[ad_1]

Perhaps, perhaps not. The NYT headline blares “Tariffs Shrank Commerce Deficit in September, New Knowledge Present”. Imports did lower from earlier, however that’s after an incredible surge. The precise article is a extra nuanced (i.e., that’s a awful title).

Brad Setser, a commerce professional on the Council on International Relations, mentioned the info confirmed “unambiguous weak point” in U.S. imports in September. “The query is the way you wish to interpret that,” he added. “Is that this payback from the entrance operating? Or are tariffs beginning to have an effect?”

Mr. Setser mentioned that it was too early to reply that query, however that international commerce information urged that U.S. imports may rise once more within the subsequent few months, fueled partly by the acquisition of international computer systems and chips to construct information facilities.

I’m going to go together with the “payback” thesis, mixed with slowing financial exercise. First think about the info; it’s not your typical time collection import collection.

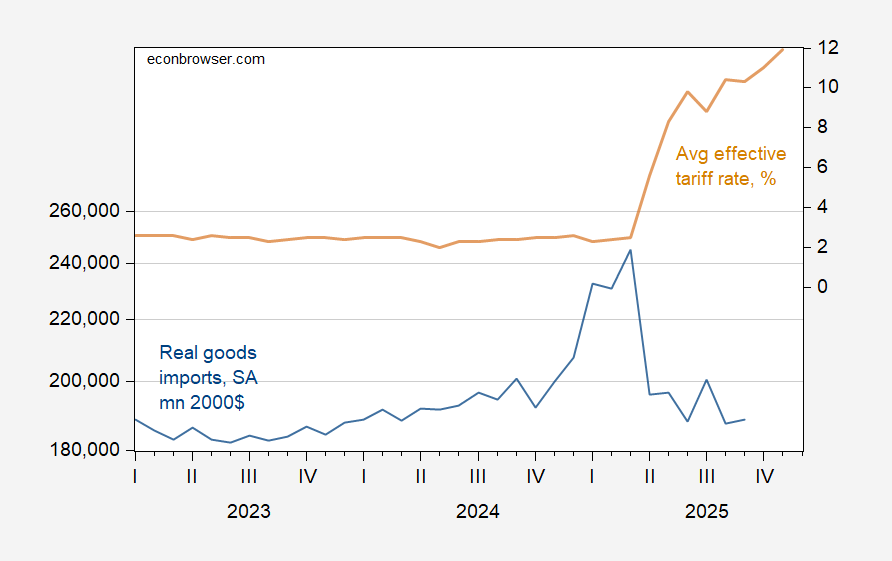

Determine 1: Actual imports of products, seasonally adjusted, in mn.2000$, BoP commonplace (blue, left log scale), and common efficient tariff price, % (tan, proper scale). Supply: Census, BLS through FRED, Paweł Skrzypczyński, and creator’s calculations.

