")

[ad_1]

Richard Drury/DigitalVision through Getty Photographs

It’s In all probability a Bubble, However There Is Lots Else to Make investments In

Govt Abstract

AI seems like a basic funding bubble to us, with very excessive valuations and indicators of rampant hypothesis. However we acknowledge that whereas many buyers harbor fears that AI could be a bubble, they’re removed from positive of that truth and have a tendency to imagine the market is appropriately priced as a reasonably robust prior. In lots of bubbles, such a state of affairs would make constructing a powerful portfolio near unimaginable because the portfolio you’d maintain should you consider within the bubble is a portfolio that will be loopy to carry if occasions have been regular. The 2007-8 Every part Bubble and the 2021 Length Bubble, as an example, have been each bubbles wherein the precise portfolio to personal should you believed there was a bubble was a portfolio that will have an unacceptably low anticipated return if markets have been pretty priced. However the 2025 AI Bubble seems little like both of these two and rather more just like the 2000 Web Bubble, wherein a bubble-agnostic investor may have owned a portfolio with an inexpensive threat/reward trade-off in both a bubble or a business-as-usual state of affairs. In the present day, non-U.S. equities, deep worth shares, and liquid alternate options provide returns that look affordable or higher, no matter whether or not AI is in a bubble. Tilting a portfolio away from AI names and towards these property might save buyers a whole lot of ache if it seems we’re in a bubble with out meaningfully lowering anticipated returns if monetary markets are one way or the other nonetheless pretty priced in the present day.

“It’s troublesome to get a person to know one thing, when his wage relies upon upon his not understanding it.”

—Upton Sinclair

Introduction

I feel most individuals can admit that there could be a bubble in AI and associated shares in the present day. I gained’t spend a whole lot of time discussing the proof, however there may be loads to level to. The S&P 500 is buying and selling at valuation ranges solely seen throughout the Web Bubble, and on some measures, is much more costly now than it was then.1 Amongst different indicators of rampant hypothesis, frantic enterprise capitalists are throwing cash at AI startups at multi-billion-dollar valuations with out even being informed their plans.2 Fairness buyers are bidding up the worth of large firms by lots of of billions of {dollars} resulting from funding offers with OpenAI, an organization whose revenues must rise a hundredfold to make good on its guarantees.3 Traders are so determined to get in early on the subsequent large factor that they’ve bid up the costs of quantum computing shares 1200% or extra over the previous yr, and at valuations that make Palantir seem like a price inventory.4 It actually seems like a bubble to us, though I don’t consider I’ll persuade any true believers within the AI model of “this time it truly is completely different” of that truth.5 This letter isn’t written for the true believer, nevertheless. It’s written as a substitute for the “agnostic investor.” Such an investor is one who acknowledges that there’s loads of proof indicating we’re in a bubble, but in addition harbors a perception that, regardless of that proof, an honest beginning assumption is that each one property are priced to ship a traditional return always. Bubbles are normally an issue for the agnostic investor, however some bubbles are extra of an issue than others. The excellent news about in the present day’s bubble is that it is one that enables an agnostic investor to construct a portfolio that may strongly outperform if there’s a bubble that in the end bursts, and can even do exactly effective if all property ship regular returns.

A Taxonomy of Bubbles

One good factor about Twenty first-century monetary markets is that they’ve generated an fascinating number of bubbles nicely throughout the reminiscence of most buyers. Once we made our case for the Web Bubble within the late Nineties, our choices have been restricted to the U.S. in 1929, the British Railway growth of the 1860s, and the Tulip Mania of the 1630s.6 Exterior of Nineteen Eighties Japan, which had already been shrugged off as irrelevant to any “regular” nation, the overwhelming majority of buyers hadn’t seen a significant funding bubble of their lifetimes.7 However the final 25 years have given us three main bubbles within the developed world: the 2000 Web Bubble, the 2007-8 Every part Bubble, and the 2021 Length Bubble. Every of those bubbles diversified considerably when it comes to the property concerned and required buyers to reply fairly otherwise to guard their portfolios. Of all of them, the present occasion seems most just like the Web Bubble of 2000, which must be a reduction to the agnostic investor. Whereas dynamic, valuation-driven asset allocation saved many buyers appreciable ache in all three bubbles, solely within the 2000 occasion was it doable to spare your self massive losses with out having to personal a portfolio that will have been loopy to carry in any regular state of affairs.

