[ad_1]

Yves right here. We warned again within the day that Brexit would impose a significant development price on the UK. The imposition of a tough border created commerce frictions and elevated prices of doing enterprise with the EU for importers and exporters, in addition to including to client costs. Monetary corporations moved some large ticket jobs to the continent as required by EU rules. The UK was additionally now not half of a giant financial bloc, and needed to lower its personal commerce offers, which had been extremely unlikely to be on as favorable phrases because the previous EU agreements. Places of work of EU analysis establishments had been closed. And these are simply examples. The checklist of losses is substantial.

The publish under estimates the full harm to the UK and likewise compares it to earlier estimates. The end result is even worse than usually anticipated as a result of prices being sturdy, versus losses that the UK might claw again over time.

By Nicholas Bloom, William Eberle Professor of Economics Stanford College; Philip Bunn, Senior Technical Advisor within the Structural Economics Division Financial institution Of England; Paul Mizen, Professor in Economics and Vice Dean, Analysis, at King’s Enterprise Faculty King’s School London; Pawel Smietanka, Analysis Economist Financial institution Of England; Senior Economist Deutsche Bundesbank; and Gregory Thwaites, Analysis Director Decision Basis; Affiliate Professor College Of Nottingham. Initially revealed at VoxEU

The UK is as soon as once more debating why its financial system has grown slowly for the reason that mid‑2010s. This column examines the impression of the choice to go away the European Union in 2016. Utilizing virtually a decade of information for the reason that referendum, the authors mix simulations primarily based on macro information with estimates derived from micro information. These estimates recommend that by 2025, Brexit had lowered UK GDP by 6% to eight%, with the impression accumulating steadily over time. Funding, employment, and productiveness had been all affected, reflecting a mixture of elevated uncertainty, lowered demand, diverted administration time, and elevated misallocation of sources.

The UK is as soon as once more debating why its financial system has grown slowly for the reason that mid‑2010s. Actual wages have barely risen, funding has been weak, and productiveness development has dissatisfied. Many components are at play – from the worldwide monetary disaster hangover to the Covid‑19 pandemic and the power value shock following Russia’s invasion of Ukraine – however one candidate has been central to the coverage debate for practically a decade: Brexit.

A big literature anticipated substantial lengthy‑run prices of leaving the EU Single Market and Customs Union (HM Treasury 2016, IMF 2016, Van Reenen et al 2016). Early ex‑publish work utilizing macro information additionally pointed to a sizeable hit to UK GDP and commerce (Born et al. 2019, Dhingra and Sampson 2022, Springford 2022, Haskel and Martin 2023, Freeman et al. 2025). VoxEU has been an essential discussion board for this analysis and debate. Our contribution is to revisit the query now that nearly a decade has handed for the reason that referendum, bringing collectively macro and micro proof in a single framework and evaluating precise outcomes to the career’s pre‑referendum forecasts.

In a brand new paper (Bloom et al. 2025), we mix micro information collected via the Choice Maker Panel (DMP), a survey of UK corporations, with publicly obtainable macro information to estimate the impression of Brexit. Our three predominant findings are:

- Brexit has had a big and chronic impact on the UK financial system. By 2025, we estimate that UK GDP per capita was 6–8% decrease than it might have been with out Brexit. Funding was 12–18% decrease, employment 3–4% decrease, and productiveness 3–4% decrease.

- These losses emerged steadily. The impression was exhausting to see in 2017–18, however accrued steadily over the next decade as uncertainty continued, commerce boundaries rose, and corporations diverted sources away from productive exercise.

- Economists had been roughly proper on the magnitude of the impression, however unsuitable on the timing. The consensus pre‑referendum forecast of a 4% lengthy‑run GDP loss turned out to be near the precise loss after 5 years, however too optimistic concerning the longer run.

Measuring Brexit’s impression: Macro Proof

Our first strategy compares the UK’s publish‑2016 efficiency with that of comparable superior economies. The concept, which has been extensively used on VoxEU to evaluate the implications of Brexit and different coverage shocks (e.g. Born et al. 2019), is to assemble an estimate of what the UK financial system may need appeared like within the absence of Brexit, primarily based on the expertise of different international locations after which ask how precise UK outcomes diverged from this counterfactual.

