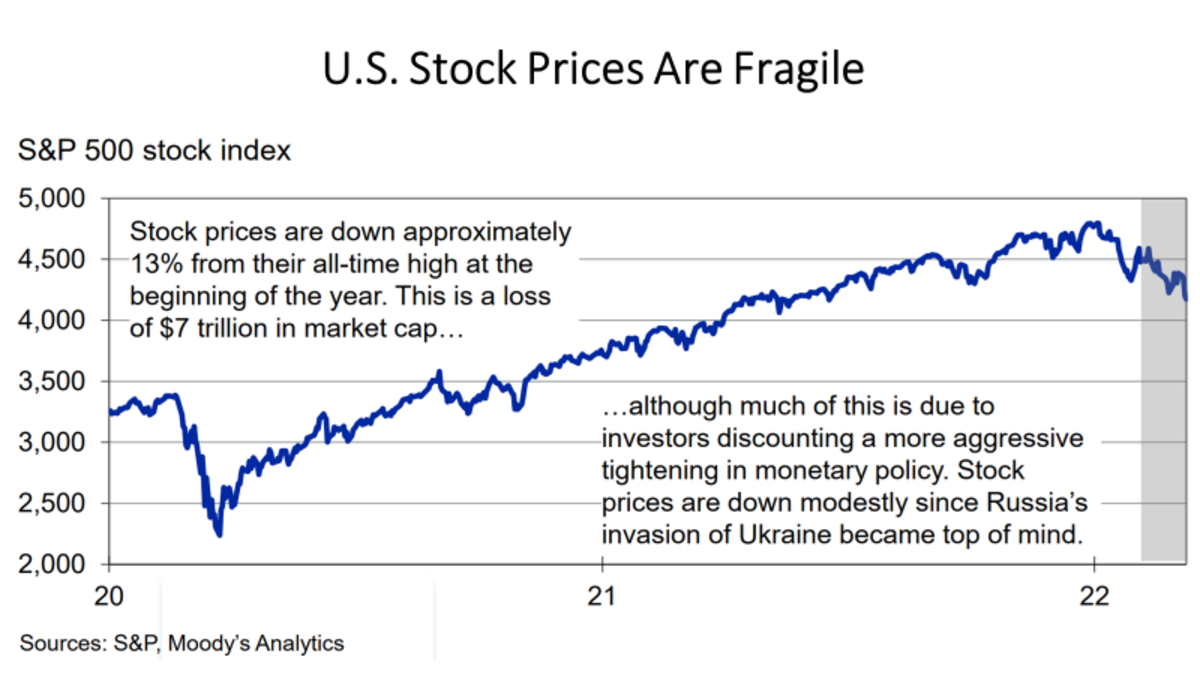

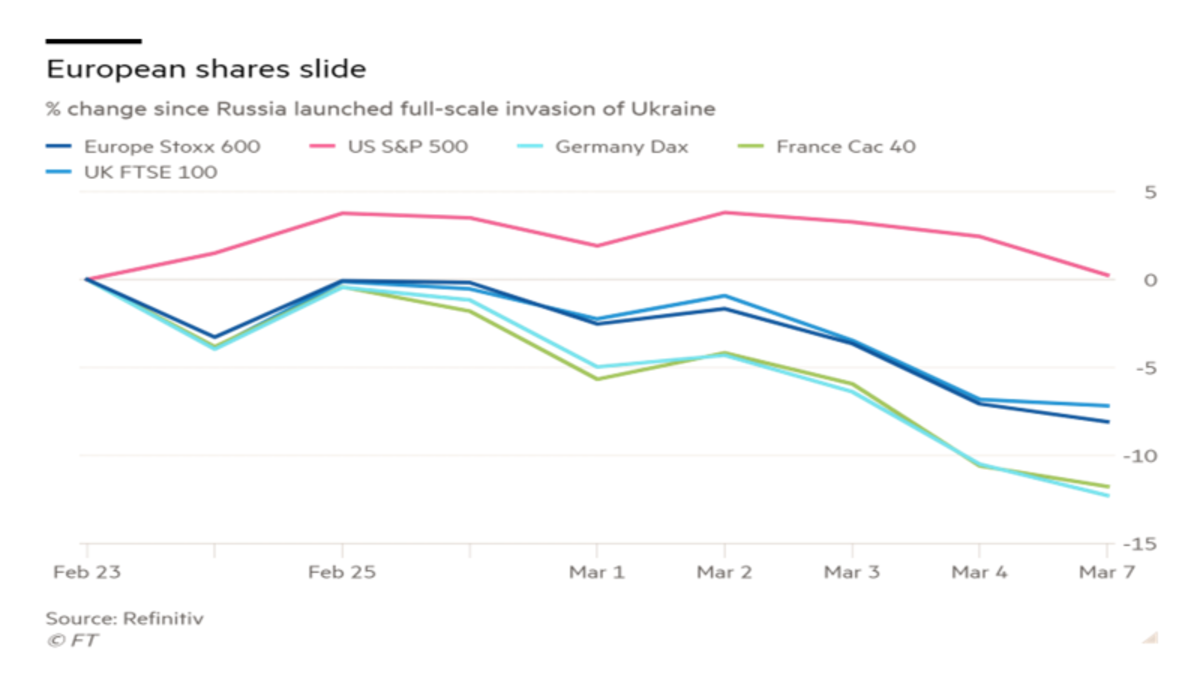

The open query is how over-leveraged monetary markets would obtain an abrupt or extreme change in monetary situations. Central banks might want to stability between curbing inflation and sustaining monetary stability. And the warfare in Ukraine has made such a rope thinner by downgrading financial progress and lifting inflation in Europe and the U.S. Shares on either side of the Atlantic have proven some sensitivity to such a situation (Figures 18 and 19).

Determine 18

Determine 19

Rising market and growing economies (EMDE)

Inflation has additionally risen in rising and growing economies, though normally not due to extra demand. Its fiscal and financial stimulus in response to the pandemic didn’t have the dimensions achieved in superior international locations, and the restoration of rising and growing economies in 2021 lagged nicely behind that of superior ones. Decrease capital inflows and, in some circumstances, sovereign debt ranking downgrades resulted in foreign money devaluation and home import worth shocks. Then again, they shared with the superior corporations the impacts of provide chain disruptions, and better costs of vitality and meals commodities. Largely of the group, the rise in home rates of interest already began final 12 months, as in Brazil.

It’s also price noting the slower tempo of restoration in rising and growing international locations and the rise within the distance between their per capita incomes and people of superior international locations as a part of the everlasting losses in GDP with the pandemic (Canuto, 2021b). In keeping with the