The Web Bubble of 2000

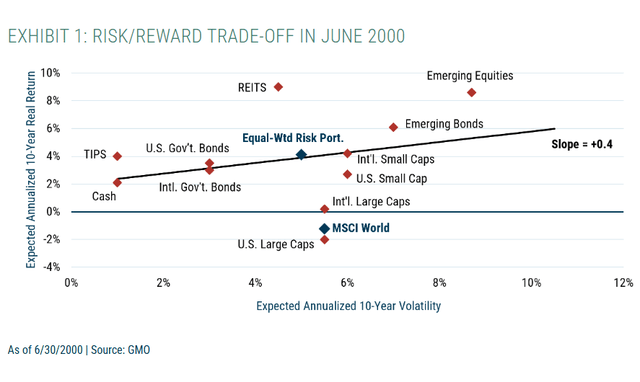

The story of the Web Bubble is acquainted sufficient to most to not require a whole lot of retelling. The real breakthroughs in communications and computing that embodied the web and (comparatively) trendy cellular phone networks of the time sparked an funding frenzy the place buyers overestimated the speed of progress in communications visitors in addition to the returns on funding for firms collaborating within the growth. Traders additionally did a poor and indiscriminate job of selecting the eventual winners within the new economic system that was being created. The S&P 500 rose to never-before-seen valuation ranges, led by expertise and telecommunications corporations buying and selling at unsustainably excessive valuations, typically with unsustainable enterprise fashions as nicely. Vendor financing by suppliers and round offers amongst web corporations created the phantasm of larger exercise and end-user demand than there truly was, and the S&P 500 in the end fell by 45% in actual phrases from the summer season of 2000 to the spring of 2003, whereas the tech-heavy Nasdaq Composite fell by 79%. It was a large bubble that led to main ache for a lot of buyers, however that ache was largely avoidable, even for these with out heroic prescience. To see why, it’s useful to have a look at the peak of the bubble by a valuation lens. Exhibit 1 reveals a threat/reward scatterplot from June 2000 utilizing the asset class forecasts we had revealed on the time.8

With U.S. massive cap shares buying and selling at their highest valuations ever, their anticipated return was considerably unfavourable in actual phrases. However for an investor ready to look elsewhere, there was loads to do. A number of different threat property have been buying and selling cheaply relative to historical past and provided better-than-normal anticipated returns. Regardless of the bubble, buyers have been truly getting paid properly for taking threat total. Drawing a threat/reward regression line by the forecasts illustrates this: the road’s slope of +0.4 isn’t far off an equilibrium slope of +0.6. The profit to diversifying past a cap-weighted portfolio was large; an equal-weighted portfolio of the danger property we forecasted had an anticipated return of +4.1% actual, far larger than the MSCI World’s -1.2%.

It’s price noting that these forecasts weren’t pushed by any assumption in regards to the timing of the bubble bursting—they merely assumed asset costs would easily revert to truthful worth over 10 years. You didn’t have to consider you knew when the bubble would burst to know that you just have been higher off proudly owning different property. And also you didn’t want to cut back your total holdings of equities or threat property on the whole. With TIPS providing 4% actual yields, shifting cash into lower-risk property actually wasn’t a loopy thought, and we did have higher-than-normal exposures to bonds in our portfolios, however it was truly fairly simple to construct a diversified portfolio of threat property buying and selling at very enticing costs. It solely required a willingness to just accept a good bit of monitoring error relative to a conventional cap-weighted fairness portfolio. If our agnostic investor believed there was a 50% likelihood that each one property have been pretty priced and a 50% likelihood that valuations would ultimately mean-revert (as our forecasts assumed), the reply was fairly apparent. A portfolio of worldwide small caps, REITs, rising fairness, and rising debt, alongside developed market authorities bonds, was the one to personal.9 If every part had turned out to be priced pretty, the portfolio’s threat and return expectations would have been similar to these of a “regular” balanced portfolio. However not like the conventional portfolio, this portfolio would nonetheless have a powerful anticipated return if the suspected bubble turned out to be actual.