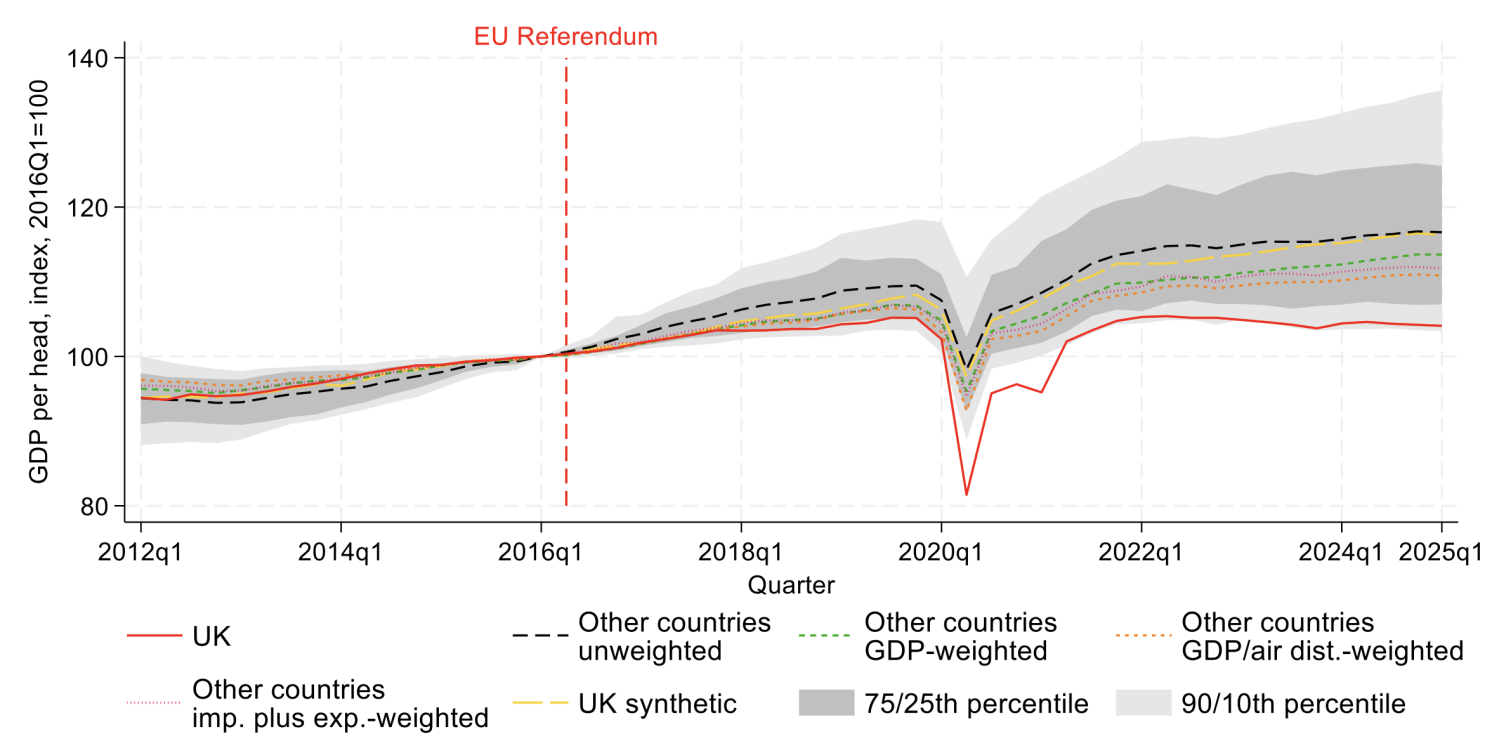

We use quarterly information for 33 superior economies (the EU27, the US, Canada, Japan, Iceland, Norway, and Switzerland) from 2006 to 2025, and study GDP per capita, enterprise funding, employment and labour productiveness. As a result of there is no such thing as a uniquely ‘right’ technique to weight the comparator international locations, we contemplate 5 totally different approaches: a easy unweighted common, a GDP‑weighted common, a gravity‑weighted common (GDP divided by distance), a commerce‑weighted common, and a proper artificial management. Our headline estimates take the easy common throughout these 5 strategies, which draw comparable conclusions regardless of the weighting scheme, together with when no weighting is used.