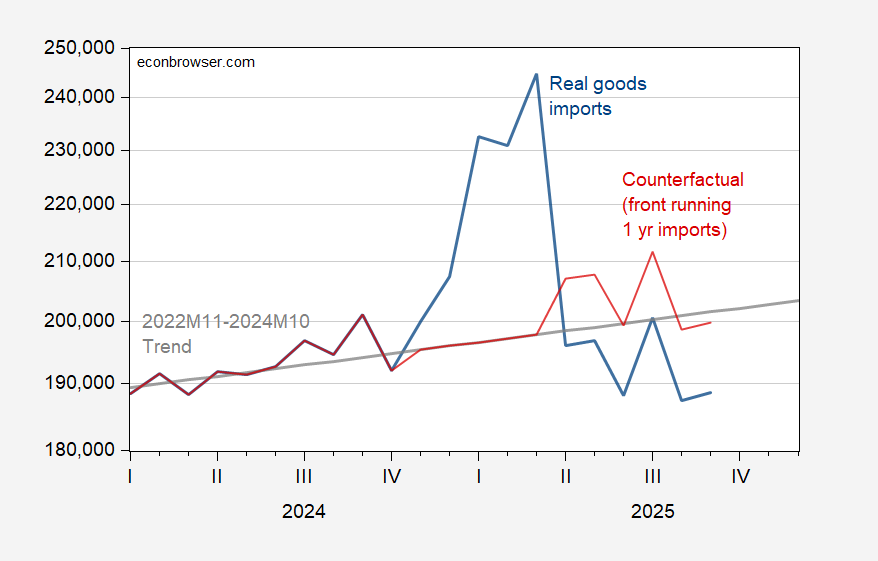

Imports surged as importers tried to front-run the tariffs, and construct up stock. There’s an apparent surge going from November to March. How massive? Quantitatively, fairly massive; utilizing a deterministic pattern estimated over 2022M11-2024M10, I discover the “extra imports” had been about 133bn 2000$. Assuming front-running was to account for a yr’s price of imports, then I generate a counterfactual collection.

Determine 2: Actual imports of products, seasonally adjusted, (blue, log scale), 2022M11-2024M10 deterministic pattern (tan), and counterfactual assuming one yr’s price of imports front-run (pink), all in mn.2000$, BoP foundation. Supply: Census, BLS through FRED, and creator’s calculations.

Seen by means of this lens, imports haven’t decreased relative to what we’d have in any other case seen. In fact, one yr’s price of import front-running is bigoted; six months would indicate imports are literally operating greater than current.

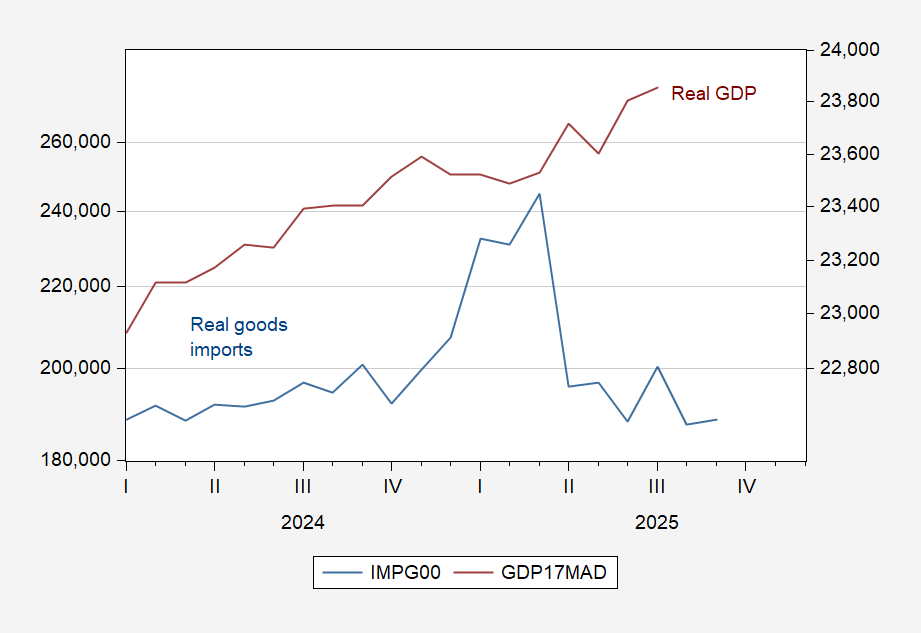

Imports depend upon the actual change price and revenue in addition to tariff charges. Whereas the actual worth of the greenback has been fairly fixed over the three months earlier than September, revenue has apparently slowed, relative to pre-Trump. Since imports are extremely revenue delicate (I estimate 2.2 at quarterly frequency), it could not be stunning to see imports fall due to lowered financial exercise, slightly than expenditure switching arising from tariffs.

Determine 3: Actual imports of products, seasonally adjusted, mn.2000$ (blue, log scale), GDP in bn.Ch.2017$ SAAR (brown, proper log scale). Supply: Census, BLS through FRED, SPGMI 9/2 launch, and creator’s calculations.

[ad_2]