At GMO, we had no doubts in our minds that the 2000 bubble was certainly a bubble. We moved our asset allocation portfolios aggressively away from U.S. massive caps and towards the cheaper property accordingly, throughout the bounds our purchasers allowed. (See Appendix for our portfolio holdings at every bubble’s peak.) Our World Asset Allocation Technique10 was subsequently in a position to outperform the 65% World Equities/35% U.S. Combination Bond11 benchmark by over 10% per yr from 2000 to 2003, earning money in actual phrases throughout the S&P 500’s bear market, whereas the 65/35 benchmark fell by over 27% after inflation. By the point the normal 65/35 portfolio regained its 2000 peak in actual phrases on the finish of 2005, our technique was up greater than 50%, an annualized web return of seven.3% actual.

The Every part Bubble of 2007-8

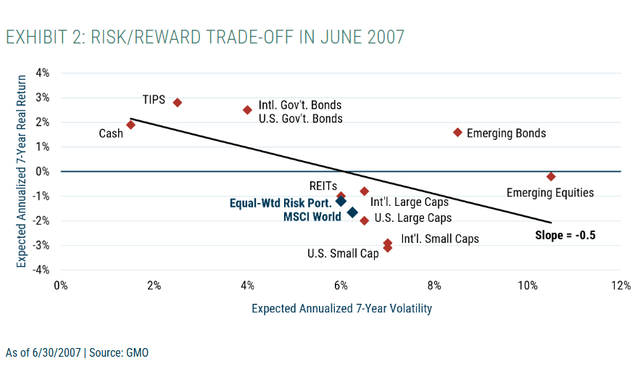

However markets weren’t totally again to regular in 2005. In truth, a world housing bubble was already nearing its peak, and the free financial coverage that enabled hypothesis in actual property had inspired buyers to bid up threat property of every kind. By 2007, this had was what Jeremy Grantham dubbed the “Every part Bubble,” the place threat property of every kind had grow to be overpriced concurrently.12 This supplied a really completely different problem for buyers, as proven in Exhibit 2, a threat/reward scatterplot of our asset class forecasts as of June 2007.

Whereas U.S. massive cap shares have been once more considerably overvalued by this level, they weren’t the worst offenders, with small cap shares around the globe considerably extra overvalued. However at a excessive stage, there have been two extraordinarily putting variations between this bubble and the 2000 Web Bubble. First, the slope of the danger/reward line, which had been a constructive +0.4 in 2000, had by this level grow to be a surprisingly unfavourable -0.5. For the primary time ever, buyers seemed to be paying for the privilege of taking threat. Understanding this didn’t require deciphering how overleveraged the monetary system had grow to be, nor the power to divine the timing of the forthcoming World Monetary Disaster (GFC). Our forecasts merely assumed that asset lessons would take seven years to revert to truthful worth. And even when reversion had taken that lengthy to happen, each single dangerous asset13 had a decrease anticipated return than each single low-risk asset.14 In contrast to in 2000, this time it didn’t a lot matter whether or not you owned a cap-weighted or equal-weighted model of the danger property, because the anticipated return of the equal-weighted portfolio of threat property was virtually as unhealthy because the MSCI World.

This example put the agnostic investor in a really troublesome place. The rational portfolio to personal should you believed what valuations have been telling you was drastically completely different from the portfolio you’ll personal if every part was priced pretty. Diversifying inside dangerous property couldn’t assist in any significant approach. You needed to de-risk the portfolio, and de-risking is a particularly dangerous factor for an agnostic investor to do. If valuation is supplying you with the unsuitable sign and property are pretty priced, de-risking places you in a a lot decrease anticipated return portfolio—one that would not probably ship the extent of actual returns buyers rely on in the long run. Since most finish purchasers and funding committees have been, at greatest, within the agnostic camp, this left their advisors and CIOs—even when they believed wholeheartedly within the existence of a bubble—in a really powerful spot. Whereas they didn’t have to consider the bust was imminent for de-risking to be the precise name, they didn’t have a lot time to be confirmed proper earlier than getting fired, or no less than earlier than being compelled to purchase again into threat property. Traders can get antsy rapidly once they suspect they’re lacking out on rising markets.