Determine 1 reveals that earlier than the referendum, UK GDP per capita grew at broadly the identical tempo as within the comparability group. After 2016, the strains diverge. By the yr to 2025 Q1, UK GDP per head had grown 6–10 share factors lower than in comparable economies, and solely about 4% in absolute phrases over the entire interval. Our central estimate – the common throughout the 5 weighting schemes – is that UK GDP per head has grown by a complete of round 8% lower than that of comparable superior economies since 2016.

We see comparable patterns for different aggregates:

- Enterprise funding was significantly exhausting hit. The UK went from being a comparatively robust performer pre‑referendum to a laggard afterwards. By 2025, enterprise funding was 12-18% under the extent implied by the comparator economies.

- Employment has additionally underperformed, however to a lesser extent: we estimate a shortfall of round 4% relative to the counterfactual.

- Labour productiveness was round 4% under the comparator group by 2025.

Determine 1 GDP per capita cross-country comparability

These macro comparisons are usually not with out caveats. The underlying assumption is that the UK would have carried out in addition to some common of different international locations within the absence of Brexit. However this may not be true. The Covid‑19 pandemic and the power shock affected international locations in another way; coverage responses, together with the UK’s furlough scheme and subsidy to family power payments, additionally assorted. Furthermore, Brexit virtually actually had some damaging spillovers on EU buying and selling companions, which might bias our estimates downwards. For these causes, we complement the macro evaluation with a micro‑econometric strategy primarily based on information from corporations positioned within the UK.

These macro comparisons are usually not with out caveats. The underlying assumption is that the UK would have carried out in addition to some common of different international locations within the absence of Brexit. However this may not be true. The Covid‑19 pandemic and the power shock affected international locations in another way; coverage responses, together with the UK’s furlough scheme and subsidy to family power payments, additionally assorted. Furthermore, Brexit virtually actually had some damaging spillovers on EU buying and selling companions, which might bias our estimates downwards. For these causes, we complement the macro evaluation with a micro‑econometric strategy primarily based on information from corporations positioned within the UK.

Micro Proof

The end result of the Brexit vote in 2016 was extensively thought to be a shock. This discrete, largely unanticipated occasion permits us to undertake a distinction‑in‑variations technique utilizing agency‑degree information.

Our micro evaluation exploits the truth that Brexit’s impression assorted systematically with corporations’ pre‑referendum publicity to the EU. Utilizing the Choice Maker Panel – a big month-to-month survey of UK corporations – we assemble a broad measure of prior EU publicity that averages six dimensions: export share to the EU, import share from the EU, dependence on EU migrant employees, publicity to EU regulation, share of administrators who’re EU nationals, and EU possession. These survey measures are matched to firm accounts information.

Companies with increased EU publicity grew quicker than others earlier than 2016. After the referendum, this sample reversed. Conditional on agency and time mounted results and controlling for Covid‑associated shocks, our micro-based outcomes suggest the next mixture impacts:

- Decrease funding development cumulating to a 12% shortfall within the degree of enterprise funding by 2023/24.

- Decrease employment development round 0.5 share factors decrease per yr, implying a 3–4% decrease degree of employment by 2023/24.

- Complete issue productiveness (TFP) development round 0.5 share factors decrease per yr, resulting in a 3–4% discount to inside‑agency TFP by 2023/24.

