[ad_1]

Right here’re key indicators adopted by the NBER’s Enterprise Cycle Relationship Committee, with indications of measures already missed (purple squares) and will likely be missed in a 34 day shutdown (and sure delayed even when a shorter shutdown happens) (purple dashed squares).

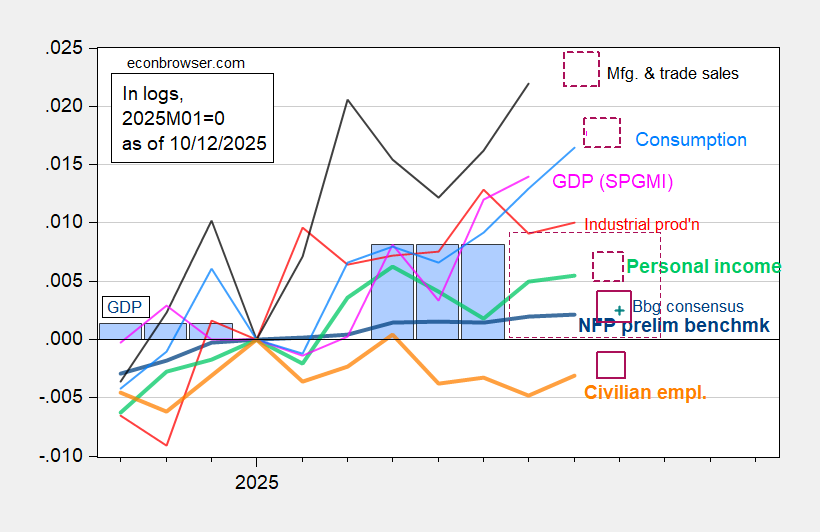

Determine 1: Implied NFP preliminary benchmark revision (daring blue), civilian employment with smoothed inhabitants controls (daring orange), industrial manufacturing (pink), Bloomberg consensus employment for implied preliminary benchmark, (blue +), private earnings excluding present transfers in Ch.2017$ (daring mild inexperienced), manufacturing and commerce gross sales in Ch.2017$ (black), consumption in Ch.2017$ (mild blue), and month-to-month GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M01=0. Purple squares denote releases already missed. Purple dashed squares point out releases that will likely be missed and/or delayed with a 31 day shutdown. Supply: BLS through FRED, Federal Reserve, BEA 2025Q3 third launch, S&P International Market Insights (nee Macroeconomic Advisers, IHS Markit) (9/2/2025 launch), and writer’s calculations.

Of those, employment and private earnings are essentially the most closely weighted — and we’ve already missed the employment numbers (of which NFP was by estimates rising meagerly, and civilian employment was as of August beneath prior peak). No advance GDP launch on the thirtieth appears prone to me, as nicely.

[ad_2]