We selected to observe the valuations and aggressively de-risked our portfolios. Within the GMO Benchmark-Free Allocation Technique (the place we had probably the most flexibility), we diminished our fairness publicity to 25% by the summer season of 2008. We invested all 25% in GMO’s High quality Technique, pushed by our perception that high-quality firms can be the most probably survivors ought to a downturn flip right into a despair. The precise GFC downturn was even sharper than that of the 2000 occasion, with a 60% MSCI ACWI/40% Bloomberg U.S. Combination bond portfolio falling 37% in actual phrases from the autumn of 2007 to the winter of 2009. In Benchmark-Free, we minimize that drawdown to twenty% and reached a brand new excessive in actual phrases by the tip of 2009, whereas the 60/40 portfolio took till 2013 to surpass its 2007 peak in actual phrases.

The 2021 Length Bubble15

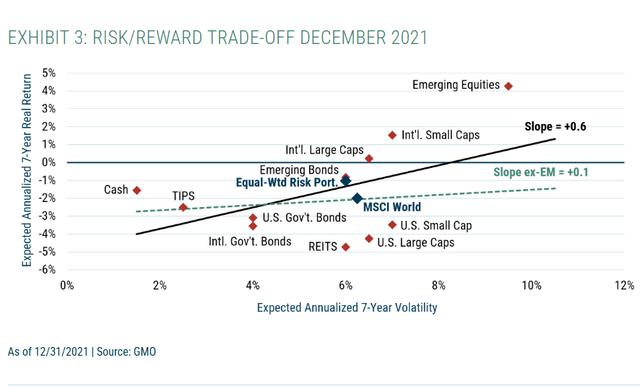

The subsequent bubble to type was arguably even trickier for our agnostic investor to deal with. By the tip of 2021, the inflation that had been largely quiescent since 2008 had come again with a vengeance, rising 6.8% within the yr to November. And but markets didn’t appear to care. T-Payments nonetheless yielded zero, whereas the 10-year notice provided a meager 1.5%. This was not as a result of buyers assumed that shopper costs would rapidly fall again to regular ranges. On the time, 10-year TIPS yielded -1.04%, promising vital losses in actual phrases for anybody who lent cash to the U.S. authorities for a decade. The issue was not restricted to authorities bonds. The S&P 500 hit its highest ever cyclically adjusted P/E outdoors of some months across the peak of the 2000 Web Bubble, and virtually all different property around the globe had joined within the enjoyable, as proven in Exhibit 3.

On this bubble, the difficulty was not notably that buyers weren’t getting paid to take threat. The slope of the danger/reward regression line was regular at +0.6, though that was largely resulting from rising equities, which weren’t notably overpriced on the time. Excluding rising equities from the regression ends in a slope of +0.1, which is actually uninspiring, however nonetheless not the catastrophe of the 2007-8 Every part Bubble. The difficulty this time was the truth that virtually all anticipated returns have been unfavourable in actual phrases.16 Once more, diversification inside threat property didn’t assist a lot, as an equal-weighted portfolio of threat property had a really comparable anticipated return as MSCI World. De-risking, as an investor may need accomplished in 2007, by shifting from shares to authorities bonds, additionally didn’t assist since authorities bonds have been no much less overvalued than shares. This bubble spanned throughout every kind of long-duration property. Equities and actual property, which have much more period than a typical bond, have been caught up alongside mounted earnings.17

This posed an virtually unimaginable drawback for our agnostic investor–one which neither de-risking into bonds nor diversification throughout threat property may repair.18 Given these forecasts, money had a greater anticipated return than bonds or shares, however money yielded actually zero. If there was any significant risk that, regardless of the valuations, property have been one way or the other nonetheless “usually” priced, the one asset that you just needed to personal should you believed there was a bubble—money—was an asset that assured losses after inflation, whether or not there was a bubble or not! The attraction of shifting to short-term investments if there was an opportunity that the bubble would possibly burst sooner slightly than later was apparent, as in that case, returns on bonds and shares can be much more unfavourable. And given how excessive inflation was on the time, there was a reasonably clear catalyst for the bubble to burst within the comparatively close to time period. Even with this clue, this occasion was virtually actually the hardest name of our agnostic investor’s profession thus far.