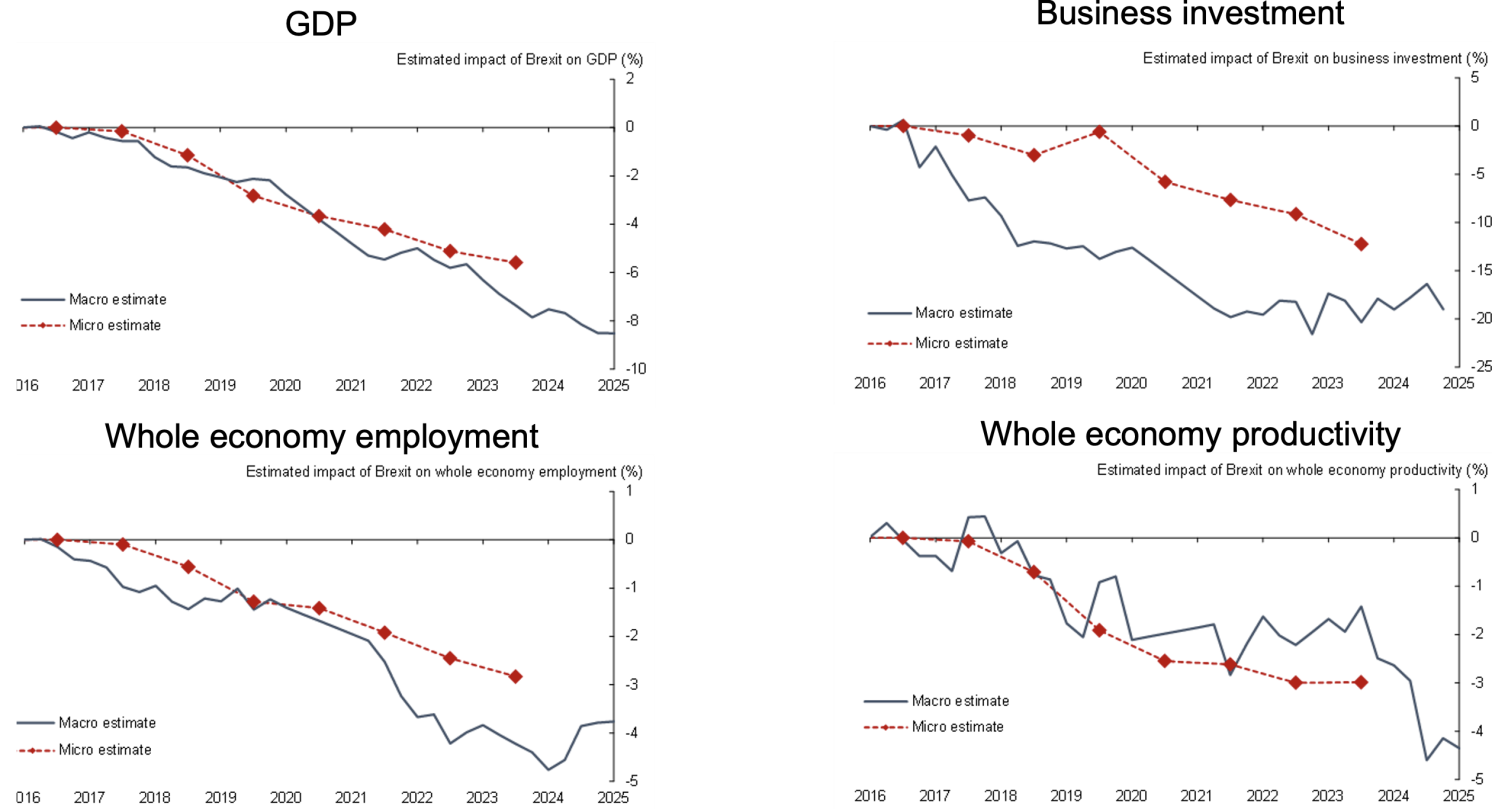

The micro strategy has a special set of issues to the macro strategy. The extra direct hyperlink to EU publicity may also help to higher establish the causal results of Brexit. However now we have to imagine that unexposed corporations weren’t affected by Brexit, when the truth is they may have confronted damaging spillovers (for instance, via demand or provide chains) or optimistic spillovers (for instance, via the labour market if unexposed corporations discovered it simpler to rent employees). Broadly talking, the macro- and micro‑primarily based estimates of the impression on GDP, funding, employment and productiveness line up moderately effectively, with the macro estimates usually being the bigger of the 2 (Determine 2).

