[ad_1]

First appeared at Coverage Heart for the New South

The heavy monetary sanctions on Russia after the invasion of Ukraine sparked speculations that the weaponization of entry to reserves in {dollars}, euros, kilos, and yen would spark a division within the worldwide financial order. China would are inclined to strengthen its personal worldwide funds system and speed up the institution of its foreign money – the Renminbi – as a rival reserve foreign money to cut back its vulnerability to strikes of the same nature towards it. Nations dealing with geopolitical dangers of their relationship with the USA and Europe would seize the chance to change out of the greenback system. Nonetheless, there’s a approach to go between prepared and doing on this case…

Final Thursday, the Worldwide Financial Fund (IMF) launched a examine (Arslanalp et al., 2022) on the evolution of worldwide reserves for the reason that starting of the century. The “greenback dominance” seems in its weight in international markets. The US greenback’s share of overseas commerce invoicing and worldwide debt issuance and non-banking transactions is properly above what the nation’s shares of worldwide commerce, worldwide bond issuance, and cross-border borrowing would counsel.

The greenback dominance remained regardless of the falling share of US GDP within the international financial system. From the Seventies onwards, it survived the top of gold convertibility and the mounted alternate charge regime inherited from Bretton Woods. Its presence in banking and non-banking transactions even grew after the 2007-08 international monetary disaster.

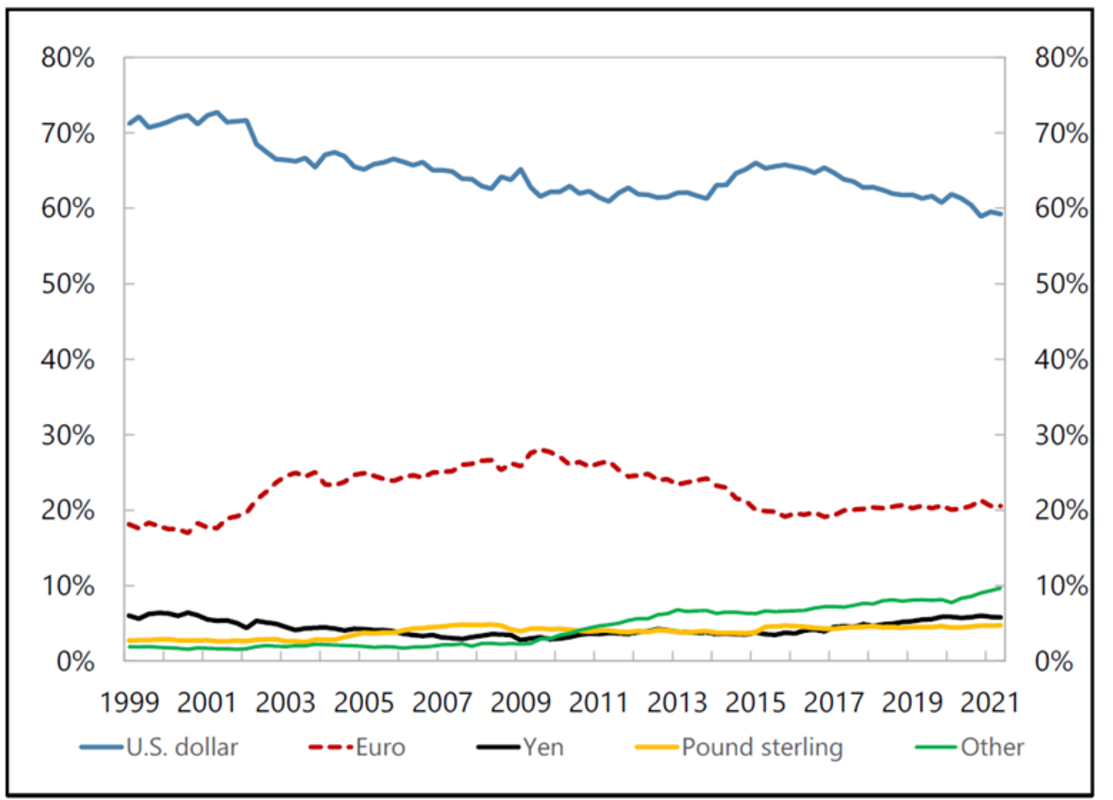

The IMF report exhibits a discount within the diploma of “dominance” with the greenback’s share of central financial institution reserves falling for the reason that starting of the century, down 12 proportion factors from 71% in 1999 to 59% final yr. Not in favor of the pound sterling, the Japanese yen, or the euro – regardless of the rise that the latter skilled throughout its first decade of existence (Determine 1). As an alternative, in favor of what the IMF’s work known as “non-traditional reserve currencies” (Australian greenback, Canadian greenback, Swiss, and others), together with the Renminbi, which reached 2.6% of the full.

Determine 1. Forex Composition of World International Alternate Reserves 1999–2021

(In %)

Supply: Arslanalp et al. (2022).

Observe: The “different” class accommodates the Australian greenback, the Canadian greenback, the Chinese language renminbi, the Swiss franc, and different currencies not individually recognized within the COFER survey. China turned a COFER reporter between 2015 and 2018.

4 gravitational components favor the continuation of the greenback’s central place in worldwide monetary markets, in commerce invoices and funds, and in private and non-private overseas alternate reserves – name it “community – complementarity and synergy – results.” The relative growth of the opposite currencies will depend on how efficiently they handle to offset these components.

First, the extra in depth put in base for dollar-denominated transactions favors the foreign money. The rise in liquidity and the discount in transaction prices within the “non-traditional” overseas alternate markets – together with technological enhancements in platforms – helped scale back this drawback.