It was a neater name for us, though that’s partly as a result of we had a option to cheat. By the tip of 2021, we had moved 60% of our Benchmark-Free portfolio to liquid alternate options—methods like fairness lengthy/brief, merger arbitrage, and international macro. Although liquid alternate options methods do take threat, they achieve this in a a lot shorter-duration approach than conventional property. Liquid alternate options search to generate returns on prime of money, slightly than on prime of bond or inventory benchmarks. This was extremely useful in 2021, given money had not solely the next anticipated return than many different property, but in addition a lot much less threat within the occasion valuation reversion occurred sooner slightly than later. Inflation didn’t rapidly recede in 2022, so reversion was certainly fast. A 60% MSCI ACWI/40% Bloomberg U.S. Combination Bond portfolio misplaced 26% in actual phrases between December 2021 and September 2022. In Benchmark-Free, we have been in a position to minimize that principally in half, to a 14% actual loss.19 Consequently, whereas that 60/40 portfolio didn’t regain its December 2021 stage till the summer season of this yr, we have been in a position to recapture the losses in 2023, and as of this writing, we’re 14% forward of the 60/40 portfolio because the 2021 Length Bubble peak.20

The AI Bubble

The autumn of 2022 was notable, and never merely as a result of it marked the low of the drawdown from the 2021 Length Bubble. It additionally marked the discharge of ChatGPT-3.5, which sparked the start of the AI growth. There may be little query that it was a real technological breakthrough, though AI already had some spectacular accomplishments earlier than that, notably mastering the computationally intractable sport of Go in 2016 and fixing protein folding in 2020. Just like the web within the late Nineties, AI since 2022 has captured the creativeness of buyers around the globe, though on this case, the bulls are making even grander claims—promising superintelligent computer systems and humanoid robots poised to render human work pointless inside a handful of years.21

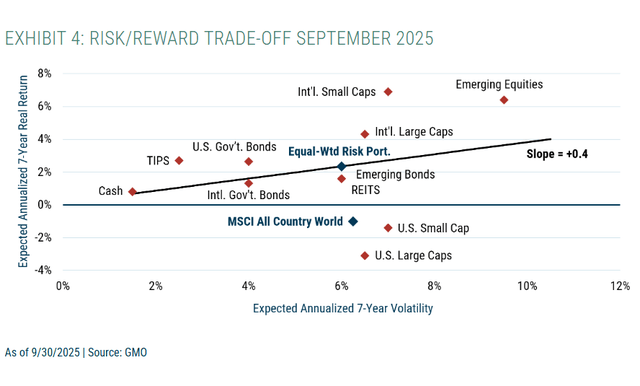

AI-related shares have accomplished exceptionally nicely because the launch of that first chatbot, whether or not pushed by huge earnings progress (Nvidia) or unrelenting hopes that they’ll one way or the other profit ultimately regardless of their quickly diminishing money move (Tesla). These AI shares have helped drive the S&P 500 above its 2021 valuation peak, which is now about 10% beneath the 2000 peak on cyclically adjusted earnings. Exhibit 4 reveals the danger/reward scatterplot based mostly on our September 2025 forecasts.22

Discover this chart is strikingly just like the 2000 model. The slope of the danger/reward regression line is once more +0.4, U.S. massive cap shares are once more probably the most overvalued asset round, and the equal-weighted portfolio of threat property once more affords a a lot larger anticipated return than MSCI World. Our agnostic investor can construct a portfolio that deserves to win handily if the bubble is a bubble and also needs to do exactly effective if all is regular. I don’t imply to say that selecting to personal a portfolio with little or no U.S. equities in it’s simple to do given U.S. equities have crushed the remainder of the world by as a lot as they’ve during the last 15 years, however retaining a traditional amount of cash in equities is a luxurious the final two bubbles didn’t permit for. In the present day, constructing a diversified portfolio of threat property which are priced to ship equity-like-or-better returns is simple. Whereas on this portfolio U.S. equities are most notable for his or her absence, there are nonetheless loads of property to select from.

Conclusion

For the agnostic investor who’s nervous that AI could be a bubble however isn’t totally satisfied, the excellent news is that in the present day, certainty isn’t required to maneuver to a portfolio that’s much less depending on the AI commerce. Loads of different threat property are buying and selling at truthful and even compelling valuations, and even when in the present day’s monetary markets turn into rationally priced, there is no such thing as a long-run anticipated return give-up for tilting your portfolio away from the AI darlings and into these different property. Worth shares all over the place are very low-cost, and within the U.S. and EAFE markets, deep worth shares are buying and selling at a number of the widest reductions on document. Non-U.S. small worth shares are additionally enticing, notably in Japan, the place they profit from each a really undervalued yen and the opening of the marketplace for company management. Liquid alternate options profit from first rate yields on money and vast valuation spreads throughout numerous asset lessons, and authorities bonds are priced to supply capital positive aspects in a recession and an honest yield if the worldwide economic system holds collectively.