Determine 2 The estimated impression of Brexit

Why Did the Harm Take So Lengthy To Present Up?

Our evaluation suggests 4 predominant channels via which Brexit affected the UK financial system, all of which operated steadily:

- Persistent uncertainty. Brexit generated an unusually lengthy‑lasting interval of coverage uncertainty. Our Brexit Uncertainty Index, primarily based on the DMP, measures the share of corporations reporting Brexit as one in every of their high three sources of uncertainty. This index rose sharply after the referendum and remained elevated till effectively after the Commerce and Cooperation Settlement (TCA) took impact in 2021. Funding is especially delicate to uncertainty, and our agency‑degree regressions recommend that the uncertainty channel explains a lot of the publish‑2016 weak spot of funding.

- Increased commerce prices and decrease demand. Despite the fact that the TCA preserves zero tariffs and quotas on most UK‑EU commerce, leaving the Single Market and Customs Union has launched substantial non‑tariff boundaries. Different work has documented sharp falls in UK–EU items commerce round 2021 and chronic disruptions to provide chains and providers commerce (Dhingra and Sampson 2022, Freeman et al. 2025). Decrease anticipated demand, particularly in tradable sectors, seems to have been to be a key driver of weaker employment development.

- Much less innovation and administration time being diverted. Productiveness inside corporations could have been affected by corporations slicing again on productivity-enhancing types of funding, and by administration time being diverted from different actions to arrange for Brexit.

- Reallocation away from extremely productive, internationally uncovered corporations. The corporations most uncovered to the EU have a tendency additionally to be the most efficient, and these had been the corporations that had been most negatively impacted by Brexit.

Taken collectively, these channels assist clarify why the financial impression of Brexit has been a sluggish‑burn phenomenon. Fairly than a single cliff‑edge occasion, the UK skilled a drawn‑out strategy of negotiation, transition, and implementation, with uncertainty and adjustment prices stretching over virtually a decade.

How Did the Pre‑Referendum Forecasts Carry out?

The Brexit referendum affords a uncommon alternative in macroeconomics to match ex‑ante forecasts with ex‑publish outcomes. IMF (2016) summarised the predictions of educational {and professional} economists concerning the lengthy‑run impression of Brexit on UK GDP. The typical forecast in that survey was a 4% lack of GDP relative to remaining within the EU, with a lot of the impression assumed to materialise inside 5 years.

Our estimates recommend that this consensus forecast carried out moderately effectively over a 5‑yr horizon: we discover a GDP shortfall of 4–6% by 2021. However by 2025 the loss had deepened to six–8%. In different phrases, economists had been broadly proper on the course and order of magnitude of the lengthy‑run impression, however they underestimated how drawn‑out the Brexit course of can be and subsequently how persistent the related uncertainty and adjustment prices would show.

This has broader implications for the way we consider macro forecasts round main political occasions. The Brexit expertise means that getting the economics ‘proper’ isn’t sufficient; the political financial system of implementation – together with the potential for delays, renegotiations and partial reversals – can materially have an effect on each the timing and the eventual measurement of the financial impression.

Classes for Future Commerce Fragmentation

The UK’s exit from the EU is a novel occasion. No different giant financial system has voluntarily stepped again from such deep integration with its neighbours. However the mechanisms we doc are prone to be related for different episodes of commerce and migration fragmentation, together with the imposition of tariffs, sanctions and tighter migration controls elsewhere.

Our work reveals that disengaging from world commerce and manufacturing networks can carry giant and lengthy‑lasting financial prices, and these prices are inclined to accumulate slowly relatively than showing in a single day. Within the case of Brexit, there was a considerable financial impression on the UK financial system.

See unique publish for references

[ad_2]