World Financial institution (2022)’s “World Financial Outlook” report in January, in 2023 solely one in all its areas – Europe and Central Asia – is predicted to come back near the extent of GDP that was projected earlier than the pandemic. Latin America and the Caribbean, the Center East and North Africa, and Sub-Saharan Africa, will all be no less than 4% under what can be the corresponding degree. The drama is predicted to be much more vital in South Asia, with 8% much less.

Each the World Financial institution and the IMF spotlight vital disparities in vaccination charges between international locations as a significant factor in uneven recoveries. In addition they spotlight the extra profound and extra prolonged character of the scars left by the pandemic on the labor markets of non-advanced economies.

The commodity worth shocks, and provide chain disruptions introduced by the warfare in Ukraine will convey differentiated impacts on rising markets and growing economies. Even commodity exporters that may profit from greater costs should take note of their impression on poor home households and native inflation.

Jap and Western Europe might be hit by way of their export publicity to Russia. Rising commodity costs damage some EMs and profit others. They could be excellent news for many of Latin America, due to the corresponding good points of phrases of commerce of commodity exporters within the area. Then again, the already excessive inflation and the burden of family fuels and meals in poor individuals’s budgets will grow to be a significant concern. A serious differentiating issue might be whether or not the EMDE is an vitality exporter or importer.