It’s at all times doable that if markets on the whole proceed to maneuver larger, our present 2000-like alternative set would possibly flip right into a 2007- or perhaps a 2021-like dilemma for buyers. However to get there, we’d have to see good returns from a big selection of property, not simply continued levitation in AI. Whereas agnostic buyers would face tougher decisions if the rally continues, they might additionally take solace within the robust returns of the well-diversified portfolios that obtained them to that time. As bubbles go, AI seems like one of many simple ones for an agnostic investor to deal with.

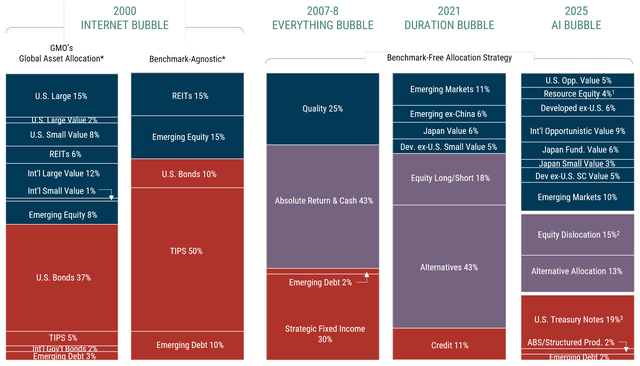

Appendix

GMO Asset Allocation Portfolios at Bubble Peaks

Exhibit 5 reveals the positioning of GMO’s Asset Allocation portfolios throughout every bubble, in addition to the present allocation for the GMO Benchmark-Free Allocation Technique.

Supply: GMO

*GMO’s World Asset Allocation Technique has a 65% MSCI ACWI/35% Bloomberg U.S. Combination benchmark. Benchmark-Free Allocation Technique was incepted within the fall of 2001. Benchmark Agnostic portfolio represents the portfolio proposed to purchasers within the fall of 1999.

1Consists of GMO’s Sources and Local weather Change methods.

2Complete allocation to Fairness Dislocation is eighteen.9% inclusive of publicity inside Different Allocation.

3The headline publicity to U.S. Treasury Notes shouldn’t be thought-about in isolation of the portfolio’s total period profile inclusive of collateral and different exposures.

The above data relies on a consultant account within the technique chosen as a result of it has the fewest restrictions and greatest represents the implementation of the technique. Weightings are as of the date indicated and are topic to alter. The teams indicated above symbolize exposures decided pursuant to proprietary methodologies and are topic to alter over time.

The 2000 Web Bubble

In 2000, our main multi-asset portfolio was a balanced technique with outlined allowable ranges round benchmark weights.

We have been 32% underweight U.S. massive cap shares, 14% chubby a mix of U.S. small worth and REITs, impartial on worldwide developed shares, 5% chubby rising market equities, and 12% chubby mounted earnings. We have been torn by the truth that we have been taking loopy quantities of monitoring error versus the benchmark whereas additionally losing 15% of our portfolio on U.S. massive cap shares, which we believed provided the worst threat/reward trade-off on the planet on the time. Within the fall of 1999, that pressure prompted us to speak to purchasers about investing in a benchmark-free method wherein we might by no means maintain property solely to regulate monitoring error relative to a benchmark.

We weren’t employed to run a reside benchmark-free portfolio till the autumn of 2001, however we’ve labeled the portfolio we believed to be acceptable on the time for buyers who cared extra about incomes actual returns than monitoring error “Benchmark Agnostic.” Our Benchmark-Agnostic portfolio had 40% of its allocation in dangerous property, cut up between REITs, rising fairness, and rising debt. The opposite 60% was in TIPS (50%) and U.S. investment-grade bonds (10%).

2007-8 Every part Bubble

By the point the subsequent bubble took place, we had transitioned quite a few our asset allocation purchasers to benchmark-free portfolios. We had moved to a really defensive portfolio by mid-2007 and continued taking threat off the desk by the summer season of 2008, culminating within the August 2008 portfolio we’ve labeled “2007-8 Every part Bubble,” proven in Exhibit 5.