As well as, no different financial system provides an equal quantity of “investment-grade” authorities bonds as the USA does. That quantity permits central banks to build up reserves and personal traders to make use of them as a “haven”, one thing strengthened by the “quantitative easing” for the reason that international monetary disaster. On this regard, the announcement by the then President of the European Central Financial institution, Mário Draghi, within the euro disaster in 2012 – that he would do “no matter it takes” as a last-resort supplier of liquidity for euro-denominated belongings issued within the eurozone – was essential. Moreover, the European Restoration Fund was created final yr. The worldwide provide of liquid and safe-haven belongings usable as central financial institution reserves tended to widen, in favor of the euro.

Third, it’s also value noting that “non-traditional currencies” have been favored by a partial seek for returns in reserve administration. Central financial institution steadiness sheets – of each superior and rising economies – have taken on monumental proportions in latest instances. Now, a few of them separate what could be the suitable tranche for “liquidity administration” (the rationale why there are reserves in liquid and low-risk belongings, with the aim of stabilization), from one other “funding tranche” (attainable to be allotted in much less liquid however extra worthwhile belongings). The seek for diversification helped “non-traditional” reserves.

The fourth gravitational in favor of the greenback could be the absence of laws limiting liquidity and asset availability, together with capital controls. Regardless of the sanctions already utilized in circumstances comparable to Iran, Venezuela, and Russia, there’s a issue right here for Chinese language bonds in comparison with these in {dollars} and the opposite three main currencies.

Because the international monetary disaster, China has sought to increase the usage of the Renminbi in worldwide commerce and as a reserve asset at different central banks. This was adopted by a proliferation of overseas alternate swap traces with different international locations.

Nonetheless, as we’ve got already famous right here, whereas commerce transactions and reserves by central banks and different international public traders could reinforce the Renminbi’s place as a substitute foreign money to the greenback, euro, yen, and pound sterling, the qualitative leap towards the internationalization of the Chinese language foreign money as a reserve foreign money will solely happen when confidence in its convertibility is adequate to persuade unofficial (personal) traders to maintain reserves denominated in it. It’s not by likelihood that the foreign money swap traces with China have been little used, whereas these of the international locations with the Federal Reserve have been activated in instances of have to stabilize flows.

The reserve issuer should settle for that giant quantities of its foreign money flow into the world and, due to this fact, that overseas traders have some weight in figuring out home long-term rates of interest and the alternate charge. By all indications, Chinese language monetary authorities don’t look like contemplating relinquishing controls as a precedence on the fast horizon. They are going to seemingly search to broaden the usage of the Renminbi to the extent that this may be carried out with out relinquishing controls and, due to this fact, with out the ambition to construct some parallel regime or substitute for the prevailing one.

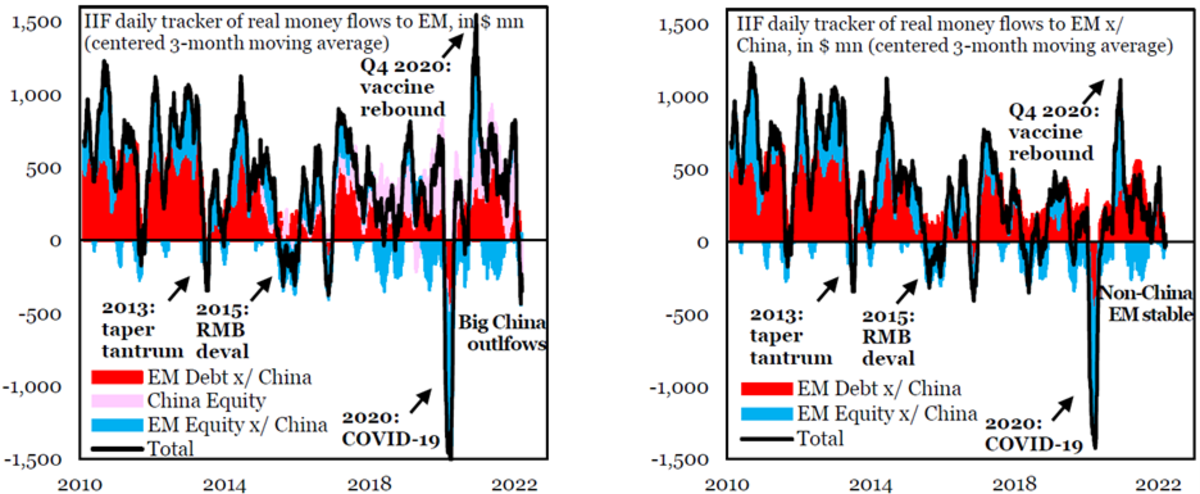

In latest weeks, portfolio overseas capital actions into China are illustrative of what’s at stake and the potential prices for China of dashing out of the prevailing regime. Knowledge launched by the Institute of Worldwide Finance (IIF) additionally final Thursday revealed an unprecedented giant outflow of portfolio (debt and equities) capital from China within the wake of the Russian invasion of Ukraine and sanctions. On the identical time, such flows remained steady in different rising economies (Determine 2). The timing means that it had some correlation not with home difficulties with the nation’s property sector or different causes however slightly with the conflict in Ukraine and sanctions. We don’t suppose it’s opportune for China to concern any indicators of a sudden departure from the system the place it at the moment operates, nor of a attainable collaboration with Russia to assist the latter circumvent the sanctions imposed on it.

Determine 2 – China sees giant outflows, whereas the remainder of EM is holding up.

Supply: IIF (2022).

The relative dominance of the greenback seems to be declining however at a really gradual tempo.

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]