The identical applies within the case of African economies (Ali et al, 2022). Meals importers within the area might be hit, whereas exporters of meals and vegetable and fish could have a chance to extend their share in each Russia and Europe because of sanctions and geopolitical dispute. Morocco’s exports of fertilizers could rise, whereas on the similar time the nation’s imports of dearer cereals and oil are inclined to impression negatively its financial system.

How about exterior finance? Given the small measurement of Russia’s financial system and its efforts to isolate itself from international monetary markets, as we approached, a broad contagion to rising markets isn’t anticipated. Nevertheless, rising markets that may dream of world relative portfolio reallocation of funds of their favor should recall that total threat aversion could run towards leverage and complete volumes of assets. Moreover, excessive ranges of private and non-private sector indebtedness enhance vulnerabilities and expose them to the danger of some vital tightening of world monetary situations (Canuto, 2022b) – a attainable situation as highlighted above.

Backside Line

The problem lies forward for central banks to seek out their balanced paths between tightening monetary situations and slowing progress to keep away from a subsequent recession. The time lag between financial coverage selections and their results is a complicating issue. Central banks should cross the river one stone at a time…

World monetary situations are nonetheless comparatively accommodative, whereas vulnerabilities stay excessive. It’s onerous to imagine that asset costs and the company monetary scenario will emerge unscathed from extra drastic changes within the face of the reorientation of financial insurance policies, notably because the shocks brought on by the warfare in Ukraine will make the coverage trade-offs between curbing inflation and avoiding monetary instability much more advanced. Further layers of complexity will are available in an extended horizon, as geopolitics could grow to be an element of reshaping worldwide fee techniques and provide and demand of commodities.

References

Ali, A.A.; Azaroual, F.; Bourhriba, O.; and Dadush, U. (2022). The Financial Implications of the Battle in Ukraine for Africa and Morocco, Coverage Middle for the New South, PB-11/22, February.

Benigno, G.; Giovanni, J.D.; Groen, J.; and Noble, A. (2022). World Provide Chain Stress Index: March 2022 Replace. Liberty Avenue Financial, Federal Reserve Financial institution of New York, March 3.

Brooks, R,; Ribakova, E.; Fortun, J.; and Hilgenstock, B. (2022). World Macro Views – Russia’s Invasion of Ukraine and EM, Institute of Worldwide Finance, March 10.

Brooks, R.; Fortun, J.; and Pingle, J. (2022). World Macro Views – The place is Rising Inflation Most Broad-Based mostly? Institute of Worldwide Finance – IIF, February 17.

Canuto, O. (2021a). Provide Chain Disruptions and Bottlenecks Dampen the World Financial Restoration, Coverage Middle for the New South, November 2.

Canuto, O. (2021b). Everlasting Output Losses from the Pandemic,

Canuto, O. (2022a). Financial Restoration and the Nice Reset, In Atlantic Currents: The Wider Atlantic in a Difficult Restoration, Coverage Middle for the New South, February.

Canuto, O. (2022b). Will rising economies face a tough touchdown? Coverage Middle for the New South, January 26.

Celasun, O.; Hansen, N-J. H.; Mineshima, A.; Spector, M.; Zhou, J. (2022). Provide Bottlenecks: The place, Why, How A lot, and What Subsequent? IMF Working Papers W.P./22/31, February 17.

Greene, R. (2022). How Sanctions on Russia Will Alter World Funds Flows, Carnegie Endowment for Worldwide Peace, March 4.

IMF (2022). G-20 Surveillance Observe, G‐20 Finance Ministers and Central Financial institution Governors’ Conferences, February 17-18.

ING (2022a). US Economic system Stays Resilient, However There Are Dangers Forward, March 3.

ING (2022b). Stagflation threat will increase within the eurozone, March 3.

Moody’s (2022). Geopolitical Threat Rattles Markets, March 4.

World Financial institution (2022). World Financial Prospects, January.

Yang, J.; Li, Z.; and Miao, H. (2021). Volatility spillovers in commodity futures markets: A community strategy, J Futures Markets, 41:1959–1987.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Middle for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]