2008 marked our lowest ever allocation to shares (all of which have been invested within the GMO High quality Technique) and our highest allocation to money and liquid alternate options. We additionally had a wholesome allocation to bonds.

2021 Length Bubble

By the tip of 2021, we got here near matching our 2008 low level in fairness allocation and exceeded our 2008 allocation to various methods.

Between fairness lengthy/brief and different alternate options, non-traditional short-duration methods made up 60% of the portfolio. Moreover, about half of the credit score allocation was to floating fee securities, which additionally had successfully no rate of interest period. We’ve labeled that portfolio “2021 Length Bubble.”

2025 AI Bubble

In the present day, we consider GMO’s Benchmark-Free Technique has a powerful anticipated return regardless of the AI Bubble, largely by advantage of proudly owning shares which have little or nothing to do with that theme.

Present allocations are about 50% shares, 28% liquid alternate options, and 20% Treasuries. Given our present forecasts, our Benchmark-Free portfolio has an anticipated return of 6.5% actual23 (if our forecasts are spot on) versus 0.2% actual for a 60% MSCI ACWI/40% Bloomberg U.S. Combination Bond portfolio. If every part seems regular regardless of appearances, the portfolio has an anticipated return of 4.5% actual, consistent with the 60/40 benchmark if it, too, proves regular.

Regardless of having rather less than half of its weight in equities, this portfolio has risen 17.9% in 2025,24 greater than 4.5% forward of a 60% MSCI World/40% Bloomberg U.S. Combination Bond portfolio and 4.1% forward of the S&P 500. Even though AI seems like the one funding story anybody cares about, non-U.S. shares, notably deep worth shares, have considerably outpaced the S&P 500 this yr. To date, it has not been essential to lean into the AI commerce to attain robust returns. Even when the AI Bubble continues to inflate for some time longer, it’s completely believable that this development continues. A rising tide needn’t solely elevate the most costly boats.

1On Robert Shiller’s Complete Return CAPE, the S&P 500 is buying and selling above its 1929 and 2021 peaks and is about 13% decrease than the 2000 peak. On normal CAPE, it’s nearer nonetheless to the 2000 peak. On value/gross sales and value/e-book, it’s at an all-time excessive.

2Pondering Machines raised $2 billion earlier this yr at a $10 billion valuation, apparently with out telling buyers what their plan was. Admittedly, they appear to have provide you with one since then, and buyers should assume it’s one, given they’re elevating capital at a $50 billion valuation about three months later. Should be one hell of a plan.

3AMD rose 24% the day it introduced their association with OpenAI, and Oracle leapt 36% upon the announcement of theirs.

4Whereas Palantir trades at 120 occasions gross sales, virtually actually larger than some other megacap firm in historical past, Rigetti Computing and D-Wave Quantum commerce at 1007 and 318 occasions gross sales, respectively. As these two firms are instantly competing with Microsoft, Alphabet, IBM, and different extraordinarily deep-pocketed firms within the nascent quantum computing area, it reveals virtually touching religion by buyers to imagine they’ll one way or the other wind up the winners if quantum computing ever quantities to something.

5The diploma of “this time is completely different” is really next-level this time round. The inimitable Matt Levine identified in his October 15 column “OpenAI Has a Enterprise Plan” that Sam Altman successfully mentioned in an interview that their marketing strategy was, “We’ll create God after which ask it for cash.” Mark Zuckerberg additionally not too long ago mentioned on the ACCESS podcast that they’d slightly threat misspending a pair hundred billion {dollars} than threat lacking out on being first to superintelligence.

6For a superb e-book on bubbles, we advocate “Satan Take the Hindmost” by our former colleague, Edward Chancellor. His new e-book, co-written with Jeremy Grantham and popping out this January, “The Making of a Permabear,” is nicely price a learn too!

7The “Nifty 50” period of the early Seventies was actually a bubble in massive cap progress shares relative to small cap worth shares, however the total U.S. inventory market was considerably cheaper on the peak of the Nifty 50 in 1972 than it had been within the mid-Nineteen Sixties, and the valuation peak of the Nineteen Sixties was considerably decrease than what had been reached in 1929.

8Whereas the fundamental thought behind our asset class forecasts has been constant since we began publishing them in 1994, some particulars have modified with time. It’s price noting that in 2000, we assumed property would take 10 years to revert to truthful worth. Beginning in 2003, we modified this assumption to 7 years. Starting within the mid-2010s, we additionally started considering a number of situations of equilibrium rates of interest.

9You possibly can have accomplished even higher by biasing your portfolio towards the worth half of these teams, given worth shares have been buying and selling at their widest-ever reductions to the market.

10Whereas we had began speaking to purchasers about investing in a benchmark-free method within the fall of 1999, we didn’t get our first consumer within the technique till the autumn of 2001. The paper portfolio of our suggestions would have accomplished even higher than the World Asset Allocation Technique we have been operating on the time.

11The particular benchmark was 48.75% S&P 500/16.25% MSCI ACWI ex-U.S./35% Bloomberg U.S. Combination Bond. Nearly all our purchasers on the time had a major residence bias to their fairness portfolios.

12It’s In every single place, in Every part: The First Really World Bubble (Grantham 2007).

13Equities, REITs, and rising debt.

14Money, TIPS, and U.S. and worldwide authorities bonds.

15Within the spirit of full disclosure, though we had written a number of items warning buyers about each a inventory bubble and the issue of excessively low bond yields on the time, we had but to label it a “period” bubble in print. See Authorities Bonds Have Given Us So A lot, Do They Have Something Left to Give? (Inker 2020), Hypothesis and Funding: Why In the present day’s Highfliers Are so More likely to Fall Again to Earth (Inker 2021); and Let the Wild Rumpus Start: (Approaching the Finish of) The First U.S. Bubble Extravaganza (Grantham 2022).

16By this level, we have been explicitly contemplating a number of situations for incorporating equilibrium rates of interest into our forecasts, and this chart is the weighted common of these situations. If we had solely been making the valuation assumptions we made in 2000 or 2007, the forecasts would have been much more unfavourable, and the slope of the regression line would have been unfavourable.

17Whereas buyers are extra used to eager about the period of mounted earnings devices than property with variable money flows, it’s simple to elucidate why equities and actual property are longer period than conventional bonds. Whereas a bond has a maturity date, equities and actual property are perpetuities. Past that truth, their money flows develop with inflation, which suggests anticipated money flows, even within the pretty distant future, have a significant contribution to their current worth. And simply as with bonds, the decrease the yield on these property, the upper the period will get.

182021 was additionally an utter nightmare for threat parity portfolios. Whereas threat parity portfolios provide ostensible diversification throughout a wide range of dangers, the one threat they inherently lean closely into is period threat—precisely the unsuitable name in a period bubble.

19Whereas 14% is greater than half of 26%, a 14% loss requires a ~16% achieve to regain the loss, whereas a 26% loss requires a ~35% achieve–greater than twice as a lot.

20As of November 18, 2025, a 60% MSCI ACWI/40% Bloomberg U.S. Combination bond portfolio has returned +6.8% because the finish of 2021 vs. our Benchmark-Free Allocation Technique’s return of +20.8%, web of charges, for a similar interval.

21The truth that AI really does look like a technological breakthrough actually doesn’t imply it will probably’t be a bubble. The web was a breakthrough. Railroads and, earlier than them, canals have been breakthroughs. Traders appear to be notably vulnerable to overestimating the returns on investing in technological breakthroughs, not least as a result of they have an inclination to throw a lot cash at them that competitors decimates the return on capital on that funding.

22These anticipated returns are for U.S. dollar-based buyers and are a weighted common of the completely different equilibrium rate of interest situations we ponder.

23Assuming our methods carry out consistent with their benchmarks. Safety choice alpha would add to that return, besides within the case of liquid alternate options, the place we assume Fairness Dislocation will return 6% above money because of the vast unfold between worth and progress shares globally, and Different Allocation, the place we’re assuming 4% above money given a typically good alternative set.

24As of November 12, 2025.

Disclaimer: The views expressed are the views of Ben Inker by the interval ending November 2025 and are topic to alter at any time based mostly on market and different circumstances. This isn’t a proposal or solicitation for the acquisition or sale of any safety and shouldn’t be construed as such. References to particular securities and issuers are for illustrative functions solely and should not supposed to be and shouldn’t be interpreted as suggestions to buy or promote such securities.

Copyright © 2025 by GMO LLC. All rights reserved.

Editor’s Word: The abstract bullets for this text have been chosen by In search of Alpha editors.

[ad_2]